In-Memory Computing Chip Market Insights

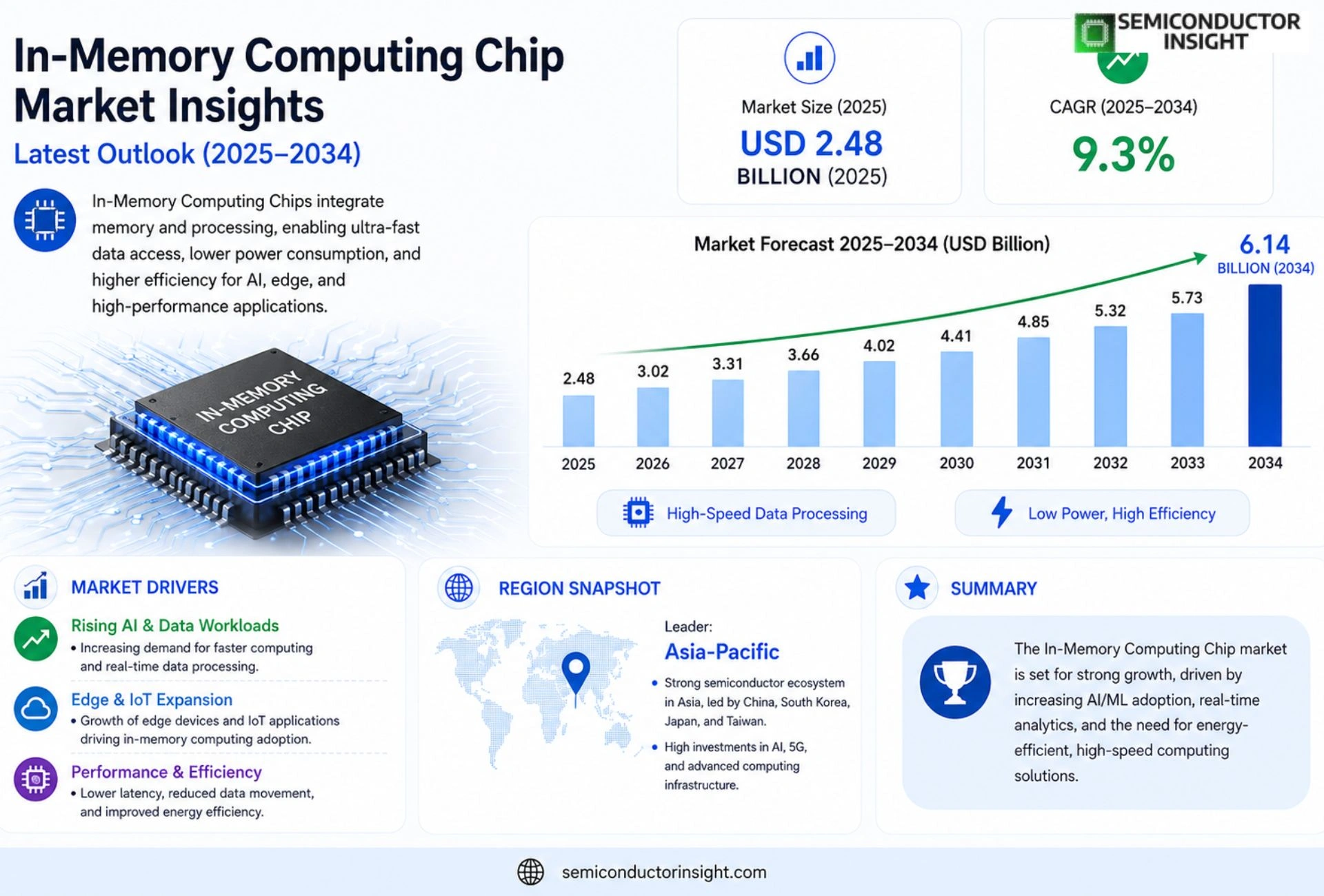

Global In‑Memory Computing Chip Market size was valued at USD 2.48 billion in 2025. The market is projected to grow from USD 3.02 billion in 2026 to USD 6.14 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

In‑memory computing chips are specialized semiconductor devices that perform data processing directly within memory arrays, eliminating the latency associated with data transfer between separate CPU and memory units. These chips leverage technologies such as resistive RAM (RRAM), phase‑change memory (PCM) and spin‑transfer torque MRAM to enable ultra‑fast analytics, AI inference and real‑time decision making.

The market is experiencing rapid growth because enterprises are demanding sub‑microsecond response times for high‑frequency trading, autonomous systems and large‑scale AI workloads. However, challenges remain in manufacturing yield and integration with existing architectures; nevertheless, continued R&D investments and strategic partnerships,such as the 2023 collaboration between Samsung Electronics and IBM on next‑generation MRAM,are expected to accelerate adoption across cloud providers and edge devices.

