Sparse Computing Chip Market Insights

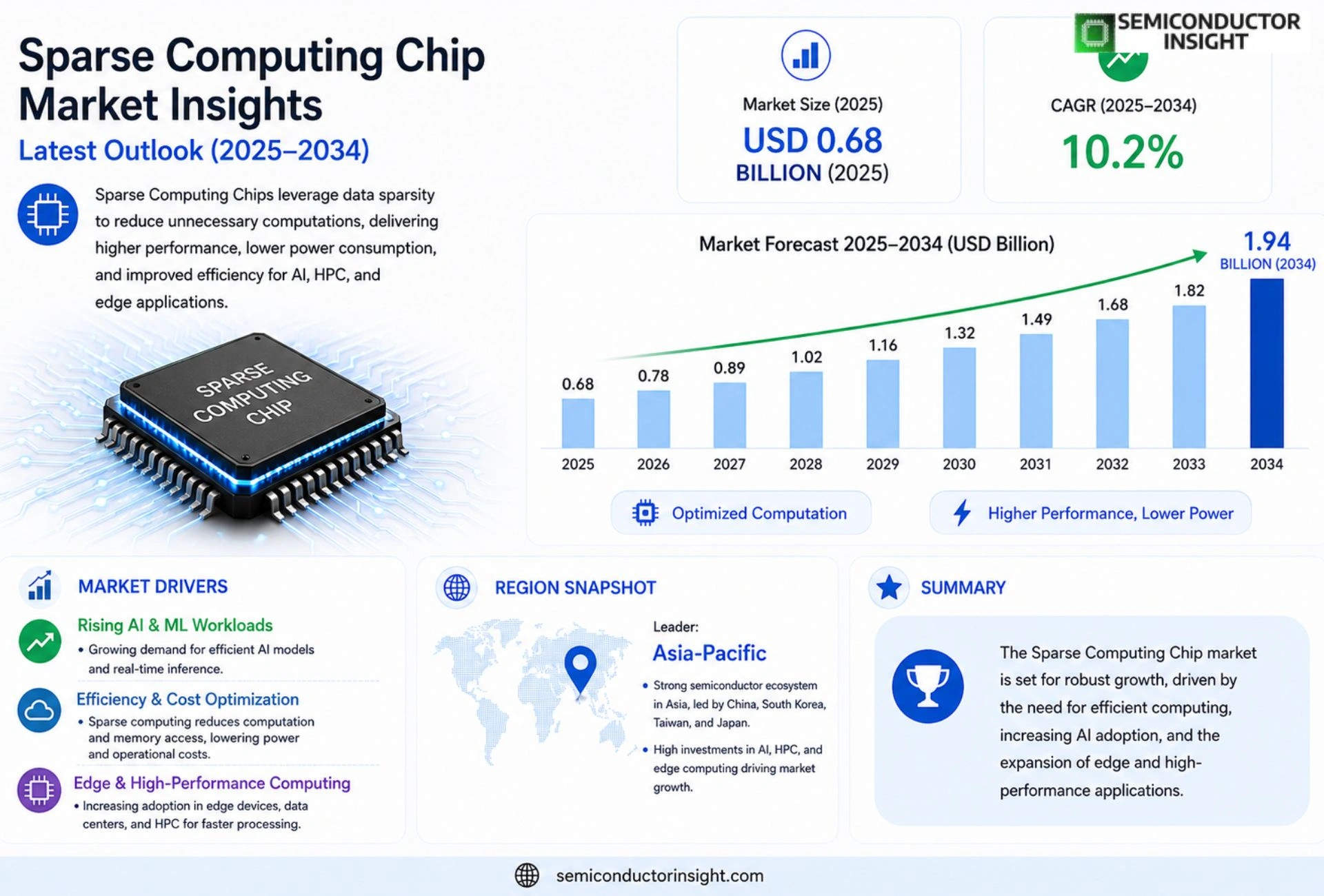

Global Sparse Computing Chip market size was valued at USD 0.68 billion in 2025. The market is projected to grow from USD 0.78 billion in 2026 to USD 1.94 billion by 2034, exhibiting a CAGR of 10.2% during the forecast period.

