Heterogeneous Compute Chiplet Platform Market Insights

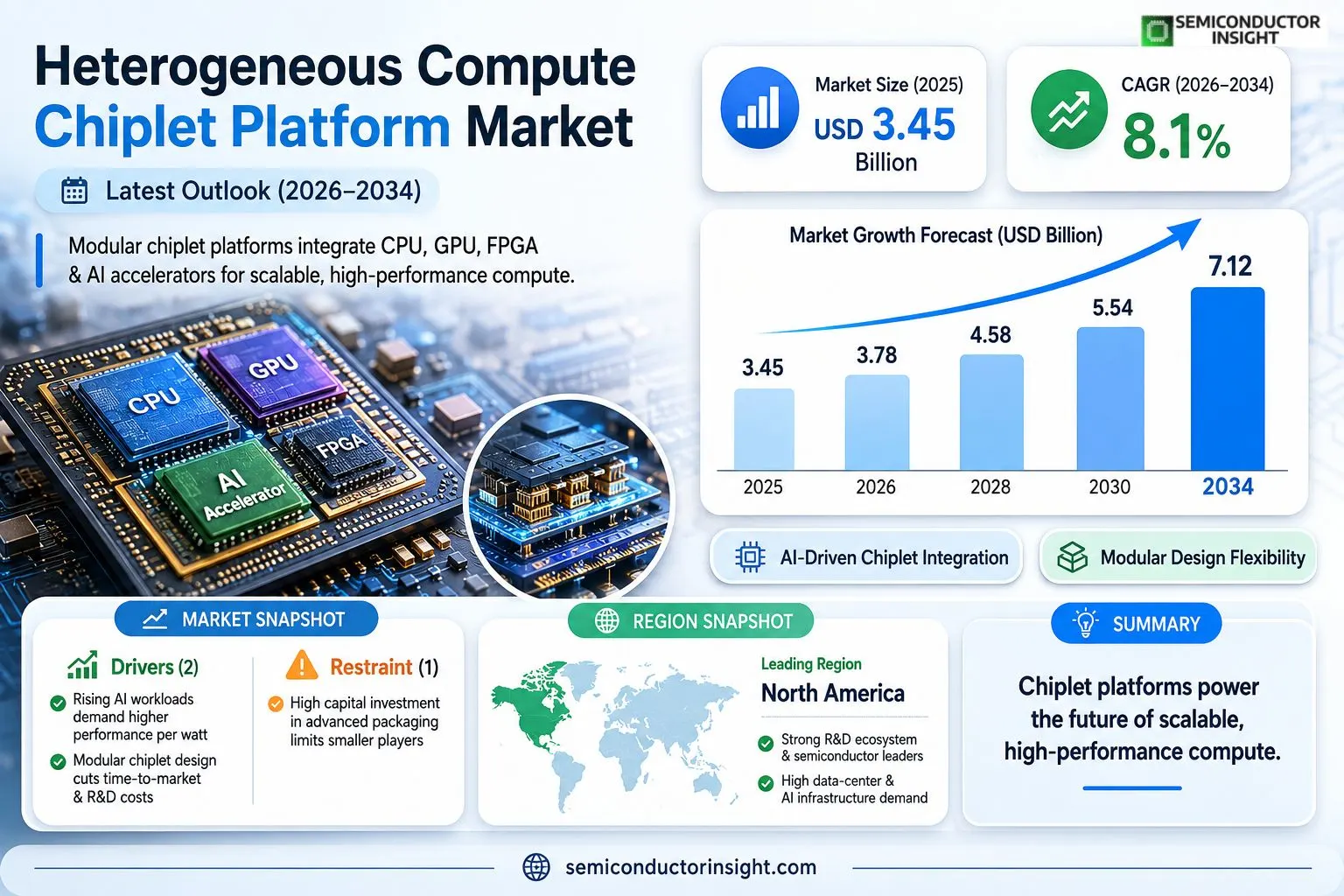

Global Heterogeneous Compute Chiplet Platform Market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.78 billion in 2026 to USD 7.12 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period.

