Photomask Blank (Binary, PSM, EUV) Market Insights

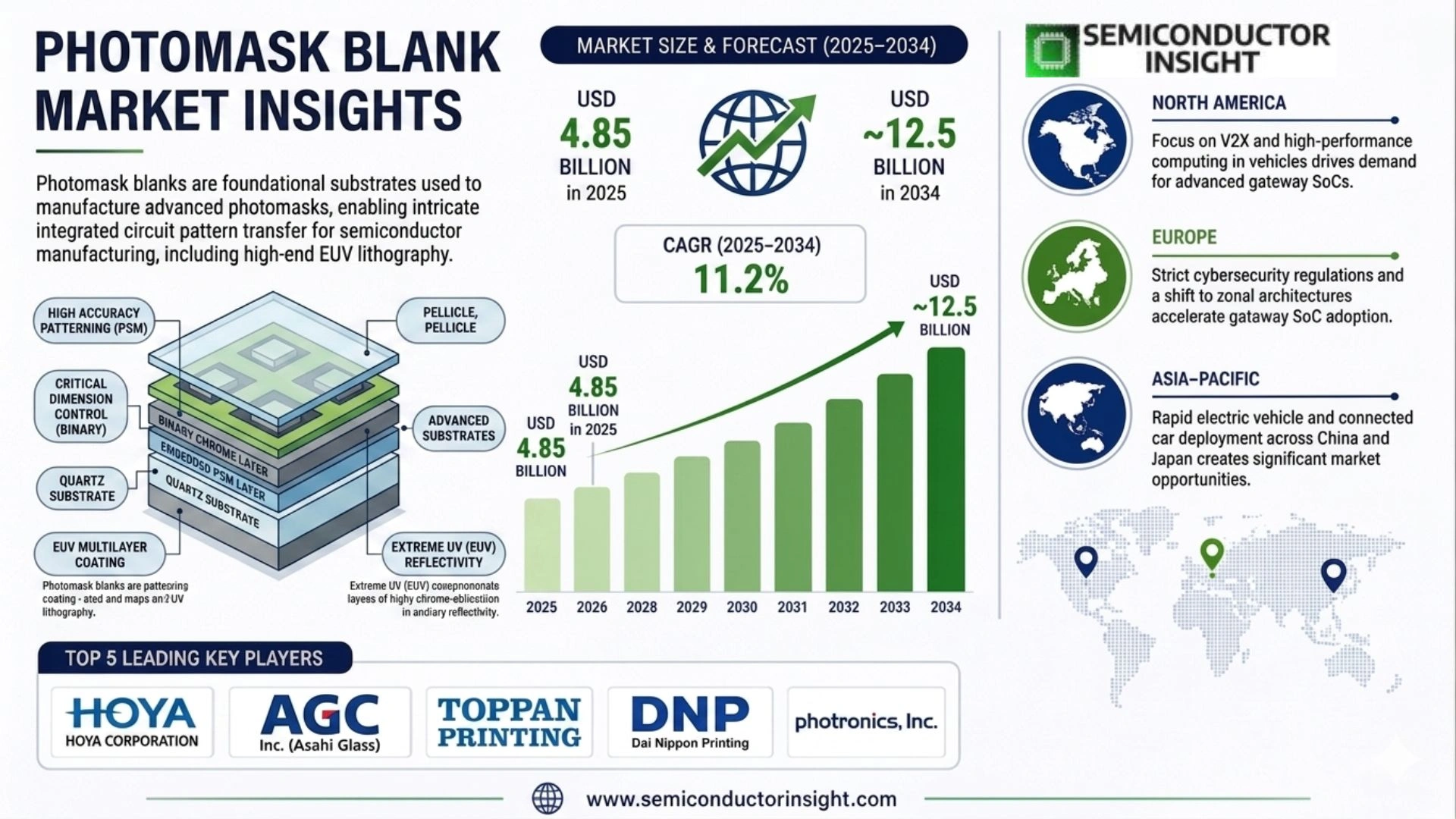

Global Photomask Blank (binary, PSM, EUV) Market size was valued at USD 4.85 billion in 2025. The market is projected to grow from USD 5.32 billion in 2026 to USD 12.47 billion by 2034, exhibiting a CAGR of 11.2% during the forecast period.

