MEMS Accelerometer (Consumer, Automotive, Industrial) Market Insights

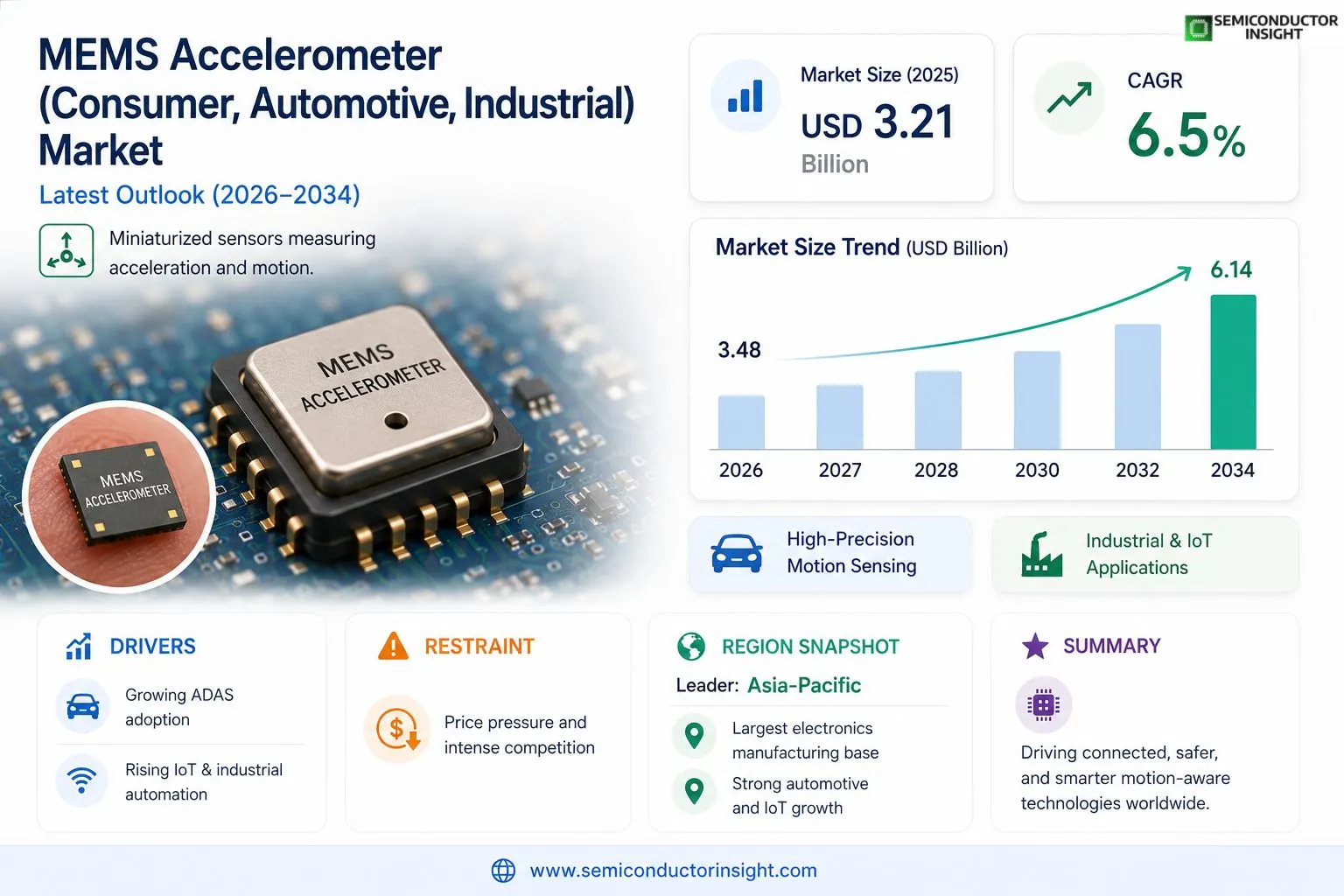

Global MEMS Accelerometer (Consumer, Automotive, Industrial) market size was valued at USD 3.21 billion in 2025. The market is projected to grow from USD 3.48 billion in 2026 to USD 6.14 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

MEMS (Micro-Electro-Mechanical Systems) accelerometers are miniaturized sensors that measure acceleration forces , static, such as gravity, or dynamic, such as vibration or movement , across one or more axes. These devices are widely deployed across consumer electronics, automotive systems, and industrial applications, encompassing smartphones, wearables, vehicle stability control systems, airbag deployment modules, condition monitoring equipment, and robotics platforms.