Heterogeneous compute chiplet platforms integrate multiple specialized silicon dies,such as CPU, GPU, FPGA, and AI accelerators,into a single package using advanced interconnect technologies like silicon photonics or high‑density EMIB. This modular approach enables designers to tailor performance, power, and cost for emerging workloads while shortening time‑to‑market.The market is accelerating because data‑center operators demand higher throughput for AI inference and training, while semiconductor firms invest heavily in chiplet ecosystems to overcome lithography limits. Furthermore, collaborations such as Intel’s partnership with TSMC on advanced packaging and AMD’s acquisition of Xilinx’s chiplet IP are fueling adoption across cloud providers and edge devices.

MARKET DRIVERS

Performance Scaling and Power Efficiency

The surge in demand for high‑performance computing across data centers and edge AI workloads is driving manufacturers to adopt heterogeneous compute chiplet platforms. By integrating specialized compute, memory, and interconnect chiplets, system designers achieve significant gains in performance per watt, meeting the stringent efficiency targets of modern enterprises.

Modular Design Flexibility

Chiplet‑based architectures allow vendors to mix and match functional blocks without redesigning full wafers, reducing time‑to‑market and R&D costs. This modularity also enables rapid response to emerging standards such as Compute Express Link (CXL), further accelerating adoption.

➤ “Modularity is the new silicon paradigm, unlocking faster innovation cycles for compute platforms.”

Investor confidence is bolstered by the steady rise in firmware and software ecosystem support, which translates into broader market acceptance and sustained revenue growth for Heterogeneous Compute Chiplet Platform Market.

MARKET CHALLENGES

Integration Complexity and Validation

While chiplet integration offers flexibility, the complexity of high‑speed interconnects and thermal management presents a formidable engineering hurdle. Validation cycles can extend, increasing development costs for early adopters.

Other Challenges

Supply Chain Constraints

Limited availability of advanced packaging facilities and specialized silicon substrates can delay production, creating bottlenecks that affect overall market momentum.

MARKET RESTRAINTS

High Capital Expenditure

The initial investment required for sophisticated assembly equipment and test infrastructure remains prohibitive for smaller players, limiting competitive diversity in the market.Moreover, uncertainties around long‑term standards convergence deter some enterprises from committing sizable budgets to chiplet‑based solutions.

MARKET OPPORTUNITIES

Emerging AI Edge Applications

Growth in edge AI inference and autonomous systems creates a significant opportunity for heterogeneous compute chiplet platforms to deliver scalable performance within tight power envelopes.Additionally, collaborative industry consortia are shaping unified interconnect specifications, which will reduce integration risk and unlock new revenue streams for early adopters.

Heterogeneous Compute Chiplet Platform Market Trends

AI‑Driven Chiplet Integration Accelerates Data‑Center Performance

Data‑center operators are increasingly prioritizing heterogeneous compute chiplet platforms to meet the steep performance requirements of AI inference and large‑scale training. By assembling specialized dies such as CPUs, GPUs, and AI accelerators into a single package, designers achieve higher bandwidth while keeping power budgets modest. Advanced interconnects like silicon photonics and dense EMIB enable near‑memory speeds, reducing latency for matrix‑multiply operations that dominate deep‑learning workloads. Recent collaborations between leading semiconductor firms and advanced‑packaging specialists have shortened development cycles, allowing cloud providers to roll out AI‑optimized servers within months rather than years. The modular nature also supports heterogeneous memory integration, allowing high‑bandwidth memory stacks to be attached directly to compute dies, which further improves data locality for latency‑sensitive AI workloads. This capability is driving adoption in hyperscale facilities where power efficiency and compute density are critical differentiators.

Other Trends

Modular Packaging Advances

The shift toward modular packaging is reshaping supply chains by decoupling die fabrication from final assembly. Foundries can produce high‑yield CPU and GPU wafers while separate specialized vendors focus on interposer and substrate engineering. This separation reduces overall mask costs and permits designers to refresh individual functional blocks without redesigning the entire system‑on‑chip. Emerging standards for die‑to‑die communication, such as Chiplet‑Level‑Interface (CLi) specifications, are gaining traction, fostering interoperability across vendors. As a result, the time required to bring a new heterogeneous compute solution to market has dropped from several years to under twelve months, accelerating innovation cycles in both cloud and edge segments. In addition, thermal management solutions such as embedded micro‑fluidic cooling are being co‑designed with chiplet stacks, ensuring reliable operation at higher power densities. These innovations are especially valuable for edge AI accelerators where space constraints demand compact, high‑performance modules.