Sparse computing chips are specialized semiconductor devices designed to efficiently process sparsely connected neural networks by exploiting zero‑valued weights, thereby reducing memory bandwidth and power consumption. These chips integrate architectures such as weight‑pruned accelerators, structured sparsity engines, and event‑driven processing units, enabling high‑performance inference for edge AI and large‑scale datacenter workloads.

The market is experiencing rapid growth due to several factors, including heightened demand for energy‑efficient AI inference, increased investment in edge computing hardware, and advancements in pruning algorithms that enable higher sparsity ratios without accuracy loss. Furthermore, collaborations between leading fabless designers and foundries,such as the partnership announced in March 2024 between Graphcore and TSMC to co‑develop next‑generation sparse tensor cores,are accelerating product rollouts. Companies like Intel (with its Habana Labs), NVIDIA (through its Sparse Tensor Cores), Qualcomm (with Hexagon DSP extensions), and Cerebras Systems are key players driving innovation in this space

MARKET DRIVERS

Rising Demand for Energy‑Efficient AI Acceleration

Sparse Computing Chip Market is being propelled by the need for AI systems that consume less power while delivering high throughput. Enterprises are adopting sparse matrix techniques to trim unnecessary calculations, leading to measurable reductions in data‑center electricity bills. This shift is especially evident in large‑scale language models where sparsity can cut energy use by up to 70%.

Advancements in Chip Architecture and Toolchains

Recent breakthroughs in architecture design, such as structured pruning and dynamic sparsity, have made it feasible to embed sparse compute units directly on silicon. Coupled with increasingly mature software stacks, developers can now translate high‑level sparse algorithms into efficient hardware instructions without extensive hand‑tuning. These innovations shorten time‑to‑market for new AI products.

➤ Sparse architectures can reduce the number of multiply‑accumulate operations by up to 90% while preserving model accuracy, unlocking cost‑effective scaling for next‑generation AI workloads.

Collectively, stronger demand for low‑power AI and the convergence of hardware‑software ecosystems create a robust growth engine for Sparse Computing Chip Market, positioning it as a cornerstone of future intelligent systems.

MARKET CHALLENGES

Algorithmic Complexity and Standardization Gaps

Designing sparse algorithms that reliably converge across diverse datasets remains a technical hurdle. The lack of universally accepted standards for sparse representation hampers interoperability between chips, frameworks, and cloud services, forcing vendors to invest heavily in custom integration.

Other Challenges

Manufacturing Yield and Cost Constraints

Producing chips with irregular compute blocks can affect wafer yield, driving up per‑unit costs. Companies must balance the economic impact of specialized layout with the performance gains of sparsity, which can slow broader market adoption.

MARKET RESTRAINTS

Limited Ecosystem Support and Software Maturity

While hardware capabilities are advancing, many AI developers still rely on dense‑matrix libraries. The relative immaturity of sparse‑optimized compilers and runtime environments restricts the immediate utility of new chips, acting as a restraint on market expansion.

MARKET OPPORTUNITIES

Emerging Edge Applications and 5G Integration

The proliferation of edge devices,ranging from autonomous drones to smart cameras,creates a fertile arena for sparsity‑focused chips. These devices must process AI inference locally under strict power envelopes, making Sparse Computing Chip Market uniquely positioned to capture demand as 5G networks drive real‑time analytics at the edge.

Sparse Computing Chip Market Trends

Energy‑Efficient AI Inference

The rise of edge AI workloads is driving manufacturers to seek chips that convert sparse neural network models into real‑time predictions while consuming minimal power. Sparse architectures exploit zero‑valued weights, cutting memory bandwidth and allowing inference engines to operate at lower voltages. By pruning redundant connections, these chips achieve up to 70 % reduction in arithmetic operations, which translates into lower heat generation and longer device lifespans. Data‑center operators benefit from a smaller silicon footprint, enabling higher density racks and reduced cooling costs. Simultaneously, the ability to maintain model accuracy despite high sparsity ratios positions energy‑efficient inference as the dominant market force, encouraging OEMs to prioritize sparsity‑aware designs in upcoming product cycles.

