Thermoelectric Cleaner Assemblies Market Insights

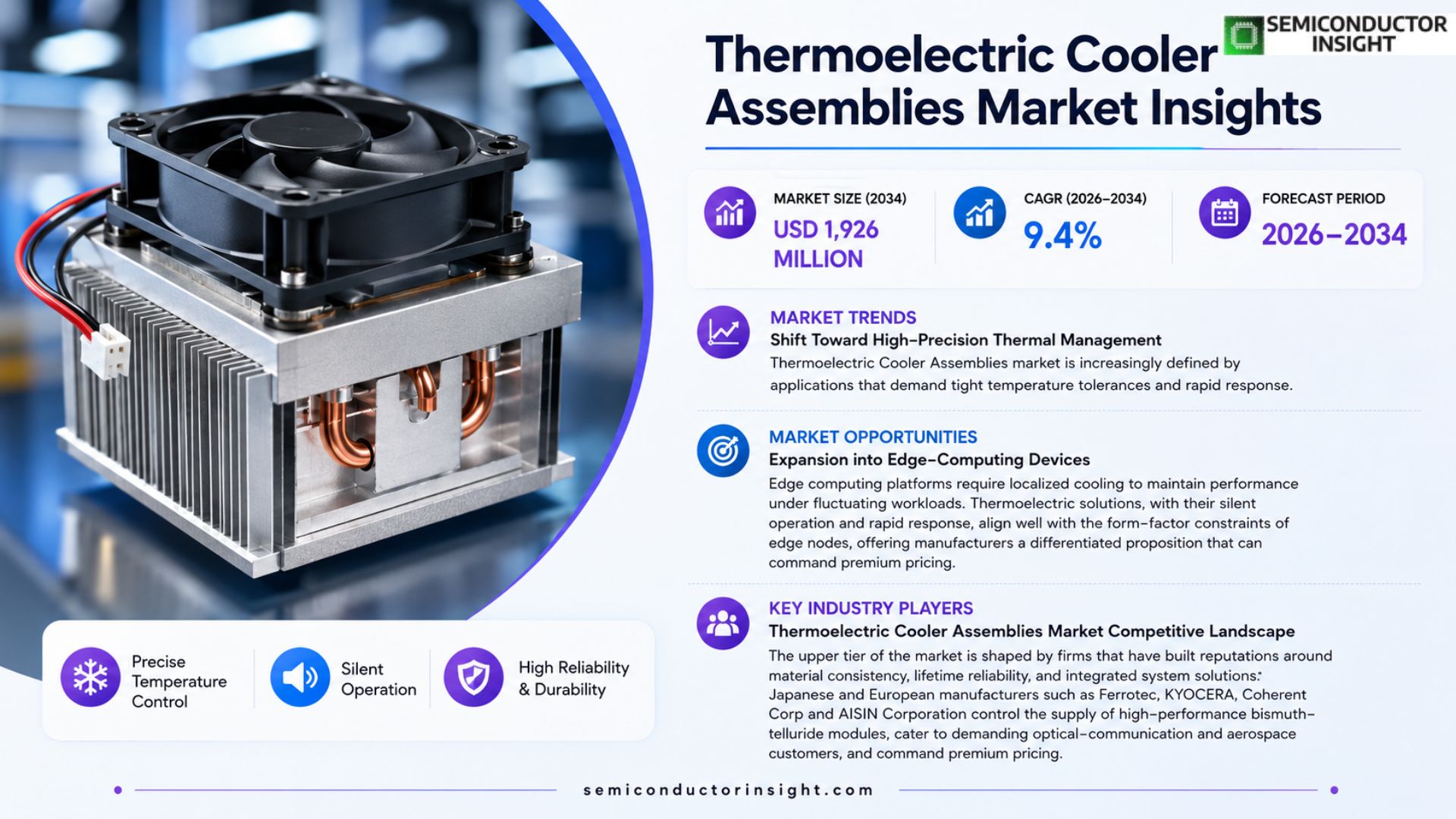

Thermoelectric Cooler Assemblies market was valued at USD 858 million in 2025 and may rise to roughly USD 1,926 million by 2034, reflecting an implied compound annual growth rate of about 9.4 % over the period.