The market is witnessing robust expansion driven by the accelerating adoption of advanced driver-assistance systems (ADAS) in the automotive sector, the proliferation of IoT-enabled industrial devices, and the sustained demand for motion-sensing capabilities in consumer electronics. Furthermore, the integration of MEMS accelerometers in electric vehicles (EVs) and the growing emphasis on predictive maintenance in industrial automation are reinforcing market momentum. Key players operating in this space , including STMicroelectronics, Bosch Sensortec, Analog Devices, Inc., TDK Corporation (InvenSense), and NXP Semiconductors , continue to expand their product portfolios through innovation in low-power, high-precision sensing technologies.

MARKET DRIVERS

Surging Adoption of MEMS Accelerometers in Consumer Electronics

MEMS Accelerometer (Consumer, Automotive, Industrial) Market has experienced robust growth driven by the widespread integration of motion-sensing technologies in smartphones, wearables, and smart home devices. Modern consumer electronics increasingly rely on MEMS accelerometers for screen orientation, gesture recognition, fitness tracking, and image stabilization. Global proliferation of smartphones,with shipments consistently exceeding one billion units annually,has created an enormous baseline demand for high-performance, low-power MEMS accelerometer solutions. As wearable device adoption accelerates across fitness bands, smartwatches, and hearables, manufacturers are sourcing increasingly compact and energy-efficient MEMS sensors to meet stringent design requirements.

Automotive Safety Regulations and ADAS Expansion Fueling Market Growth

The automotive segment represents one of the most significant growth engines for MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Stringent government mandates requiring electronic stability control (ESC), airbag deployment systems, and advanced driver-assistance systems (ADAS) in new vehicles have made MEMS accelerometers an indispensable component in modern automotive architectures. As the automotive industry transitions toward electric vehicles (EVs) and autonomous driving platforms, the demand for high-reliability, temperature-resilient MEMS inertial sensors has intensified considerably. Each new vehicle generation integrates multiple accelerometer nodes for collision detection, rollover prevention, adaptive suspension, and navigation systems, multiplying per-vehicle sensor content.

➤ The transition to Level 3 and Level 4 autonomous driving architectures is expected to increase the average number of MEMS inertial sensors per vehicle significantly, as redundant sensing layers become mandatory for functional safety compliance under ISO 26262 standards.

Industrial automation and the broader Industrial Internet of Things (IIoT) ecosystem are contributing meaningfully to demand across MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Predictive maintenance platforms, condition monitoring systems, and industrial robotics applications require ruggedized MEMS accelerometers capable of operating reliably under harsh environmental conditions. As manufacturers invest in smart factory infrastructure and digital twin technologies, the deployment of vibration and motion sensors across production equipment has expanded substantially, reinforcing sustained demand across the industrial vertical.

MARKET CHALLENGES

Intense Price Competition and Margin Pressure Across Consumer Segments

One of the most persistent challenges confronting participants in MEMS Accelerometer (Consumer, Automotive, Industrial) Market is severe price erosion in consumer-grade segments. As the technology has matured, commoditization has accelerated, compelling suppliers to continuously reduce average selling prices to remain competitive. This dynamic compresses gross margins and forces manufacturers to achieve higher production volumes to maintain revenue targets. Smaller and mid-tier MEMS accelerometer vendors, in particular, face difficulties investing in next-generation process nodes and advanced packaging technologies when operating under sustained pricing pressure from large-scale competitors with superior economies of scale.

Other Challenges

Complex Automotive Qualification Requirements

Supplying MEMS accelerometers into the automotive segment demands compliance with rigorous qualification standards including AEC-Q100, IATF 16949, and functional safety certifications under ISO 26262. These certification processes are time-consuming and resource-intensive, often requiring multi-year development cycles before a new MEMS accelerometer design achieves production approval. For emerging suppliers seeking to penetrate the automotive vertical of MEMS Accelerometer (Consumer, Automotive, Industrial) Market, these barriers represent substantial challenges in terms of both timeline and capital expenditure.

Supply Chain Vulnerabilities and Semiconductor Shortages

MEMS Accelerometer (Consumer, Automotive, Industrial) Market remains exposed to periodic semiconductor supply chain disruptions, as demonstrated during Global chip shortage cycle. MEMS fabrication relies on specialized foundry capacity and proprietary process technologies that are not easily substitutable. Geopolitical tensions and concentration risks in wafer fabrication geography have prompted OEMs to seek supply chain diversification, but transitioning qualified MEMS accelerometer suppliers involves lengthy re-qualification processes that limit agility in responding to supply disruptions.