Other Trends

Edge‑Device Adoption

Edge deployments are increasingly leveraging sparse processing units because they align with the limited silicon area and thermal envelopes of mobile platforms. Vendors such as Qualcomm have integrated sparsity extensions into their Hexagon DSP, enabling smart cameras and wearables to run deep‑learning models locally without offloading to the cloud. This on‑device execution eliminates latency spikes and preserves user privacy, which is critical for applications like biometric authentication and autonomous navigation. The reduced data‑transfer demands also lower network bandwidth usage, extending battery life for IoT sensors that operate on constrained power budgets. As a result, developers are redesigning computer‑vision and speech‑recognition pipelines to maximize sparsity, accelerating the adoption curve across consumer electronics, industrial robotics, and remote‑monitoring equipment.

Industry Collaboration and Architecture Innovation

Strategic partnerships are accelerating the rollout of next‑generation sparse tensor cores, providing a clear signal that the ecosystem is consolidating around shared standards. The March 2024 alliance between Graphcore and TSMC exemplifies how fabless designers and foundries co‑develop custom silicon to achieve higher sparsity ratios without sacrificing accuracy, shortening time‑to‑market for advanced inference accelerators. At the same time, Intel’s Habana Labs, NVIDIA’s Sparse Tensor Cores, and Cerebras Systems are refining weight‑pruned accelerators and structured sparsity engines that support both training and inference phases. These collaborative efforts are reinforcing Sparse Computing Chip Market’s trajectory toward broader adoption across cloud and edge environments, as organizations seek unified solutions that can scale from low‑power edge nodes to high‑throughput data‑center clusters.

COMPETITIVE LANDSCAPE

Key Industry Players

Sparse Computing Chip Market: Structure, Growth Drivers and Competitive Dynamics

Sparse Computing Chip Market is currently dominated by a small cohort of semiconductor powerhouses that have integrated sparsity‑aware architectures into their product portfolios. Intel’s Habana Labs offers the Gaudi series, which combines weight‑pruned accelerators with high‑bandwidth memory to target datacenter AI inference. NVIDIA leverages its industry‑leading Sparse Tensor Cores across the Ampere and Hopper families, delivering up to 2× speed‑up for zero‑filled weight matrices. Graphcore, in partnership with TSMC, is co‑developing next‑generation sparse tensor cores that emphasize low latency for edge AI. Qualcomm’s Hexagon DSP extensions add structured sparsity support for mobile and IoT devices, while Samsung Electronics provides high‑density logic processes that enable fabless designers to ship custom sparse engines at scale. These leading players benefit from deep fab‑foundry relationships, extensive AI software stacks, and sizable R&D budgets, positioning them at the apex of a market projected to reach $1.94 billion by 2034.

Beyond the tier‑one firms, a vibrant ecosystem of niche innovators is expanding the functional breadth of sparse computing. Cerebras Systems introduced the Wafer‑Scale Engine with built‑in event‑driven sparsity processing, targeting ultra‑large transformer models. SambaNova Systems offers the Dataflow Architecture that natively exploits weight pruning for rapid model rollout in enterprise clouds. Tenstorrent focuses on modular chips that can be tiled to achieve high‑density sparse inference. Huawei’s Ascend line embeds structured sparsity engines for 5G edge workloads, while Google’s TPU v5 incorporates sparsity primitives to slash power consumption in search services. AMD’s MI300 series and Alibaba’s DAMO Academy also contribute specialized accelerators that support sparse tensor operations, rounding out a competitive field that blends fabless design agility with foundry scale.

List of Key Sparse Computing Chip Companies Profiled

- Intel (Habana Labs)

- NVIDIA

- Graphcore

- Qualcomm

- Samsung Electronics

- Cerebras Systems

- SambaNova Systems

- Tenstorrent

- Huawei

- AMD

- Google (TPU)

- Alibaba DAMO Academy

- Microsoft (Project Brainwave)

- TSMC (foundry partner)

- Synopsys (EDA for sparse architectures)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Weight‑Pruned Accelerators are recognized as the leading type because they:

|

| By Application |

|

Edge AI Inference drives the market because it:

|

| By End User |

|

Device Manufacturers dominate this segment as they:

|

| By Architecture |

|

ASIC‑Based Sparse Chips lead this architectural dimension because they:

|

| By Value Proposition |

|

Energy Efficiency stands out as the primary value driver, delivering:

|

Regional Analysis:

United States

The increasing demand for scalable and energy-efficient data centers is a primary driver for sparse computing chip adoption. These chips offer significant advantages in reducing power consumption and enhancing performance for computationally intensive workloads.

