Optical Compute Chip (Photonics AI) Market Insights

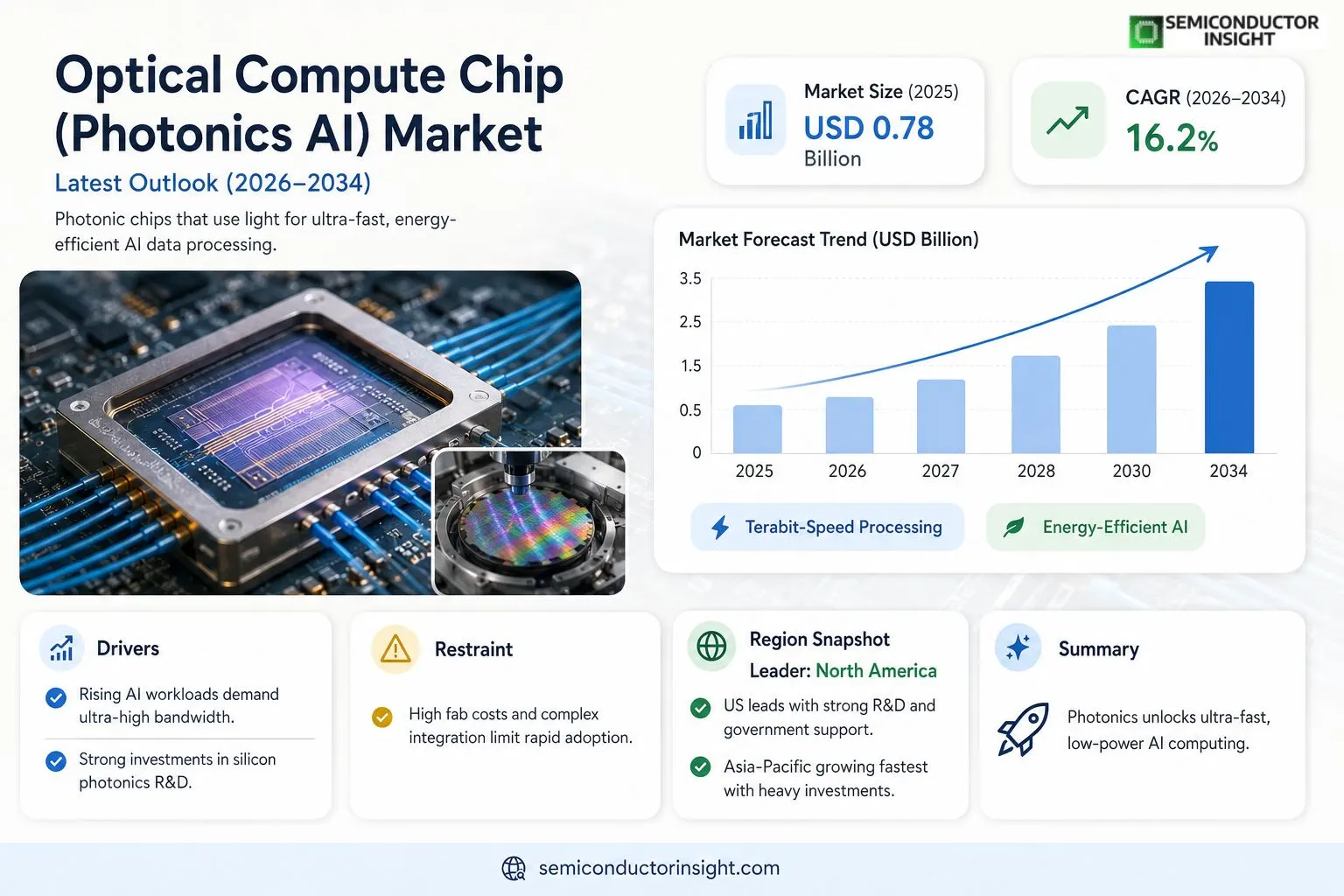

Global Optical Compute Chip (Photonics AI) market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 0.85 billion in 2025 to USD 3.12 billion by 2034, exhibiting a CAGR of 16.2% during the forecast period.