Photomask blanks are the foundational substrates used in semiconductor lithography, serving as the base material upon which circuit patterns are etched to create photomasks for chip manufacturing. These blanks are categorized into three primary types: binary masks, which feature simple chrome-on-glass patterns; phase-shifting masks (PSM), which manipulate light phase to enhance resolution; and extreme ultraviolet (EUV) mask blanks, which utilize multilayer reflective coatings for sub-7nm node production. Each type addresses distinct technological requirements across varying semiconductor process nodes.

The market is experiencing substantial growth driven by accelerating demand for advanced semiconductors in artificial intelligence, high-performance computing, and 5G applications. While binary masks continue serving mature nodes, EUV mask blanks are witnessing exceptional expansion because leading foundries such as TSMC and Samsung have ramped up 3nm and below production capacity. Furthermore, the transition toward higher-numerical-aperture (High-NA) EUV lithography is intensifying investment in next-generation mask blank infrastructure. In February 2024, Intel announced the shipment of its first commercial High-NA EUV lithography system from ASML, signaling critical momentum for EUV blank demand. Hoya Corporation, AGC Inc., and S&S Tech Corporation remain dominant suppliers, collectively controlling approximately 85% of global photomask blank production capacity.

MARKET DRIVERS

Increasing Demand for Advanced Semiconductor Devices

Photomask Blank (binary, PSM, EUV) Market is primarily driven by the surging demand for advanced semiconductor devices in various end-use industries such as consumer electronics, automotive, and telecommunications. With the growing adoption of 5G technology and IoT devices, the need for highly precise and defect-free photomasks has intensified, fueling the market growth.

Technological Advancements in Photolithography Techniques

Continuous innovation in photolithography, especially the transition to Extreme Ultraviolet (EUV) lithography, has significantly increased the relevance of high-quality photomask blanks. The development of binary and phase shift masks (PSM) with enhanced resolution capabilities has enabled chip manufacturers to achieve smaller node sizes, thus propelling the demand for premium photomask blanks.

➤ The rise of EUV technology is a pivotal driver, offering unprecedented resolution and patterning efficiency that directly impacts photomask blank requirements.

As semiconductor fabrication evolves towards sub-7nm nodes, the precision and quality standards for photomask blanks have become more stringent, underscoring the critical role of these components in high-volume manufacturing processes.

MARKET CHALLENGES

High Production Costs of Photomask Blanks

The production of photomask blanks, particularly EUV masks, involves sophisticated materials and stringent quality control, which contribute to elevated manufacturing costs. This high cost can limit adoption among smaller semiconductor fabs and act as a barrier in cost-sensitive markets.

Other Challenges

Complexity in Defect Detection and Repair

Defect detection and repair on photomask blanks remain challenging due to the ultra-fine patterns and high precision required. Inadequate inspection techniques can lead to yield losses and affect overall production efficiency.

MARKET RESTRAINTS

Supply Chain Disruptions Affecting Raw Material Availability

Photomask Blank (binary, PSM, EUV) Market faces restraints due to supply chain disruptions impacting the availability of essential raw materials such as high-purity quartz and specialty chromium. Fluctuations in supply can lead to delays and increased costs, constraining market growth. Moreover, geopolitical tensions have added uncertainty to the sourcing landscape, compelling manufacturers to seek alternative suppliers or increase inventory buffers.

MARKET OPPORTUNITIES

Expansion of EUV Lithography Adoption

The accelerating uptake of EUV lithography technology presents a significant opportunity for Photomask Blank (binary, PSM, EUV) Market. As more semiconductor manufacturers transition to EUV for advanced node production, the demand for specialized EUV photomask blanks with improved defect control and mask durability is expected to rise substantially.

Emerging Semiconductor Markets in Asia-Pacific

Emerging semiconductor fabrication hubs in the Asia-Pacific region, supported by substantial government investments and favorable policies, offer lucrative opportunities for photomask blank suppliers. The expansion of fab capacities in countries like China, Taiwan, and South Korea is predicted to increase photomask blank consumption significantly in the forthcoming years.

Trends

Technological Evolution and Production Capacity Expansion

Photomask Blank (binary, PSM, EUV) Market is witnessing dynamic shifts as semiconductor fabrication advances toward smaller nodes and higher complexity. Binary mask blanks remain essential for mature semiconductor nodes, providing reliable and cost-effective solutions. In contrast, phase-shifting masks (PSM) enhance lithographic resolution by manipulating light phases, thus supporting the industry’s progression into more intricate chip designs. Most notably, EUV mask blanks are becoming increasingly critical with the industry’s focus on sub-7nm nodes, driven by leading foundries such as TSMC and Samsung expanding their 3nm and below manufacturing capabilities. This shift underlines a growing dependence on advanced multi-layer reflective coatings that EUV blanks offer, suitable for high-precision photolithography processes.

