CXL (Compute Express Link) Controller Chip Market Insights

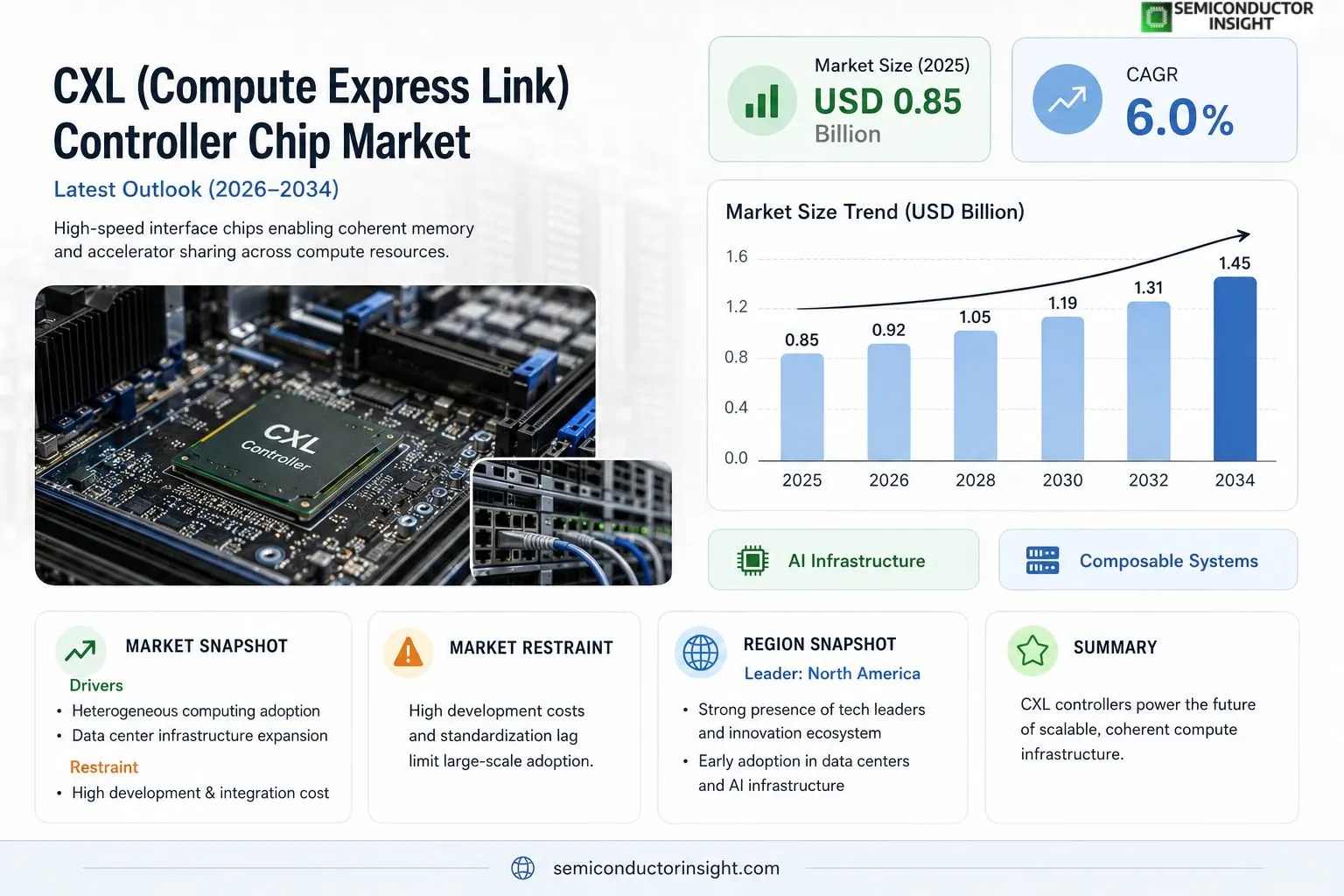

Global CXL (Compute Express Link) Controller Chip Market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period.

