Optical AI Interconnect Chip Market Insights

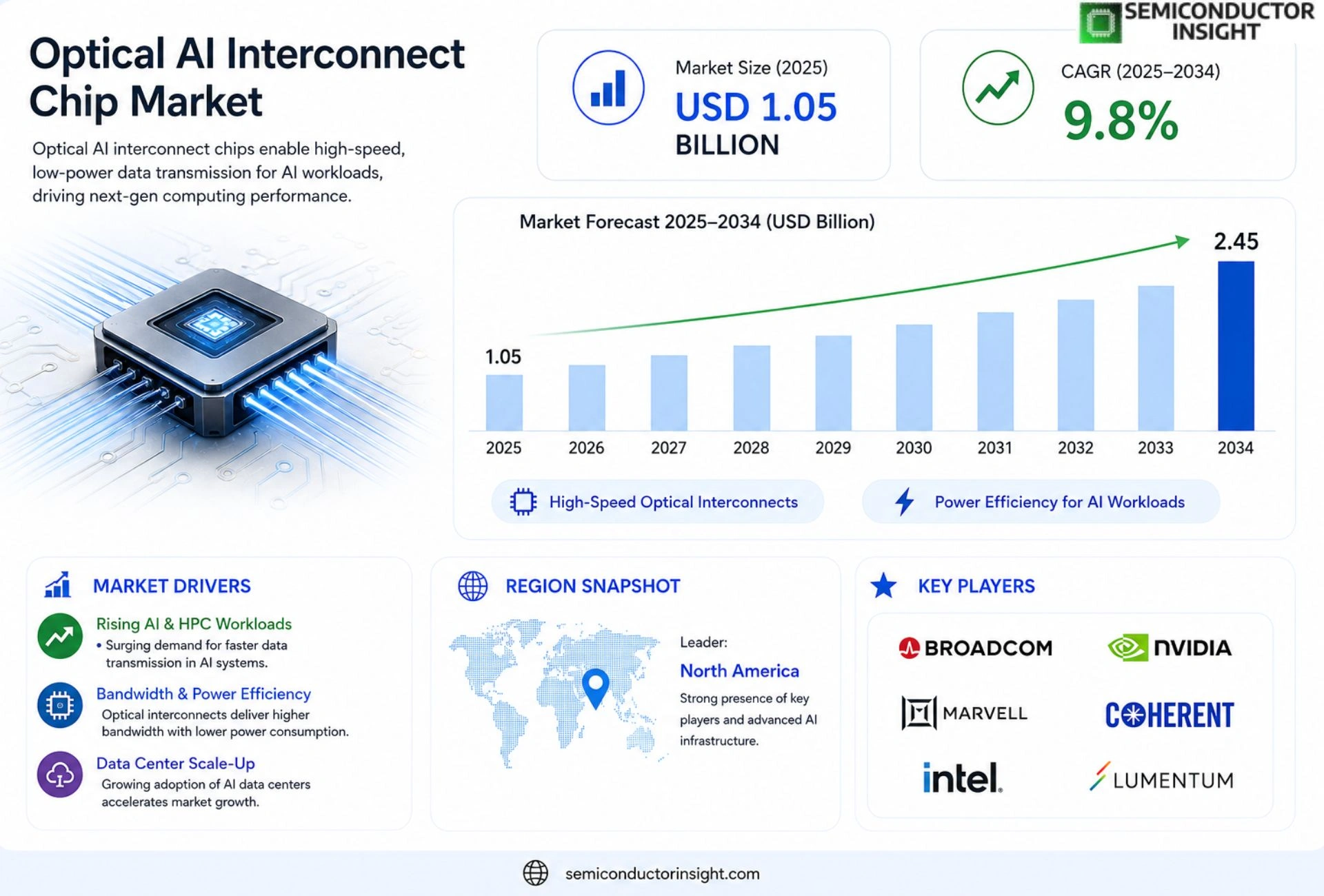

Global Optical AI Interconnect Chip Market size was valued at USD 1.05 billion in 2025.