Recent developments such as the commercial shipment of Intel’s High-NA EUV lithography system mark significant milestones, signaling a new phase of investment in next-generation EUV mask blank infrastructure. This high-numerical-aperture technology is expected to escalate demand and further fuel market growth by enhancing resolution and throughput, pointing to a technology-driven transformation within photomask blank production.

Other Trends

Supplier Market Concentration

The market structure for photomask blank production remains highly concentrated, with dominant players such as Hoya Corporation, AGC Inc., and S&S Tech Corporation collectively controlling approximately 85% of global manufacturing capacity. This concentration underscores the high barriers to entry, driven by the complexity and capital intensity of producing high-quality blanks suitable for advanced lithographic processes. Their leading positions allow these suppliers to steer innovation and respond swiftly to shifts in demand patterns, particularly in the EUV segment.

Driver Markets and Application Growth

Strong demand growth is propelled by key end-user domains including artificial intelligence, high-performance computing, and 5G telecommunications. These applications require increasingly sophisticated semiconductor devices, increasing the reliance on cutting-edge photomask blanks to meet precision and yield requirements. The proliferation of AI workloads and 5G infrastructure worldwide continues to underpin sustained momentum in advanced photomask blank demand.

Future Outlook and Market Dynamics

Looking ahead, Photomask Blank (binary, PSM, EUV) Market is set to evolve with a focus on supporting emerging semiconductor manufacturing technologies. The ongoing transition to High-NA EUV lithography and sub-3nm production nodes will likely reinforce investment in process innovation and new materials development. Meanwhile, maintaining supply chain robustness and addressing capacity constraints will be critical for suppliers to capitalize on expanding opportunities. In summary, the market is poised for sustained growth driven by continuous technology upgrades and escalating demand from the semiconductor industry’s leading-edge segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Photomask Blank Market Dominated by Leading Suppliers Amid Accelerated EUV Adoption

The photomask blank market is primarily led by a few dominant players including Hoya Corporation, AGC Inc., and S&S Tech Corporation, which together control around 85% of the global production capacity. These companies have established a robust presence through extensive technological capabilities and capacity expansion, addressing a broad range of semiconductor lithography needs from binary and phase-shifting masks (PSM) to advanced extreme ultraviolet (EUV) blanks. The market structure reflects a high degree of concentration, particularly as demand surges for sub-7nm node production and High-NA EUV technologies, with leading foundries such as TSMC and Samsung driving significant growth through their advanced chip manufacturing requirements.

Besides the market leaders, several niche yet significant players contribute specialized photomask blank solutions tailored to specific semiconductor processes or regional demands. Companies like Mitsui Chemicals, Shin-Etsu Chemical, and HOYA ALPHA Plastics provide competitive offerings, often focusing on innovation within binary and PSM segments. Moreover, emerging suppliers such as Corning Incorporated and Fukuda Chemicals are investing in next-generation blank technologies to keep pace with evolving industry standards. This diverse competitive environment supports ongoing advancements in semiconductor lithography driven by AI, high-performance computing, and 5G application demands.

List of Key Photomask Blank Companies Profiled

- Hoya Corporation

- AGC Inc.

- S&S Tech Corporation

- Mitsui Chemicals

- Shin-Etsu Chemical

- Corning Incorporated

- Fukuda Chemicals

- Takagi Seiki

- Komatsu Ltd.

- Sumitomo Chemical

- Seiko Epson Corporation

- Heptagon Micro Optics

- Tantec Ltd.