MARKET DRIVERS

Rising Demand for Real‑Time Data Processing

In-Memory Computing Chip Market is being propelled by enterprises that require sub‑millisecond latency for analytics, AI inference, and high‑frequency trading. Modern workloads generate petabytes of data daily, and conventional storage hierarchies cannot keep pace, driving customers toward memory‑first architectures.

Adoption of Edge‑AI and 5G Applications

Edge devices and 5G infrastructure are increasingly embedding specialized chips that process data directly in memory, reducing bandwidth consumption and power usage. This trend expands the addressable market across automotive, IoT, and smart‑city deployments.

➤ “Memory‑centric designs can shave up to 70% of energy per operation compared with traditional CPU‑DRAM pipelines.”

Investment from major semiconductor firms in custom memory‑compute solutions further validates the growth trajectory, as they integrate AI accelerators with high‑bandwidth memory stacks to meet enterprise performance targets.

MARKET CHALLENGES

Complexity of Integration with Existing Systems

Many organizations face significant engineering effort when retrofitting legacy applications to leverage in‑memory chips, resulting in higher upfront costs and extended deployment timelines.

Other Challenges

Thermal Management Constraints

The dense interconnects and high activity rates generate heat that must be efficiently dissipated, adding design complexity and potentially limiting scalability in data centers.

MARKET RESTRAINTS

High Capital Expenditure

Deploying large‑scale in‑memory solutions requires substantial upfront investment in hardware, cooling infrastructure, and skilled personnel, which can deter cost‑sensitive enterprises.

Limited Software Ecosystem

While hardware capabilities advance rapidly, the surrounding software stack,compilers, libraries, and development tools,lags, creating a bottleneck for broader adoption.

Regulatory and data‑sovereignty concerns in certain regions also impose restrictions on where memory‑intensive workloads can be processed, further constraining market expansion.

MARKET OPPORTUNITIES

Emergence of AI‑Driven Cloud Services

Cloud providers are integrating in‑memory chips to accelerate AI model training and inference, offering differentiated services that command premium pricing and open new revenue streams for chip manufacturers.

Growth in Real‑Time Analytics Platforms

Industries such as finance, telecommunications, and biotechnology are investing in platforms that require instant insights. The need for ultra‑fast data access creates a fertile environment for In-Memory Computing Chip Market to capture value.

In-Memory Computing Chip Market Trends

Rise of Near‑Memory Architectures

The In‑Memory Computing Chip Market is being reshaped by the growing requirement for sub‑microsecond response times in high‑frequency trading, autonomous platforms, and large‑scale AI inference. By embedding compute units directly within memory arrays, manufacturers eliminate the data‑movement bottleneck that traditionally hampers CPU‑centric designs. This architectural shift enables developers to achieve ultra‑fast analytics while reducing overall system power consumption, a combination that is increasingly valued by cloud providers and edge device makers.

Other Trends

Manufacturing Yield and Integration

Despite the clear performance benefits, the industry faces practical hurdles related to fabrication yield and seamless integration with existing semiconductor ecosystems. Yield variability in emerging technologies such as resistive RAM (RRAM), phase‑change memory (PCM) and spin‑transfer‑torque MRAM requires sustained investment in process optimisation. Collaborative programmes,exemplified by the 2023 partnership between Samsung Electronics and IBM,are focusing on defect reduction and design‑for‑manufacturability, thereby lowering barriers for broader adoption across data‑center and edge deployments.

Emerging Memory Technologies Driving Expansion

Parallel to yield improvements, the market is witnessing accelerated research into novel memory cells that promise higher density and lower latency. RRAM’s ability to toggle resistance states without charge movement, PCM’s rapid phase transitions, and the non‑volatile nature of MRAM each contribute distinct advantages for specific workload profiles. As these technologies mature, they are expected to diversify the solution portfolio within the In‑Memory Computing Chip Market, allowing system architects to match memory‑compute characteristics to application requirements such as real‑time decision making in autonomous vehicles or massive parallelism in AI training clusters.

Overall, the convergence of demand for instantaneous data processing, strategic alliances aimed at overcoming manufacturing constraints, and the steady emergence of next‑generation memory primitives creates a robust growth trajectory for the In‑Memory Computing Chip Market. Stakeholders that align product roadmaps with these trend vectors are positioned to capture competitive advantage while supporting the broader digital transformation agenda across industries.

COMPETITIVE LANDSCAPE

Key Industry Players

In-Memory Computing Chip Market Competitive Landscape

The market is currently dominated by a handful of large semiconductor firms that have integrated in‑memory computing (IMC) into their product portfolios. Samsung Electronics leads the space, leveraging its 2023 collaboration with IBM to advance MRAM technologies that target sub‑microsecond AI inference workloads. Intel and Micron follow closely, each offering RRAM‑based solutions that are gaining traction in high‑frequency trading platforms and edge‑AI devices. These tier‑one players benefit from deep fabrication capacity, extensive IP portfolios, and established relationships with cloud providers, positioning them to capture the bulk of the projected USD 6.14 billion market by 2034.

