MEMS Gas Sensor (e-nose, VOC) Market Insights

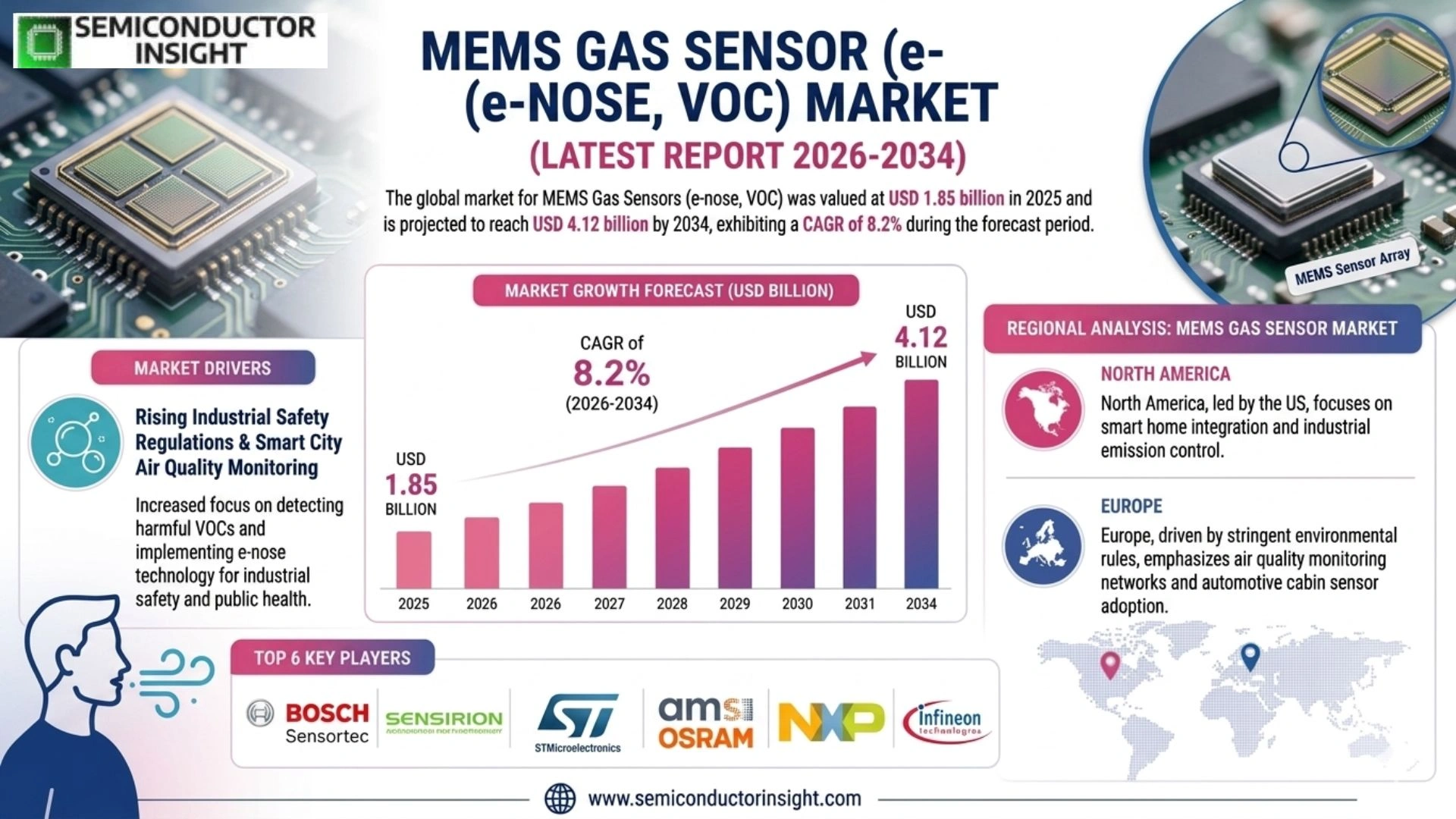

Global MEMS Gas Sensor (e-nose, VOC) Market size was valued at USD 1.85 billion in 2025. The market is projected to grow from USD 2.03 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period.