A Thermoelectric Cooler Assembly is a solid‑state thermal‑management device that exploits the Peltier effect to deliver active cooling and precise temperature control without moving parts or refrigerants. It typically comprises alternating P‑type and N‑type semiconductor elements bonded between ceramic substrates together with electrodes and thermal‑interface structures; when direct current passes through, one side absorbs heat while the opposite side dissipates it.

This technology serves optical communication modules, laser systems, semiconductor equipment, medical instruments, automotive thermal management, consumer electronics, industrial sensors and aerospace electronics because it provides compactness, fast response time and reversible heating‑cooling capability.

MARKET DRIVERS

Rising Demand for Energy‑Efficient Cooling

Thermoelectric Cooler Assemblies Market is gaining traction as manufacturers in consumer electronics and automotive sectors seek solutions that cut power consumption while delivering precise temperature control. This shift is propelled by stricter efficiency standards and the growing preference for solid‑state devices that eliminate moving parts, thereby lowering maintenance overhead.

Advances in Semiconductor Materials

Recent breakthroughs in bismuth‑telluride alloys and nanostructured modules have pushed the coefficient of performance to levels previously attainable only by traditional refrigeration. These material improvements expand the feasible application range, allowing designers to embed thermoelectric modules in compact spaces such as wearable health monitors and electric vehicle battery packs.

➤ “Customers are now evaluating total cost of ownership rather than upfront price, and thermoelectric solutions are delivering measurable savings over the product lifecycle.”

Consequently, OEMs are revising bill‑of‑materials strategies to prioritize thermoelectric assemblies, a move that reshapes supplier negotiations and catalyzes further R&D investment across the value chain.

MARKET CHALLENGES

Thermal Management Complexity in High‑Power Systems

While thermoelectric technology offers precise temperature regulation, integrating these modules into high‑power environments,such as data‑center cooling or aerospace avionics,introduces design complications. Engineers must address heat‑sink sizing, voltage control loops, and reliability under thermal cycling, which can extend development timelines and inflate costs.

Other Challenges

Supply‑Chain Vulnerabilities

The reliance on rare‑earth elements for high‑efficiency modules ties Thermoelectric Cooler Assemblies Market to geopolitical fluctuations and mining constraints, creating bottlenecks that can delay product launches.

MARKET RESTRAINTS

Higher Initial Capital Outlay

Compared with conventional vapor‑compression systems, thermoelectric assemblies carry a premium price tag due to specialized semiconductor processing. For price‑sensitive segments, such as mass‑market appliances, the cost disparity hampers rapid adoption and limits market penetration despite the long‑term energy benefits.

MARKET OPPORTUNITIES

Expansion into Edge‑Computing Devices

Edge computing platforms require localized cooling to maintain performance under fluctuating workloads. Thermoelectric solutions, with their silent operation and rapid response, align well with the form‑factor constraints of edge nodes, offering manufacturers a differentiated proposition that can command premium pricing.

Thermoelectric Cooler Assemblies Market Trends

Shift Toward High‑Precision Thermal Management

Thermoelectric Cooler Assemblies Market is increasingly defined by applications that demand tight temperature tolerances and rapid response. Optical‑communication modules, semiconductor test equipment, and advanced automotive battery systems now account for a growing share of orders because their performance hinges on millikelvin stability. Manufacturers are responding with designs that emphasize low thermal resistance, high heat‑flux capability, and extended cycle life. This move away from generic consumer cooling toward niche, value‑added segments improves per‑unit margins,often in the 30‑40% range,and creates space for differentiated pricing based on reliability certifications.

Other Trends

Supply‑Chain Realignment and Regional Competitive Dynamics

From a supply perspective, the industry displays a clear geographic split: Japan and Europe continue to dominate the high‑end material tier, supplying bismuth‑telluride alloys and precision‑grade laminates. Meanwhile, Chinese firms have scaled single‑line capacities to between 500,000 and 1,000,000 units, leveraging local copper‑clad laminates and extrusion processes to undercut price points. This dual‑track structure forces downstream customers,such as telecom equipment makers and medical device OEMs,to balance material consistency with cost efficiency. In the short term, original equipment manufacturers favour established suppliers for critical batches, but medium‑term forecasts suggest Chinese players will capture a larger share of standard‑grade orders, pressing incumbents to streamline logistics and offer more flexible delivery windows.