- Fujifilm Holdings Corporation

- Tokuyama Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Extreme Ultraviolet (EUV) Mask Blanks are rapidly gaining prominence due to their critical role in next-generation semiconductor nodes, supporting sub-7nm technologies. Their advanced multilayer reflective coatings are indispensable for high-resolution chip fabrication.

|

| By Application |

|

Semiconductor Manufacturing remains the primary application area where advancements in photomask blanks directly contribute to improvements in chip resolution and functionality.

|

| By End User |

|

Foundries dominate demand due to their focus on cutting-edge fabrication nodes, especially the push towards 3nm and smaller technologies requiring EUV mask blanks.

|

| By Lithography Technology |

|

Extreme Ultraviolet (EUV) lithography is a key driver for demand in advanced photomask blanks, enabling critical resolution enhancements.

|

| By Supplier Type |

|

Specialized Photomask Manufacturers such as industry leaders provide critical technology and production capacity to meet advanced blank specifications.

|

Regional Analysis: Global Photomask Blank (binary, PSM, EUV) Market

The Asia-Pacific region benefits from continuous innovation in photomask blank design, particularly enhancing EUV blank defectivity and binary blank uniformity. Collaboration between equipment suppliers and semiconductor fabs accelerates technology adoption, supporting the evolution of complex patterning techniques.

Strong vertical integration and supply chain coordination characterize Asia-Pacific’s photomask blank market. Local suppliers manage raw material sourcing and finishing processes to reduce lead times and improve responsiveness to fab requirements.

Increasing semiconductor wafer fabrication capacity expansion driven by consumer electronics and automotive industries directly boosts photomask blank consumption. Strategic government initiatives on semiconductor autonomy also underpin sustained growth.

Despite notable advances, managing complex defect inspection requirements and cost pressures remains a challenge. However, the rising demand for EUV photomask blanks presents ample opportunity for innovation and market differentiation.

North America

North America maintains a significant role Photomask Blank (binary, PSM, EUV) Market through its concentration of semiconductor design houses and cutting-edge fab operations. The region excels in developing advanced mask-making technologies, focusing on improving defect control and mask durability to address increasingly smaller process nodes. Collaboration among leading equipment manufacturers, mask shops, and fabs fosters innovation. Moreover, initiatives to strengthen domestic semiconductor manufacturing contribute to sustained demand, enhancing North America’s strategic importance in the photomask blank supply chain.

Europe

Europe’s presence Photomask Blank (binary, PSM, EUV) Market is driven by specialized research institutions and companies developing niche photomask products, particularly for PSM and binary masking solutions. The region emphasizes sustainability and precision manufacturing, complementing its focus on automotive semiconductors and industrial electronics. Collaborative projects under the European Union’s semiconductor initiatives promote advanced photomask blank technologies, although the overall market size remains optimistic but comparatively moderate.

South America

South America exhibits nascent activity in the photomask blank arena with growing interest in semiconductor component assembly and testing. Although direct manufacturing of photomask blanks remains limited, the market benefits indirectly from increasing fab outsourcing and demand for high-quality mask blanks related to regional electronics manufacturing growth. Strategic partnerships and investments could accelerate the region’s photomask blank capabilities in coming years.

Middle East & Africa

The Middle East & Africa market for photomask blanks is in early development stages, with emerging investments in semiconductor fabrication and advanced manufacturing clusters. Demand is currently limited but shows potential linked to regional diversification into high-tech industries. Efforts focusing on technology transfers and infrastructure development may gradually strengthen the market position in this region, particularly for next-generation EUV photomask blanks.

Report Scope

This market research report provides a comprehensive analysis of the Photomask Blank (Binary, PSM, EUV) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Photomask Blank (Binary, PSM, EUV) Market?

-> Photomask Blank (binary, PSM, EUV) Market was valued at USD 4.85 billion in 2025 and is expected to reach USD 12.47 billion by 2034.

Which key companies operate Photomask Blank (binary, PSM, EUV) Market?

-> Key players include Hoya Corporation, AGC Inc., and S&S Tech Corporation, who collectively control approximately 85% of global photomask blank production capacity.

What are the key growth drivers?

-> Key growth drivers include accelerating demand for advanced semiconductors in artificial intelligence, high-performance computing, and 5G applications, as well as investments in next-generation mask blank infrastructure driven by the transition to High-NA EUV lithography.

Which region dominates the market?

-> While the reference content does not explicitly specify regional dominance, it highlights major foundries like TSMC and Samsung (Asia-Pacific) ramping up production, indicating strong market activity in the Asia-Pacific region.

What are the emerging trends?

-> Emerging trends include the expansion of EUV mask blanks for sub-7nm node production, the adoption of phase-shifting masks to enhance resolution, and the deployment of High-NA EUV lithography systems such as Intel’s first commercial High-NA EUV system shipping in 2024.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...