MEMS (Micro-Electro-Mechanical Systems) gas sensors are miniaturized sensing devices engineered to detect and measure volatile organic compounds (VOCs) and a broad spectrum of gaseous analytes with high sensitivity and precision. These sensors underpin electronic nose (e-nose) technologies, which replicate the olfactory function by identifying complex gas mixtures through an array of sensing elements combined with pattern recognition algorithms. The core product categories encompass metal oxide semiconductor (MOS) sensors, electrochemical sensors, optical sensors, acoustic wave sensors, and capacitive sensors, each tailored to specific detection requirements across industrial, environmental, and consumer applications.

The market is witnessing robust expansion driven by escalating demand for air quality monitoring, stringent environmental regulations governing VOC emissions, and the rapid integration of MEMS gas sensors into consumer electronics and smart home devices. Furthermore, the growing adoption of e-nose platforms in the food and beverage industry for quality control, coupled with increasing healthcare applications in non-invasive disease diagnostics through breath analysis, is significantly broadening the addressable market. Key players such as Sensirion AG, Bosch Sensortec GmbH, ams-OSRAM AG, Figaro Engineering Inc., and SGX Sensortech continue to advance their product portfolios with next-generation MEMS-based sensing solutions to capture emerging opportunities across diverse end-use sectors.

MARKET DRIVERS

Rising Demand for Air Quality Monitoring and Environmental Sensing

The MEMS gas sensor market, encompassing electronic nose (e-nose) technologies and volatile organic compound (VOC) detection systems, is experiencing robust growth driven by increasing global awareness of indoor and outdoor air quality. Regulatory bodies across North America, Europe, and Asia-Pacific have tightened emission standards and indoor air quality guidelines, compelling industries and municipalities to deploy advanced gas sensing solutions. MEMS-based gas sensors offer a compelling combination of miniaturization, low power consumption, and high sensitivity that traditional sensing technologies cannot match, making them the preferred choice for continuous environmental monitoring applications.

Expanding Integration in Consumer Electronics and IoT Ecosystems

The proliferation of smart home devices, wearables, and Internet of Things (IoT) platforms has created significant demand for compact, energy-efficient gas sensing components. MEMS gas sensors are increasingly embedded in smartphones, air purifiers, HVAC systems, and smart appliances to detect VOCs, carbon dioxide, methane, and other hazardous gases in real time. The convergence of MEMS fabrication techniques with advanced metal-oxide semiconductor (MOX) and electrochemical sensing materials has enabled sensor manufacturers to deliver high-performance e-nose modules at commercially viable price points, accelerating adoption across consumer and industrial IoT segments.

➤ The integration of artificial intelligence and machine learning algorithms with MEMS-based e-nose arrays is fundamentally transforming VOC pattern recognition capabilities, enabling applications in food quality assessment, medical diagnostics, and industrial process control that were previously not achievable with conventional single-analyte sensors.

Healthcare applications represent one of the most compelling growth drivers for the MEMS gas sensor market. Non-invasive breath analysis using e-nose technology has demonstrated clinical potential for early-stage disease biomarker detection, including respiratory conditions and metabolic disorders. Simultaneously, the food and beverage industry is leveraging VOC sensing arrays for freshness monitoring and adulteration detection, further broadening the addressable market for MEMS-based olfactory sensing platforms.

MARKET CHALLENGES

Selectivity and Cross-Sensitivity Limitations in Complex Gas Environments

Despite significant technological advancements, selectivity remains a persistent challenge for MEMS gas sensors operating in real-world environments. Metal-oxide-based MEMS sensors are inherently susceptible to cross-sensitivity, responding to multiple gas species simultaneously, which can compromise measurement accuracy in applications requiring precise VOC identification. In complex gas matrices , such as industrial exhaust streams or human breath , distinguishing target analytes from interfering compounds demands sophisticated sensor array architectures and advanced signal processing, adding cost and complexity to system design. Manufacturers continue to invest in novel sensing materials, including functionalized polymers and 2D nanomaterials, to improve selectivity without sacrificing sensitivity.

Other Challenges

Sensor Drift and Long-Term Stability

MEMS gas sensors, particularly those based on metal-oxide semiconductors, are prone to baseline drift over extended operational periods due to surface poisoning, humidity interference, and thermal aging of sensing materials. This drift necessitates periodic recalibration, which increases maintenance costs and limits deployment in unattended or remote monitoring scenarios. Addressing long-term stability through advanced encapsulation technologies and self-calibration algorithms remains an active area of development across the MEMS gas sensor industry.

