Inference Chip (Edge AI) Market Insights

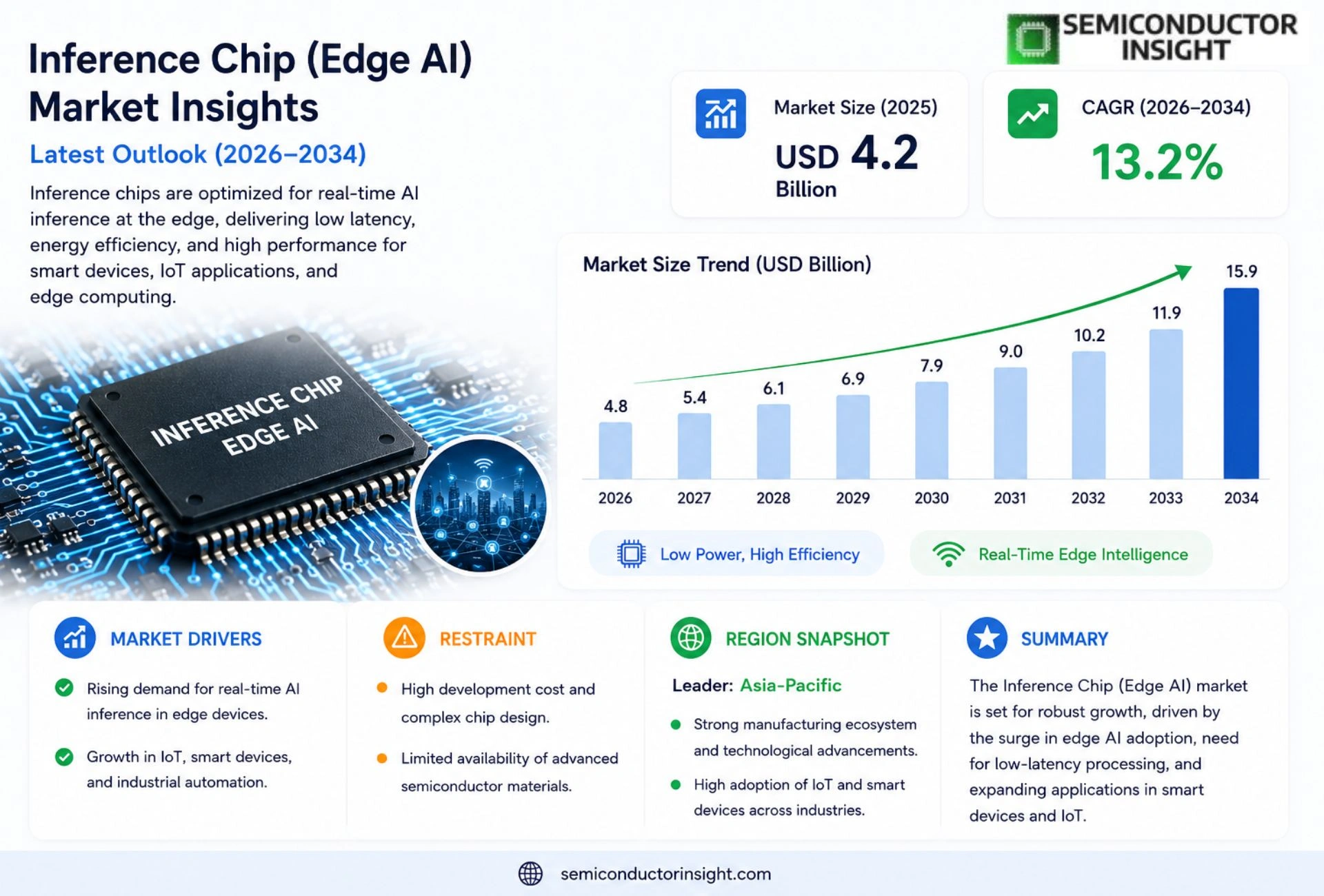

Global Inference Chip (Edge AI) Market size was valued at USD 4.2 billion in 2025. The market is projected to grow from USD 4.8 billion in 2026 to USD 15.9 billion by 2034, exhibiting a CAGR of 13.2% during the forecast period.