Technical Complexity in High-Performance Industrial Applications

Industrial applications increasingly demand MEMS accelerometers with superior noise density, wider dynamic range, and enhanced temperature stability compared to consumer-grade equivalents. Meeting these specifications while maintaining cost competitiveness presents significant engineering challenges. Achieving the balance between sensitivity, bandwidth, power consumption, and robustness required for advanced industrial condition monitoring and precision motion control applications demands continuous R&D investment, which strains development resources, particularly for smaller market participants in MEMS Accelerometer (Consumer, Automotive, Industrial) Market.

MARKET RESTRAINTS

Technology Substitution Risk from Alternative Sensing Modalities

A notable restraint on MEMS Accelerometer (Consumer, Automotive, Industrial) Market is the potential displacement of standalone accelerometers by integrated inertial measurement units (IMUs) and multi-axis sensor fusion platforms. As system designers migrate toward consolidated sensor architectures that combine accelerometers, gyroscopes, magnetometers, and pressure sensors within a single package, the addressable market for discrete MEMS accelerometers may face contraction in certain application segments. While this trend simultaneously creates opportunity for higher-value integrated solutions, it represents a meaningful restraint for suppliers focused exclusively on standalone accelerometer products.

High Capital Intensity of MEMS Fabrication Infrastructure

The capital-intensive nature of MEMS semiconductor fabrication represents a structural restraint on new market entrants and capacity expansion initiatives within MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Establishing or upgrading a MEMS-capable fabrication facility requires substantial capital investment, and the proprietary nature of MEMS process technologies limits access to standard foundry services. This dynamic concentrates production capacity among a relatively small number of established players, constraining supply flexibility and creating bottlenecks during periods of elevated demand. Fabless design companies face dependency risks on a limited pool of MEMS foundry partners, which can restrict their ability to scale output rapidly in response to market demand cycles.

Regulatory and Compliance Complexity Across Global Markets

Divergent regulatory frameworks governing electronics, automotive safety, and industrial equipment across major geographic markets impose incremental compliance costs and complexity on MEMS accelerometer manufacturers. Navigating varying RoHS directives, REACH regulations, export control requirements, and regional automotive homologation standards requires dedicated regulatory affairs capabilities and adds to the overall cost structure of operating in Global MEMS Accelerometer (Consumer, Automotive, Industrial) Market. For manufacturers targeting simultaneous penetration of consumer, automotive, and industrial verticals across multiple geographies, managing this regulatory complexity represents an ongoing operational restraint.

MARKET OPPORTUNITIES

Expansion of IoT and Smart Infrastructure Creating New Application Frontiers

The rapid expansion of Internet of Things ecosystems across smart cities, connected infrastructure, and industrial automation platforms presents significant untapped opportunity for MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Structural health monitoring of bridges, buildings, and critical infrastructure requires distributed accelerometer networks capable of detecting micro-vibrations and seismic activity over extended operational lifetimes. As governments and private sector entities invest in smart infrastructure modernization, demand for durable, low-power MEMS accelerometers optimized for long-term field deployment is projected to grow meaningfully, opening addressable markets beyond traditional consumer and automotive end-uses.

Electric Vehicle and Two-Wheeler Electrification as a High-Growth Vertical

Global transition toward electric mobility,encompassing passenger EVs, commercial electric vehicles, and the rapidly expanding electric two- and three-wheeler segment, particularly across Asia-Pacific markets,represents a compelling growth opportunity for MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Electric drivetrains introduce new motion sensing requirements for battery management system protection, regenerative braking optimization, and vehicle dynamics control that differ from conventional internal combustion engine platforms. MEMS accelerometer suppliers capable of developing application-specific solutions tailored to EV architectural requirements are well-positioned to capture incremental content gains as electrification penetration deepens across global automotive markets.

Advances in Low-Power and AI-Integrated MEMS Accelerometer Design

Ongoing semiconductor innovation is unlocking new performance frontiers that expand the addressable opportunity for MEMS Accelerometer (Consumer, Automotive, Industrial) Market. The integration of always-on machine learning inference engines directly within MEMS accelerometer packages enables real-time edge processing of motion data without transmitting raw sensor streams to central processors, dramatically reducing system power consumption. This capability is particularly valuable for battery-powered wearable and IoT applications where energy efficiency is critical. Suppliers investing in AI-augmented MEMS accelerometer architectures are positioned to differentiate their offerings and command premium pricing, countering commoditization pressures prevalent in standard consumer-grade product lines and driving higher-value market participation across all three end-use verticals.