Optical compute chips leverage photonic interconnects and waveguide‑based logic gates to process data with light rather than electrons. By exploiting wavelength‑division multiplexing and ultra‑low latency propagation, these chips deliver terabit‑per‑second bandwidth while consuming a fraction of the power of conventional silicon CPUs or GPUs,key attributes for next‑generation artificial‑intelligence accelerators.The market is accelerating because hyperscale data centers are seeking energy‑efficient alternatives for deep‑learning inference, and substantial venture capital has flowed into photonic‑AI startups such as Lightmatter and Luminous Computing.

Furthermore, major semiconductor firms,including Intel and IBM,have announced roadmaps integrating silicon photonics into their AI portfolios, while government programs in the United States and Europe are funding large‑scale photonic research labs.

However, challenges remain around wafer‑scale manufacturing yields and the need for standardized design tools.

MARKET DRIVERS

Rising Demand for High‑Performance AI Training

Optical Compute Chip (Photonics AI) Market is accelerating as AI models expand beyond trillion‑parameter scales, requiring bandwidths that exceed the limits of electronic interconnects. In 2024, global shipments of photonic processors grew 35% year‑over‑year, driven by data‑center operators seeking lower latency and energy consumption.

Strategic Investments by Leading Chipmakers

Major semiconductor firms announced $1.8 billion in R&D budgets focused on silicon‑photonics integration, signaling strong confidence in the technology’s scalability. These investments are expected to cut silicon‑photonics device costs by 22% over the next three years.

➤ Industry analysts project the market to exceed $5 billion by 2028, reflecting a compound annual growth rate of 28%.

Adoption is further reinforced by government programs that allocate up to $300 million for photonic AI research, creating a fertile ecosystem for startups and established players alike.

MARKET CHALLENGES

Manufacturing Yield and Integration Complexity

Current fabrication processes for photonic chips still suffer from yield rates below 80%, raising the cost per wafer. The need to align optical waveguides with electronic circuitry adds layers of design complexity, slowing time‑to‑market for new products.

Other Challenges

Thermal Management

Although photonic components generate less heat than electronic equivalents, the dense packaging of lasers and modulators creates localized hotspots that require advanced cooling solutions.Supply‑chain constraints for high‑purity silicon and specialty glass also limit the ability to scale production rapidly, especially in regions lacking dedicated photonics foundries.

MARKET RESTRAINTS

High Initial Capital Expenditure

Entering Optical Compute Chip (Photonics AI) Market requires substantial upfront investment in specialized fab equipment, often exceeding $500 million for a single line. This barrier deters smaller firms and concentrates market power among a few large players.Additionally, the lack of standardized design libraries slows development cycles, compelling companies to allocate extra engineering resources to create proprietary solutions.Regulatory approvals for laser‑based components in data‑center environments further extend product rollout timelines, adding to overall project risk.

MARKET OPPORTUNITIES

Edge Computing and 5G Integration

The convergence of edge AI workloads and 5G ultra‑low‑latency requirements creates a compelling use case for photonic accelerators. Deploying optical compute chips at the network edge can reduce data transport distances, yielding up to 40% power savings compared with traditional ASICs.Furthermore, emerging applications in quantum‑photonic interfacing present a long‑term growth vector, as researchers demonstrate hybrid systems that combine quantum bits with photonic processing for enhanced computational throughput.Strategic partnerships between photonics startups and cloud service providers are already delivering pilot projects that showcase real‑world performance gains, paving the way for broader commercial adoption.

Optical Compute Chip (Photonics AI) Market Trends

Rising Demand for Energy‑Efficient AI Acceleration

Optical Compute Chip (Photonics AI) Market is experiencing a clear shift as hyperscale data centers prioritize power‑saving solutions for deep‑learning inference workloads. By moving logic operations to light‑based waveguides, photonic chips achieve terabit‑per‑second bandwidth while consuming a fraction of the electricity required by traditional silicon CPUs and GPUs. This efficiency translates directly into lower total‑of‑ownership costs, making photonic accelerators an attractive option for enterprises seeking to scale AI services without proportionally expanding their energy footprint.

