Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market Insights

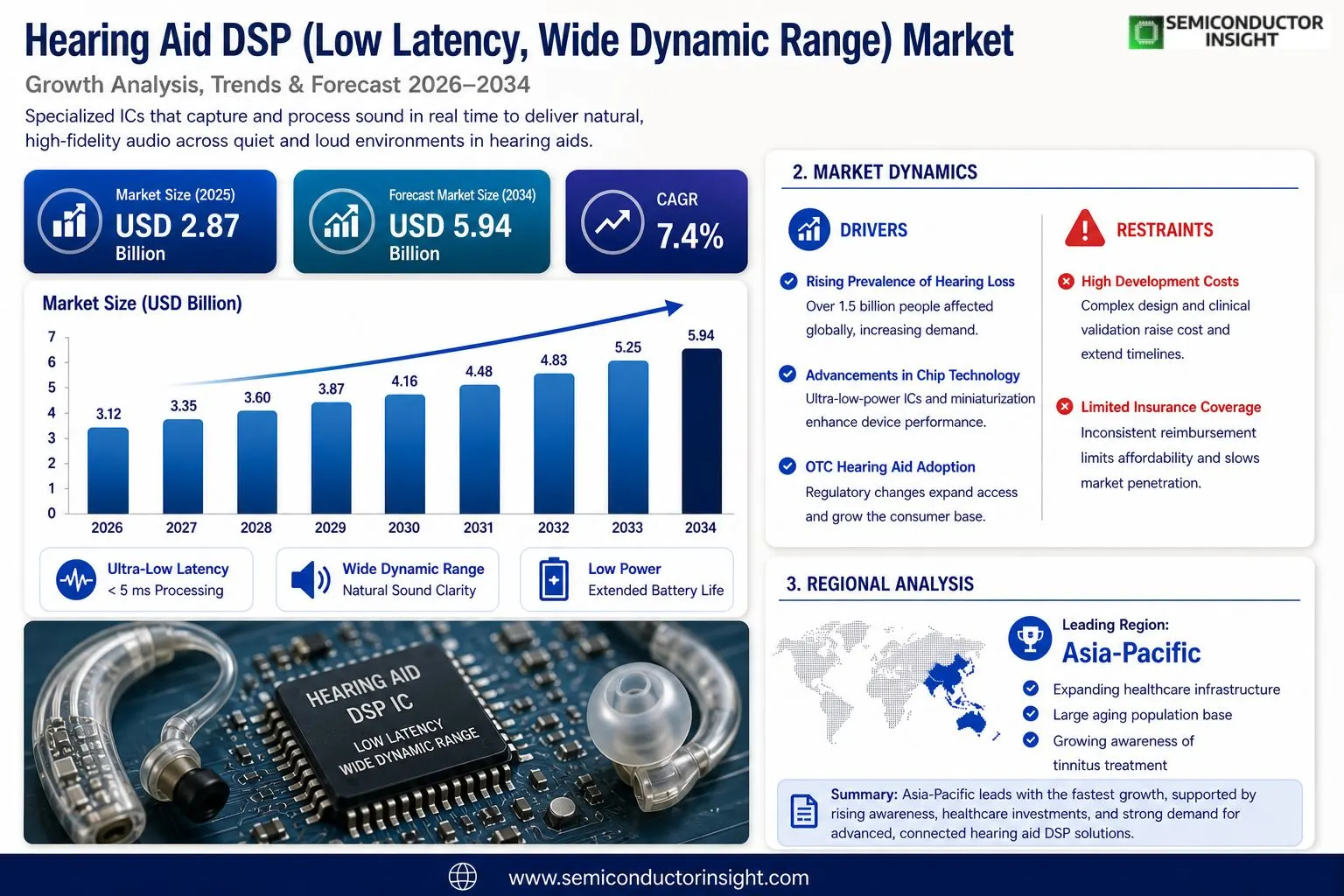

Global Hearing Aid DSP (Low Latency, Wide Dynamic Range) market size was valued at USD 2.87 billion in 2025. The market is projected to grow from USD 3.12 billion in 2026 to USD 5.94 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period.

