Training Chip (Datacenter AI) Market Insights

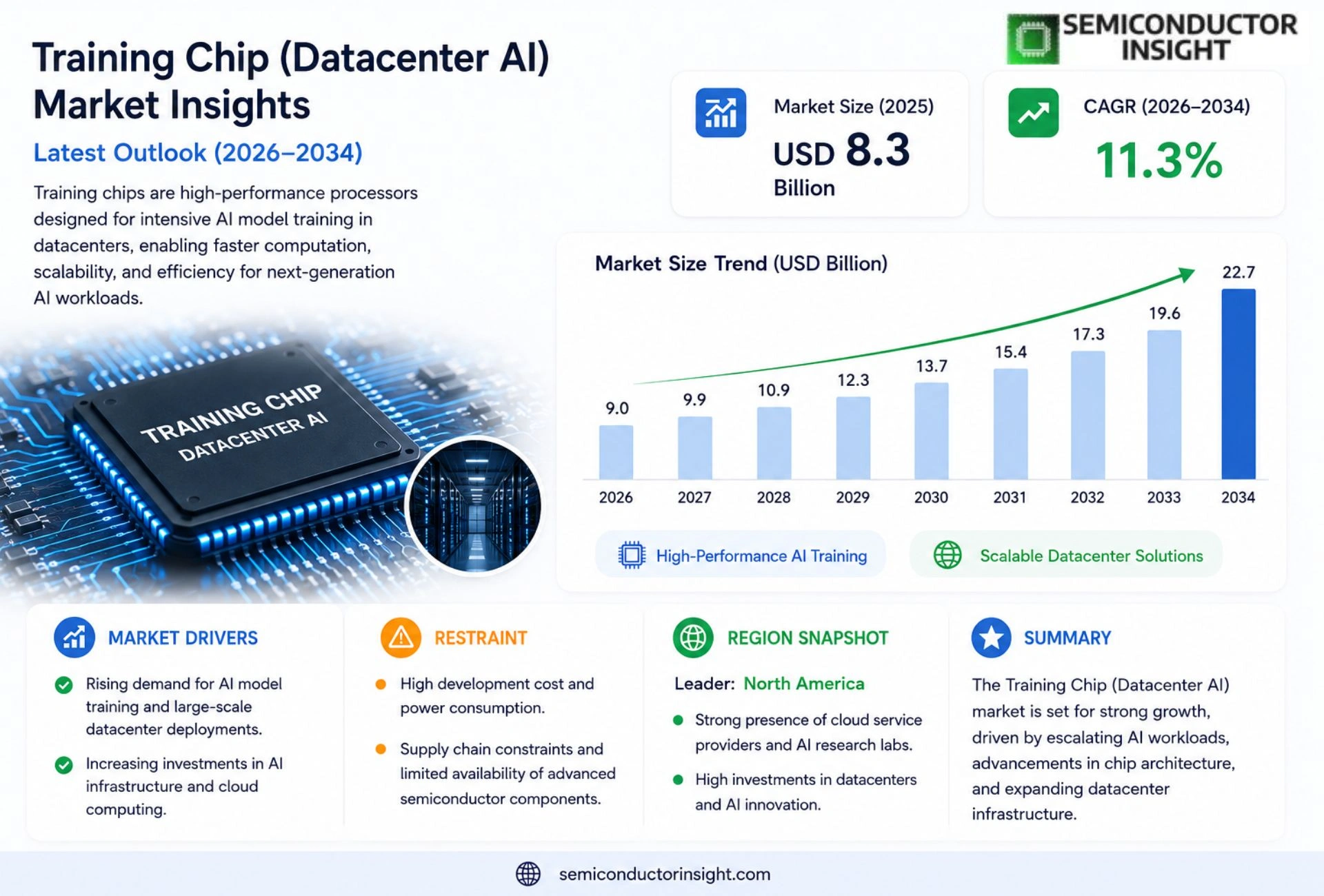

Global Training Chip (Datacenter AI) market size was valued at USD 8.3 billion in 2025. The market is projected to grow from USD 9.0 billion in 2026 to USD 22.7 billion by 2034, exhibiting a CAGR of 11.3% during the forecast period.