CXL controller chips are high‑speed interface silicon that enable coherent memory and accelerator sharing across CPUs, GPUs, FPGAs and other compute resources. They implement the open‑industry standard defined by the Compute Express Link Consortium, supporting bandwidths up to 64 GT/s per lane and multiple protocol generations (Gen3‑Gen5). By translating PCIe physical layers into cache‑coherent transactions, these chips simplify system architecture while delivering low latency and scalable bandwidth.The market is accelerating because hyperscale data centers demand tighter CPU‑accelerator coupling, AI workloads require massive shared memory pools, and emerging form factors such as composable infrastructure rely on CXL’s flexibility.Furthermore, recent announcements,Intel’s launch of Gen5‑compatible CXL switches in Q1 2024,Marvell’s integration of CQL controllers into its OCTEON line,and Samsung’s roadmap for on‑package CQL memory,are driving adoption.

Key players including Intel Corp., AMD Inc., Marvell Technology Group Ltd., and Synopsys Inc. continue to expand their portfolios, reinforcing the upward trajectory of the sector.

MARKET DRIVERS

Increasing Adoption of Heterogeneous Computing

The rise of AI, ML and real‑time analytics is prompting enterprises to deploy heterogeneous architectures that blend CPUs, GPUs, FPGAs and memory disaggregated resources. CXL (Compute Express Link) Controller Chip Market is at the core of this shift, delivering low‑latency, high‑bandwidth interconnects that enable seamless memory sharing across devices.

Expansion of Data Center Infrastructure

Data centers are scaling to meet cloud demand, and operators are redesigning rack ecosystems to support modular, composable infrastructure. CXL controller chips facilitate rapid provisioning of compute pools, reducing capital expense by up to 15% in large‑scale deployments.

➤ CXL adoption is projected to exceed 30% of new server shipments by 2028, driving robust growth for controller chip suppliers.

Overall, the synergy between workload diversification and datacenter modularity is accelerating the demand for CXL‑based solutions, positioning the controller chip segment for double‑digit CAGR through 2032.

MARKET CHALLENGES

Technical Integration Complexity

Integrating CXL controllers with legacy PCIe and proprietary interconnects requires extensive firmware and BIOS updates. Companies often face compatibility testing cycles that extend product‑to‑market timelines, especially for OEMs with extensive product portfolios.

Other Challenges

Supply Chain Constraints

The semiconductor shortage that began in 2020 continues to affect advanced node manufacturing. Limited fab capacity for specialized controller chips can inflate prices by 10‑20% and cause lead‑time delays for large cloud providers.

MARKET RESTRAINTS

High Development Cost

Designing CXL controller IP demands deep expertise in high‑speed signalling and protocol compliance. R&D expenditures can exceed $120 million per generation, making entry barriers significant for emerging vendors.

Standardization Lag

Although the CXL 3.0 specification was released in 2023, full ecosystem adoption is still uneven. Variations in firmware support across CPU vendors can delay large‑scale deployments and suppress market momentum.

MARKET OPPORTUNITIES

Emerging AI and HPC Use Cases

AI training clusters and high‑performance computing platforms require near‑memory latency and terabit‑scale bandwidth. CXL controller chips enable memory pooling across thousands of nodes, creating a substantial growth avenue for chip manufacturers.

Geographic Expansion in APAC

Investment in hyperscale data centers across China, South Korea and India is accelerating. Local OEMs are partnering with global silicon vendors to develop region‑specific CXL solutions, offering a strategic foothold for market participants.

Licensing and Ecosystem Services

Beyond silicon sales, providers can capture value through IP licensing, reference designs and co‑development services. This revenue diversification is expected to become a pivotal growth driver as the ecosystem matures.

CXL (Compute Express Link) Controller Chip Market Trends

Rising Demand for Coherent Memory Architecture

The market is gaining momentum as hyperscale data‑center operators seek tighter coupling between CPUs and accelerators. AI‑intensive workloads, which require massive shared memory pools, are pushing architects toward solutions that reduce latency while delivering scalable bandwidth. CXL controller chips act as high‑speed interface silicon that translate PCIe physical layers into cache‑coherent transactions, thereby simplifying system design and enabling efficient memory and accelerator sharing across CPUs, GPUs, FPGAs and other compute resources. This technical advantage, combined with the open‑industry standard defined by the Compute Express Link Consortium, is driving broader adoption across cloud providers and enterprise IT environments.

Other Trends

Key Vendor Initiatives

Leading silicon suppliers are expanding their CXL portfolios to meet emerging demand. Intel introduced Gen5‑compatible CXL switches in early 2024, positioning the company to support the next generation of bandwidth‑intensive deployments. Marvell incorporated CXL controllers into its OCTEON line, offering integrated solutions for networking and storage appliances. Samsung disclosed a roadmap that includes on‑package CXL memory, highlighting a move toward tightly integrated system‑in‑package designs. In addition to these moves, AMD and Synopsys continue to develop complementary IP and verification tools, reinforcing a diversified ecosystem that facilitates rapid product development and adoption.

