AI Accelerator Chip Market Insights

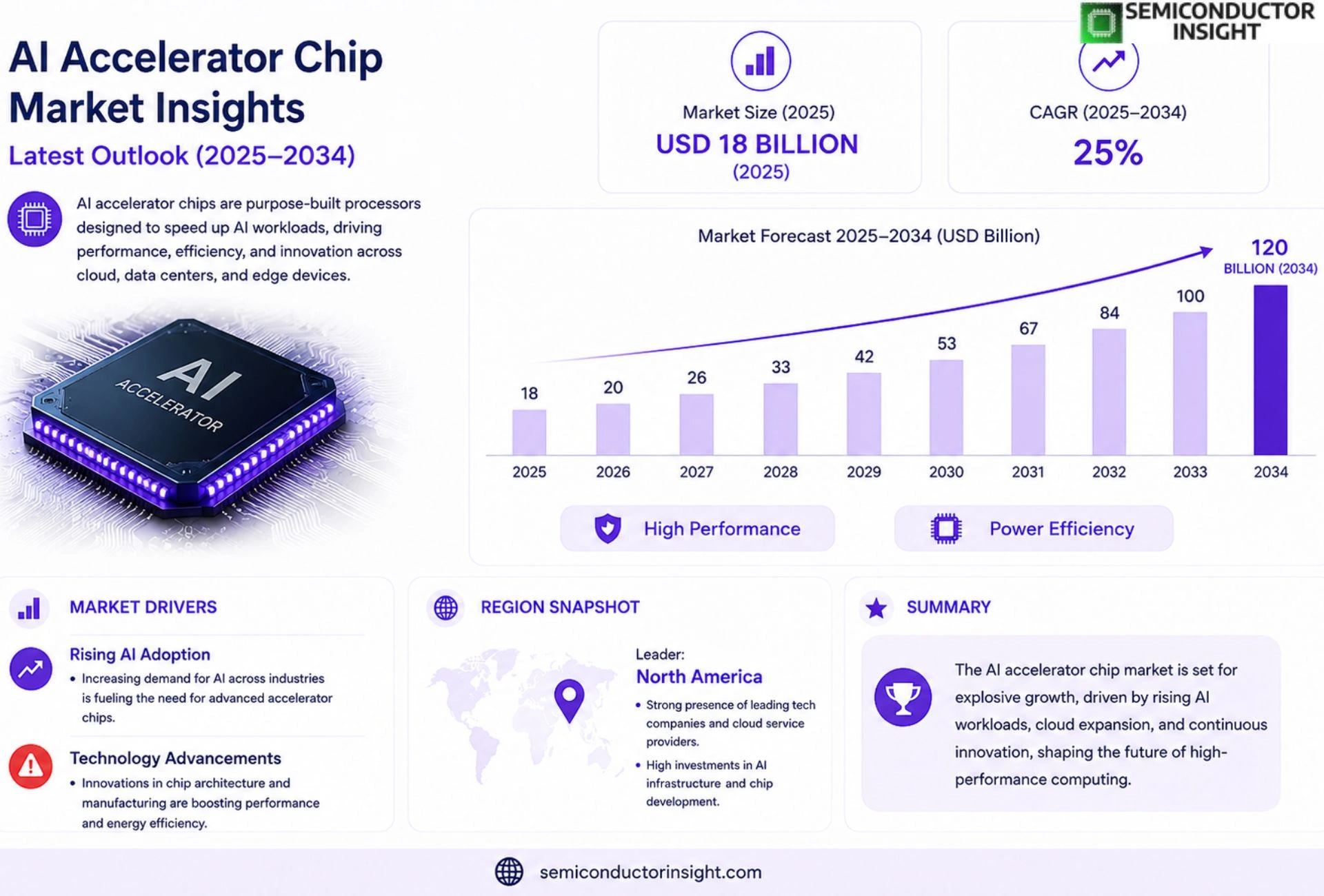

Global AI Accelerator Chip Market size was valued at USD 18 billion in 2025. The market is projected to grow from USD 20 billion in 2026 to USD 120 billion by 2034, exhibiting a CAGR of 25% during the forecast period.

AI accelerator chips are specialized semiconductor devices engineered to speed up artificial‑intelligence workloads such as deep‑learning inference and training. They integrate architectures like tensor processing units (TPUs), neural processing units (NPUs), and purpose‑built GPUs that optimize matrix multiplications and convolution operations. Because these chips deliver high‑throughput parallelism while minimizing latency and power consumption, they enable edge devices, data‑center servers, and autonomous systems to execute complex models efficiently.

MARKET DRIVERS

Rising Demand for Real‑Time AI Processing

AI Accelerator Chip Market is being propelled by the exponential growth of AI workloads that require sub‑millisecond latency. Enterprises are migrating inference tasks from general‑purpose CPUs to purpose‑built accelerators to meet the performance expectations of autonomous vehicles, smart factories, and immersive media. This shift is creating a clear preference for chips that can deliver high throughput while minimizing power draw.

