Graphics Processing Unit (GPU) for AI Market Insights

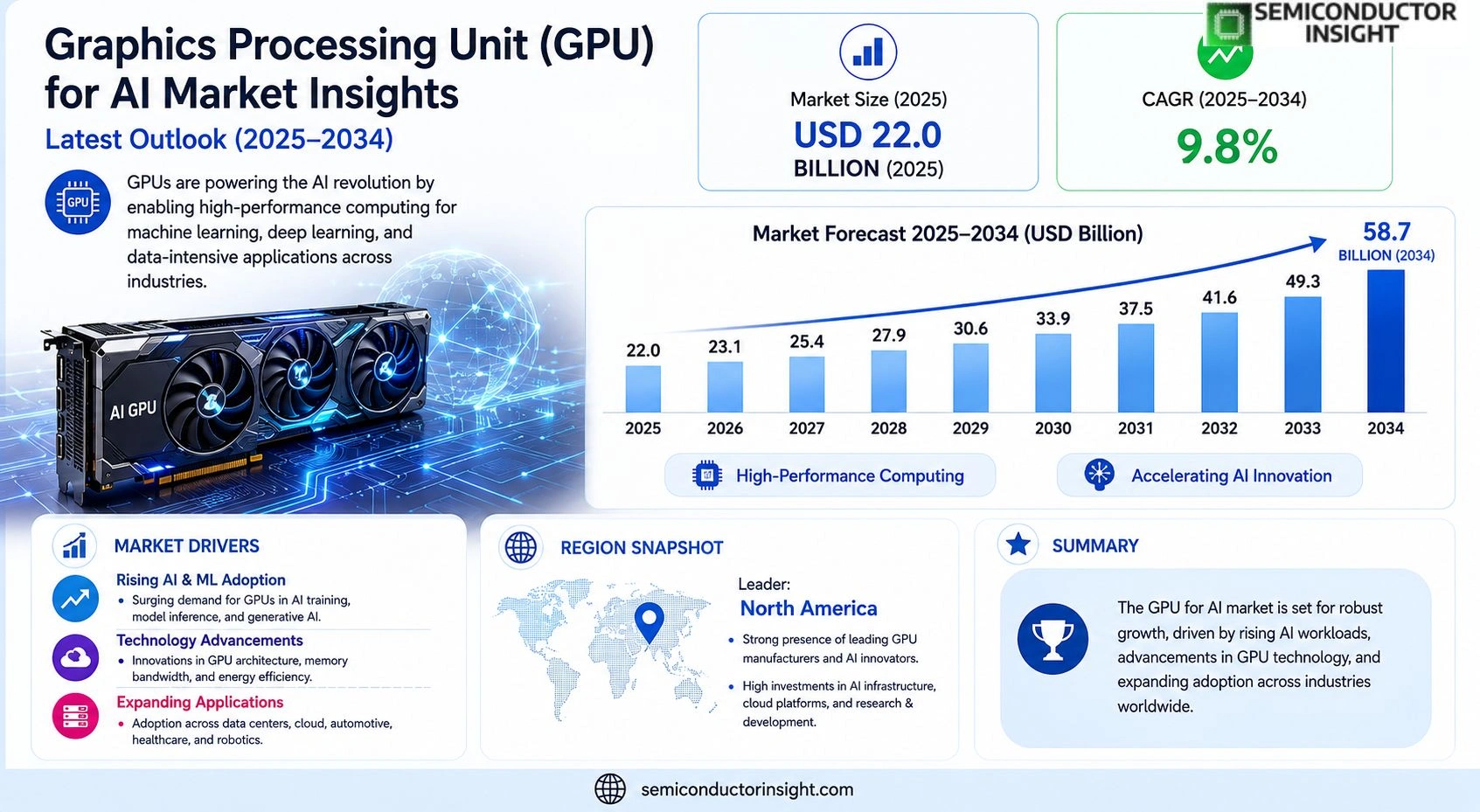

Global Graphics Processing Unit (GPU) for AI Market size was valued at USD 22.0 billion in 2025. The market is projected to grow from USD 23.1 billion in 2025 to USD 58.7 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period.

Graphics Processing Units designed for artificial intelligence accelerate deep‑learning training and inference by executing massive parallel matrix operations far faster than traditional CPUs. These GPUs integrate high‑bandwidth memory, tensor cores optimized for mixed‑precision arithmetic, and software stacks such as CUDA and ROCm that enable developers to harness their computational power efficiently.