Hearing aid digital signal processors (DSPs) with low latency and wide dynamic range are specialized semiconductor chips designed to capture, process, and amplify sound in real time while faithfully reproducing both very quiet and very loud acoustic signals. These processors integrate advanced noise reduction algorithms, feedback cancellation, multi-channel compression, and directional microphone processing to deliver natural, high-fidelity sound. Key product categories encompass behind-the-ear (BTE), receiver-in-canal (RIC), in-the-ear (ITE), and completely-in-canal (CIC) hearing aid DSP platforms, each demanding distinct performance benchmarks in latency and dynamic range.

The market is experiencing robust growth driven by the rising global prevalence of hearing loss , the World Health Organization estimates that over 1.5 billion people currently live with some degree of hearing loss , combined with rapid advancements in ultra-low-power chip architectures and Bluetooth Low Energy (LE Audio) connectivity. Furthermore, the growing adoption of over-the-counter (OTC) hearing aids following regulatory changes in major markets such as the United States has significantly expanded the addressable consumer base. Key players operating in this space include Qualcomm Technologies, Inc., Sonova Holding AG, GN Audio A/S, Starkey Hearing Technologies, and Nordic Semiconductor, all maintaining competitive portfolios of high-performance, low-latency DSP solutions.

MARKET DRIVERS

Rising Global Prevalence of Hearing Loss Accelerating Demand for Advanced DSP Solutions

Global burden of hearing loss continues to expand at a concerning pace, with the World Health Organization estimating that over 1.5 billion people worldwide experience some degree of hearing impairment. This growing patient population is a fundamental driver propelling Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market, as individuals increasingly seek devices capable of delivering naturalistic sound processing. Modern hearing aid users demand seamless auditory experiences across diverse acoustic environments, from quiet conversations to loud social gatherings, making low latency digital signal processing a non-negotiable feature in contemporary hearing aid architectures.

Technological Advancements in Wide Dynamic Range Compression Driving Adoption

Continuous innovation in wide dynamic range compression (WDRC) algorithms has significantly enhanced the ability of hearing aids to manage complex sound environments. Manufacturers are investing heavily in proprietary DSP chipsets capable of processing audio signals with latency below 5 milliseconds, ensuring that users do not experience the disorienting audio-visual misalignment that plagued earlier-generation devices. The integration of machine learning techniques into hearing aid DSP platforms enables real-time environment classification, allowing devices to adaptively optimize compression ratios and frequency shaping without manual user intervention. This convergence of low latency processing and intelligent dynamic range management is reshaping clinical benchmarks across the industry.

➤ Industry data indicates that hearing aid users report significantly higher satisfaction rates when devices incorporate sub-5ms processing latency combined with multi-band wide dynamic range compression, underscoring the clinical and commercial imperative for continued DSP innovation in the hearing technology sector.

The aging demographic structure of developed economies in North America, Europe, and East Asia is creating a sustained, long-term demand trajectory for premium hearing aid solutions featuring advanced DSP capabilities. Simultaneously, increasing awareness campaigns by audiological associations and government health bodies are shortening diagnosis-to-treatment timelines, expanding the addressable market for low latency, wide dynamic range hearing aid DSP technologies. These converging demographic and awareness-driven forces are expected to sustain robust market momentum through the coming decade.

MARKET CHALLENGES

High Development Complexity and Power Consumption Constraints Limiting DSP Performance Scalability

One of the most persistent technical challenges confronting Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market is the inherent tension between computational performance and power efficiency. Achieving ultra-low latency signal processing alongside high-fidelity wide dynamic range compression demands substantial processing resources, yet hearing aid form factors impose severe constraints on battery capacity. Engineers must navigate the difficult trade-off of delivering clinically meaningful DSP performance within power envelopes typically measured in microwatts, a challenge that demands continuous advancement in semiconductor design and embedded algorithm optimization. The miniaturization requirements of receiver-in-canal and completely-in-canal device categories further compound these engineering constraints.

Other Challenges

Regulatory and Reimbursement Complexity

The hearing aid DSP market faces a heterogeneous regulatory landscape across key geographies, with varying approval pathways in the United States, European Union, and Asia-Pacific markets creating compliance burdens for manufacturers seeking global commercialization. Inconsistent reimbursement frameworks across national healthcare systems limit patient access to premium low latency, wide dynamic range devices, particularly in middle-income markets where out-of-pocket expenditure represents a significant adoption barrier.