High Development and Certification Costs

The development of MEMS gas sensors for regulated applications , including industrial safety, automotive cabin air quality, and medical diagnostics , requires extensive validation, reliability testing, and compliance with stringent international standards. These certification processes can be time-intensive and costly, creating barriers to entry for smaller sensor manufacturers and extending time-to-market for new product launches. The capital-intensive nature of MEMS fabrication facilities further concentrates production capacity among a limited number of established semiconductor foundries.

MARKET RESTRAINTS

Humidity and Temperature Sensitivity Affecting Sensor Accuracy

One of the most significant technical restraints facing the MEMS gas sensor market is the pronounced sensitivity of sensing materials to ambient humidity and temperature variations. Changes in relative humidity can alter the electrical resistance of metal-oxide sensing layers, generating false positive or false negative VOC readings that undermine system reliability. While compensation algorithms and integrated temperature-humidity reference sensors can partially mitigate this effect, they introduce additional Bill of Materials (BoM) costs and computational overhead. This limitation is particularly constraining in outdoor deployment scenarios and tropical climates where humidity fluctuations are substantial and unpredictable.

Fragmented Standards and Interoperability Constraints

The absence of universally accepted calibration standards and data communication protocols for MEMS gas sensors and e-nose platforms creates interoperability challenges across the supply chain. End users operating multi-vendor sensor networks face difficulties in data normalization and cross-platform comparison, reducing confidence in sensor-derived insights. The fragmentation of sensing material formulations, operating temperatures, and output signal formats across manufacturers further complicates the development of plug-and-play integration frameworks, restraining adoption in enterprise-scale deployments where standardization and scalability are paramount considerations for procurement decisions.

MARKET OPPORTUNITIES

Emerging Applications in Non-Invasive Medical Diagnostics and Breath Analysis

The application of MEMS-based e-nose technology in non-invasive medical diagnostics represents a high-value growth opportunity for market participants. Breath analysis platforms utilizing miniaturized VOC sensor arrays have shown promise in research settings for identifying disease-specific volatile biomarkers associated with respiratory, gastrointestinal, and oncological conditions. As clinical validation studies progress and regulatory pathways become better defined, medical-grade MEMS gas sensor modules are expected to transition from research environments into point-of-care diagnostic devices, opening a substantial new revenue stream for sensor manufacturers and integrated system providers.

Smart Agriculture and Food Safety Monitoring

Precision agriculture and intelligent food supply chain management present significant untapped opportunities for MEMS gas sensor deployment. VOC detection in post-harvest storage facilities enables early identification of spoilage, fungal contamination, and ripening stage, reducing food waste and improving supply chain efficiency. Similarly, e-nose systems are gaining traction in quality assurance applications for premium food and beverage products, including coffee, wine, and edible oils, where consistent flavor profiling and adulteration detection add measurable commercial value. The decreasing cost trajectory of MEMS sensor fabrication is making these applications economically viable at scale for the first time.

Industrial Safety and Occupational Health in Hazardous Environments

Stringent occupational health and safety regulations governing exposure to hazardous VOCs and toxic industrial gases are driving adoption of MEMS gas sensors in manufacturing, petrochemical, mining, and semiconductor fabrication facilities. The miniaturization advantage of MEMS technology enables the development of wearable personal gas detection devices that provide continuous worker exposure monitoring, complementing fixed-point detection infrastructure. As industrial facilities accelerate their digital transformation initiatives and adopt connected worker platforms, the demand for low-power, network-connected MEMS gas sensing nodes is expected to grow considerably, creating a sustained and scalable market opportunity for sensor vendors and system integrators operating in the occupational safety domain.

Trends

Rising Demand for Air Quality Monitoring Drives MEMS Gas Sensor Adoption

MEMS Gas Sensor (e-nose, VOC) Market is experiencing significant momentum as governments and regulatory bodies worldwide tighten environmental standards around volatile organic compound emissions. Industrial facilities, commercial buildings, and urban infrastructure are increasingly deploying MEMS-based gas sensing systems to ensure compliance with air quality mandates. The compact form factor, low power consumption, and high sensitivity of MEMS gas sensors make them particularly well-suited for continuous, real-time environmental monitoring applications. This regulatory push has become one of the most consistent growth catalysts shaping the market landscape.