Training chips are specialized semiconductor processors designed to accelerate deep‑learning model training within high‑performance datacenters. These devices combine massive parallel compute cores, high‑bandwidth memory interfaces, and optimized interconnects to handle the intensive matrix‑multiplication workloads that underpin modern artificial‑intelligence workloads.

The market is experiencing rapid expansion due to soaring demand for generative AI services, increased cloud‑provider investments in dedicated AI infrastructure, and breakthroughs in chip architecture that improve performance per watt. Furthermore, strategic collaborations,such as NVIDIA’s March 2024 partnership with Microsoft Azure for next‑generation H100 GPUs and Google’s rollout of fourth‑generation TPUs,are fueling adoption across hyperscale operators like Amazon Web Services and Alibaba Cloud.

MARKET DRIVERS

Rising Compute Demand in AI Workloads

Training Chip (Datacenter AI) Market is expanding rapidly as enterprises scale deep‑learning models that require petaflop‑level processing power. Cloud service providers are provisioning larger clusters of specialized training chips to meet the exponential growth of generative‑AI applications, which drives hardware orders across the supply chain.

Advancements in Chip Architecture

Recent innovations such as 3‑nm process nodes, tensor‑core optimizations, and on‑chip high‑bandwidth memory have reduced latency and increased throughput, making training chips more cost‑effective per operation. These technical gains encourage data‑center operators to replace legacy GPUs with next‑generation training accelerators.

➤ Training Chip (Datacenter AI) Market is being propelled by strategic investments from leading cloud providers.

In addition, collaborative roadmaps between semiconductor manufacturers and AI software developers streamline compiler support, further accelerating adoption of purpose‑built training silicon across hyperscale facilities.

MARKET CHALLENGES

Manufacturing Complexity

Fabricating advanced training chips demands sophisticated lithography equipment and tight process control, which limits the number of qualified foundries. This scarcity elevates lead times and makes capacity planning difficult for chip designers.

Other Challenges

Supply‑Chain Constraints

Global shortages of high‑purity silicon wafers and specialized packaging materials create bottlenecks that can delay product launches and increase unit costs for Training Chip (Datacenter AI) Market.

Thermal management at scale also presents a hurdle; densely packed training accelerators generate significant heat, requiring innovative cooling solutions that add to the overall datacenter OPEX.

MARKET RESTRAINTS

High Capital Expenditure

Deploying state‑of‑the‑art training chips involves substantial upfront investment in power delivery infrastructure, rack redesign, and software stack integration. Smaller cloud operators often delay adoption until economies of scale lower total cost of ownership.

Regulatory scrutiny over energy consumption in large‑scale AI facilities can impose additional compliance costs, further restraining rapid expansion of Training Chip (Datacenter AI) Market.

MARKET OPPORTUNITIES

Emerging Edge‑Datacenter Convergence

Hybrid architectures that blend edge inference with centralized training present a new revenue stream for chip vendors. By offering modular training accelerators that can be scaled from edge nodes to core datacenters, manufacturers can capture a broader portion of AI workloads.

In parallel, the rise of custom ASIC design services enables enterprises to tailor training chip specifications to niche AI models, driving differentiated product offerings and higher margin opportunities withTraining Chip (Datacenter AI) Market.

Training Chip (Datacenter AI) Market Trends

Accelerating Demand for Generative AI Services

The surge in generative AI applications is reshaping compute requirements across hyperscale datacenters. Providers are prioritizing hardware that can absorb massive model‑training workloads, driving the adoption of specialized Training Chip (Datacenter AI) Market solutions. These chips deliver higher throughput per watt, reducing operational expenses while meeting latency expectations for emerging services such as real‑time content synthesis and code generation. In addition, the convergence of AI with cloud‑native orchestration tools enables dynamic allocation of training jobs, cutting idle capacity and improving overall utilisation. Vendors are also embedding silicon‑level security features to protect proprietary model parameters, a concern that is increasingly influencing procurement decisions. Moreover, the rise of AI‑as‑a‑service platforms is prompting service providers to standardise on training chip families that enable multi‑tenant isolation and rapid provisioning, reducing capital outlay for individual enterprises. Edge‑located micro‑datacenters are also adopting scaled‑down versions of these chips to support latency‑sensitive inference‑training loops, further widening the market’s deployment scenarios.

