Neural Processing Unit (NPU) Market Insights

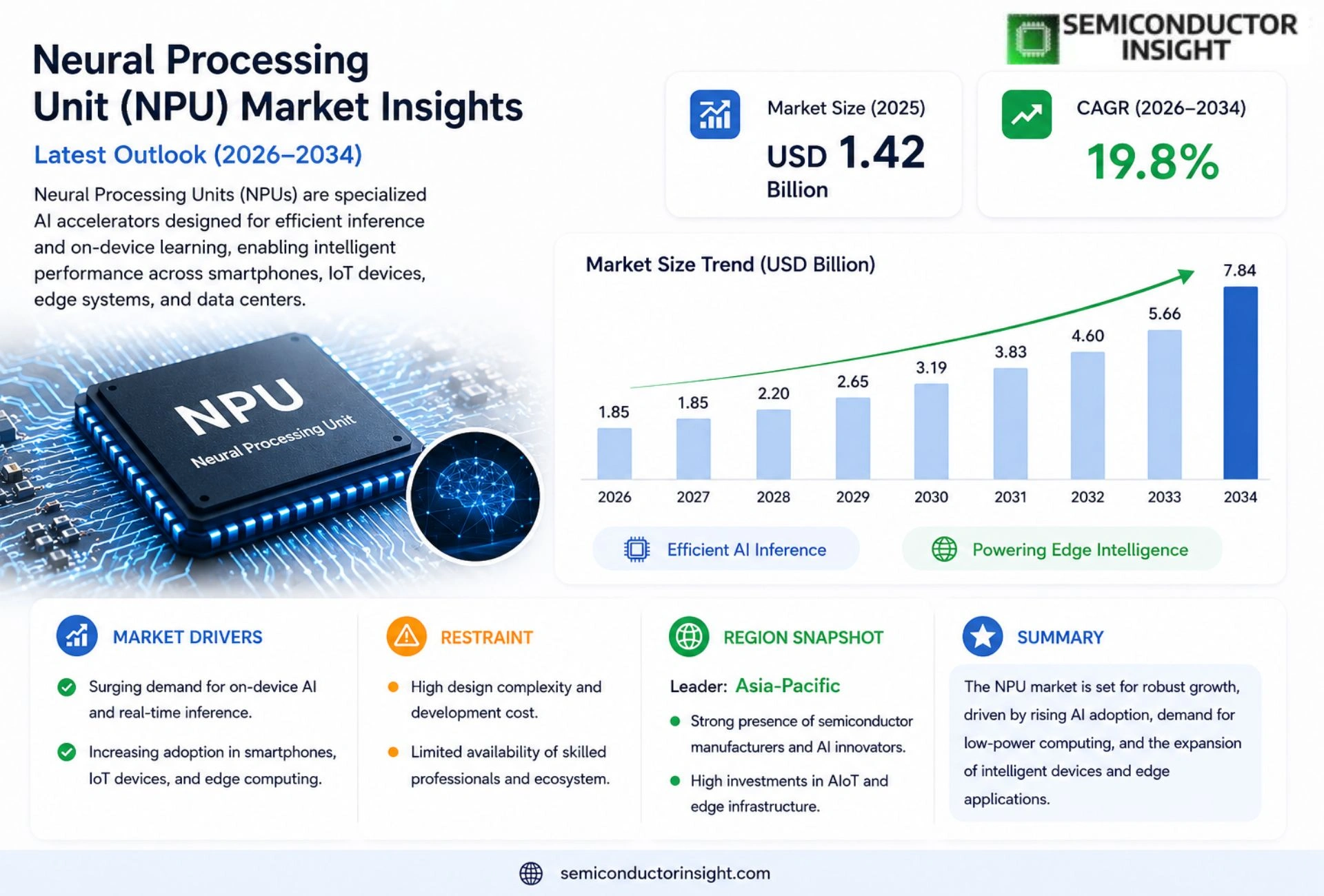

Global Neural Processing Unit (NPU) Market size was valued at USD 1.42 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 7.84 billion by 2034, exhibiting a CAGR of 19.8% during the forecast period.

Neural Processing Units are specialized AI accelerators designed to execute deep‑learning inference and training workloads with high efficiency. They integrate matrix‑multiply engines, tensor cores, and low‑precision arithmetic units that accelerate convolutional neural networks, transformer models, and computer‑vision tasks while reducing power consumption compared with general‑purpose CPUs or GPUs.

The market is experiencing rapid expansion because semiconductor manufacturers are investing heavily in edge‑AI chips, mobile devices demand on‑device intelligence, and data‑center operators seek higher throughput per watt. Furthermore, collaborations such as Samsung’s partnership with Arm for custom NPU IPs and Apple’s continuous enhancement of its Neural Engine illustrate how leading players are driving adoption across smartphones, autonomous vehicles, and industrial IoT.

MARKET DRIVERS

Growing AI Workload Demands

The surge in edge‑AI applications, such as autonomous devices and real‑time analytics, is prompting manufacturers to adopt specialized compute fabrics. Performance‑per‑watt improvements offered by neural accelerators are a decisive factor for OEMs seeking to extend battery life while maintaining inference speed.