Trends

Rising Adoption of ADAS Fueling Demand in the Automotive Segment

MEMS Accelerometer (Consumer, Automotive, Industrial) Market is experiencing a significant shift driven by the rapid integration of advanced driver-assistance systems (ADAS) across passenger and commercial vehicles. Automakers are increasingly embedding high-precision MEMS accelerometers in stability control units, airbag deployment modules, and electronic braking systems to enhance vehicle safety and comply with evolving regulatory standards. As electric vehicles gain global traction, the demand for reliable, low-power inertial sensing solutions has intensified, with MEMS accelerometers serving as critical components in battery management and chassis dynamics monitoring. This trend is reinforcing the pivotal role of automotive applications within the broader MEMS Accelerometer (Consumer, Automotive, Industrial) Market landscape.

Other Trends

Expansion of IoT-Enabled Industrial Devices

Industrial automation and the widespread deployment of IoT-connected machinery are reshaping demand dynamics in MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Manufacturers across sectors such as aerospace, energy, and heavy machinery are adopting MEMS accelerometers for real-time condition monitoring and predictive maintenance, reducing unplanned downtime and operational costs. The shift from reactive to proactive maintenance strategies has made high-sensitivity accelerometers indispensable in smart factory environments, further accelerating market adoption in the industrial segment.

Sustained Consumer Electronics Demand and Wearable Technology Growth

Consumer electronics continues to be a foundational pillar of MEMS Accelerometer (Consumer, Automotive, Industrial) Market. Smartphones, fitness trackers, smartwatches, and augmented reality devices rely on multi-axis MEMS accelerometers for motion detection, screen orientation, and gesture recognition. As wearable technology evolves toward health monitoring applications , including fall detection and activity tracking , the requirement for compact, energy-efficient accelerometers is growing steadily. Leading manufacturers such as STMicroelectronics, Bosch Sensortec, and TDK Corporation (InvenSense) are advancing low-power sensing architectures specifically tailored for wearable and portable consumer devices.

Innovation in Low-Power, High-Precision Sensing Technologies

Technological innovation remains a defining trend in MEMS Accelerometer (Consumer, Automotive, Industrial) Market, with key players including Analog Devices, Inc. and NXP Semiconductors investing substantially in next-generation sensor designs. Advances in signal processing, noise reduction, and miniaturization are enabling accelerometers to deliver enhanced accuracy at reduced power consumption , a critical requirement across all three end-use verticals. The convergence of MEMS accelerometers with artificial intelligence-driven edge computing platforms is also emerging as a forward-looking trend, enabling smarter, autonomous sensing at the device level and opening new application frontiers across consumer, automotive, and industrial domains.

COMPETITIVE LANDSCAPE

Key Industry Players

MEMS Accelerometer (Consumer, Automotive, Industrial) Market: Competitive Intelligence and Strategic Positioning of Leading Sensor Manufacturers

Global MEMS Accelerometer market is characterized by a moderately consolidated competitive landscape, with a handful of technologically advanced semiconductor and sensor manufacturers commanding significant market share across the consumer, automotive, and industrial verticals. STMicroelectronics stands as a dominant force in the market, leveraging its broad portfolio of high-performance, low-power MEMS accelerometers widely adopted in smartphones, wearables, and automotive safety systems including airbag deployment and electronic stability control. Bosch Sensortec, a subsidiary of Robert Bosch GmbH, maintains a formidable presence driven by deep integration with the automotive sector and a robust lineup of inertial sensors catering to ADAS and IoT applications. Analog Devices, Inc. and TDK Corporation (operating through its InvenSense division) are also pivotal players, continuously advancing precision sensing technologies for industrial condition monitoring, robotics, and motion-tracking platforms. NXP Semiconductors reinforces the automotive-grade accelerometer segment, offering solutions compliant with functional safety standards such as ISO 26262.

Beyond the tier-one leaders, the MEMS Accelerometer market hosts a competitive set of niche and regionally significant players that contribute meaningfully to product diversification and application-specific innovation. Murata Manufacturing Co., Ltd. holds a strong foothold in automotive-grade inertial sensors, while Kionix (a ROHM Group company) serves consumer and industrial segments with compact, energy-efficient accelerometer solutions. Honeywell International and TE Connectivity address specialized industrial and aerospace applications requiring high-reliability sensing under extreme environmental conditions. Memsic Semiconductor and mCube cater to cost-sensitive consumer electronics segments, while companies such as Colibrys (now part of Safran) and Silicon Sensing Systems focus on high-precision, defense-grade inertial sensing. The competitive intensity is further amplified by increasing investments in electric vehicle integration, predictive maintenance systems, and miniaturized wearable devices, compelling all market participants to accelerate R&D cycles and expand manufacturing capabilities to sustain long-term growth.