The market is projected to grow from USD 1.05 billion in 2025 to USD 2.45 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period.

Optical AI interconnect chips are photonic integrated circuits that transmit data between artificial-intelligence accelerators using light-guided waveguides rather than conventional copper traces.

These chips combine wavelength-division multiplexing, silicon-photonic modulators and low-power receivers to deliver terabit-per-second bandwidth with sub-nanosecond latency, enabling next-generation

MARKET DRIVERS

Data Center Bandwidth Demands

The rapid expansion of hyperscale data centers is creating unprecedented bandwidth requirements. Photonic interconnects can deliver terabits per second with lower latency, making them a natural fit for Optical AI Interconnect Chip Market. Recent deployments have shown up to a 45% reduction in power consumption compared with traditional copper solutions.

AI Model Complexity

Emerging generative AI models now exceed 1 trillion parameters, pushing the limits of conventional silicon interconnects. Optical AI chips enable parallel data pathways, supporting high‑throughput training while keeping thermal profiles manageable. Industry surveys indicate a 30% annual increase in investment for photonic AI acceleration.

➤ “The transition to photonic interconnects is accelerating as data‑intensive AI workloads dominate the next‑generation computing landscape.”

Regulatory incentives for energy‑efficient computing in major economies are further stimulating adoption. Analysts expect the Optical AI Interconnect Chip Market to outpace overall AI hardware growth by double‑digit percentages through 2030.

MARKET CHALLENGES

Manufacturing Yield and Scale

Fabricating optical components at wafer scale remains technically demanding. Yield rates for integrated photonic wafers hover around 70%, driving up unit costs and slowing market penetration of Optical AI Interconnect Chip Market. Efforts to standardize process nodes are still in early stages.

Other Challenges

Integration with Existing Infrastructures

Data centers built on legacy electrical backplanes require significant redesign to accommodate photonic modules, creating upfront capital expenditures that can deter early adopters.

MARKET RESTRAINTS

High Capital Expenditure

Initial deployment costs for Optical AI interconnect solutions are substantially higher than conventional copper alternatives. Many operators cite budget constraints as a primary restraint, especially in regions with limited access to financing for advanced infrastructure.

Technical Skill Gap

The specialized knowledge required to design, test, and maintain photonic AI chips is scarce. Companies often need to invest in training programs or partner with niche vendors, adding operational complexity that can slow adoption rates within Optical AI Interconnect Chip Market.

MARKET OPPORTUNITIES

Edge Computing Expansion

Edge locations are increasingly hosting AI inference tasks that demand low‑latency, high‑bandwidth connections. Optical AI interconnect chips can provide the necessary performance while reducing power footprints, opening a substantial growth avenue for the market.

Strategic Partnerships

Collaborations between photonic foundries and AI chipset manufacturers are accelerating product roadmaps. Joint ventures aimed at co‑developing standardized optical interfaces are expected to unlock new revenue streams and expand the addressable market for Optical AI Interconnect Chip Market.

Optical AI Interconnect Chip Market Trends

Shift Toward Photonic Data Fabric

Optical AI Interconnect Chip Market is experiencing a decisive shift as leading data‑center operators adopt photonic data‑fabric architectures. By replacing traditional copper traces with light‑guided waveguides, these chips reduce power consumption while delivering terabit‑per‑second bandwidth. The trend is reinforced by the need for sub‑nanosecond latency in AI accelerator clusters, where every nanosecond of delay translates into measurable performance loss. Consequently, hardware designers are embedding wavelength‑division multiplexing and silicon‑photonic modulators directly into the interconnect layer, creating a more deterministic communication substrate that aligns with the compute‑intensive nature of modern AI workloads.