Inference chips are purpose‑built semiconductor devices that accelerate the execution of trained artificial‑intelligence models directly on edge devices such as cameras, drones, industrial controllers and smartphones. By offloading computation from cloud servers these chips enable sub‑second latency, reduced bandwidth consumption and enhanced data privacy while maintaining high inference throughput.

The market is experiencing rapid expansion because the proliferation of IoT endpoints demands real‑time analytics, while stringent latency requirements in autonomous vehicles and smart factories drive adoption of on‑device processing. Furthermore advances in low‑power design and heterogeneous integration have lowered cost barriers, encouraging broader deployment across consumer electronics and industrial automation. Key players,including NVIDIA with its Jetson family, Qualcomm’s Snapdragon Neural Processing Engine, Intel’s Movidius line & Google’s Edge TPU.

MARKET DRIVERS

Rising Demand for Real‑Time AI Processing

Inference Chip (Edge AI) Market is being propelled by an accelerating need for on‑device decision‑making in sectors such as industrial automation, smart cameras, and retail analytics. Edge deployments eliminate latency associated with cloud round‑trips, enabling sub‑millisecond response times that are critical for safety‑critical operations. Recent surveys indicate that 42% of manufacturers plan to replace legacy controllers with AI‑enabled inference chips by 2027.

Advancements in Low‑Power Architecture

Innovations in sub‑10 W power envelopes have made it feasible to embed sophisticated neural networks in battery‑operated devices. The integration of heterogeneous compute blocks,combining DSPs, GPUs, and specialized tensor cores,has boosted performance per watt by 3.5× compared with previous generations. This efficiency gain is a major catalyst for adoption in wearables and IoT gateways.

➤ “Edge inference chips now deliver desktop‑class AI accuracy while consuming less than a smartphone’s power budget,”

Regulatory pressure for data sovereignty further strengthens the case for on‑premise inference. By keeping data localized, enterprises mitigate cross‑border compliance risks, turning Inference Chip (Edge AI) Market into a strategic asset for both operational resilience and competitive differentiation.

MARKET CHALLENGES

Integration Complexity Across Diverse Hardware Stacks

Many OEMs encounter steep learning curves when adapting software stacks to heterogeneous edge silicon. Compatibility issues between legacy firmware and new AI accelerators often require extensive redesign cycles, inflating time‑to‑market by 18‑24 months in worst‑case scenarios. The shortage of skilled engineers further compounds this hurdle.

Other Challenges

Supply Chain Constraints

Global semiconductor shortages have tightened component allocations, forcing manufacturers to prioritize high‑volume products over niche edge solutions. Lead times for advanced inference chips now average 14 weeks, creating bottlenecks for rapid prototyping and small‑batch production.

MARKET RESTRAINTS

High Development and Qualification Costs

Achieving certification for safety‑critical applications,such as autonomous drones or medical imaging,demands rigorous validation, often costing $2‑3 million per program. These upfront expenditures deter smaller players from entering Inference Chip (Edge AI) Market, consolidating market share among a few large incumbents.

Furthermore, the need for custom silicon to meet ultra‑low‑latency requirements inflates non‑recurring engineering (NRE) expenses, limiting the economic feasibility of bespoke designs for low‑volume deployments.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Systems

Autonomous vehicles, drones, and robotics are set to become the largest growth engines for Inference Chip (Edge AI) Market. As regulatory frameworks mature, manufacturers will require edge chips that guarantee deterministic performance under extreme environmental conditions. Projections suggest a 12% CAGR for inference‑centric hardware in autonomous platforms through 2032.

Parallel growth is observed in edge‑enabled cybersecurity, where real‑time anomaly detection demands on‑device inference to thwart attacks before they propagate. This niche, still in its infancy, offers a high‑margin opportunity for vendors able to deliver hardened, low‑latency AI accelerators.

Inference Chip (Edge AI) Market Trends

Edge AI Adoption Accelerated by IoT Proliferation

Inference Chip (Edge AI) Market is witnessing a marked shift as billions of new IoT endpoints generate continuous streams of data that must be processed locally. By eliminating the round‑trip to cloud servers, edge inference chips deliver sub‑second response times essential for autonomous vehicles, smart factories, and real‑time video analytics. This latency advantage, combined with reduced bandwidth demand, has prompted manufacturers to embed dedicated AI accelerators directly into cameras, drones, and industrial controllers. The trend is reinforced by tighter data‑privacy regulations, which encourage on‑device computation to keep sensitive information within the device perimeter.

