Peltier Thermoelectric Cooler Devices Market Insights

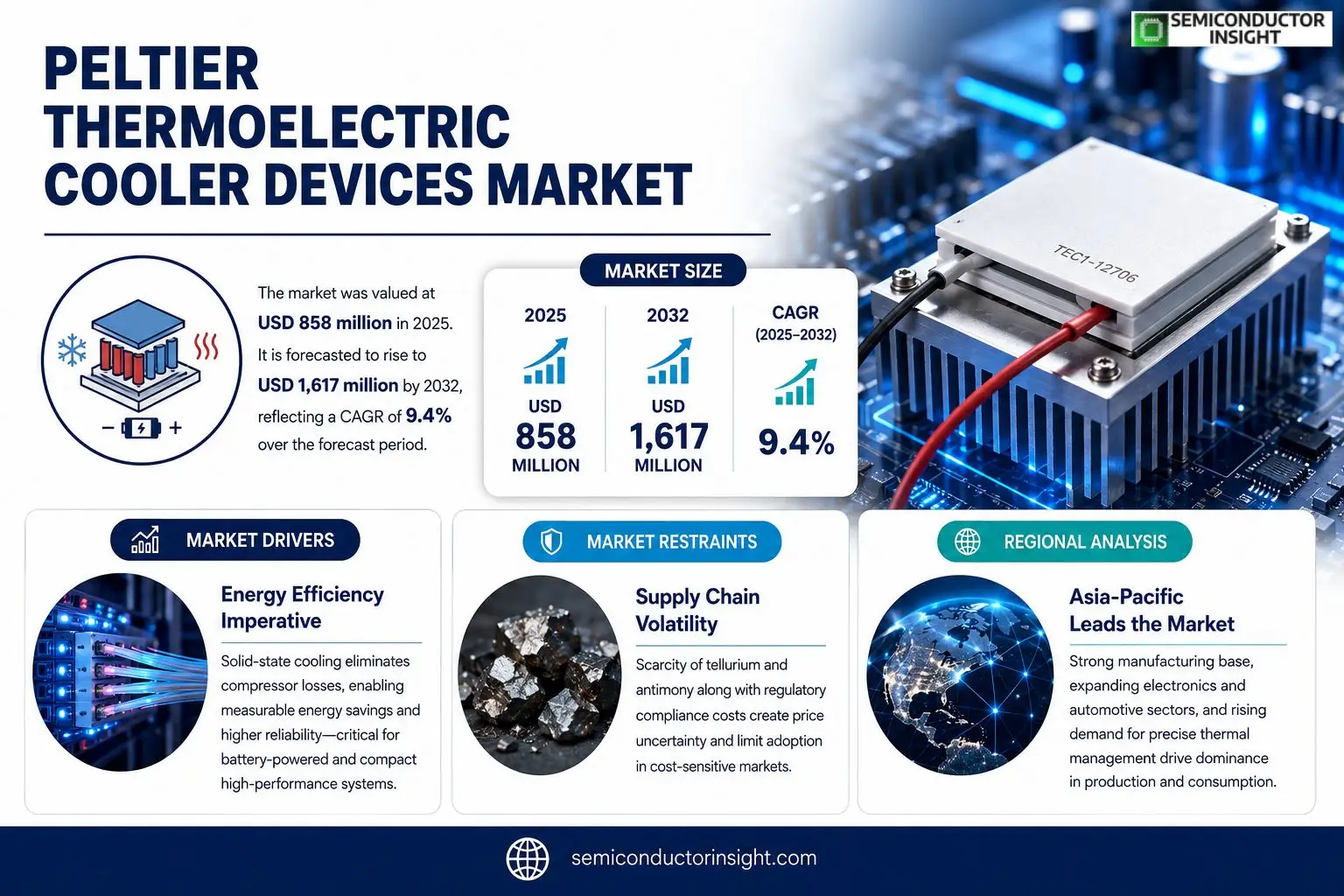

Peltier Thermoelectric Cooler Devices market was valued at USD 858 million in 2025. It is forecasted to rise to USD 1,617 million by 2032, reflecting a compound annual growth rate of 9.4 % over the period.