Interoperability and Standardization Gaps

The absence of universal interoperability standards for hearing aid DSP platforms creates fragmented ecosystems that complicate connectivity with smartphones, assistive listening devices, and telehealth infrastructure. Proprietary chipset architectures adopted by leading manufacturers restrict third-party algorithm integration, limiting the pace of collaborative innovation. Addressing these standardization gaps remains a critical prerequisite for realizing the full market potential of next-generation low latency, wide dynamic range DSP solutions.

MARKET RESTRAINTS

Elevated Device Cost and Limited Insurance Coverage Constraining Market Penetration

The sophisticated semiconductor engineering underpinning low latency, wide dynamic range hearing aid DSP platforms contributes to premium retail pricing that remains prohibitive for a substantial segment of Global hearing-impaired population. In many markets, premium hearing aids incorporating advanced DSP chipsets retail at price points that are not fully offset by insurance or public health reimbursement, resulting in high rates of unmet clinical need. This economic restraint disproportionately affects elderly populations and individuals in lower-income demographics, limiting the effective addressable market despite strong underlying clinical demand for hearing aid DSP technologies.

Shortage of Trained Audiological Professionals Impeding Optimal Device Utilization

Global shortage of qualified audiologists and hearing care professionals presents a structural restraint on market growth within Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market. The precise calibration required to optimize wide dynamic range compression parameters and low latency processing pathways for individual audiological profiles demands specialized clinical expertise. In underserved regions, the limited availability of trained practitioners reduces fitting accuracy and post-fitting support quality, contributing to device abandonment rates that suppress long-term market expansion. Tele-audiology platforms are emerging as a partial mitigation strategy, though their adoption remains uneven across geographies.

Consumer Stigma and Low Hearing Aid Adoption Rates Among Eligible Patients

Despite significant advances in hearing aid DSP performance and device aesthetics, social stigma associated with hearing aid use continues to suppress adoption rates among individuals who would clinically benefit from intervention. Studies consistently indicate that a substantial proportion of individuals with diagnosed hearing loss delay seeking treatment for extended periods, reducing the effective conversion of the clinical population into active device users. This attitudinal restraint limits the commercial potential of even the most technically sophisticated low latency, wide dynamic range hearing aid platforms.

MARKET OPPORTUNITIES

Over-the-Counter Hearing Aid Regulations Opening New Market Access Channels

Regulatory reforms enabling over-the-counter (OTC) hearing aid sales in major markets, most notably the United States Food and Drug Administration’s OTC framework implemented in 2022, are creating substantial new commercial channels for Hearing Aid DSP (Low Latency, Wide Dynamic Range) technology developers. Consumer electronics companies and digital health startups are entering the hearing care space with OTC-positioned devices that leverage advanced DSP capabilities to deliver clinically meaningful performance at accessible price points. This democratization of hearing technology access is expected to significantly expand the installed base of low latency, wide dynamic range DSP-equipped devices, stimulating both hardware and software ecosystem growth.

Integration of Artificial Intelligence and Edge Computing Enhancing DSP Capabilities

The accelerating integration of artificial intelligence and edge computing architectures into hearing aid DSP platforms represents one of the most consequential near-term opportunities in the market. AI-driven sound scene analysis enables hearing aids to dynamically reconfigure wide dynamic range compression settings and beamforming parameters in real time, delivering personalized auditory experiences that static DSP configurations cannot achieve. Leading semiconductor developers are producing purpose-built neural processing units optimized for hearing aid applications, enabling on-device machine learning inference with minimal power overhead. These advances position low latency, wide dynamic range hearing aid DSP as a platform for continuous performance improvement through firmware updates, creating durable differentiation opportunities for technology-forward manufacturers.

Emerging Market Expansion and Tele-Audiology Growth Broadening Geographic Opportunity

Rapidly expanding middle-class populations in Asia-Pacific, Latin America, and the Middle East represent largely underpenetrated geographic opportunities for Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market. Improving healthcare infrastructure, rising disposable incomes, and growing awareness of hearing health are converging to accelerate adoption of advanced hearing care solutions in these regions. Concurrently, the maturation of tele-audiology platforms is enabling remote fitting and fine-tuning of DSP-equipped hearing aids, reducing the dependence on dense brick-and-mortar audiological clinic networks that has historically constrained market penetration in geographically dispersed populations. These dynamics collectively position emerging markets as a high-growth frontier for low latency, wide dynamic range hearing aid technology over the medium-to-long term.