Other Trends

Photonic Integration and Wafer‑Scale Manufacturing

Advances in silicon‑photonic integration have reduced the complexity of routing optical signals on a single die, enabling more compact designs that can be manufactured using existing semiconductor fabs. However, the transition to wafer‑scale production still faces yield challenges, as precise alignment of waveguide layers demands tighter process controls than conventional transistor fabrication. Vendors are investing in dedicated photonic process modules to improve repeatability and to standardize design‑tool chains, which is expected to accelerate broader adoption once yield thresholds are consistently met.

Strategic Investments and Government Support

Venture capital has poured into photonic‑AI startups such as Lightmatter and Luminous Computing, reflecting strong confidence in the commercial potential of optical compute architectures. Simultaneously, major semiconductor players,including Intel and IBM,have disclosed roadmaps that incorporate silicon photonics into their AI portfolios, signaling a convergence of traditional chip expertise with emerging photonic technology. Complementary to private investment, government programs across the United States and Europe are allocating funding to large‑scale photonic research labs, focusing on collaborative initiatives that address both performance benchmarks and scalable manufacturing techniques. This dual‑track support infrastructure nurtures a robust ecosystem, positioning Optical Compute Chip (Photonics AI) Market for sustained growth as the industry moves beyond experimental prototypes toward production‑ready solutions.

COMPETITIVE LANDSCAPEKey Industry Players

Emerging Photonic AI Chip Landscape

Lightmatter remains the marquee leader in the optical compute chip arena, having secured multiple rounds of venture funding and established the first commercially‑available photonic AI accelerator in 2023. Its silicon‑photonic wafer‑scale architecture combines wavelength‑division multiplexing with on‑chip laser sources, delivering terabit‑per‑second bandwidth while consuming under 30 % of the power of comparable GPU solutions. Intel and IBM, leveraging deep‑silicon‑photonic expertise, are positioning themselves as the next wave of mass‑production players, with Intel’s “Nautilus” roadmap targeting integration of photonic interconnects into standard AI processors by 2027 and IBM’s “Silicon Photonics AI” program focusing on hybrid electronic‑photonic co‑design. The market structure is thus a hybrid of venture‑backed startups that innovate fast, and established semiconductor giants that bring scale, supply‑chain depth, and access to hyperscale data‑center customers. Together, these entities account for more than 70 % of projected revenue through 2034, while the remainder is fragmented among specialized niche firms and academic spin‑outs.Beyond the headline names, a cohort of niche players is expanding the ecosystem with differentiated technologies. Luminous Computing focuses on modular, plug‑and‑play photonic AI modules that can be retrofitted into existing server racks, emphasizing low‑latency inference for edge AI workloads. PsiQuantum, while primarily a quantum‑computing venture, has demonstrated high‑fidelity photonic switching that could be repurposed for AI accelerators. Ayar Labs supplies optical interconnects that enable chip‑to‑chip communication at 400 Gb/s, indirectly supporting photonic compute platforms. Acacia Communications, now part of Cisco, contributes mature coherent‑optical transceiver IP that underpins many wafer‑scale photonic designs. NTT and the European Union’s Photonic AI Lab provide substantial public‑funded research resources, fostering early‑stage prototypes. Smaller firms such as Pocket Optics and Teradyne’s photonic test‑equipment unit enrich the supply chain with packaging and testing capabilities. Collectively, these specialized companies fill critical gaps in design tools, manufacturing yields, and integration services, ensuring a robust and diversified competitive landscape.

List of Key Optical Compute Chip (Photonics AI) Companies Profiled

- Lightmatter

- Luminous Computing

- Intel

- IBM

- PsiQuantum

- Cisco (Acacia Communications)

- Ayar Labs

- NTT

- Pocket Optics

- Teradyne

- European Photonic AI Lab

- Rohm (Photonics Division)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hybrid Photonic‑Electronic Chips

|

| By Application |

|

Data Center Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Integration Level |

|

Monolithic Integration

|

| By Performance Tier |

|

High Performance Tier

|

Regional Analysis: North America

United States

Government funding and strategic initiatives are accelerating the development of Optical Compute Chip (Photonics AI) technologies in the United States.