Integration of System‑Level Thermal Solutions

The final trend reshaping Thermoelectric Cooler Assemblies Market is the migration from standalone modules to integrated cooling subsystems. Recent product launches combine TECs with cold plates, liquid‑circulation loops, and intelligent temperature‑control electronics, enabling end‑users to address total‑system heat removal rather than isolated hotspots. This approach aligns with the rise of AI‑driven data‑center servers and high‑density photonic interconnects, where power densities exceed 100 W per square centimeter. By bundling components, suppliers can lock in longer service contracts and differentiate on engineering support, while customers benefit from reduced footprint and simplified validation. The net effect is a more resilient value chain that rewards firms capable of delivering turnkey thermal‑management platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Thermoelectric Cooler Assemblies Market Competitive Landscape

The upper tier of the market is shaped by firms that have built reputations around material consistency, lifetime reliability, and integrated system solutions. Japanese and European manufacturers such as Ferrotec, KYOCERA, Coherent Corp and AISIN Corporation control the supply of high‑performance bismuth‑telluride modules, cater to demanding optical‑communication and aerospace customers, and command premium pricing. Their dominance reflects deep R&D pipelines, stringent quality certifications, and longstanding relationships with OEMs that require low‑cycle‑life variance. Meanwhile, a growing cadre of Chinese companies is expanding capacity for standard‑grade TECs, leveraging lower labor costs and government incentives to offer volume‑oriented pricing. This dual‑track structure forces downstream buyers to balance cost efficiency against the need for ultra‑stable temperature control, creating a segmentation where high‑end applications remain anchored to legacy players while broader industrial adoption leans toward emerging Chinese suppliers.

Beyond the headline names, a set of specialized manufacturers enriches the competitive fabric. ARCTIC TEC and Guangdong Fuxin Technology focus on compact modules for consumer electronics and gaming rigs, emphasizing rapid thermal response. Z‑MAX and Zhejiang Wangu Semiconductor have carved niches in automotive seat‑heating and battery‑thermal‑management segments, where integration with vehicle control units is critical. Companies such as Xianghe Oriental Electronic and Thermonamic Electronics provide customized packaging for medical diagnostics, delivering tailored ceramic substrates that meet stringent sterility standards. This diversity of focused players increases resilience in the supply chain and offers customers a broader palette of performance‑cost trade‑offs, especially as emerging applications like AI‑accelerated photonics demand ever‑tighter thermal budgets.

List of Key Thermoelectric Cooler Assemblies Companies Profiled

- Ferrotec

- Kyocera

- Coherent Corp

- AISIN Corporation

- Phononic

- ARCTIC TEC

- Guangdong Fuxin Technology

- Z‑MAX

- Zhejiang Wangu Semiconductor

- Xianghe Oriental Electronic

- Thermonamic Electronics

- KELK Ltd. (Komatsu)

- Tark Thermal Solutions

- Same Sky (formerly CUI Devices)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi‑stage Type is emerging as the preferred architecture for high‑precision temperature control.

|

| By Application |

|

Communication & Data‑Center applications are gaining traction as the leading growth engine.

|

| By End User |

|

Medical Device Makers prioritize reliability and precision.

|

| By Package Geometry |

|

Custom‑shaped packages are becoming pivotal for niche high‑performance applications.

|

| By Cooling Capacity |

|

Above 100 W segment is gaining relevance for emerging high‑heat‑flux scenarios.

|

Regional Analysis: Thermoelectric Cooler Assemblies Market

Europe

The European ecosystem links high‑grade silicon wafer manufacturers with niche assemblers, creating a vertically integrated value chain that shortens time‑to‑market. Collaborative R&D agreements between material suppliers and OEMs allow rapid adjustment to emerging thermal‑performance specifications.

EU directives on refrigerant‑free cooling drive adoption of thermoelectric solutions, especially in medical and food‑preservation equipment. Compliance testing frameworks have become more rigorous, rewarding firms that embed traceability and lifecycle assessments.

Medical diagnostics, electric‑vehicle power‑modules, and high‑end portable electronics dominate demand. Each segment values the silent operation and precise temperature regulation that thermoelectric assemblies uniquely provide.

Research consortia are exploring nanostructured thermoelectric materials that promise higher efficiency at lower cost, a development that could broaden adoption beyond premium niches.