A Peltier Thermoelectric Cooler Device is a solid‑state thermal management component that exploits the Peltier effect for active cooling and precise temperature regulation. The module typically integrates multiple pairs of p‑type and n‑type semiconductor elements, ceramic substrates, electrodes and thermal interface structures; when direct current passes through, one side absorbs heat while the opposite side dissipates it.Demand acceleration stems from expanding use cases such as optical communication modules, laser systems, semiconductor manufacturing equipment, medical diagnostics instruments and automotive thermal management solutions. Customers increasingly prefer these devices because they offer compact form factors, rapid response times and refrigerant‑free operation, enabling higher reliability in environments where vibration or moving parts are undesirable.

MARKET DRIVERS

Energy Efficiency Imperative

Manufacturers across consumer electronics and industrial automation are prioritising power‑savvy thermal solutions. Peltier Thermoelectric Cooler Devices Market benefits from the fact that solid‑state coolers eliminate compressor‑related standby losses, enabling system‑level energy savings that can be quantified in annual operating costs. This efficiency advantage is especially compelling for battery‑powered equipment where every watt counts.

Miniaturization and System Integration

The relentless push toward smaller form‑factors in wearables, edge‑computing nodes, and telecom gear has amplified demand for compact cooling. Peltier modules, with thicknesses measured in millimetres, can be mounted directly onto heat‑generating components, reducing thermal resistance and simplifying assembly. Integrating thermoelectric devices at the board level shortens time‑to‑market for high‑density products.

➤ Industry analysts note that the shift toward solid‑state cooling is redefining thermal‑management portfolios, prompting OEMs to allocate larger R&D budgets toward thermoelectric research.

Collectively, these dynamics are prompting strategic investments in material engineering and module design, positioning Peltier Thermoelectric Cooler Devices Market to capture a larger share of the overall cooling solutions landscape.

MARKET CHALLENGES

Thermal Performance Limits

While solid‑state coolers excel in size and reliability, their temperature‑drop capability remains lower than that of conventional compressors, particularly under high‑heat‑flux conditions. End‑users in heavy‑duty refrigeration or high‑power laser cooling often find the achievable ΔT insufficient, prompting them to retain hybrid approaches rather than fully transition to thermoelectric technology.

Other Challenges

Cost Competitiveness

The price premium associated with high‑purity bismuth‑telluride alloys and precise assembly processes keeps unit costs above those of traditional cooling methods. OEMs evaluating total cost of ownership must weigh the upfront expense against long‑term reliability gains, a calculation that can stall adoption in price‑sensitive markets.

MARKET RESTRAINTS

Supply Chain Volatility

Raw‑material scarcityparticularly for tellurium and antimonyhas introduced price fluctuations that ripple through the manufacturing pipeline. Recent geopolitical shifts have accentuated the risk of supply interruptions, prompting several producers to re‑evaluate inventory strategies and consider secondary sourcing.Regulatory frameworks such as RoHS and REACH impose strict limits on heavy‑metal content, requiring additional certification steps for thermoelectric modules destined for European markets. Compliance costs can erode margins for smaller players, consolidating market power among established manufacturers.Finally, the relative novelty of thermoelectric cooling among many engineering teams translates into a learning curve. Without clear design guidelines, some OEMs defer integration, limiting market penetration despite the technology’s attractive attributes.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicles

Thermal management of battery packs and power electronics in electric vehicles is increasingly relying on solid‑state solutions to address localized hot‑spots without adding moving parts. Peltier devices can be strategically placed to balance cell temperatures, extending cycle life and supporting fast‑charging protocols.Medical diagnostics and portable imaging equipment present another growth frontier. The need for quiet, vibration‑free cooling in field‑deployed devices dovetails with the silent operation of thermoelectric modules, enabling new product categories such as handheld PCR units.Strategic collaborations between semiconductor manufacturers and automotive suppliers are launching joint development programmes focused on integrated thermoelectric‑heat‑sink packages. These alliances not only accelerate technology validation but also create a pipeline of customized solutions that can be rapidly scaled.

Peltier Thermoelectric Cooler Devices Market Trends

Shift Toward High‑Precision Thermal Management

The supply side is increasingly bifurcated. Japanese and European firms retain control of premium‑grade bismuth‑telluride alloys and ultra‑reliable module assembly, while Chinese manufacturers scale capacity for standard‑grade products. This structural split lets end‑users choose between cost‑effective volume parts and high‑reliability modules that meet stringent cycle‑life specifications. For OEMs of laser‑based communication gear and medical analyzers, the reliability premium justifies a higher unit price, whereas consumer‑electronics makers gravitate toward the lower‑cost Chinese output. The divergence is reinforced by profit margins that still hover between 30 % and 40 % for well‑engineered devices, indicating that even commodity‑type production can sustain healthy earnings when scale is sufficient.