Emerging Form Factors and Ecosystem Expansion

Composable infrastructure and modular data‑center designs are leveraging the flexibility of CXL controller chips to enable dynamic reconfiguration of compute resources. By providing a standardized, low‑latency pathway for memory and accelerator sharing, these chips support a range of form factors,from blade servers to ultra‑dense edge nodes,without sacrificing performance. The growing alignment among hardware vendors, software developers, and standards bodies is fostering a robust ecosystem that is expected to sustain the upward trajectory of the CXL (Compute Express Link) Controller Chip Market well beyond the current forecast horizon.

COMPETITIVE LANDSCAPEKey Industry Players

CXL Controller Chip Market: Competitive Overview 2024‑2034

Intel Corporation remains the dominant force in the CXL (Compute Express Link) controller chip market, leveraging its early‑stage investments in Gen5‑compatible CXL switches and integrated silicon solutions. The company’s extensive CPU and data‑center portfolio creates a natural demand pipeline for its CXL controllers, positioning Intel at the core of the ecosystem and influencing design standards across hyperscale operators. The market structure is thus characterized by an oligopolistic concentration where a handful of vertically integrated firms control most of the high‑performance controller IP, while a growing cohort of fabless innovators seeks niche differentiation through power‑efficiency or specialized memory‑coherent features.Beyond Intel, several validated players contribute significant depth to the competitive landscape. AMD, through its acquisition of Xilinx, expands FPGA‑centric CXL offerings, while Marvell Technology Group supplies interoperable controllers for networking‑oriented platforms. Synopsys provides comprehensive IP cores that enable rapid integration for OEMs, and Samsung Electronics pushes on‑package memory‑coherent solutions that embed CXL functionality. Additional contributors include Qualcomm, Broadcom, NVIDIA (via Mellanox), IBM, Google, Alibaba Cloud, and Renesas, each targeting specific workloads such as AI accelerators, composable infrastructure, or edge compute, thereby enriching the market’s diversification and fostering innovation beyond the primary leaders.

List of Key Compute Express Link Controller Chip Companies Profiled

- Intel Corporation

- AMD Inc.

- Marvell Technology Group Ltd.

- Synopsys Inc.

- Samsung Electronics

- Qualcomm Technologies

- Broadcom Inc.

- NVIDIA Corporation

- IBM

- Google (Alphabet Inc.)

- Alibaba Cloud (Aliyun)

- Renesas Electronics Corp.

- Microsoft Azure (Azure Edge)

- Huawei Technologies Co., Ltd.

- TSMC (as foundry partner for CXL IP)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Accelerator‑focused Controllers enable tighter CPU‑accelerator integration, support dynamic scaling of accelerator resources, and reduce latency for demanding AI and data‑intensive workloads. • They act as the logical bridge that preserves cache coherence across heterogeneous compute elements. • Their design prioritizes low‑latency pathways, crucial for real‑time inference. • They simplify system architecture by abstracting protocol translation, allowing designers to focus on performance innovation. |

| By Application |

|

Data Center Servers benefit from the ability to share memory pools across CPUs and accelerators, fostering workload elasticity and simplifying resource provisioning. • The coherent link accelerates large‑scale training models by reducing data movement overhead. • It supports modular upgrades, allowing operators to insert new accelerator types without redesigning the entire platform. • The technology drives a more streamlined chassis design, freeing space for additional compute density. |

| By End User |

|

Hyperscale Cloud Providers leverage CXL controllers to construct highly unified compute fabrics that can serve diverse tenant workloads with consistent performance. • They gain architectural flexibility to pivot between CPU‑heavy and accelerator‑heavy configurations on demand. • The coherent memory model minimizes software complexity when orchestrating multi‑node AI pipelines. • It strengthens platform reliability by reducing the number of interconnect hops. |

| By Architecture |

|

Integrated SoC Controllers embed CXL logic directly within processor packages, delivering the tightest possible latency envelope and enabling on‑die memory coherence. • This integration supports compact system designs for space‑constrained edge deployments. • It reduces board‑level complexity, improving overall system reliability. • Designers value the ability to co‑optimize compute and interconnect pathways for bespoke workloads. |

| By Deployment Model |

|

Composable Rack Systems capitalize on the fluid nature of CXL to reconfigure resource pools in real‑time, matching compute, memory, and accelerator allocations to workload needs. • The approach encourages a pay‑as‑you‑grow infrastructure philosophy. • It enables rapid prototyping of novel hardware topologies without physical rewiring. • Operators benefit from streamlined maintenance cycles, as components can be replaced or upgraded with minimal disruption. |

Regional Analysis: North America

United States

The data center segment within the US market is a primary driver for CXL adoption, with increasing demands for high bandwidth and low latency interconnects to support demanding workloads.

