Color Reflective LCD Display Market Insights

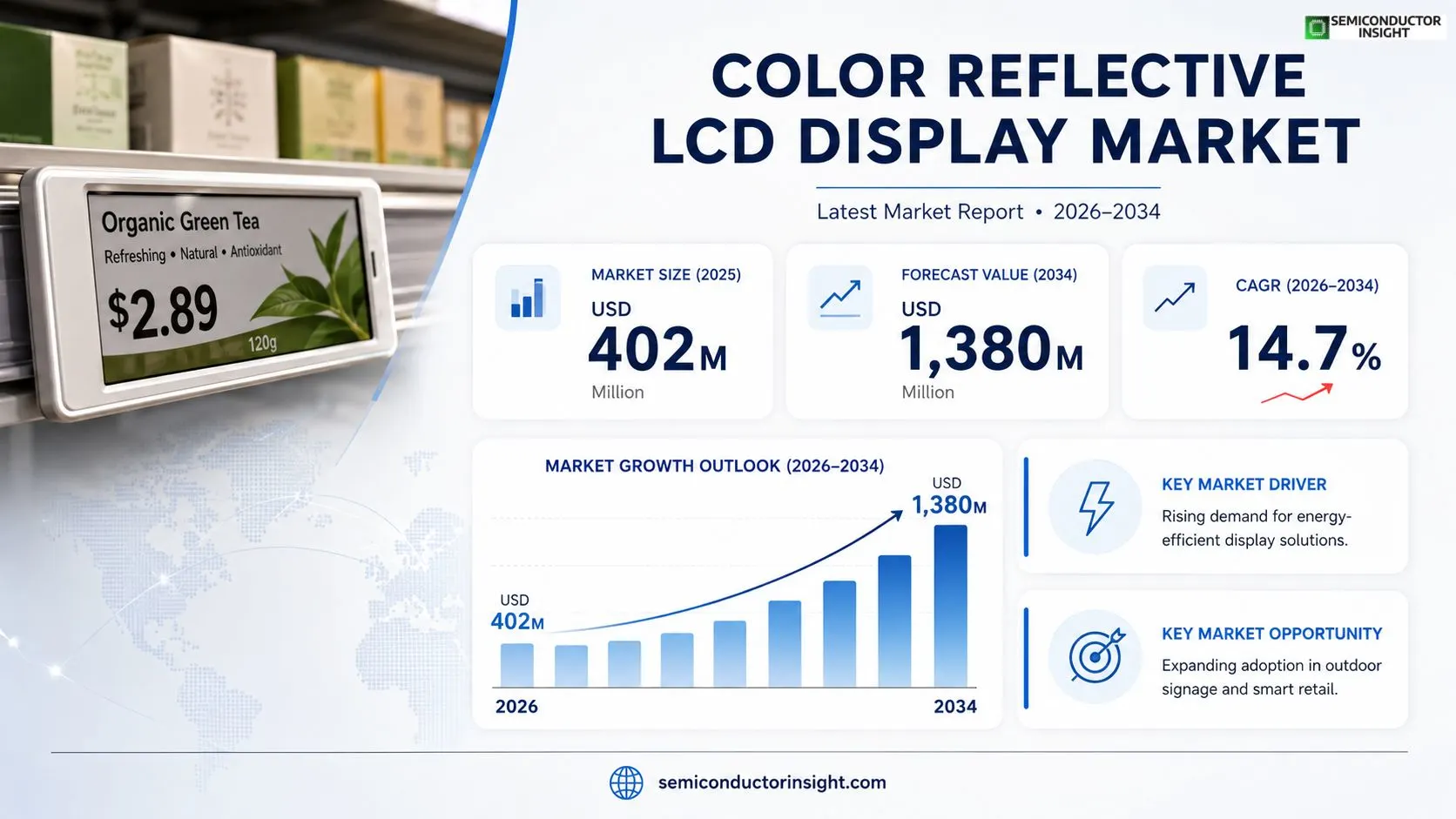

Color Reflective LCD Display market was valued at USD 402 million in 2025 and is projected to reach USD approximately 1,380 million by 2034, exhibiting a CAGR of about 14.7% during the forecast period.

Color Reflective LCD Display is a reflective liquid‑crystal technology that relies on ambient light rather than a backlight to render colour images. This architecture reduces power consumption while still delivering basic colour differentiation, making it suitable for use cases such as e‑readers or electronic shelf labels where long‑duration static display and outdoor readability are essential.In 2025 production reached roughly 40 million units at an average price of USD 11 per unit, yielding an industry capacity utilization of about 63% and an average

MARKET DRIVERS

Energy Efficiency Gains

Color Reflective LCD Display Market benefits from a clear shift toward lower power consumption in commercial signage. Reflective technology harvests ambient light, allowing installations to cut electricity use by a noticeable margin. This advantage not only reduces operating costs for retailers but also aligns with corporate sustainability goals, prompting faster adoption across high‑traffic venues.