Other Trends

Strategic Cloud Partnerships

Leading cloud operators have cemented collaborations that accelerate deployment cycles. NVIDIA’s March 2024 alliance with Microsoft Azure integrates next‑generation GPUs optimized for large‑scale training, while Google’s rollout of fourth‑generation TPUs extends its service catalog for enterprise AI workloads. These joint initiatives enhance the market’s credibility and encourage rapid adoption among customers seeking turnkey AI infrastructure. The partnerships also incorporate joint research programs that explore transformer‑scale training optimisations and supply‑chain co‑design, guaranteeing that emerging silicon matches cloud service roadmaps. Consequently, hyperscale operators observe shorter time‑to‑market for novel AI offerings, underscoring the strategic importance of the sector for both hardware makers and cloud providers.

Advances in Chip Architecture and Energy Efficiency

Recent semiconductor roadmaps emphasize heterogeneous integration and on‑die memory that boost data locality. By embedding high‑bandwidth memory alongside compute cores, newer models achieve up to 30 percent lower power draw for equivalent training throughput. This efficiency gain positions the market to satisfy sustainability targets across global datacenters, while delivering the performance bandwidth required for next‑generation foundation models. Emerging regulatory standards that reward energy‑efficient computing reinforce the shift toward low‑power silicon, and forthcoming advances in 3‑D stacking and chip‑let composability are projected to double training capacity within the same rack footprint. Such innovations cement the market’s role as a critical catalyst for AI evolution. Industry analysts expect continued acceleration through 2028.

COMPETITIVE LANDSCAPE

Key Industry Players

Training Chip (Datacenter AI) Market Competitive Landscape

Training Chip market is currently led by a handful of megacorporations that command the majority of revenue and set the technical direction for datacenter AI acceleration. NVIDIA dominates with its H100 and forthcoming Hopper‑based GPUs, leveraging deep integration with Microsoft Azure and a robust software stack that simplifies scaling of large language models. Google’s fourth‑generation Tensor Processing Units (TPUs) are closely competitive, offering custom ASICs that excel in matrix‑multiply throughput and are tightly coupled with Google Cloud’s AI services. AMD’s Instinct series has gained traction by delivering high‑bandwidth memory and open‑source ROCm drivers, attracting hyperscale operators seeking cost‑effective alternatives. Intel, through its acquisition of Habana Labs, provides Gaudi AI training processors that balance performance and power efficiency, reinforcing Intel’s position in both cloud and edge datacenters. Collectively these leaders shape market structure, driving pricing, roadmap cadence, and ecosystem standards.

Beyond the dominant tier, a vibrant niche of specialized firms adds depth and innovation to the competitive landscape. Graphcore’s IPU architecture focuses on graph‑centric workloads, delivering superior efficiency for certain model types. Cerebras Systems differentiates with its wafer‑scale engine, offering unprecedented memory bandwidth for massive models. Tenstorrent pursues a flexible dataflow design that targets a broad spectrum of AI workloads. Samsung and Huawei are expanding their semiconductor portfolios to include AI‑optimized training chips, aiming for regional market capture. Chinese cloud giants Alibaba, Tencent, and Baidu are also developing proprietary accelerators to reduce reliance on Western suppliers and to tailor performance for their AI services. These niche players, while smaller in revenue, contribute critical diversification and often drive breakthroughs that influence the strategies of the market leaders.

List of Key Training Chip (Datacenter AI) Companies Profiled

- NVIDIA

- AMD

- Google (Alphabet)

- Intel (including Habana Labs)

- Microsoft (Azure AI)

- Alibaba Cloud

- Tencent Cloud

- Baidu AI

- Samsung Electronics

- Huawei Technologies

- Graphcore

- Cerebras Systems

- Tenstorrent

- Qualcomm AI Research

- Alibaba DAMO Academy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GPU‑based training chips dominate due to their flexible programming model and rapid ecosystem support.

|

| By Application |

|

Large‑scale model training is the primary driver, requiring massive parallel compute and high‑bandwidth memory.

|

| By End User |

|

Hyperscale cloud providers lead adoption, shaping the market through large‑volume deployments.

|

| By Architecture |

|

Tensor‑core optimized architecture is favored for its ability to accelerate mixed‑precision workloads.

|

| By Deployment Mode |

|

Managed cloud AI services accelerate market penetration by abstracting hardware complexity.

|

Regional Analysis:

United States

The primary drivers in the US market include increasing adoption of AI across various industries like healthcare, finance, and automotive, the growing demand for cloud-based AI services, and the continuous evolution of deep learning algorithms requiring more powerful processors.