The market is experiencing rapid growth because enterprises are scaling generative‑AI services, while hyperscale cloud providers expand dedicated AI clusters worldwide. However, supply‑chain constraints and rising energy costs pose challenges that manufacturers must address. Furthermore, sustained investment from leading players—NVIDIA’s Hopper architecture rollout, AMD’s MI300 series launch, and Intel’s Xe‑HPC GPUs—continues to drive adoption across sectors ranging from autonomous vehicles to healthcare analytics.

MARKET DRIVERS

Explosive Growth in Generative AI

Graphics Processing Unit (GPU) for AI Market is being propelled by the rapid adoption of generative AI models such as large language models and diffusion image generators. In 2023, global AI‑focused GPU shipments exceeded 120 million units, a 25 % year‑over‑year increase, and revenue is projected to surpass $30 billion by 2028, driven by a compound annual growth rate (CAGR) of roughly 28 %.

Edge Computing and Real‑Time Inference

Enterprises are shifting AI workloads to the edge to reduce latency and bandwidth costs. This trend boosts demand for power‑efficient GPUs that can operate in constrained environments such as autonomous vehicles, smart factories, and remote‑sensing stations. Forecasts indicate that edge‑deployed AI GPUs will account for nearly 20 % of total GPU revenue by 2027.

➤ “Optimized GPU architectures that balance performance and energy use are becoming the cornerstone of next‑generation AI services.”

Regulatory incentives for AI research and the emergence of AI‑as‑a‑service platforms further accelerate investment in high‑performance GPUs, ensuring sustained momentum for Graphics Processing Unit (GPU) for AI Market across multiple verticals.

MARKET CHALLENGES

Supply Chain Constraints

Global semiconductor shortages, triggered by pandemic‑related disruptions and geopolitical tensions, have limited the availability of advanced GPU wafers. Lead times for 7 nm and 5 nm processes have extended to 6‑9 months, pressuring OEMs and inflating prices for AI‑oriented GPUs.

Other Challenges

High Power Consumption

AI‑intensive workloads often require GPUs that draw 300 W or more, leading to increased cooling infrastructure costs and limiting deployment in data‑center environments with strict energy budgets.

Furthermore, software compatibility challenges persist as developers transition from legacy CUDA‑based ecosystems to emerging heterogeneous computing frameworks, creating friction in optimizing GPU utilization.

MARKET RESTRAINTS

Escalating Development Costs

Designing GPUs capable of handling trillion‑parameter models demands substantial R&D investment. Major players allocate upwards of $2 billion annually to architecture refinement, which can deter new entrants and concentrate market power.

In addition, the high capital expense of building AI‑optimized data centers—often exceeding $15 million per megawatt—acts as a financial barrier for smaller firms seeking to leverage cutting‑edge GPUs.

The need for specialized talent in parallel computing and deep‑learning optimization further restrains rapid market expansion, as the talent pool remains limited relative to demand.

MARKET OPPORTUNITIES

Specialized AI Accelerators

Emerging architectures that fuse GPU cores with dedicated tensor processing units (TPUs) present a lucrative growth avenue. These hybrid designs deliver up to 2.5× performance gains for transformer‑based workloads while reducing power draw, opening new market segments in scientific computing and drug discovery.

Another opportunity lies in the growing demand for custom ASIC‑GPU solutions tailored for specific industries such as finance, healthcare, and autonomous navigation. Partnerships between GPU manufacturers and domain experts enable rapid time‑to‑market for niche AI applications.

Finally, the expansion of AI services in emerging economies, supported by government AI initiatives, promises to increase the addressable market for cost‑effective GPUs, driving volume growth and diversification of Graphics Processing Unit (GPU) for AI Market.

Graphics Processing Unit (GPU) for AI Market Trends

Rapid Expansion of Generative AI Services

The acceleration of generative‑AI workloads has become the dominant catalyst for GPU demand. Enterprises are deploying large‑scale language models for customer support, content creation, and data synthesis, while hyperscale cloud providers are building dedicated AI clusters that rely on high‑throughput GPUs. This shift is driving a steady increase in unit shipments and prompting data‑center operators to prioritize devices with tensor cores and high‑bandwidth memory. As a result, the ecosystem of software frameworks, such as CUDA, ROCm, and emerging open‑source libraries, is expanding to simplify model training and inference across diverse hardware platforms.