Advancements in Semiconductor Manufacturing

Recent process‑node reductions to 5 nm and below enable higher transistor density, directly benefiting AI accelerator designs. The ability to integrate on‑chip memory and specialized compute units reduces data movement overhead, which translates into faster model execution and lower total cost of ownership for customers of AI Accelerator Chip Market.

➤ Integrated AI accelerators are becoming a cornerstone of modern data‑center architectures, driving both efficiency and scalability.

Overall, the convergence of latency‑critical applications and cutting‑edge silicon technology creates a robust foundation for continued expansion of AI Accelerator Chip Market across cloud, edge, and embedded segments.

MARKET CHALLENGES

Design Complexity and Power Efficiency

Engineers must balance aggressive performance targets with stringent power budgets, especially for edge devices where thermal envelopes are limited. The intricate architecture of AI accelerators,featuring heterogeneous cores, bespoke interconnects, and on‑chip memory hierarchies,demands sophisticated verification workflows, extending development cycles for AI Accelerator Chip Market.

Other Challenges

Supply Chain Constraints

Global semiconductor shortages, combined with the need for specialized packaging materials, can delay volume production. Manufacturers must secure reliable sources of high‑purity silicon and advanced lithography services to meet the escalating demand for AI‑optimized chips.

MARKET RESTRAINTS

High Development Costs

Designing and fabricating AI accelerators requires significant capital investment in EDA tools, silicon prototypes, and validation infrastructure. Smaller players often lack the financial resources to compete, which concentrates market power among a few large vendors and limits the breadth of innovation withAI Accelerator Chip Market.

MARKET OPPORTUNITIES

Emerging Edge AI Applications

Edge computing scenarios,such as intelligent surveillance cameras, AR/VR headsets, and industrial IoT gateways,are creating new demand for low‑power, high‑performance AI chips. These applications prioritize on‑device inference to reduce bandwidth costs and enhance privacy, presenting a significant growth avenue for AI Accelerator Chip Market as vendors tailor architectures for specific workload profiles.

AI Accelerator Chip Market Trends

Expansion of Edge AI Deployments

AI Accelerator Chip Market is increasingly shaped by the surge of edge computing applications. Manufacturers are integrating purpose‑built tensor units directly into cameras, sensors, and micro‑controllers to meet the demand for real‑time inference with minimal latency. Power‑efficient designs enable battery‑operated devices to run sophisticated models, reducing reliance on cloud connectivity and lowering operational costs. As 5G networks mature, the bandwidth advantage further encourages on‑device processing, driving semiconductor firms to prioritize low‑power, high‑throughput architectures that can operate within strict thermal envelopes.

Other Trends

Data‑Center Integration and Scale‑Out Architectures

Within large‑scale data‑center environments, AI Accelerator Chip Market is witnessing a shift toward modular, scale‑out solutions. Companies are deploying clusters of AI‑specific ASICs and GPUs that can be flexibly added to server racks, matching workload spikes without over‑provisioning. This approach capitalizes on the chips’ ability to accelerate both training and inference pipelines, offering consistent throughput improvements for deep‑learning workloads while maintaining a balanced power‑to‑performance ratio. The trend also encourages software ecosystems that abstract hardware heterogeneity, allowing enterprises to program across diverse accelerator families with unified frameworks.

Architectural Diversification and Software Co‑Design

Another significant direction AI Accelerator Chip Market is the convergence of multiple processing paradigms in a single silicon package. Designers are embedding neural processing units alongside conventional CPUs and programmable logic to create heterogeneous compute tiles. This diversification addresses the varying precision and latency requirements of different AI models, from quantized inference to mixed‑precision training. Concurrently, co‑design of hardware and compilers is becoming a standard practice, optimizing code generation to exploit chip‑specific instructions and memory hierarchies. The result is a measurable uplift in execution efficiency and a reduction in development cycles for AI‑driven products.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Accelerator Chip Market: Competitive Landscape Overview

NVIDIA remains the dominant force AI Accelerator Chip Market, leveraging its CUDA‑optimized GPUs and the dedicated Hopper architecture to capture the majority of data‑center and high‑performance computing workloads. Its ability to integrate software stacks such as cuDNN and TensorRT creates a strong ecosystem that locks in customers and sustains premium pricing. Intel, with its acquisition of Habana Labs and the subsequent Gaudi line, competes directly in the training segment, while Google’s custom Tensor Processing Units (TPUs) dominate hyperscale inference workloads within the company’s own cloud services. The market structure is therefore tiered: a handful of megacap semiconductor firms command the bulk of revenue, supported by cloud providers that develop internal ASICs to reduce operating costs.

Beyond the Tier‑1 vendors, several specialist firms are expanding market depth. AMD’s MI series GPUs offer a price‑competitive alternative for edge AI, and Qualcomm’s Snapdragon Neural Processing Units power mobile and IoT devices at low power. Samsung and Huawei are investing in on‑chip AI engines for smartphones and edge gateways, while Graphcore’s IPU and Cerebras’s wafer‑scale engine target ultra‑low‑latency training. Emerging startups such as Tenstorrent and Mythic bring novel architectures that emphasize energy efficiency for embedded applications. Collectively, these niche players increase innovation pressure and diversify supply chains, creating a more fragmented yet resilient competitive landscape.