The migration to cloud-based services further necessitates the use of these specialized chips to optimize resource utilization and minimize operational costs.

The burgeoning fields of artificial intelligence and machine learning are heavily reliant on sparse computing to accelerate model training and inference. Sparse models, characterized by a large number of zero-valued parameters, benefit significantly from the computational efficiency offered by these specialized chips.

This application segment is expected to witness substantial growth, driven by the increasing deployment of AI and ML applications across various industries.

High-performance computing (HPC) applications, including scientific simulations, weather forecasting, and drug discovery, are increasingly leveraging sparse computing to tackle complex computational problems.

Sparse models enable researchers and scientists to perform more computationally intensive tasks with reduced power consumption and improved efficiency.

Emerging applications in the automotive and robotics sectors are also exploring the potential of sparse computing chips. These chips can contribute to enhanced perception systems, autonomous driving capabilities, and efficient control algorithms.

The need for real-time processing and low latency in these applications is driving the adoption of sparse computing solutions.

Europe

Europe is witnessing a steady rise in interest in Sparse Computing Chip Market, spurred by strong government support for digital transformation and a growing focus on sustainable computing. Key markets like Germany, the UK, and France are investing in research and development initiatives aimed at fostering innovation in this area. The automotive sector in Europe is a significant driver, with increasing adoption of sparse computing for advanced driver-assistance systems (ADAS) and autonomous driving technologies. Business strategies in Europe emphasize collaboration on research projects and the development of open-source tools to accelerate innovation. The region’s commitment to energy efficiency aligns well with the benefits offered by sparse computing.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in Sparse Computing Chip Market. Countries like China, Japan, and South Korea are leading the charge, driven by substantial investments in AI, big data, and high-performance computing. China’s ambitious digital economy initiatives are creating significant demand for sparse computing solutions across various industries. The region’s strong manufacturing base and increasing domestic chip production capabilities are further fueling market growth. Business strategies in Asia-Pacific focus on developing cost-effective sparse computing solutions and building strong partnerships with local technology companies.

South America

South America’s Sparse Computing Chip Market is in its nascent stages but exhibits promising growth potential. Brazil and Argentina are the key markets, driven by increasing investments in technology and a growing demand for data processing capabilities. The adoption of sparse computing is expected to be driven primarily by the telecommunications and finance sectors. Business strategies in the region focus on introducing cost-effective solutions and building awareness about the benefits of sparse computing.

Middle East & Africa

The Middle East & Africa region presents a relatively smaller but potentially high-growth market for sparse computing chips. Governments in countries like Saudi Arabia and the UAE are investing heavily in digital infrastructure and smart city initiatives, which are expected to drive demand for these specialized chips. The energy and defense sectors are also key drivers of adoption in this region. Business strategies typically involve partnerships with international technology providers and a focus on providing tailored solutions to meet specific regional needs.

Report Scope

This market research report provides a comprehensive analysis of the Sparse Computing Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Sparse Computing Chip Market?

-> Sparse Computing Chip market size was valued at USD 0.68 billion in 2025. The market is projected to grow from USD 0.78 billion in 2026 to USD 1.94 billion by 2034, exhibiting a CAGR of 10.2%.

Which key companies operate in Sparse Computing Chip Market?

-> Key players include Intel (Habana Labs), NVIDIA, Qualcomm, Graphcore, Cerebras Systems, and TSMC, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy‑efficient AI inference, increased investment in edge computing hardware, advances in pruning algorithms that enable higher sparsity ratios, and strategic collaborations between fabless designers and foundries.

Which region dominates the market?

-> North America remains a dominant market due to a strong semiconductor ecosystem, while Asia‑Pacific is emerging as a fast‑growing region.

What are the emerging trends?

-> Emerging trends include weight‑pruned accelerators, structured sparsity engines, event‑driven processing units, and the integration of sparse tensor cores into edge and datacenter AI workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...