Other Trends

Integration into Consumer Electronics and Smart Home Devices

A notable trend MEMS Gas Sensor (e-nose, VOC) Market is the accelerating integration of miniaturized VOC sensors into consumer-grade products such as smart air purifiers, wearable devices, and home automation systems. Leading MEMS sensor manufacturers including Sensirion AG and Bosch Sensortec GmbH have developed ultra-compact sensor modules optimized for integration into handheld and IoT-connected devices. As consumer awareness of indoor air quality continues to grow, demand for embedded gas sensing capabilities within everyday electronics is expected to intensify across both developed and emerging markets.

E-Nose Technology Expanding into Food and Beverage Quality Control

Electronic nose platforms leveraging MEMS gas sensor arrays are gaining considerable traction in the food and beverage industry. These systems utilize pattern recognition algorithms combined with multi-sensor arrays to assess freshness, detect spoilage, and authenticate product quality without destructive testing. The ability of e-nose technology to replicate complex olfactory assessments with consistency and speed presents a compelling value proposition for food manufacturers seeking to enhance quality assurance processes and reduce dependence on trained human sensory panels.

Healthcare Applications Through Breath Analysis

Non-invasive disease diagnostics via breath analysis represents one of the most transformative emerging applications withMEMS Gas Sensor (e-nose, VOC) Market. Researchers and clinical developers are leveraging VOC detection capabilities to identify biomarker patterns associated with conditions such as diabetes, lung disease, and metabolic disorders. Companies including ams-OSRAM AG and Figaro Engineering Inc. are advancing sensor chemistries and signal processing technologies to meet the sensitivity and selectivity requirements demanded by medical-grade breath analysis platforms.

Technological Advancements Reinforcing Competitive Differentiation

Ongoing innovations in metal oxide semiconductor sensor design, acoustic wave sensing, and optical detection are enabling next-generation MEMS gas sensors with enhanced selectivity and reduced cross-sensitivity to interfering gases. Key market participants such as SGX Sensortech continue to invest in advanced fabrication techniques to improve sensor durability, response times, and calibration stability. These technological advancements are expected to broaden the application scope of MEMS Gas Sensor (e-nose, VOC) Market across industrial safety, environmental monitoring, automotive cabin air quality, and precision agriculture over the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

MEMS Gas Sensor (E-Nose, VOC) Market: Competitive Dynamics and Leading Innovators Shaping the Industry

Global MEMS Gas Sensor (e-nose, VOC) Market is characterized by a moderately consolidated competitive landscape, with a mix of established semiconductor giants and specialized sensing technology firms vying for market share. Sensirion AG holds a prominent position in the market, leveraging its expertise in digital gas and environmental sensors to deliver high-accuracy VOC and air quality monitoring solutions that are widely adopted across consumer electronics, HVAC, and industrial applications. Bosch Sensortec GmbH is another dominant force, offering its BME688 environmental sensor that integrates gas, humidity, pressure, and temperature sensing in a single MEMS package , a product widely recognized for enabling e-nose functionality in smart devices. ams-OSRAM AG reinforces the competitive field through its advanced chemical sensing platforms, while companies such as Figaro Engineering Inc. and SGX Sensortech continue to maintain strong footholds through decades of application-specific sensor expertise. The market is further driven by increasing R&D investment across players to develop next-generation low-power, miniaturized MEMS solutions that align with stringent VOC emission regulations and the growing demand for real-time air quality intelligence.

Beyond the market leaders, a range of niche and regionally significant players contribute to the competitive ecosystem of the MEMS Gas Sensor market. Amphenol Advanced Sensors and Alphasense Ltd. are recognized for their electrochemical and metal oxide sensing solutions catering to industrial safety and environmental monitoring segments. Honeywell International Inc. leverages its broad sensing portfolio to serve process industries and smart building applications. AMS AG, Omron Corporation, and Murata Manufacturing Co., Ltd. add competitive depth through their diversified MEMS capabilities and global distribution networks. Emerging players such as Nanoscent and Aryballe are pioneering digital olfaction platforms that integrate e-nose technologies with artificial intelligence, targeting food quality, healthcare diagnostics, and consumer fragrance applications. This diverse competitive landscape underscores the accelerating pace of innovation and the broadening application scope of MEMS-based gas sensing technologies through 2034.