Other Trends

Supply‑Chain Resilience and Energy Efficiency

The rapid uptake has exposed persistent supply‑chain bottlenecks, especially for advanced silicon and high‑capacity memory modules. Manufacturers are investing in diversified fab capacity and longer‑lead component contracts to mitigate shortages. At the same time, rising electricity prices are prompting designers to improve performance‑per‑watt. Techniques such as mixed‑precision computing and dynamic voltage scaling are now standard features in the latest GPU generations, helping operators balance cost and sustainability while maintaining the latency required for real‑time AI services. Growing ESG expectations further encourage data‑center owners to select hardware that delivers lower carbon footprints.

Innovation in GPU Architectures

The competitive landscape is marked by a succession of architecture releases. Nvidia’s Hopper series introduced fourth‑generation tensor cores that double matrix‑multiply throughput, while AMD’s MI300 integrates CPU and GPU dies to reduce data movement latency. Intel’s Xe‑HPC line emphasizes scalability across server racks, offering flexible interconnect options for multi‑node training. These hardware advances are complemented by optimized software stacks that enable model parallelism and efficient memory management, accelerating adoption across sectors including autonomous vehicles, medical imaging, and financial analytics, where rapid tensor processing translates directly into business value.

COMPETITIVE LANDSCAPEKey Industry Players

GPU for AI Market Competitive Landscape

NVIDIA remains the undisputed leader in the AI‑oriented GPU segment, leveraging its Hopper and Ampere architectures, extensive CUDA ecosystem, and deep partnerships with hyperscale cloud providers. Its market share is reinforced by a broad portfolio spanning data‑center accelerators, edge modules, and developer tools that enable rapid deployment of generative‑AI workloads. AMD follows closely with the MI300 series, emphasizing open‑source ROCm support and high‑bandwidth memory, while Intel has accelerated its entry through Xe‑HPC GPUs and the acquisition of Habana Labs, targeting both inference and training efficiency. The competitive structure is characterized by a tri‑pole of large incumbents that dominate volume sales, complemented by strategic alliances that lock in ecosystem lock‑in and reinforce pricing power.

Beyond the three majors, a diverse set of niche players enriches the GPU for AI landscape. Qualcomm’s Snapdragon AI Engine extends GPU acceleration to mobile and edge devices, while Samsung’s Exynos line integrates high‑performance graphics cores for on‑device inference. European and Asian innovators such as Graphcore (IPU), Cerebras Systems (Wafer‑Scale Engine), and Cambricon (MLU) provide specialized architectures that compete on bandwidth and scalability. Start‑ups like Tenstorrent, Groq, and Mythic focus on low‑latency inference and energy‑efficient designs, carving out market segments in autonomous vehicles, robotics, and embedded AI. These challengers promote rapid innovation, compel incumbents to accelerate roadmap cycles, and broaden the overall supplier ecosystem.

List of Key GPU for AI Companies Profiled

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Intel Corporation

- Qualcomm Inc.

- Samsung Electronics

- Graphcore Ltd.

- Cerebras Systems

- Cambricon Technologies

- Tenstorrent Inc.

- Groq Inc.

- Mythic AI

- Huawei Technologies (Kunpeng GPU)

- MediaTek Inc.

- AMD Xilinx

- SiFive Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

General‑purpose GPUs are the dominant choice because they offer a broad software ecosystem, flexible workload handling, and continuous performance improvements.

|

| By Application |

|

Data‑center training drives the strategic direction of GPU development, emphasizing raw compute density and memory bandwidth.

|

| By End User |

|

Cloud service providers shape market momentum by offering on‑demand GPU resources that democratize access to AI capabilities.

|

| By Architecture |

|

Tensor‑core focused architectures dominate strategic roadmaps because they deliver mixed‑precision efficiency crucial for modern AI workloads.

|

| By Deployment Model |

|

On‑premise AI clusters remain critical for organizations prioritizing data sovereignty and latency‑sensitive workloads.

|

Regional Analysis

The primary drivers in the US market include increasing adoption of AI across industries, growing investments in AI infrastructure, and the rise of cloud-based GPU offerings. The demand for specialized GPUs tailored for AI workloads is steadily increasing, further propelling market growth.

The US market features a highly competitive landscape with established players and emerging startups vying for market share. Key players are focused on developing and offering high-performance GPUs optimized for AI tasks, along with providing comprehensive software and support services.