The rapid growth of AI and ML applications in the US is creating a significant demand for CXL controllers to accelerate model training and inference processes.

HPC clusters in the US are increasingly leveraging CXL to enhance computational performance for scientific research and engineering applications.

Major cloud providers in the US are actively integrating CXL into their infrastructure to offer enhanced performance and efficiency to their customers.

Europe

Europe represents a significant and growing market for CXL Controller Chips. The region’s strong focus on technological advancement, particularly in areas like automotive, industrial automation, and scientific research, is propelling the adoption of CXL. The European Union’s initiatives promoting digital sovereignty and boosting domestic semiconductor manufacturing are creating a favorable environment for the CXL market. Key trends include the increasing demand for CXL in edge computing applications, the development of advanced memory-centric interconnects, and the growing interest from research institutions in utilizing CXL for high-performance computing. While the US currently holds a lead, Europe is rapidly catching up, with several leading chip manufacturers and system integrators investing heavily in CXL technologies. The automotive industry, with its evolving needs for autonomous driving and advanced driver-assistance systems, is emerging as a critical driver for CXL adoption in Europe.

Asia-Pacific

Asia-Pacific is poised to become the fastest-growing market for CXL Controller Chips, driven by the massive expansion of the data center infrastructure in countries like China, India, and Japan. The region’s burgeoning AI and IoT industries are creating significant demand for high-performance computing solutions, where CXL plays a crucial role. Government support for technology innovation and semiconductor manufacturing in several APAC nations is further accelerating market growth. Key trends include the increasing adoption of CXL in cloud computing, the development of advanced memory technologies, and the growing interest from telecommunications companies in utilizing CXL for 5G and future network infrastructure. The Asia-Pacific market presents a significant opportunity for CXL vendors, but also poses challenges related to evolving regulatory landscapes and intense competition.

South America

South America represents a relatively nascent market for CXL Controller Chips, but it holds significant long-term potential. The region’s growing digital economy, increasing adoption of cloud services, and expanding data center footprint are creating a gradual demand for CXL technologies. While the adoption rate is currently lower compared to North America, Europe, and Asia-Pacific, the market is expected to experience substantial growth in the coming years. Key drivers include the increasing demand for high-performance computing in sectors like mining, oil & gas, and financial services, as well as the growing interest from educational institutions in utilizing CXL for research and development. Market players are focusing on building awareness and demonstrating the benefits of CXL to potential customers in the region.

Middle East & Africa

The Middle East & Africa region is an emerging market for CXL Controller Chips, with a growing focus on digital transformation and technological advancement. The region’s expanding data center infrastructure, increasing adoption of cloud services, and growing investments in AI and IoT are driving demand for high-performance computing solutions. While the market is still in its early stages of development, it presents significant opportunities for growth in the coming years. Key drivers include the increasing demand for data analytics and AI applications in sectors like finance, healthcare, and government. Market players are focusing on building partnerships and providing tailored solutions to meet the specific needs of customers in the region.

Report Scope

This market research report provides a comprehensive analysis of the CXL (Compute Express Link) Controller Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CXL (Compute Express Link) Controller Chip Market?

-> Global CXL (Compute Express Link) Controller Chip Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034, reflecting a CAGR of 6.0% over the forecast period.

Which key companies operate in CXL (Compute Express Link) Controller Chip Market?

-> Key players include Intel Corp., AMD Inc., Marvell Technology Group Ltd., and Synopsys Inc.

What are the key growth drivers?

-> Key growth drivers include hyperscale data‑center demand for tighter CPU‑accelerator coupling, AI workloads requiring massive shared memory pools, and the rise of composable infrastructure leveraging CXL’s flexibility.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia‑Pacific is emerging as a fast‑growing region.

What are the emerging trends?

-> Emerging trends include integration of CXL in Gen5‑compatible switches, on‑package CXL memory solutions, and broader adoption of CXL in AI accelerator ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...