Trends

Rising Prevalence of Hearing Loss Fueling Demand for Advanced DSP Solutions

Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market is witnessing significant momentum as Global burden of hearing loss continues to rise. The World Health Organization estimates that over 1.5 billion people worldwide currently live with some degree of hearing loss, creating sustained demand for high-performance digital signal processors capable of delivering real-time sound amplification with minimal latency. Hearing aid DSPs with low latency and wide dynamic range have become central to modern audiological solutions, as they enable faithful reproduction of both quiet and loud acoustic signals while integrating advanced noise reduction, feedback cancellation, and multi-channel compression capabilities. As consumer expectations for natural, high-fidelity sound experiences increase, manufacturers are under growing pressure to deliver processors that meet stringent performance benchmarks across all hearing aid form factors, including behind-the-ear (BTE), receiver-in-canal (RIC), in-the-ear (ITE), and completely-in-canal (CIC) platforms.

Other Trends

OTC Hearing Aid Regulation Expanding the Consumer Addressable Market

One of the most transformative trends shaping Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market is the regulatory shift toward over-the-counter (OTC) hearing aids in major markets, particularly the United States. This policy change has significantly broadened the addressable consumer base by removing prescription requirements for mild-to-moderate hearing loss solutions, thereby accelerating the integration of cost-effective yet high-performance DSP chipsets into consumer-grade devices. Semiconductor companies and hearing aid developers are now designing low-latency, wide dynamic range DSP platforms that can meet both clinical-grade and consumer-grade performance standards simultaneously.

Bluetooth LE Audio and Ultra-Low-Power Chip Architectures Driving Innovation

Advancements in Bluetooth Low Energy (LE Audio) connectivity are playing a pivotal role in reshaping Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market landscape. LE Audio protocols enable lower transmission latency and improved audio quality, directly complementing the performance goals of wide dynamic range DSP processors. Concurrently, breakthroughs in ultra-low-power chip architectures are allowing manufacturers to deliver more sophisticated signal processing capabilities without compromising battery life , a critical consideration for miniaturized hearing aid form factors. Key industry participants including Qualcomm Technologies, Sonova Holding AG, GN Audio A/S, Starkey Hearing Technologies, and Nordic Semiconductor are actively advancing their DSP portfolios to capitalize on these converging technological developments.

Competitive Landscape Intensifying Around High-Performance, Low-Latency DSP Platforms

The competitive dynamics within Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market are intensifying as leading semiconductor and hearing solutions companies invest heavily in differentiating their processing platforms through superior latency reduction, extended dynamic range, and enhanced directional microphone processing algorithms. The convergence of artificial intelligence-driven noise management and real-time acoustic environment classification is emerging as a key area of product differentiation, positioning high-performance DSP solutions at the forefront of next-generation hearing aid development.

COMPETITIVE LANDSCAPE

Key Industry Players

Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market , Competitive Intelligence & Strategic Positioning of Leading Semiconductor and Hearing Technology Companies

Global Hearing Aid DSP (Low Latency, Wide Dynamic Range) market is characterized by a concentrated yet increasingly competitive landscape, with a handful of technologically advanced semiconductor and integrated hearing solutions companies commanding significant market share. Qualcomm Technologies, Inc. stands out as a dominant force, leveraging its extensive expertise in ultra-low-power chip architectures and Bluetooth LE Audio connectivity to deliver high-performance DSP platforms optimized for next-generation hearing aids. Sonova Holding AG, operating through its Phonak and Unitron brands, maintains a strong vertical integration advantage by developing proprietary DSP chipsets alongside complete hearing aid systems, enabling tightly optimized latency and wide dynamic range performance across its BTE, RIC, and CIC product lines. GN Audio A/S, through its ReSound brand, continues to invest heavily in AI-driven sound processing algorithms and cloud-connected DSP ecosystems, reinforcing its competitive position in premium hearing aid segments. These leading players collectively drive the majority of innovation in multi-channel compression, adaptive feedback cancellation, and directional microphone processing technologies that define the current state of the art in hearing aid DSP design.