Beyond the dominant tier, a vibrant ecosystem of specialized innovators is expanding the technology frontier. Fujitsu’s PCM chips, HP’s spin‑transfer torque MRAM, and SK Hynix’s emerging ReRAM modules address niche segments such as autonomous vehicle control and real‑time analytics. Smaller firms like Nantero, Everspin, and GSI Technology focus on emerging memory architectures that promise higher density and lower power consumption. Start‑ups including Cognitive Computing Inc. and HPE Labs are also contributing through partnerships and joint‑development agreements, accelerating integration of IMC across data‑center and edge environments.

List of Key In-Memory Computing Chip Companies Profiled

- Samsung Electronics

- Intel Corporation

- Micron Technology

- IBM

- Fujitsu

- SK Hynix

- HP Inc.

- Nantero

- Everspin Technologies

- GSI Technology

- Cognitive Computing Inc.

- HPE Labs

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Resistive RAM (RRAM)

|

| By Application |

|

High‑Frequency Trading

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

3D Stacked Memory

|

| By Deployment Model |

|

Edge Devices

|

Regional Analysis: North America

North America

The data center segment in North America is a major consumer of in-memory computing chips, driven by the exponential growth of data volumes and the need for faster analytics and application performance.

The financial services industry is heavily reliant on real-time processing for fraud detection, risk management, and high-frequency trading, creating a significant demand for high-performance in-memory computing solutions.

In healthcare, in-memory computing enables faster analysis of patient data, supporting improved diagnostics, personalized medicine, and real-time monitoring.

The telecommunications sector utilizes in-memory computing for real-time network optimization, customer analytics, and service delivery enhancements.

North America

The North American In-Memory Computing Chip Market is characterized by a proactive approach to technological advancement. Several key trends are shaping its trajectory. One prominent trend is the increasing adoption of hybrid cloud environments, requiring solutions that can seamlessly operate across on-premise and cloud infrastructure. This is driving demand for in-memory computing platforms that offer portability and scalability. Businesses are also focusing on optimizing their data infrastructure to accommodate the growing volume and velocity of data, further propelling the need for faster data processing capabilities. Business strategies revolve around offering specialized in-memory solutions tailored to specific industry verticals, such as finance and healthcare, and developing robust security features to address growing data privacy concerns. The emphasis is on delivering high-performance, energy-efficient chips that can meet the evolving demands of modern applications.

Europe

Europe represents a steadily growing market for In-Memory Computing Chips. Driven by increasing investments in digital transformation and a growing focus on data-driven decision-making, the demand for real-time analytics and high-performance computing is on the rise. The adoption rate is gradually increasing across various industries, including finance, automotive, and manufacturing. European companies are particularly interested in energy-efficient solutions and those that align with data privacy regulations like GDPR. Business strategies in Europe focus on partnerships with system integrators and cloud providers to expand market reach and offer comprehensive solutions. There’s a notable emphasis on developing in-memory computing solutions for edge computing applications.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing market for In-Memory Computing Chips, propelled by rapid industrialization, increasing digital penetration, and significant investments in technology. Countries like China, Japan, and South Korea are leading the way in adopting in-memory computing solutions for applications such as e-commerce, financial services, and manufacturing. The region’s strong focus on 5G and IoT is further fueling demand for these chips. Business strategies in Asia-Pacific are centered around cost-effective solutions and collaborations with local partners to address specific regional needs. The market is witnessing a rise in local chip manufacturers and innovative startups.

South America

South America is a relatively nascent market for In-Memory Computing Chips, but with significant growth potential. The increasing adoption of cloud computing and the rising demand for data analytics are driving initial interest. The financial services and e-commerce sectors are key early adopters. Business strategies focus on providing pilot projects and educational initiatives to demonstrate the value proposition of in-memory computing. Cost considerations play a critical role in adoption decisions in this region.

Middle East & Africa

The Middle East & Africa region presents a promising, albeit early-stage, market for In-Memory Computing Chips. Investments in smart city initiatives, digital infrastructure, and government-led technological advancements are expected to drive growth. Key application areas include government services, finance, and telecommunications. Business strategies emphasize tailored solutions addressing the specific challenges and opportunities in the region, including considerations for climate and infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the In-Memory Computing Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of In-Memory Computing Chip Market?

-> In-Memory Computing Chip Market was valued at USD 2.48 billion in 2025 and is expected to reach USD 6.14 billion by 2034.

Which key companies operate in In-Memory Computing Chip Market?

-> Key players include Samsung Electronics and IBM, which have announced strategic collaborations on next‑generation MRAM technologies.

What are the key growth drivers?

-> Key growth drivers include enterprise demand for sub‑microsecond response times in high‑frequency trading, autonomous systems, and large‑scale AI workloads, driving adoption of ultra‑fast in‑memory processing.

Which region dominates the market?

-> The reference does not specify a dominant region for the In‑Memory Computing Chip Market.

What are the emerging trends?

-> Emerging trends include advancements in resistive RAM (RRAM), phase‑change memory (PCM), and spin‑transfer torque MRAM technologies, as well as integration of these chips with AI/IoT edge and cloud platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...