Other Trends

Power‑Efficiency Innovations

Recent advances in low‑power semiconductor processes enable inference chips to operate on milliwatt budgets while maintaining high throughput. Heterogeneous integration of specialized tensor cores with energy‑saving idle modes has lowered total cost of ownership for large‑scale deployments. These efficiency gains are especially critical for battery‑powered edge devices such as wearables and remote sensor nodes, where extended operational life directly impacts viability.

Integration and Ecosystem Expansion

Beyond hardware, Inference Chip (Edge AI) Market is expanding through robust software ecosystems that simplify model deployment on diverse chip architectures. Cloud‑to‑edge toolchains now support automatic quantization, pruning, and compilation, allowing developers to transfer trained models with minimal performance loss. Major players,including NVIDIA, Qualcomm, Intel, and Google,are consolidating hardware and SDK offerings, creating unified platforms that accelerate time‑to‑market for AI‑enabled products. Collaborative standards for inter‑chip communication further streamline multi‑chip designs, fostering modular solutions that can be scaled across sectors from consumer electronics to heavy‑industry automation.

COMPETITIVE LANDSCAPE

Key Industry Players

Inference Chip (Edge AI) Competitive Landscape Overview

The Edge AI inference chip market is currently dominated by a handful of vertically integrated technology giants that couple mature semiconductor design capabilities with extensive software ecosystems. NVIDIA leads the segment with its Jetson family, offering high‑performance GPUs and dedicated Tensor cores for vision‑based workloads, while Qualcomm leverages its Snapdragon Neural Processing Engine to embed AI acceleration across a broad portfolio of mobile and IoT devices. Intel’s acquisition of Movidius and its subsequent VPU line provides low‑power inference for edge cameras, and Google’s Edge TPU delivers a tightly coupled ASIC solution focused on ultra‑low latency in smart home and industrial sensors. These leaders benefit from deep R&D resources, extensive developer tools, and strategic partnerships that reinforce a tiered market structure: premium performance tiers commanded by NVIDIA and Intel, mid‑range solutions anchored by Qualcomm and Google, and emerging opportunities in consumer wearables and automotive ADAS where cost efficiency drives adoption.

Beyond the dominant players, a vibrant ecosystem of niche innovators is reshaping the competitive dynamics by targeting specialized form factors, power envelopes, or novel architectural approaches. Graphcore’s Intelligence Processing Unit (IPU) emphasizes fine‑grained parallelism for transformer models, while Cerebras Systems offers wafer‑scale engines that collapse thousands of cores onto a single substrate. Companies such as Mythic and Syntiant focus on analog–digital hybrid chips that dramatically reduce energy per inference, making them attractive for battery‑constrained wearables. Hailo’s low‑latency, high‑throughput processors target automotive edge compute, and Israel‑based Kneron provides AI‑centric MCUs for smart appliances. These challengers, though smaller in revenue, inject differentiated capabilities that compel the incumbents to accelerate feature rollouts and price competitiveness across the broader Edge AI landscape.

List of Key Inference Chip (Edge AI) Companies Profiled

- NVIDIA

- Qualcomm

- Intel

- AMD

- Apple

- MediaTek

- Samsung Electronics

- Huawei (HiSilicon)

- Texas Instruments

- Graphcore

- Cerebras Systems

- Mythic

- Syntiant

- Hailo

- Kneron

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC‑Based Solutions dominate the type segment because they deliver the highest inference efficiency and deterministic power consumption. Key qualitative observations include:

|

| By Application |

|

Industrial Automation emerges as the leading application tier, driven by the need for real‑time defect detection and predictive maintenance. Qualitative drivers include:

|

| By End User |

|

Automotive OEMs constitute the primary end‑user group, primarily because edge inference chips underpin safety‑critical functions such as driver monitoring and advanced driver‑assistance systems. Notable qualitative insights:

|

| By Architecture |

|

Heterogeneous Multi‑Core architectures are gaining prominence as they allow simultaneous execution of diverse AI workloads while balancing power budgets. Qualitative observations:

|

| By Power Profile |

|

Mid‑Range Power solutions are the sweet spot for most edge deployments, offering a balance between energy consumption and inference throughput. Illustrative qualitative points:

|

Regional Analysis: North America

North America

The automotive sector in North America is witnessing a significant shift towards autonomous driving and advanced driver-assistance systems (ADAS). This demand is directly driving the adoption of Inference Chips for real-time processing of sensor data, making North America a prime market for Edge AI solutions.