Ecosystem Consolidation and IP Licensing

The broader ecosystem is moving toward consolidation as major players acquire complementary chiplet IP portfolios, streamlining design flows and reducing integration risk. Licensing models that bundle verification suites with standardized interface libraries are enabling smaller design houses to adopt heterogeneous compute chiplet platforms without extensive in‑house validation. This trend is reinforced by open collaboration forums that publish reference designs and best‑practice guidelines, lowering barriers for entry across the market. Consequently, Heterogeneous Compute Chiplet Platform Market is poised to expand its user base beyond traditional data‑center manufacturers to include automotive, aerospace, and high‑performance networking vendors seeking differentiated performance. Moreover, standardized testing frameworks are emerging to certify compliance with power‑efficiency targets, further encouraging OEMs to select heterogeneous compute chiplet solutions for next‑generation products.

COMPETITIVE LANDSCAPEKey Industry Players

Heterogeneous Compute Chiplet Platform Market Overview

The market is currently anchored by a few vertically integrated semiconductor giants that control both design IP and advanced packaging capabilities. Intel remains the de‑facto leader, leveraging its EMIB and Foveros technologies to deliver high‑density CPU‑GPU‑FPGA chiplet solutions for hyperscale data‑centers. AMD, after acquiring Xilinx’s chiplet IP, combines Zen CPU cores with Radeon GPU dies, creating a compelling heterogeneous offering that challenges Intel’s dominance. TSMC’s CoWoS and InFO services provide the foundry backbone, enabling third‑party designers to assemble custom chiplet stacks while Samsung’s advanced packaging (I-Cube) and Qualcomm’s 3D System‑in‑Package (SiP) platforms expand the ecosystem for edge AI workloads. Collectively, these leaders drive a market projected to reach USD 7.12 billion by 2034, with a CAGR of roughly 8 % as cloud operators and AI developers seek modular, high‑performance compute blocks.Beyond the headline players, a vibrant cohort of specialized firms fuels niche adoption and innovation. Nvidia’s DGX‑Chiplet architecture integrates tensor cores with ARM CPU die for AI training acceleration, while Graphcore’s IPU‑centric chiplet approach targets machine‑learning inference at the edge. Cerebras introduces wafer‑scale chiplet arrays for extreme parallelism. Marvell, Broadcom, and IBM contribute high‑speed interconnect and networking die that enhance system‑level bandwidth. Huawei’s HiSilicon and GlobalFoundries’ design services round out the supply chain, offering cost‑effective alternatives for regional markets and emerging form‑factors. This diversified landscape ensures competitive pressure across performance, power, and price dimensions, encouraging continual refinement of silicon photonics, EMIB, and hybrid bond technologies.

List of Key Heterogeneous Compute Chiplet Platform Companies Profiled

- Intel Corporation

- Advanced Micro Devices (AMD)

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Samsung Electronics

- Qualcomm Incorporated

- NVIDIA Corporation

- Graphcore Ltd.

- Cerebras Systems

- Marvell Technology Group Ltd.

- Broadcom Inc.

- International Business Machines Corporation (IBM)

- Huawei Technologies Co., Ltd.

- GlobalFoundries Inc.

- Arm Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CPU‑Centric Chiplets dominate early design cycles due to their proven design ecosystems and ease of integration.

|

| By Application |

|

Data‑Center AI Workloads emerge as the primary driver for heterogeneous chiplet adoption.

|

| By End User |

|

Cloud Service Providers spearhead adoption thanks to their need for flexible compute fabrics.

|

| By Integration Technology |

|

Silicon Interposers are the leading integration avenue for high‑density heterogeneous designs.

|

| By Workload Focus |

|

AI Inference shapes the strategic roadmap for chiplet ecosystems.

|

Regional Analysis: North America

United States

The market in the United States is currently witnessing a surge in demand for advanced packaging technologies that enable the integration of diverse chiplets. A key trend is the increasing adoption of open standards and interoperability frameworks to facilitate seamless integration across different chiplet designs. Furthermore, there’s a growing emphasis on security features within heterogeneous compute platforms to address the escalating concerns related to data privacy and cyber threats.