List of Key AI Accelerator Chip Companies Profiled

- NVIDIA

- AMD

- Intel (Habana Labs)

- Google (TPU)

- Amazon Web Services (Inferentia)

- Qualcomm

- Apple

- Samsung Electronics

- Huawei

- Graphcore

- Cerebras Systems

- Tenstorrent

- Mythic

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tensor Processing Units

|

| By Application |

|

Data‑Center AI Inference

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

Systolic Arrays

|

| By Deployment Environment |

|

Edge Edge Nodes

|

Regional Analysis:

United States

The data center segment is a major consumer of AI accelerator chips, driven by the massive computational demands of cloud-based AI services. Demand is consistently high, with deployments of advanced accelerators becoming standard.

Focus is on energy efficiency and scalability to meet the growing needs of AI workloads.

The automotive sector is experiencing rapid adoption of AI for applications such as autonomous driving, advanced driver-assistance systems (ADAS), and in-car infotainment. AI accelerator chips are crucial for processing sensor data and enabling real-time decision-making.

The stringent safety and reliability requirements of the automotive industry are driving innovation in chip design and validation.

AI is transforming healthcare, with applications in medical imaging, drug discovery, and personalized medicine. AI accelerator chips are enabling faster and more accurate analysis of medical data.

Regulatory compliance and data privacy are key considerations in this sector.

The financial services industry is leveraging AI for fraud detection, risk management, and algorithmic trading. AI accelerator chips are accelerating the processing of large datasets and enabling real-time analytics.

Security and data protection are paramount concerns in this highly regulated sector.

Europe

Europe is emerging as a significant player AI Accelerator Chip Market, with strong government support and a growing ecosystem of AI companies. Countries like Germany, France, and the UK are investing heavily in AI research and development, fostering innovation in chip design and manufacturing. The focus is on developing energy-efficient solutions and promoting collaboration between academia and industry. While Europe lags behind the United States in terms of market size, it is rapidly catching up, particularly in areas such as automotive and industrial applications. Regulatory frameworks like GDPR are influencing chip design and data privacy considerations. The increasing demand for AI in sectors such as manufacturing, healthcare, and finance is driving market growth. Several European startups are focusing on niche applications, offering specialized AI accelerator chips for specific tasks. The European Union’s initiatives, such as the Digital Europe Programme, are providing funding and support for AI innovation.

Asia-Pacific

The Asia-Pacific region, particularly China and Japan, represents a rapidly growing market for AI Accelerator Chips. China’s massive domestic market and strong government initiatives are fueling demand, with significant investments in AI infrastructure and applications. Japan is focusing on AI for robotics, manufacturing, and healthcare. The region is witnessing the rise of local chip manufacturers and a growing ecosystem of AI startups. The demand is driven by a wide range of applications, including smart cities, e-commerce, and industrial automation. While there are challenges related to supply chain disruptions and geopolitical tensions, the Asia-Pacific region is expected to remain a key growth driver for AI Accelerator Chip Market. The focus is on developing cost-effective and high-performance solutions to meet the evolving needs of the region.

South America

South America is an emerging market with growing potential for AI Accelerator Chips. Countries like Brazil and Argentina are beginning to invest in AI research and development, driven by the need to improve efficiency and competitiveness across various industries. The adoption of AI is gaining traction in sectors such as agriculture, finance, and retail. While the market size is currently smaller compared to North America and Asia-Pacific, there is significant growth potential in the coming years. Challenges include limited infrastructure and a relatively small pool of skilled AI professionals. Government initiatives and private sector investments are crucial for fostering innovation and accelerating market growth. Focus is increasingly on leveraging AI for data analysis and predictive modeling in industries like agriculture and mining.

Middle East & Africa

The Middle East and Africa represent a relatively nascent market for AI Accelerator Chips, but with significant long-term potential. Countries like Saudi Arabia, the UAE, and South Africa are investing in digital transformation initiatives, creating opportunities for AI adoption across various sectors. The demand is driven by applications in smart cities, healthcare, finance, and infrastructure management. While the market size is currently limited, there is substantial growth potential in the coming years, particularly with increasing investments in technology and infrastructure. Key challenges include limited domestic manufacturing capabilities and a need for skilled talent. Government-led initiatives and foreign investments are crucial for driving innovation and market development. Focus is on optimizing resource management and improving operational efficiency through AI deployments.

Report Scope

This market research report provides a comprehensive analysis of the AI Accelerator Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Accelerator Chip Market?

-> AI Accelerator Chip Market size was valued at USD 18 billion in 2025. The market is projected to grow from USD 20 billion in 2026 to USD 120 billion by 2034, exhibiting a CAGR of 25% during the forecast period.

Which key companies operate AI Accelerator Chip Market?

-> Key players include NVIDIA, Intel, AMD, Google (TPU), Qualcomm, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include surging AI workloads in data centers, rapid adoption of edge AI, expanding autonomous vehicle development, and increasing demand for high‑performance computing.

Which region dominates the market?

-> North America holds the largest market share, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include neuromorphic AI chips, RISC‑V based AI processors, and enhanced integration of AI accelerators in edge devices and IoT ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...