Integration with 5G and IoT Ecosystems

Deployment of 5G‑enabled sensors generates massive data streams that must be processed locally. Low‑latency processing enabled by neural processing units reduces reliance on cloud back‑haul, thereby supporting privacy‑centric use cases in smart cities and industrial automation.

➤ “By 2028, AI‑driven edge devices are projected to account for over 40% of total AI inference workloads, fueling demand for dedicated neural hardware.”

Investments from leading semiconductor firms into NPU IP blocks are accelerating time‑to‑market for custom silicon solutions, creating a virtuous cycle of innovation and adoption across consumer, automotive, and data‑center segments.

MARKET CHALLENGES

Fragmented Software Toolchains

Developers face a disparate ecosystem of compilers, frameworks, and runtime libraries, which hampers portability of models across different hardware generations. Toolchain consolidation remains a critical hurdle for broad market penetration.

Other Challenges

Power Management Constraints

While NPUs excel in efficiency, thermal design power limits in ultra‑compact devices restrict scaling. Engineers must balance throughput and heat dissipation, often resorting to aggressive duty‑cycling strategies.

MARKET RESTRAINTS

High Development Costs

Custom silicon projects demand multi‑year design cycles and substantial capital outlays. Small‑to‑medium enterprises find it difficult to justify the upfront investment, limiting the breadth of NPU adoption beyond large incumbents.

Supply‑chain bottlenecks for advanced process nodes further exacerbate time‑to‑market, creating a restraint on rapid scaling of new product lines.

MARKET OPPORTUNITIES

Emerging Edge‑AI Segments

Verticals such as health‑tech wearables and AR/VR headsets require on‑device inference with stringent latency budgets. These niches present high‑value opportunities for NPU vendors capable of delivering sub‑10‑ms response times.

Open‑source AI frameworks are converging around standardized operator sets, paving the way for cross‑vendor compatibility and lowering entry barriers for new market participants.

Strategic partnerships between semiconductor foundries and AI software houses are expected to unlock co‑optimized solutions, accelerating adoption in both consumer and industrial domains.

Neural Processing Unit (NPU) Market Trends

Edge AI Acceleration Drives Growth

The proliferation of edge‑AI workloads is reshaping processor strategies across the industry. Semiconductor firms are prioritizing designs that embed inference capabilities directly into devices, reducing latency and bandwidth costs. This shift is especially evident in smartphones, autonomous‑driving platforms, and industrial IoT sensors, where on‑device intelligence enables real‑time decision making while conserving power. Analysts attribute the momentum to commodity‑grade GPUs reaching power‑efficiency limits, prompting a migration toward purpose‑built accelerators that specialize in matrix multiplication and tensor operations.

Other Trends

Integration with Mobile SoCs

Major mobile chipset providers have begun to incorporate dedicated NPU blocks into their system‑on‑chips (SoCs). By co‑locating the accelerator with CPUs, GPUs, and memory controllers, manufacturers achieve tighter data paths and lower energy per operation. Recent product roadmaps reveal a trend toward configurable compute engines that can be programmed for a range of AI models, from computer‑vision filters to natural‑language transformers. This flexibility allows device makers to future‑proof hardware against the rapid evolution of AI algorithms.

Custom NPU IP Partnerships Expand Ecosystem

Strategic collaborations are accelerating ecosystem development. Leading fabless companies are licensing customizable NPU intellectual property (IP) from architecture specialists, enabling rapid differentiation without extensive in‑house R&D. Such partnerships also foster a broader software stack, as SDKs and compilers are aligned with the specific micro‑architectural features of the licensed IP. Consequently, developers can more efficiently map neural network graphs to hardware, shortening time‑to‑market for new AI‑enabled products. The cumulative effect is a more vibrant supplier network that supports a range of performance‑per‑watt targets, reinforcing the overall health of Neural Processing Unit (NPU) Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of the Global Neural Processing Unit (NPU) Market (2025‑2034)

Neural Processing Unit (NPU) Market is currently dominated by a handful of semiconductor powerhouses that have integrated dedicated AI accelerators into flagship products. Samsung Electronics leverages its partnership with Arm to offer customized NPU IPs across premium smartphones, while Apple continues to expand its Neural Engine performance in each iPhone generation. Qualcomm’s Hexagon DSPs, now branded as AI‑focused NPUs, provide a scalable solution for edge devices, and MediaTek’s APU series targets mid‑range markets. In the data‑center arena, Google’s Tensor ASIC, Nvidia’s Jetson family, and Intel’s Movidius VPU maintain a strong foothold, delivering high throughput per watt for inference workloads. This concentration of capital and R&D creates a tiered landscape where a few tier‑one firms command the majority of revenue, and the rest compete on niche performance or power‑efficiency advantages.