List of Key MEMS Accelerometer Companies Profiled

- STMicroelectronics

- Bosch Sensortec GmbH

- Analog Devices, Inc.

- TDK Corporation (InvenSense)

- NXP Semiconductors

- Murata Manufacturing Co., Ltd.

- Kionix, Inc. (ROHM Group)

- Honeywell International Inc.

- TE Connectivity

- Memsic Semiconductor Co., Ltd.

- mCube Inc.

- Colibrys Ltd. (Safran Group)

- Silicon Sensing Systems Ltd.

- Northrop Grumman LITEF GmbH

- Microchip Technology Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tri-Axis MEMS Accelerometers represent the dominant type segment, driven by their ability to capture comprehensive three-dimensional motion data in a single compact package.

|

| By Application |

|

Automotive Safety & ADAS stands as the leading application segment, underpinned by the accelerating global rollout of advanced driver-assistance systems and the surging adoption of electric vehicles.

|

| By End User |

|

Automotive OEMs & Tier-1 Suppliers constitute the leading end-user segment, reflecting the automotive industry’s deep reliance on high-reliability MEMS sensing technology across safety-critical and performance-driven applications.

|

| By Technology |

|

Capacitive MEMS Accelerometers lead the technology segment owing to their well-established performance profile, which combines low power consumption with high sensitivity and robust noise immunity.

|

| By Range |

|

Low-g Accelerometers represent the dominant range segment, primarily serving the expansive consumer electronics and wearables market where precise detection of subtle motion, tilt, and gravitational orientation is a core functional requirement.

|

Regional Analysis: MEMS Accelerometer (Consumer, Automotive, Industrial) Market

Asia-Pacific

Asia-Pacific’s consumer electronics supply chain is deeply integrated with MEMS accelerometer production. The region’s dominance in smartphone, wearable, and gaming device manufacturing creates a perpetual and high-volume demand stream. Local ODMs and OEMs routinely embed MEMS accelerometer sensors into devices at a scale that no other region approaches, ensuring continued market primacy through the forecast period.

The rapid electrification of vehicle fleets across China and growing ADAS adoption throughout Southeast Asia are powerful catalysts for automotive-grade MEMS accelerometer demand. Automakers in the region are integrating these sensors into electronic stability control, airbag deployment, and advanced driver-assistance systems, establishing Asia-Pacific as a critical hub for automotive MEMS accelerometer sourcing and deployment.

China’s “Made in China 2025” initiative and Japan’s Society 5.0 vision are accelerating industrial automation investments, directly boosting demand for industrial-grade MEMS accelerometers used in predictive maintenance, vibration monitoring, and precision robotics. The region’s factory modernization wave shows no signs of slowing, ensuring robust industrial segment growth throughout the 2026–2034 forecast window.

Government-backed investments in MEMS fabrication capacity across China, South Korea, and Taiwan are reducing the region’s reliance on imported sensor components. This strategic push toward semiconductor self-sufficiency is strengthening the regional MEMS accelerometer supply chain, lowering production costs, and enabling faster commercialization of next-generation consumer, automotive, and industrial sensor platforms.

North America

North America represents a technologically advanced and high-value segment of Global MEMS accelerometer market, with the United States serving as the primary engine of growth. The region’s strength lies in its robust automotive innovation ecosystem, particularly around autonomous vehicles and advanced driver-assistance systems, where automotive-grade MEMS accelerometers play a mission-critical role. Silicon Valley and the broader U.S. semiconductor corridor continue to drive breakthroughs in MEMS design and packaging, attracting significant R&D investment from both private enterprises and federal programs. The industrial segment is equally vibrant, with aerospace, defense, and energy sectors deploying high-performance MEMS accelerometers for structural health monitoring and navigation applications. Consumer demand remains strong, fueled by the widespread adoption of connected devices, AR/VR headsets, and fitness wearables. Canada is also gaining recognition as a growing hub for MEMS-based sensor innovation, particularly in cleantech and industrial IoT applications. North America’s regulatory environment and emphasis on safety standards further reinforce the demand for precision MEMS accelerometer solutions across all three end-use segments throughout the forecast period.