Beyond the dominant players, a diverse group of specialized semiconductor firms and hearing technology innovators are actively shaping niche segments of the Hearing Aid DSP market. Nordic Semiconductor has established a compelling position through its low-power wireless SoC platforms that integrate seamlessly with hearing aid DSP architectures, particularly in OTC and consumer-grade hearing devices benefiting from recent U.S. regulatory liberalization. Starkey Hearing Technologies differentiates itself through proprietary Livio AI chipsets embedding on-device machine learning for real-time acoustic scene classification and noise suppression. Knowles Corporation, a specialist in miniature acoustic components and MEMS microphones, supplies critical sensing front-ends that interface directly with DSP platforms. Texas Instruments and Analog Devices contribute foundational mixed-signal and audio DSP IP widely adopted in hearing aid reference designs. Swiss-based Bernafon (a Demant subsidiary) and Widex , now merged with Sivantos under WS Audiology , also maintain proprietary DSP development programs targeting audiophile-grade sound fidelity. Emerging fabless semiconductor companies such as Indie Semiconductor and established Asian chipmakers including MediaTek are increasingly entering the low-cost OTC hearing DSP space, intensifying competitive pressure across price tiers and accelerating the overall market growth trajectory projected to reach USD 5.94 billion by 2034.

List of Key Hearing Aid DSP Companies Profiled

- Qualcomm Technologies, Inc.

- Sonova Holding AG

- GN Audio A/S (ReSound)

- Starkey Hearing Technologies

- Nordic Semiconductor

- Knowles Corporation

- Texas Instruments

- Analog Devices, Inc.

- WS Audiology (Widex | Sivantos)

- Bernafon (William Demant / Demant A/S)

- Oticon A/S (Demant Group)

- Indie Semiconductor

- MediaTek Inc.

- Cochlear Limited

- Audina Hearing Instruments

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Receiver-in-Canal (RIC) DSP stands as the leading segment within the type category, driven by its superior ability to balance discreet form factor demands with high-fidelity signal processing requirements.

|

| By Application |

|

Prescription Hearing Aids remain the dominant application segment, as clinically fitted devices continue to require the most sophisticated DSP capabilities available in the market.

|

| By End User |

|

Geriatric Population constitutes the largest end-user segment, reflecting the well-established correlation between advancing age and progressive sensorineural hearing deterioration.

|

| By Connectivity Technology |

|

Bluetooth Low Energy (LE Audio) Enabled DSP is the fastest-advancing connectivity segment, reshaping the competitive landscape for hearing aid chip developers.

|

| By Processing Architecture |

|

AI-Integrated DSP is rapidly emerging as the most strategically significant processing architecture segment, as machine learning capabilities become embedded directly into hearing aid chipsets.

|

Regional Analysis: Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market

North America

The FDA’s landmark authorization of over-the-counter hearing aids has reshaped the competitive landscape in North America, enabling DSP manufacturers to reach a significantly broader consumer base without traditional audiologist gatekeeping. This deregulatory shift has fostered a wave of direct-to-consumer product launches that prominently feature low latency and wide dynamic range capabilities, making advanced hearing technology more accessible and competitively priced across the United States and Canada.

North America’s dense network of semiconductor firms, AI startups, and established hearing health companies creates a fertile environment for continuous DSP advancement. Research into ultra-low latency processing and adaptive wide dynamic range compression is actively pursued at both corporate R&D centers and university laboratories, ensuring that the region maintains a technological edge in developing next-generation hearing aid chipsets optimized for real-world complex acoustic environments.

Demographic aging represents one of the most powerful structural demand drivers for the Hearing Aid DSP market in North America. With a substantial and growing segment of the population experiencing age-related hearing loss, the urgency for effective, comfortable, and technologically sophisticated hearing solutions continues to intensify. This demographic reality compels manufacturers to prioritize DSP features that deliver natural sound quality, seamless background noise suppression, and minimal processing delay for daily usability.

Progressive insurance coverage expansions and veterans’ healthcare benefits in the United States have significantly reduced the financial barriers associated with premium hearing aids featuring advanced DSP architectures. These reimbursement developments encourage audiologists and healthcare providers to recommend high-performance, wide dynamic range devices, positioning sophisticated DSP-equipped hearing aids as clinically preferred solutions rather than discretionary consumer electronics across the North American healthcare continuum.

Europe

Europe represents the second most significant regional market for Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market, characterized by a well-established universal healthcare tradition that systematically supports hearing aid procurement and audiology services. Countries such as Germany, Denmark, the United Kingdom, and the Netherlands are particularly prominent, with Denmark notably home to several globally influential hearing technology manufacturers that have pioneered DSP miniaturization and energy-efficient wide dynamic range processing. The European market benefits from stringent quality standards enforced through the EU Medical Device Regulation framework, which encourages manufacturers to invest in clinically validated low latency DSP solutions. An aging European population, especially concentrated in Western and Northern Europe, creates sustained demand for hearing aids that offer natural, low-distortion sound reproduction. Additionally, growing awareness campaigns by national health agencies about untreated hearing loss continue to expand the addressable market across the continent, positioning Europe as a consistent growth contributor through the forecast horizon of 2026 to 2034.