Other Trends

Material Supply Chain Consolidation

Upstream inputs such as bismuth telluride, copper‑clad laminates and extrusion‑aluminum sheets remain concentrated among a handful of suppliersFurukawa, Rogers, and ESPI Metals dominate the high‑purity segment, while firms like Shanghai Vital and ABSCO Limited serve the broader market. Recent negotiations between Japanese material producers and Chinese module assemblers have reduced lead times for standard parts, yet quality audits for aerospace and defense programs still require certification from the original high‑grade sources. This dual‑track sourcing strategy mitigates risk for Peltier Thermoelectric Cooler Devices Market while preserving a premium niche for firms that can guarantee material consistency across large batches.

Application Diversification and System Integration

Demand is no longer confined to generic cooling of small appliances. Automotive thermal managementparticularly battery‑temperature regulation and seat‑comfort systemshas emerged as a visible growth vector, exemplified by a recent module that lifted heat‑absorption capacity by over 20 %. Simultaneously, the rollout of 800 Gb/s optical networking and AI‑accelerated servers drives a need for compact, low‑vibration cooling that can be integrated directly onto photonic chips. Companies such as Coherent and Phononic are bundling TEC modules with cold plates, liquid‑flow controllers and smart drivers, turning a standalone cooler into a subsystem. This shift compels system integrators to evaluate total‑cost‑of‑ownership rather than per‑unit price, creating opportunities for firms that can offer validated, end‑to‑end solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics and market structure in the Peltier Thermoelectric Cooler Devices sector

Ferrotec remains the benchmark for high‑performance modules, leveraging its Japanese heritage in bismuth‑telluride processing and a service network that satisfies automotive OEMs and aerospace integrators alike. The company’s ability to couple material consistency with long‑cycle reliability gives it a decisive edge in premium applications such as laser cooling and AI‑server thermal management. Parallel to Ferrotec, European firms like KELK and Kyocera dominate the niche where ultra‑low vibration and stringent certification are non‑negotiable, reinforcing a tiered market where high‑margin bespoke solutions coexist with volume‑driven offerings.Chinese manufacturers, exemplified by Guangdong Fuxin Technology, Zhejiang Wangu Semiconductor, and TE Technology, have accelerated capacity expansion, targeting standard and micro‑TEC segments that feed consumer electronics and telecom infrastructure. These players benefit from domestic raw‑material supply chains and policy incentives that lower cost structures, enabling them to capture price‑sensitive contracts while progressively advancing toward higher‑reliability portfolios. Smaller specialized firms such as ARCTIC TEC, Phononic, and Tark Thermal Solutions enrich the ecosystem with system‑level integrationscold‑plate assemblies, liquid‑coupled modules, and intelligent controllersthereby broadening the value chain beyond discrete devices.

List of Key Peltier Thermoelectric Cooler Devices Companies Profiled

- Ferrotec Corp.

- KELK Ltd.

- Kyocera

- Coherent Corp.

- Phononic Ltd.

- Tark Thermal Solutions

- Guangdong Fuxin Technology

- ARCTIC TEC

- TE Technology

- Zhejiang Wangu Semiconductor

- Xi’an Oriental Electronic

- Thermion Company

- Thermoelectric New Energy Technology

- Beijing Xinyu Kaimeng Electronic Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single-stage devices are favored for applications requiring compact form factor and rapid response. Their simplicity supports reliable manufacturing and easier integration into consumer‑grade products.

|

| By Application |

|

Optical communication modules lead the application landscape because they demand ultra‑stable thermal environments for high‑speed data transmission. The solid‑state nature of Peltier devices eliminates vibration, supporting stringent performance criteria.

|

| By End User |

|

Medical and laboratory instruments dominate the end‑user profile as they require absolute temperature stability and minimal mechanical disturbance. The reliability of solid‑state cooling underpins critical diagnostic and analytical processes.

|

| By [Segment Category 3]] |

|

Emerging integration solutions are gaining attention as manufacturers seek holistic thermal management that combines Peltier modules with cold plates and active controllers. The trend reflects a shift toward turnkey cooling architectures.

|

| By [Segment Category 4]] |

|

High‑reliability aerospace applications benefit from the vibration‑free operation and deterministic temperature control of thermoelectric coolers. Their adaptability to extreme environments makes them a strategic component in next‑generation avionics.

|

Regional Analysis: Peltier Thermoelectric Cooler Devices Market

North America

The region hosts an integrated network of silicon wafer fabs and specialty alloy producers, allowing rapid prototyping of custom Peltier modules. Partnerships between university labs and mid‑size manufacturers accelerate technology transfer, resulting in a pipeline of higher‑performance devices that keep North American firms ahead of rivals.