Other Trends

Integration with Silicon Photonics Platforms

Manufacturers are increasingly standardizing Optical AI Interconnect Chip Market components on silicon‑photonic foundries, leveraging mature CMOS processes to achieve volume production at competitive cost. This integration simplifies the supply chain and allows seamless co‑packaging with AI accelerator dies, reducing the overall footprint of high‑performance servers. Moreover, the convergence of photonic‑electronic co‑design enables designers to balance optical link density with electronic control logic, fostering a more modular ecosystem where chip vendors can offer customizable interconnect solutions tailored to specific AI inference or training workloads.

Emergence of Low‑Power Modulation Techniques

Another notable development within Optical AI Interconnect Chip Market is the adoption of low‑power modulation schemes such as electro‑absorption and micro‑ring resonator modulators. These technologies achieve high‑speed data transmission with markedly lower drive voltages, directly addressing the power‑budget constraints of dense AI accelerator racks. When combined with advanced low‑noise receivers, the overall energy per bit improves, supporting longer link lengths without resorting to repeaters. This progression not only enhances the economic viability of photonic interconnects but also reinforces their strategic relevance for next‑generation AI infrastructure deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

Optical AI Interconnect Chip Market Overview

The market is currently dominated by large semiconductor firms that have leveraged their existing AI accelerator portfolios to integrate photonic interconnect technologies. Intel leads with its Lightwave platform, combining silicon‑photonic modulators and wavelength‑division multiplexing to deliver terabit‑per‑second bandwidth for data‑center AI workloads. Nvidia has accelerated its strategy by acquiring optical‑AI startups and embedding photonic links into its DGX systems, positioning itself as a vertically integrated solution provider. IBM’s research arm contributes advanced silicon‑photonic circuits that support sub‑nanosecond latency, while Broadcom supplies high‑performance transceivers that complement AI accelerator designs. These incumbents benefit from extensive R&D budgets, global supply chains, and existing relationships with cloud service providers, creating a market structure where scale and integration depth dictate competitive advantage.

Beyond the dominant tier, several niche innovators are shaping specialized segments of the Optical AI Interconnect Chip ecosystem. Lightmatter focuses on chip‑scale photonic compute engines that co‑locate AI inference engines with optical interconnects, targeting edge and hyperscale deployments. Rockley Photonics supplies customized wavelength‑division multiplexed modules for hyperscale AI clusters. Ayar Labs offers chip‑to‑chip optical communication bridges that enable low‑power, high‑density interconnects for AI ASICs. Acacia Communications (now part of Cisco) provides coherent optical modules that enhance data‑center AI fabric reliability. Infinera, Ciena, and Luxtera (Cisco) deliver carrier‑grade photonic platforms that can be repurposed for AI workloads, while startups such as MacroPhotonics and PhotonIC focus on next‑generation silicon‑photonic integration techniques to address emerging latency‑critical AI applications.

List of Key Optical AI Interconnect Chip Companies Profiled

- Intel

- Nvidia

- IBM

- Broadcom

- Lightmatter

- Rockley Photonics

- Ayar Labs

- Acacia Communications

- Infinera

- Ciena

- Luxtera (Cisco)

- MacroPhotonics

- PhotonIC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Photonic Integrated Circuits

|

| By Application |

|

Data Center Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Technology |

|

Wavelength‑Division Multiplexing (WDM)

|

| By Deployment Mode |

|

On‑Premise Data Centers

|

Regional Analysis: North America

The primary drivers in the North American market include escalating demand for high bandwidth, the proliferation of AI workloads, and advancements in optical chip technology. Increasing data center density and the need for low-latency communication are also significantly impacting market growth.

The competitive landscape is characterized by established semiconductor manufacturers and emerging startups focusing on specialized optical interconnect solutions. Key players are investing heavily in R&D to develop innovative chip architectures and enhance performance metrics. Strategic partnerships and collaborations are becoming increasingly common to gain access to advanced technologies and expand market reach.