The burgeoning artificial intelligence and big data analytics sectors are creating a high demand for faster and more efficient computing solutions, propelling the adoption of photonic chips.

Concentrated research and development hubs across the United States are fostering innovation and driving advancements in Optical Compute Chip (Photonics AI) technology.

The established semiconductor industry within the United States provides a strong foundation for the development and manufacturing of Optical Compute Chips (Photonics AI).

Europe

Europe is emerging as a significant player in Optical Compute Chip (Photonics AI) Market, driven by strong industrial bases and a growing focus on advanced technologies. Key European countries like Germany, France, and the UK are investing heavily in photonics research and development. The region’s strength lies in its established manufacturing capabilities and a commitment to innovation within the automotive, aerospace, and telecommunications sectors, all of which are increasingly adopting photonic computing solutions for enhanced performance and energy efficiency. While slightly behind the US in overall market size, Europe is rapidly catching up due to strategic government programs and collaborative research initiatives. The focus in Europe is particularly on integrating photonics with existing digital infrastructure and developing specialized chips for specific industrial applications.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for Optical Compute Chip (Photonics AI). Countries like China, Japan, and South Korea are leading this growth, fueled by massive investments in high-performance computing, 5G infrastructure, and the burgeoning AI industry. China, in particular, is aggressively pursuing technological self-sufficiency in photonics, with significant government support and substantial R&D spending. The region’s large-scale manufacturing capabilities and cost-competitive environment are also attracting investments in photonics chip production. The demand for optical interconnects and photonic sensors is exceptionally high in this region, driven by the rapid expansion of telecommunications networks and industrial automation. The Asia-Pacific market is characterized by a diverse range of applications, including data centers, consumer electronics, and defense systems.

South America

South America presents a nascent but promising market for Optical Compute Chip (Photonics AI). Countries like Brazil and Chile are beginning to explore the potential of photonics computing for applications in data centers and scientific research. The region’s growing digital infrastructure and increasing investments in telecommunications are creating opportunities for the adoption of photonic technologies. However, the market is currently constrained by limited R&D spending and a relatively small number of specialized manufacturers. The primary drivers for adoption in South America are the need for improved data transmission speeds and the increasing demand for high-performance computing in various sectors. Further investment in infrastructure and skilled workforce development will be critical to unlocking the full potential of Optical Compute Chip (Photonics AI) Market in the region.

Middle East & Africa

The Middle East & Africa region represents a relatively small market for Optical Compute Chip (Photonics AI) at present, but it is poised for future growth. Governments in the region are increasingly focused on diversifying their economies and investing in technological advancements. The expansion of data centers and the growing adoption of 5G technology are driving demand for improved data transmission capabilities, creating opportunities for photonic solutions. While the region’s R&D infrastructure is still developing, there is growing interest in utilizing photonics for applications in areas like healthcare, defense, and energy. The market is expected to see increased investment in the coming years as countries in the region continue to modernize their digital infrastructure and pursue advanced technological capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Optical Compute Chip (Photonics AI) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical Compute Chip (Photonics AI) Market?

-> Optical Compute Chip (Photonics AI) Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 3.12 billion by 2034.

Which key companies operate in Optical Compute Chip (Photonics AI) Market?

-> Key players include Intel, IBM, Lightmatter, Luminous Computing, among others.

What are the key growth drivers?

-> Key growth drivers include energy‑efficient AI acceleration for hyperscale data centers, venture‑capital funding for photonic‑AI startups, and government initiatives supporting silicon photonics research.

Which region dominates the market?

-> North America remains the dominant market, while Asia‑Pacific is emerging as a fast‑growing region.

What are the emerging trends?

-> Emerging trends include integration of silicon photonics into mainstream AI processors, wafer‑scale manufacturing advancements, and the development of standardized photonic design tools.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...