Precision cooling for photonics testing and cryogenic medical imaging drives demand for compact thermoelectric solutions. These high‑value niches justify premium pricing and support a steady flow of orders that fund further innovation.

Energy‑Star and EPA efficiency guidelines indirectly promote thermoelectric cooling, as manufacturers seek to meet low‑power targets without compromising performance, creating a subtle but persistent market pull.

A handful of legacy firms dominate volume production, yet a surge of start‑ups focusing on niche applications fragments the landscape, fostering a competitive environment that rewards agility and specialized expertise.

Europe

European manufacturers leverage stringent environmental standards to position thermoelectric coolers as low‑impact alternatives to vapor‑compression units. The automotive sector, especially in Germany and France, experiments with Peltier devices for battery‑thermal‑management, anticipating future electric‑vehicle architectures. Meanwhile, research institutions in the Nordics develop thin‑film technologies that could lower material costs, offering a pathway for broader adoption across consumer electronics. The region’s collaborative innovation ecosystems enable cross‑border projects that accelerate time‑to‑market for next‑generation solutions.

Asia‑Pacific

Asia‑Pacific balances massive consumer demand with a burgeoning industrial base. In China, rapid expansion of data‑center capacity fuels interest in solid‑state cooling for high‑density server racks, while Japanese firms invest heavily in precision instrumentation that requires stable temperature control. Indian start‑ups are targeting portable refrigeration for agricultural supply chains, illustrating how local market needs shape product development. The diversity of end‑uses across the sub‑region creates a resilient demand foundation for thermoelectric technologies.

South America

South American countries are exploring thermoelectric cooling to address logistics challenges in remote areas where conventional refrigeration is impractical. Brazil’s agribusiness sector, for instance, sees value in compact coolers for transporting perishable produce across vast distances. Local manufacturers are beginning to assemble modules using imported semiconductor materials, gradually building domestic capabilities. Government incentives for energy‑efficient equipment provide a modest boost, encouraging early adopters to experiment with solid‑state solutions.

Middle East & Africa

In the Middle East, extreme ambient temperatures create a niche for thermoelectric coolers in electronic enclosures and medical storage, where reliability under heat stress is paramount. African markets, particularly South Africa and Kenya, view thermoelectric devices as a low‑maintenance option for off‑grid refrigeration in rural health clinics. Partnerships with multinational distributors are facilitating technology transfer, while regional trade shows highlight the growing awareness of solid‑state cooling as a viable alternative to traditional compressors.

Report Scope

This market research report provides a comprehensive analysis of the Peltier Thermoelectric Cooler Devices Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Peltier Thermoelectric Cooler Devices Market?

-> Peltier Thermoelectric Cooler Devices Market was valued at USD 858 million in 2025 and is expected to reach USD 1,617 million by 2032 with a CAGR of 9.4% during the forecast period.

Which key companies operate in Peltier Thermoelectric Cooler Devices Market?

-> Key players include Ferrotec, KELK Ltd., Kyocera, Coherent Corp, Tark Thermal Solutions, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, KJLP, Thermion Company, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high‑precision temperature control in optical communication and laser modules, automotive battery and seat thermal management, AI‑driven data‑center cooling, and the shift toward solid‑state cooling solutions with higher heat‑flux density and reliability.

Which region dominates the market?

-> Asia (particularly China) dominates in production volume and market share, while Japan and Europe retain leadership in high‑end material technology and reliability‑focused applications.

What are the emerging trends?

-> Emerging trends include integration of cold‑plate and liquid‑cooling hybrids, multi‑stage TEC modules for higher heat‑absorption, system‑level thermal‑management platforms for AI servers and 800G/1.6T optical networking, and the expansion of automotive thermal‑management applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...