Significant technological advancements are being made in areas such as silicon photonics, co-packaged optics, and advanced modulation techniques. These innovations are enabling higher data rates, improved energy efficiency, and smaller form factors for optical AI interconnect chips. The integration of AI algorithms for chip design and optimization is also gaining traction.

Investment in optical AI interconnect chip technology is steadily increasing in North America, driven by the growing demand from data centers and high-performance computing facilities. Venture capital funding and corporate investments are fueling innovation and accelerating the commercialization of new solutions.

North America

North America is experiencing substantial growth in Optical AI Interconnect Chip Market. The region’s strong focus on technological innovation and significant investments in artificial intelligence are key factors driving this expansion. Data centers across the United States and Canada are actively upgrading their infrastructure to support the increasing demands of AI and machine learning applications, creating a direct need for high-bandwidth, low-latency optical interconnect solutions. The increasing adoption of cloud computing and the rise of edge computing further contribute to the market’s growth trajectory. Furthermore, research institutions and universities in North America are at the forefront of developing novel optical chip architectures and technologies, fostering a vibrant ecosystem for innovation. The focus is on creating more energy-efficient and powerful chips to handle the massive data flows associated with advanced AI algorithms. This demand is translating into substantial opportunities for semiconductor manufacturers and optical technology providers operating within the region.

Europe

Europe represents a significant and growing market for Optical AI Interconnect Chips. Driven by the European Union’s commitment to digital sovereignty and the continent’s burgeoning AI sector, investment in this technology is on the rise. Key players in the automotive, industrial automation, and telecommunications industries are actively seeking enhanced data processing capabilities, fueling demand. The strong research base in countries like Germany, the UK, and France is contributing to innovation in silicon photonics and other advanced optical technologies. However, fragmented market structures and varying regulatory landscapes across European nations present some challenges. Strategic collaborations and EU-led initiatives are aimed at fostering a more cohesive and competitive market environment for Optical AI Interconnect Chips.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing market for Optical AI Interconnect Chip Market. Countries like China, Japan, and South Korea are leading the way in adopting advanced AI technologies and investing heavily in data center infrastructure. The rapid expansion of 5G networks and the increasing deployment of edge computing facilities are driving significant demand for high-performance optical interconnect solutions. China’s government support for technological innovation and its ambitious AI development plans are creating a massive market opportunity. The region is witnessing a surge in local optical chip manufacturers and a growing emphasis on indigenous innovation. However, geopolitical tensions and trade uncertainties pose potential risks to the market’s growth.

South America

South America is an emerging market for Optical AI Interconnect Chip Market, with potential for significant growth in the coming years. Increased investments in telecommunications infrastructure and the adoption of cloud computing services are driving demand. The growing presence of multinational technology companies in the region is also contributing to market expansion. However, infrastructure limitations, regulatory complexities, and economic uncertainties present challenges to market development. The focus is on providing cost-effective optical solutions to meet the needs of a rapidly evolving digital landscape.

Middle East & Africa

The Middle East & Africa represent a relatively nascent market for Optical AI Interconnect Chip Market, but with considerable growth potential. Large-scale infrastructure projects, particularly in the telecommunications and energy sectors, are driving demand for advanced communication solutions. The increasing adoption of cloud computing and the growing focus on smart city initiatives are also creating opportunities. However, limited investment, infrastructure constraints, and geopolitical instability present significant challenges. The market is expected to witness gradual growth as technological advancements and economic development progress.

Report Scope

This market research report provides a comprehensive analysis of the Optical AI Interconnect Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical AI Interconnect Chip Market?

-> Optical AI Interconnect Chip Market size was valued at USD 1.05 billion in 2025.

The market is projected to grow from USD 1.05 billion in 2025 to USD 2.45 billion by 2034, exhibiting a CAGR of 9.8%.

Which key companies operate in Optical AI Interconnect Chip Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...