Asia-Pacific

The Asia-Pacific region is emerging as the fastest-growing market for Hearing Aid DSP (Low Latency, Wide Dynamic Range) solutions, propelled by rapidly expanding healthcare infrastructure, rising disposable incomes, and growing public health awareness about hearing impairment. China, Japan, South Korea, and Australia are the primary contributors to regional market expansion, with Japan standing out due to its exceptionally large elderly population and strong domestic demand for premium audiology products. China presents a particularly compelling growth narrative as government-led healthcare reforms and urban expansion drive increasing audiological care uptake. The presence of a growing local manufacturing ecosystem for hearing aid components, including DSP chipsets, is gradually reducing dependence on Western imports. South Korea’s advanced electronics manufacturing culture also contributes to regional innovation in compact, high-performance DSP solutions, making Asia-Pacific a region to watch closely as Global Hearing Aid DSP market continues its evolution through 2034.

South America

South America occupies a developing but progressively important position within Global Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market. Brazil, as the region’s largest economy, anchors much of the market activity, with a growing network of audiological clinics and increasing governmental focus on public health access to hearing care services. Argentina and Colombia also contribute to regional market development, though economic volatility in several South American nations periodically constrains consumer spending on premium hearing devices. Despite these challenges, the fundamentally underserved nature of hearing healthcare across the continent presents a considerable long-term opportunity for DSP-equipped hearing aid manufacturers willing to adapt pricing strategies for emerging market realities. Awareness initiatives led by non-governmental organizations and international health bodies are gradually reducing the stigma associated with hearing aid use, creating a more receptive environment for advanced low latency and wide dynamic range hearing solutions in the years ahead.

Middle East & Africa

The Middle East and Africa region currently represents the nascent stage of Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market, yet it carries notable long-term growth potential as healthcare investment accelerates across both sub-regions. In the Middle East, Gulf Cooperation Council nations such as the United Arab Emirates and Saudi Arabia are investing substantially in healthcare modernization, creating demand for sophisticated medical devices including advanced DSP-based hearing aids among their increasingly health-conscious urban populations. South Africa serves as the primary market anchor within the African continent, supported by a relatively more developed private healthcare sector. Across much of Africa, however, access to audiology services and hearing aid technology remains limited due to infrastructural and economic constraints. Nonetheless, expanding mobile health platforms and NGO-driven hearing screening programs are beginning to lay foundational awareness that could support broader market penetration of Hearing Aid DSP technologies across the Middle East and Africa through the 2026 to 2034 forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market?

-> Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market was valued at USD 2.87 billion in 2025 and is expected to reach USD 5.94 billion by 2034, growing at a CAGR of 7.4% during the forecast period from 2026 to 2034.

Which key companies operate in Hearing Aid DSP (Low Latency, Wide Dynamic Range) Market?

-> Key players include Qualcomm Technologies, Inc., Sonova Holding AG, GN Audio A/S, Starkey Hearing Technologies, and Nordic Semiconductor, among others, all maintaining competitive portfolios of high-performance, low-latency DSP solutions.

What are the key growth drivers?

-> Key growth drivers include the rising global prevalence of hearing loss (with over 1.5 billion people affected worldwide according to the World Health Organization), rapid advancements in ultra-low-power chip architectures, Bluetooth Low Energy (LE Audio) connectivity, and the growing adoption of over-the-counter (OTC) hearing aids following regulatory changes in major markets such as the United States.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by expanding healthcare infrastructure and a large aging population, while North America remains a dominant market supported by regulatory advancements enabling OTC hearing aid adoption and the presence of leading DSP technology providers.

What are the emerging trends?

-> Emerging trends include ultra-low-power DSP chip architectures, Bluetooth Low Energy (LE Audio) integration, advanced noise reduction and feedback cancellation algorithms, and the expansion of over-the-counter (OTC) hearing aid platforms across behind-the-ear (BTE), receiver-in-canal (RIC), in-the-ear (ITE), and completely-in-canal (CIC) form factors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...