Current technological trends in the US GPU for AI market emphasize the development of more energy-efficient GPUs, enhanced memory capabilities, and specialized architectures for deep learning and other AI applications. The integration of AI-specific hardware accelerators is also gaining traction.

The future outlook for the GPU for AI market in the United States remains exceptionally positive. Continued innovation in GPU technology, coupled with the expanding AI adoption across various industries, is expected to drive significant growth in the coming years.

Europe

Europe presents a significant and rapidly expanding market for Graphics Processing Units (GPUs) in the context of the burgeoning Artificial Intelligence (AI) sector. While lagging slightly behind the United States in overall market size, Europe demonstrates strong potential for growth, underpinned by substantial investments in AI research, a skilled talent pool, and a commitment to technological advancement. Several European nations are actively fostering AI ecosystems, attracting both domestic and international investment. The European Union’s focus on digital transformation and the development of strategic technologies like AI are creating favorable market conditions for GPU adoption. Key application areas driving demand include autonomous driving, robotics, healthcare, and financial modeling, all of which are experiencing significant growth within the region. Companies are increasingly recognizing the importance of high-performance GPUs for training and deploying sophisticated AI models, leading to a steady increase in demand. The focus on energy efficiency and sustainable computing is also influencing GPU development and adoption strategies in Europe.

Asia-Pacific

The Asia-Pacific region is poised to become the largest and fastest-growing market for Graphics Processing Units (GPUs) in the AI domain. Driven by rapid economic expansion, increasing digital penetration, and a growing focus on technological innovation, countries like China, Japan, South Korea, and India are witnessing explosive demand for GPU technology. China’s ambitious AI development plans and significant investments in AI infrastructure are fueling considerable GPU demand. The region’s large and diverse user base, coupled with the growth of e-commerce, cloud computing, and smart cities, are further contributing to market expansion. While the market is characterized by a mix of established and emerging players, the competition is intensifying, leading to innovation in GPU design and pricing. The focus on AI applications in manufacturing, healthcare, and financial services is expected to continue driving strong growth in the coming years.

South America

South America represents an emerging market for Graphics Processing Units (GPUs) within the AI landscape. While currently smaller than North America, Europe, and Asia-Pacific, the region exhibits considerable growth potential due to increasing investments in technology, a growing AI talent pool, and expanding digital infrastructure. Countries like Brazil and Argentina are leading the way in AI adoption, particularly in areas such as agriculture, finance, and retail. The demand for GPUs is primarily driven by the need to support AI applications in these sectors. However, challenges such as limited access to advanced technology and relatively high costs are hindering market growth. As the region continues to develop its digital economy and invest in AI research, the demand for GPUs is expected to increase steadily in the coming years.

Middle East & Africa

The Middle East and Africa constitute a nascent but promising market for Graphics Processing Units (GPUs) in the AI sector. Driven by increasing government investments in technology, a growing focus on digitalization, and expanding AI applications in areas such as healthcare, finance, and defense, the region is witnessing early stages of GPU adoption. Countries like Saudi Arabia, the United Arab Emirates, and South Africa are leading the way in AI development and deployment. The demand for GPUs is primarily driven by the need to support AI applications in these sectors. However, challenges such as limited infrastructure, a shortage of skilled talent, and high upfront costs are hindering market growth. As the region continues to invest in AI and digital transformation, the demand for GPUs is expected to increase significantly in the coming years, presenting significant opportunities for GPU vendors.

Report Scope

This market research report provides a comprehensive analysis of the Graphics Processing Unit (GPU) for AI Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Graphics Processing Unit (GPU) for AI Market?

-> Graphics Processing Unit (GPU) for AI Market size was valued at USD 22.0 billion in 2025. The market is projected to grow from USD 23.1 billion in 2025 to USD 58.7 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period.

Which key companies operate Graphics Processing Unit (GPU) for AI Market?

-> Key players include NVIDIA, AMD, Intel.

What are the key growth drivers?

-> Key growth drivers include scaling of generative‑AI services, expansion of AI clusters by hyperscale cloud providers, and continued investment in GPU architectures such as NVIDIA Hopper, AMD MI300, and Intel Xe‑HPC.

Which region dominates the market?

-> The market exhibits strong adoption across North America, Europe, and Asia‑Pacific, with no single region dominating globally.

What are the emerging trends?

-> Emerging trends include integration of high‑bandwidth memory, tensor‑core acceleration, mixed‑precision computing, and advanced software stacks like CUDA and ROCm.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...