List of Key MEMS Gas Sensor Companies Profiled

- Sensirion AG

- Bosch Sensortec GmbH

- ams-OSRAM AG

- Figaro Engineering Inc.

- SGX Sensortech

- Amphenol Advanced Sensors

- Alphasense Ltd.

- Honeywell International Inc.

- Omron Corporation

- Murata Manufacturing Co., Ltd.

- Nanoscent

- Aryballe

- Winsen Electronics Technology Co., Ltd.

- TDK Corporation

- Renesas Electronics Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Metal Oxide Semiconductor (MOS) Sensors represent the leading segment within the MEMS gas sensor market, owing to their well-established manufacturing compatibility with standard CMOS fabrication processes and their inherent versatility in detecting a broad range of volatile organic compounds.

|

| By Application |

|

Air Quality Monitoring stands as the dominant application segment, propelled by intensifying global regulatory frameworks targeting VOC emissions and a heightened public awareness surrounding indoor and outdoor air pollution and its long-term health implications.

|

| By End User |

|

Industrial and Manufacturing remains the leading end-user segment, driven by the critical need for continuous VOC emission monitoring, hazardous gas leak detection, and occupational safety compliance across process-intensive industries such as petrochemicals, pharmaceuticals, and semiconductor fabrication.

|

| By Technology Platform |

|

Electronic Nose (E-Nose) Arrays represent the most technologically sophisticated and fastest-evolving platform segment, combining multiple heterogeneous MEMS sensing elements with advanced pattern recognition algorithms and machine learning models to replicate and exceed the discriminatory power of biological olfactory systems.

|

| By Connectivity and Integration |

|

Wireless and IoT-Enabled Sensors constitute the leading and most dynamically expanding connectivity segment, reflecting the overarching industry transition toward interconnected sensing ecosystems that enable remote monitoring, data aggregation, and cloud-based analytics at scale.

|

Regional Analysis: MEMS Gas Sensor (e-nose, VOC) Market

Asia-Pacific

Asia-Pacific hosts a highly integrated MEMS fabrication supply chain, with foundries, packaging specialists, and component suppliers clustered in China, Taiwan, and South Korea. This concentration reduces lead times and production costs for MEMS gas sensor manufacturers, enabling faster commercialization of new e-nose and VOC detection platforms compared to other global regions.

Governments across Asia-Pacific are tightening air quality standards and industrial emission regulations, creating sustained institutional demand for MEMS-based VOC monitoring solutions. China’s ongoing pollution control campaigns and Japan’s occupational safety frameworks are compelling industrial operators to deploy continuous gas sensing infrastructure at scale.

The region’s dominance in consumer electronics manufacturing has accelerated the embedding of miniaturized MEMS gas sensors into smartphones, wearables, and smart home devices. South Korean and Chinese OEMs are among the earliest adopters of integrated e-nose modules for indoor air quality monitoring, reflecting strong consumer appetite for health-conscious connected devices.

Academic institutions and government-backed research centers across Japan, China, and South Korea are actively advancing MEMS gas sensor sensitivity, selectivity, and power efficiency. Collaborative programs between universities and industry players are yielding next-generation VOC sensor arrays with artificial intelligence-driven pattern recognition capabilities for e-nose applications.

North America

North America represents a technologically sophisticated and high-value segment of the global MEMS gas sensor and e-nose market. The United States leads regional demand, underpinned by robust investment in environmental monitoring infrastructure, industrial process safety, and advanced healthcare diagnostics. The presence of leading MEMS technology companies, well-funded research universities, and a mature venture capital ecosystem creates fertile conditions for continuous innovation in VOC detection and electronic nose platforms. Federal regulatory bodies such as the EPA and OSHA enforce stringent air quality and occupational exposure standards, generating sustained institutional procurement of gas sensing solutions. The defense and aerospace sectors also represent significant niche demand, with MEMS-based chemical sensing technologies being evaluated for threat detection and environmental surveillance applications. Canada contributes through growing smart building and clean energy initiatives that incorporate distributed VOC monitoring. The region’s strong emphasis on miniaturization, low-power design, and wireless connectivity is shaping the next generation of portable e-nose devices aimed at clinical and field diagnostic use cases.