North America

In North America, Thermoelectric Cooler Assemblies Market is shaped by a competitive landscape where large‑scale semiconductor players intersect with agile start‑ups targeting niche applications. The United States’ defense‑grade requirements for reliable thermal management have spurred early adoption in aerospace, while Canada’s focus on sustainable building technologies fuels interest in solid‑state cooling for HVAC retrofits. Market participants benefit from a well‑established venture‑capital ecosystem that funds next‑generation module designs, encouraging rapid iteration. However, fragmented regulatory standards across states can complicate product qualification, prompting manufacturers to adopt flexible certification strategies that satisfy both federal and regional mandates.

Asia‑Pacific

Asia‑Pacific presents a dynamic mix of volume‑driven demand and emerging technological capability. Nations such as China, Japan, and South Korea invest heavily in consumer‑electronics and electric‑vehicle platforms where compact cooling is essential. While cost considerations dominate procurement decisions, rising awareness of energy‑saving technologies is nudging OEMs toward thermoelectric options despite higher unit prices. Local supplier networks provide abundant raw materials, yet the region’s reliance on imported high‑purity semiconductor wafers introduces supply‑chain sensitivities that firms mitigate through strategic stockpiling and regional fabrication partnerships.

South America

South American markets are gradually recognizing the benefits of thermoelectric cooling, especially within the agricultural sector where precise temperature control extends produce shelf‑life. Brazil’s expanding pharmaceutical manufacturing base requires reliable cold‑chain components, prompting local assemblers to collaborate with European technology partners. Infrastructure constraints and variable power quality pose operational challenges, encouraging designers to integrate robust thermal‑management algorithms that can tolerate voltage fluctuations without compromising performance.

Middle East & Africa

In the Middle East & Africa, Thermoelectric Cooler Assemblies Market is still nascent but poised for acceleration as data‑center expansion and renewable‑energy projects demand efficient heat‑rejection solutions. Harsh ambient temperatures drive interest in solid‑state coolers that can function without refrigerants, aligning with regional sustainability goals. Limited local manufacturing capacity has led many operators to import fully assembled modules, yet emerging industrial zones in the UAE and South Africa are attracting joint‑venture facilities aimed at reducing lead‑times and fostering skill transfer.

Report Scope

This market research report provides a comprehensive analysis of the Thermoelectric Cooler Assemblies Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Thermoelectric Cooler Assemblies Market?

-> Thermoelectric Cooler Assemblies Market was valued at USD 858 million in 2025 and is expected to reach USD 1,617 million by 2032, growing at a CAGR of 9.4% during the forecast period.

Which key companies operate in Thermoelectric Cooler Assemblies Market?

-> Key players include Ferrotec, KELK Ltd., Coherent Corp, Tark Thermal Solutions, KYOCERA, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, KJLP, Thermion Company, Z-MAX, Zhejiang Wangu Semiconductor, Xianghe Oriental Electronic, Thermonamic Electronics, TE Technology, P&N Technology, AISIN Corporation, Sensor Controls Co., Ltd., Wakefield Thermal, Same Sky, TEC Microsystems GmbH, Peltron GmbH, Kryotherm Industries, Crystal Ltd, Liaoning Lengxin Technology, Thermoelectric new energy technology, Jianju Technology, Bi Sheng Semiconductor, Henan Hongchang Electronic, Wei County Zhongtian Electron Stock Cooperative, Beijing Xinyu Kaimeng Electronic Technology, Beijing Huimao Refrigeration Equipment, Hangzhou Aurin Cooling Device, Henan Guanjing Semiconductor Technology, and Hubei Sagreon New Energy Technology.

What are the key growth drivers?

-> Key growth drivers include the shift toward high‑precision temperature control in optical modules, lasers, medical testing, and semiconductor equipment; expanding automotive battery and seat‑temperature management applications; rising power density in AI computing and 800G/1.6T optical networking demanding compact heat‑removal solutions; and increasing demand for energy‑efficient, refrigerant‑free cooling in data‑center and communications infrastructure.

Which region dominates the market?

-> Asia‑Pacific is the largest market, driven primarily by China’s rapid manufacturing scale and domestic substitution, while Europe retains a strong position in high‑end material supply and reliability‑focused applications.

What are the emerging trends?

-> Emerging trends include integration of cold‑plate and liquid‑cooling modules with TECs, development of high‑heat‑flux, low‑power devices capable of >100,000 thermal cycles, solid‑state thermal solutions for next‑generation AI servers and data centres, and the launch of higher‑performance Peltier modules (e.g., KYOCERA’s 2024 module with 21% higher heat absorption) targeting automotive battery and seat‑temperature control.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...