The competitive landscape in the US market is characterized by the presence of established semiconductor giants and emerging startups. Key players are focusing on developing innovative chiplet architectures and expanding their product portfolios to cater to the diverse needs of end-users. Strategic collaborations and partnerships are becoming increasingly common as companies seek to leverage complementary expertise and resources to accelerate innovation and market penetration.

Companies operating in the US market are implementing various business strategies to gain a competitive edge. These include focusing on specialized chiplet designs for specific applications, offering customized solutions to meet individual customer requirements, and investing in talent acquisition to build strong engineering teams. A key strategy is to establish robust supply chain networks to ensure the reliable availability of chiplet components.

The future outlook for Heterogeneous Compute Chiplet Platform Market in the United States remains highly promising. Continued advancements in chiplet technology, coupled with increasing demand for high-performance computing, are expected to drive significant market growth in the coming years. The focus on power efficiency and scalability will further fuel adoption across various industries.

Europe

The European market for Heterogeneous Compute Chiplet Platform Market is experiencing steady growth, driven by strong government initiatives promoting digital transformation and investments in advanced manufacturing capabilities. Several European countries are actively fostering innovation in semiconductor technologies, creating a favorable environment for the development and adoption of chiplet solutions. The automotive industry and industrial automation are key end-use sectors contributing to market demand in the region. Emphasis is placed on energy efficiency and sustainable computing practices.

Asia-Pacific

Asia-Pacific represents a significant and rapidly expanding market for Heterogeneous Compute Chiplet Platform Market. Countries like China, Japan, and South Korea are witnessing substantial investments in high-performance computing infrastructure, artificial intelligence, and 5G technologies, which are driving demand for advanced compute chiplet platforms. The region’s large electronics manufacturing base and increasing adoption of cloud computing services further contribute to market growth.

South America

Heterogeneous Compute Chiplet Platform Market in South America is currently in its nascent stages but is poised for growth in the coming years. Increasing investments in telecommunications infrastructure, government initiatives promoting digital inclusion, and the growing adoption of cloud services are expected to drive market expansion. The region presents a significant opportunity for companies offering cost-effective and scalable compute solutions.

Middle East & Africa

The Middle East & Africa region is witnessing increasing interest in Heterogeneous Compute Chiplet Platform Market, driven by government initiatives focused on technological advancement and diversification of economies. Investments in smart cities, industrial sectors, and defense applications are creating demand for high-performance computing platforms. While the market is relatively small compared to other regions, it offers significant growth potential.

Report Scope

This market research report provides a comprehensive analysis of the Heterogeneous Compute Chiplet Platform Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Heterogeneous Compute Chiplet Platform Market?

-> Heterogeneous Compute Chiplet Platform Market was valued at USD 3.45 billion in 2025 and is expected to reach USD 7.12 billion by 2034, representing a CAGR of 8.1% over the forecast period.

Which key companies operate in Heterogeneous Compute Chiplet Platform Market?

-> Key players include Intel Corp., Advanced Micro Devices (AMD), Taiwan Semiconductor Manufacturing Co. (TSMC), Xilinx (now part of AMD), Samsung Electronics, and Qualcomm Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include rising AI inference and training workloads in data centers, demand for high‑performance edge computing, advances in advanced packaging (silicon photonics, EMIB) and the need to overcome lithography scaling limits.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong semiconductor manufacturing ecosystems in China, Taiwan, South Korea, and Japan, while North America remains a major hub for design and R&D activities.

What are the emerging trends?

-> Emerging trends include integration of heterogeneous chiplet ecosystems via silicon photonic interconnects, development of AI‑optimized chiplets, and collaborative standardization efforts among industry consortia to accelerate time‑to‑market.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...