Europe

Europe occupies a prominent position in the global MEMS gas sensor market, distinguished by its rigorous environmental legislation, advanced automotive industry, and growing focus on occupational health and indoor air quality. The European Union’s comprehensive chemical safety directives and air quality frameworks create a strong regulatory pull for VOC monitoring technologies across industrial, commercial, and residential sectors. Germany, France, and the Netherlands are key innovation hubs, with established MEMS research centers and automotive OEMs integrating e-nose technologies into cabin air management and emission monitoring systems. The region’s well-developed food and beverage industry is also emerging as a significant application area, where electronic nose platforms are being deployed for freshness detection, quality control, and contamination screening. European cleantech investment trends are further accelerating the adoption of MEMS gas sensors in smart building management and urban air quality networks, reinforcing the region’s position as a premium-value market with strong long-term growth credentials through 2034.

South America

South America represents an emerging opportunity within the global MEMS gas sensor and VOC monitoring landscape, with growth anchored in expanding industrial activity, rising environmental awareness, and gradual regulatory modernization. Brazil dominates regional demand, with its substantial agricultural, petrochemical, and mining sectors creating practical requirements for gas detection and emissions monitoring solutions. The region’s food processing industry presents a compelling application frontier for e-nose technologies, particularly for quality assurance in export-oriented agricultural commodities. While infrastructure limitations and economic volatility have historically moderated technology adoption rates, increasing government emphasis on environmental compliance and occupational safety is beginning to stimulate institutional procurement of MEMS-based sensing systems. As regional manufacturing capabilities mature and international technology partnerships deepen, South America is expected to gradually increase its share of the global MEMS gas sensor market through the forecast period.

Middle East & Africa

The Middle East and Africa region presents a long-term growth narrative for the MEMS gas sensor and e-nose market, shaped by the hydrocarbon industry’s pervasive safety requirements, expanding urban infrastructure investment, and rising public health awareness. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, represent the most advanced adoption environments, where oil and gas operators deploy continuous VOC and toxic gas monitoring systems across upstream and downstream facilities to meet both safety mandates and sustainability commitments. Smart city programs in Dubai and Riyadh are integrating distributed air quality sensing networks that incorporate MEMS-based gas detection nodes. Africa, while at an earlier stage of market development, is witnessing growing demand for affordable gas monitoring solutions tied to mining safety, industrial expansion, and urban pollution management. Improving telecommunications infrastructure and increasing foreign direct investment in manufacturing are expected to gradually unlock broader adoption of MEMS gas sensor technologies across the continent through 2034.

Report Scope

This market research report provides a comprehensive analysis of the MEMS Gas Sensor (e-nose, VOC) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MEMS Gas Sensor (e-nose, VOC) Market?

-> MEMS Gas Sensor (e-nose, VOC) Market was valued at USD 1.85 billion in 2025 and is expected to reach USD 4.12 billion by 2034, growing at a CAGR of 8.2% during the forecast period from 2026 to 2034.

Which key companies operate MEMS Gas Sensor (e-nose, VOC) Market?

-> Key players include Sensirion AG, Bosch Sensortec GmbH, ams-OSRAM AG, Figaro Engineering Inc., and SGX Sensortech, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for air quality monitoring, stringent environmental regulations governing VOC emissions, rapid integration of MEMS gas sensors into consumer electronics and smart home devices, growing adoption of e-nose platforms in the food and beverage industry for quality control, and increasing healthcare applications in non-invasive disease diagnostics through breath analysis.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by expanding industrial and consumer electronics sectors, while North America and Europe remain significant markets due to stringent environmental regulations and advanced healthcare infrastructure.

What are the emerging trends?

-> Emerging trends include next-generation MEMS-based sensing solutions, integration of electronic nose (e-nose) technologies with pattern recognition algorithms, adoption of metal oxide semiconductor (MOS) sensors, electrochemical sensors, optical sensors, acoustic wave sensors, and capacitive sensors across industrial, environmental, and consumer applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...