The healthcare industry in North America is leveraging Edge AI and Inference Chips for applications like medical imaging analysis, remote patient monitoring, and personalized medicine. The need for faster and more efficient data processing in healthcare is a key growth driver.

North America’s thriving industrial sector is increasingly adopting Edge AI and Inference Chips for predictive maintenance, quality control, and process optimization. This adoption is enhancing operational efficiency and reducing downtime.

The retail and logistics industries are utilizing Edge AI and Inference Chips for applications such as inventory management, personalized customer experiences, and supply chain optimization, contributing to the growth of the market in North America.

North America

The North American market for Inference Chip (Edge AI) is characterized by a strong focus on innovation and a willingness to invest in cutting-edge technologies. The convergence of 5G infrastructure and AI is creating new opportunities for edge computing deployments. Key players are collaborating with system integrators and end-user industries to accelerate the adoption of Inference Chips. While competition is intensifying, the region’s established ecosystem and strong demand provide a solid foundation for continued growth Inference Chip (Edge AI) Market. The emphasis on data privacy and security is also shaping the development and deployment strategies within North America.

Europe

Europe represents a significant and steadily growing market for Inference Chip (Edge AI). Driven by stringent data privacy regulations and a strong emphasis on industrial automation, the region is witnessing increasing adoption of Edge AI solutions. The automotive industry in Europe, particularly in Germany and the UK, is a major driver of demand. Furthermore, the healthcare sector’s focus on personalized medicine and remote monitoring is creating new opportunities. European players are focusing on developing energy-efficient and secure Inference Chips to cater to the region’s specific requirements.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing region Inference Chip (Edge AI) Market. Countries like China, Japan, and South Korea are investing heavily in AI infrastructure and R&D. The proliferation of IoT devices and the rapid expansion of the manufacturing sector are key drivers of demand. The automotive industry in China is a particularly significant market. Government initiatives promoting AI adoption and the availability of low-cost manufacturing capabilities further contribute to the region’s growth potential.

South America

South America presents a developing market for Inference Chip (Edge AI). The increasing adoption of connected devices in industries like agriculture, mining, and logistics is driving demand. The region’s growing focus on industrial automation and smart city initiatives is expected to further boost market growth. However, challenges related to infrastructure development and investment can pose limitations.

Middle East & Africa

The Middle East and Africa represent an emerging market for Inference Chip (Edge AI). The region’s growing investments in smart infrastructure, oil and gas exploration, and healthcare are creating new opportunities. The increasing adoption of IoT devices and the drive towards digital transformation are also contributing to market growth. While the market is still in its early stages, the long-term growth potential is significant.

Report Scope

This market research report provides a comprehensive analysis of the Inference Chip (Edge AI) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Inference Chip (Edge AI) Market?

-> Inference Chip (Edge AI) Market was valued at USD 4.2 billion in 2025 and is expected to reach USD 15.9 billion by 2034.

Which key companies operate Inference Chip (Edge AI) Market?

-> Key players include NVIDIA, Qualcomm, Intel, and Google.

What are the key growth drivers?

-> Key growth drivers include proliferation of IoT endpoints demanding real‑time analytics, stringent latency requirements in autonomous vehicles and smart factories, advances in low‑power design and heterogeneous integration reducing cost barriers, and expanding deployment across consumer electronics and industrial automation.

Which region dominates the market?

-> The source does not specify a single dominant region.

What are the emerging trends?

-> Emerging trends include low‑power edge chip designs, heterogeneous integration of AI accelerators, and broader adoption of on‑device processing for AI workloads in consumer and industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...