The competitive landscape is intensely contested by established players like NVIDIA and AMD, alongside emerging chip designers and specialized AI accelerator companies. Partnerships between hardware and software providers are becoming increasingly common to deliver optimized AI solutions.

Key technological trends include the development of specialized AI accelerators, advancements in chiplet designs for enhanced scalability, and the increasing adoption of heterogeneous computing architectures combining CPUs, GPUs, and specialized AI chips.

Significant investments are being directed towards AI infrastructure, including the construction of new data centers and the expansion of existing ones to support the growing demand for training chips. Government funding and private equity are fueling this growth.

Europe

Europe is rapidly emerging as a significant player Training Chip (Datacenter AI) Market, driven by strong government support for digital transformation and a growing ecosystem of AI startups. Countries like Germany, France, and the UK are actively investing in AI research and development, creating a favorable environment for chip manufacturers and AI solution providers. The focus in Europe is particularly strong on energy-efficient AI solutions and the development of chips optimized for edge computing applications. However, the market faces challenges related to fragmented regulatory landscapes and the need for greater standardization to facilitate wider adoption. Collaboration between European research institutions and industry players is crucial for fostering innovation and competitiveness in this rapidly evolving field. The commitment to sustainable technology is influencing chip design towards lower power consumption.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for Training Chips (Datacenter AI). China is leading the charge, with substantial investments in AI infrastructure and a rapidly expanding domestic market. Other key markets in the region include Japan, South Korea, and India, each with unique growth drivers and challenges. The demand for training chips is primarily fueled by the growth of cloud computing, e-commerce, and the increasing adoption of AI in manufacturing and healthcare. The region is witnessing a rise in local chip design companies, challenging the dominance of established players. Government policies promoting domestic semiconductor manufacturing are also playing a significant role in the market dynamics. The emphasis is on cost-effectiveness and scalability to cater to the vast data processing needs of the region.

North America

North America, particularly the United States and Canada, remains at the forefront of innovation Training Chip (Datacenter AI) Market. The region boasts a strong foundation in semiconductor technology, a robust AI ecosystem, and substantial investment in research and development. Large tech corporations and established semiconductor manufacturers are key drivers of growth. Demand is concentrated in data centers, cloud computing, and AI-driven applications across industries. The focus is on high-performance, energy-efficient chips and the development of specialized accelerators. Government initiatives and venture capital funding are fostering further innovation and expansion.

South America

South America is an emerging market for Training Chips (Datacenter AI), with growth potential driven by increasing adoption of cloud services and AI in sectors like finance and retail. Brazil and Argentina are key markets, with growing investments in digital infrastructure. However, the market is still relatively nascent, facing challenges related to limited investment and infrastructure constraints. The demand for cost-effective and scalable AI solutions is a key factor driving market growth. The focus is on leveraging AI for optimization and automation across various industries.

Middle East & Africa

The Middle East & Africa region presents a long-term growth opportunity for Training Chip (Datacenter AI) Market. Countries like Saudi Arabia, the UAE, and South Africa are investing in digital transformation initiatives, driving demand for AI infrastructure. The region’s focus is on leveraging AI for smart cities, healthcare, and industrial automation. While the market is currently small, it is expected to witness significant growth in the coming years, driven by increasing government investments and a growing awareness of AI’s potential. The demand for energy-efficient solutions is particularly relevant in the region’s hot climate.

Report Scope

This market research report provides a comprehensive analysis of the Training Chip (Datacenter AI) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Training Chip (Datacenter AI) Market?

-> Training Chip (Datacenter AI) Market was valued at USD 8.3 billion in 2025 and is expected to reach USD 22.7 billion by 2034, growing at a CAGR of 11.3% during the forecast period.

Which key companies operate Training Chip (Datacenter AI) Market?

-> Key players include NVIDIA, Google, Intel, AMD, and Graphcore, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for generative AI services, increased investments by cloud providers in AI infrastructure, and breakthroughs in chip architecture that improve performance per watt.

Which region dominates the market?

-> North America remains the dominant market, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include deployment of next‑generation GPUs such as NVIDIA H100, fourth‑generation TPUs, and specialized AI accelerators optimized for large‑scale model training.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...