Europe

Europe occupies a strategically significant position in Global MEMS accelerometer market, underpinned by its world-class automotive manufacturing base and stringent vehicle safety regulations. Germany, France, and the United Kingdom are the principal contributors to regional demand, with the automotive segment leading adoption as European automakers accelerate electrification and integrate advanced sensor suites into next-generation vehicles. The region’s industrial sector, particularly in precision machinery, robotics, and smart factory infrastructure, is a consistent driver of industrial-grade MEMS accelerometer uptake. Europe’s commitment to the European Green Deal and Industry 4.0 transformation is channeling investment into connected manufacturing environments where MEMS-based motion sensing is indispensable. On the consumer side, demand for wearables and health-monitoring devices is growing steadily. European research institutions and universities also play a meaningful role in advancing MEMS accelerometer technology, fostering close collaboration between academia and industry. Regulatory frameworks around functional safety in automotive applications, particularly ISO 26262, ensure that high-reliability MEMS accelerometers remain a non-negotiable component of European vehicle architectures through 2034.

South America

South America is an emerging growth frontier for the MEMS accelerometer market, gradually building momentum across consumer, automotive, and industrial segments. Brazil dominates regional activity, supported by a growing automotive assembly industry and an expanding middle class with rising appetite for consumer electronics. As vehicle production in Brazil and Argentina adopts more electronically sophisticated platforms to meet evolving safety standards, demand for automotive-grade MEMS accelerometers is expected to increase steadily. The industrial mining and oil and gas sectors across the Andean region present a compelling use case for robust MEMS accelerometer sensors in equipment monitoring and predictive maintenance. Consumer electronics penetration, while still below global averages, is rising consistently as smartphone and wearable adoption accelerates among younger demographics. Infrastructure investment limitations and currency volatility remain constraints on faster market development, but the longer-term trajectory for South America’s MEMS accelerometer market remains positive, particularly as regional manufacturing capabilities mature and international sensor suppliers deepen their distribution networks in the region.

Middle East & Africa

The Middle East and Africa region represents the early-stage opportunity segment of Global MEMS accelerometer market, characterized by nascent but increasingly promising demand dynamics. In the Middle East, Gulf Cooperation Council nations are channeling significant investment into smart city development, industrial automation, and transportation infrastructure modernization, all of which create tangible demand for MEMS accelerometer technology in both industrial and automotive applications. The UAE and Saudi Arabia are particularly active in deploying sensor-enabled smart infrastructure as part of their economic diversification agendas. Africa’s MEMS accelerometer market is at an earlier stage of development, with consumer electronics adoption serving as the primary near-term growth lever, particularly in South Africa, Nigeria, and Kenya where smartphone penetration is expanding rapidly. Industrial applications in mining and resource extraction offer a longer-term growth avenue for ruggedized MEMS accelerometer sensors. While the region currently accounts for a modest share of Global MEMS accelerometer market, rising urbanization, growing industrial investment, and increasing digital infrastructure development are expected to drive gradual but consistent market expansion through the 2026–2034 forecast period.

Report Scope

This market research report provides a comprehensive analysis of the MEMS Accelerometer (Consumer, Automotive, Industrial) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MEMS Accelerometer (Consumer, Automotive, Industrial) Market?

-> MEMS Accelerometer (Consumer, Automotive, Industrial) Market was valued at USD 3.21 billion in 2025 and is expected to reach USD 6.14 billion by 2034, growing at a CAGR of 6.5% during the forecast period from 2026 to 2034.

Which key companies operate in MEMS Accelerometer (Consumer, Automotive, Industrial) Market?

-> Key players include STMicroelectronics, Bosch Sensortec, Analog Devices, Inc., TDK Corporation (InvenSense), and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include accelerating adoption of advanced driver-assistance systems (ADAS) in the automotive sector, proliferation of IoT-enabled industrial devices, sustained demand for motion-sensing capabilities in consumer electronics, integration of MEMS accelerometers in electric vehicles (EVs), and growing emphasis on predictive maintenance in industrial automation.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by strong consumer electronics manufacturing and automotive production, while North America and Europe remain significant markets owing to advanced automotive and industrial automation sectors.

What are the emerging trends?

-> Emerging trends include low-power high-precision sensing technologies, integration of MEMS accelerometers in electric vehicles (EVs), expansion of IoT-enabled industrial devices, adoption of MEMS sensors in robotics platforms, and innovation in condition monitoring and predictive maintenance solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...