Beyond the tier‑one incumbents, a vibrant ecosystem of specialized players is accelerating innovation in the NPU space. Chinese firms such as Huawei’s Ascend, Cambricon, and Horizon Robotics focus on automotive and industrial IoT applications, while European startups like Graphcore and SambaNova bring novel architecture designs for training‑heavy workloads. Mythic and Tenstorrent pursue analog‑in‑memory and dataflow approaches respectively, aiming to disrupt conventional silicon pathways. Strategic alliances—e.g., Samsung‑Arm co‑development, Apple’s in‑house silicon design, and collaborative roadmaps between Qualcomm and OpenAI—underscore a market that rewards both integration depth and cross‑industry partnerships.

List of Key Neural Processing Unit (NPU) Market Companies Profiled

- Samsung Electronics

- Qualcomm

- Apple Inc.

- MediaTek

- Nvidia

- Intel

- Huawei

- Cambricon Technologies

- Graphcore

- Mythic

- SambaNova Systems

- Tenstorrent

- Horizon Robotics

- Alibaba DAMO Academy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Convolutional‑Optimized NPU is favored for image‑heavy workloads because it delivers high throughput for convolutional kernels, integrates efficient memory tiling, and reduces power draw on edge devices.

|

| By Application |

|

Smartphones & Wearables drive NPU adoption through on‑device intelligence, allowing real‑time vision and voice features without cloud dependency.

|

| By End User |

|

Device Manufacturers view NPUs as essential silicon blocks that enable differentiated AI experiences while maintaining strict power budgets.

|

| By Architecture |

|

Programmable NPU is gaining traction because it balances performance with flexibility for emerging AI models.

|

| By Deployment |

|

Edge Deployment is the dominant narrative as manufacturers prioritize low‑latency, power‑efficient inference close to data sources.

|

Regional Analysis:

United States

The mobile sector continues to be a primary driver for NPU adoption, as smartphones increasingly incorporate AI-powered features like advanced photography, natural language processing, and personalized user experiences.

The automotive industry is witnessing a rapid shift towards autonomous driving and advanced driver-assistance systems (ADAS), necessitating the integration of NPUs for real-time data processing and decision-making.

Data centers are increasingly leveraging NPUs to accelerate AI workloads, such as machine learning inference and large-scale data analytics, driven by the escalating demands of cloud computing.

The rise of edge computing is creating new opportunities for NPUs to enable localized AI processing, reducing latency and enhancing data privacy.

Europe

The European NPU market is experiencing steady growth, propelled by increasing investments in AI across various industries. Stringent data privacy regulations, such as GDPR, are influencing the design and deployment of NPUs towards enhanced security features. The automotive sector in Europe is also a significant contributor to NPU demand, with a strong focus on autonomous driving technologies. Furthermore, the European Union’s initiatives to boost semiconductor manufacturing are expected to further stimulate the NPU market in the region.

Asia-Pacific

The Asia-Pacific region represents the largest and fastest-growing market for NPUs globally. China, in particular, is driving this growth with substantial investments in AI infrastructure and a rapidly expanding consumer electronics market. The demand for NPUs is strong in sectors like telecommunications, consumer electronics, and industrial automation. Government support for domestic semiconductor industries and the increasing adoption of 5G technology are key factors contributing to the region’s robust NPU market.

South America

The South American NPU market is in its nascent stages but is poised for significant expansion. The increasing adoption of smartphones and the growing demand for AI-powered applications are creating opportunities for NPU vendors. The telecommunications sector and the automotive industry are also expected to drive demand in the coming years. While the market is currently smaller compared to North America and Asia-Pacific, the long-term growth potential remains substantial.

Middle East & Africa

The Middle East and Africa represent a smaller but emerging market for NPUs. The increasing investments in smart city initiatives, healthcare technologies, and e-commerce platforms are driving demand for AI-powered solutions and, consequently, for NPUs. The growing adoption of 5G networks and the expansion of the automotive industry are also expected to contribute to the market’s growth.

Report Scope

This market research report provides a comprehensive analysis of the Neural Processing Unit (NPU) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Neural Processing Unit (NPU) Market?

-> Neural Processing Unit (NPU) Market was valued at USD 1.42 billion in 2025 and is expected to reach USD 7.84 billion by 2034, reflecting a compound annual growth rate (CAGR) of 19.8% over the forecast period.

Which key companies operate in Neural Processing Unit (NPU) Market?

-> Key players include Samsung Electronics, Apple Inc., and Arm Ltd. These companies are actively developing custom NPU IPs and integrating neural engines into consumer devices and data‑center solutions.

What are the key growth drivers?

-> Key growth drivers include heavy investments by semiconductor manufacturers in edge‑AI chips, rising demand for on‑device intelligence in mobile devices, and data‑center operators seeking higher throughput per watt.

Which region dominates the market?

-> Asia‑Pacific leads the market, driven by robust smartphone adoption, extensive semiconductor manufacturing bases, and aggressive AI‑focused R&D initiatives, while North America and Europe also show strong demand.

What are the emerging trends?

-> Emerging trends include custom NPU IP development, tighter integration of AI with IoT edge devices, and the deployment of low‑precision arithmetic engines to boost performance while minimizing power consumption.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...