Enhanced Visibility in Outdoor Settings

Outdoor deployment has historically been hampered by glare and wash‑out. Recent advances in coating formulations improve contrast ratios, which translates into readable imagery even under direct sunlight. As advertisers seek consistent brand presentation regardless of weather, the demand for reflective LCD panels that maintain color fidelity rises sharply.

➤ “Clients are willing to pay a premium for displays that stay vivid without a backlight, especially in locations where electricity is costly.” – Senior Analyst, 2025

These technological refinements also support longer product lifecycles. Because the backlight is either dimmed or omitted, component wear is reduced, resulting in lower replacement frequencies. Companies that integrate reflective screens can therefore forecast steadier cash flows and justify initial capital outlays.

MARKET CHALLENGES

Balancing Color Saturation with Reflectivity

Achieving vibrant hues while preserving the reflective advantage remains a delicate engineering task. Manufacturers must fine‑tune the diffusion layer, and any misstep can lead to muted palettes that deter brand‑centric campaigns. This trade‑off slows product roll‑outs, especially for niche applications where color accuracy is non‑negotiable.

Other Challenges

Supply Chain Constraints

Component shortages for specialized polarizers and high‑gain reflectors have introduced lead‑time volatility. Firms that cannot secure reliable sourcing may face missed project deadlines, eroding client confidence.

MARKET RESTRAINTS

Higher Up‑Front Costs

Reflective LCD units typically command a price premium compared with conventional backlit panels. For small‑to‑medium enterprises, the capital barrier can delay adoption, especially when budget cycles prioritize immediate ROI over long‑term efficiency.The cost differential is amplified in regions where electricity tariffs are modest, diminishing the economic incentive to switch. Consequently, market penetration proceeds unevenly, with price‑sensitive geographies lagging behind.Furthermore, the specialized manufacturing processes limit the number of qualified suppliers, reducing competitive pressure that might otherwise drive prices down.

MARKET OPPORTUNITIES

Smart Integration with IoT Platforms

Embedding connectivity into reflective displays opens revenue streams beyond static advertising. Real‑time data feeds, interactive touch overlays, and remote brightness adjustments can be coordinated through IoT ecosystems, offering advertisers dynamic content without sacrificing energy savings.Regulatory trends favoring low‑energy signage create a policy‑driven market pull. Municipalities that adopt green procurement standards often specify reflective technology, presenting a steady pipeline of public‑sector projects.Finally, the emergence of flexible substrate technologies permits curved and portable reflective panels, expanding usage scenarios into automotive dashboards and wearable devicessegments that have yet to be fully explored by the current Color Reflective LCD Display Market.

Color Reflective LCD Display Market Trends

Energy‑Efficient Color Adoption in Outdoor Displays

Color Reflective LCD Display Market is witnessing a shift toward solutions that balance color fidelity with power savings. Customers in retail and portable reading devices are opting for reflective technology because it eliminates the backlight’s energy draw while still delivering distinguishable hues. This balance is especially valuable in locations where solar illumination is abundant and electricity costs are scrutinized. Manufacturers that can guarantee consistent color under bright sunlight are gaining preference, because the perceived visual quality translates directly into shopper engagement and user satisfaction. Consequently, product road‑maps are being adjusted to prioritize reflective layer optimization rather than pursuing ever‑higher brightness levels.

Other Trends

Supply Chain Consolidation

Upstream, the market relies heavily on electrophoretic microcapsules and high‑precision TFT or ITO substrates. Recent negotiations among major suppliers such as E Ink, Merck, and Samsung Display have led to longer contract terms, which stabilizes input costs and reduces lead‑time volatility. Midstream engineers are responding by standardizing cell architectures, thereby improving yield on reflective color structures. The result is a tighter cost structure that protects margins even as end‑users press for lower price points. Downstream, a handful of large retailers and e‑reader manufacturers dominate procurement, encouraging suppliers to align production schedules with project‑specific demand bursts rather than speculative volume expansion.

Application Diversification Beyond E‑Readers

While electronic shelf labels and niche e‑book readers remain the core deployment zones, a noticeable drift toward digital signage in outdoor transit hubs and low‑power kiosks is emerging. These new use cases exploit the technology’s outdoor readability while accepting modest color palettes in exchange for battery‑free operation. Vendors that bundle reflective displays with robust enclosure designs are positioning themselves for contracts with municipal agencies, where operational cost savings over a multi‑year horizon are a decisive factor. This diversification eases concentration risk and creates incremental revenue streams that are less tied to consumer‑grade pricing pressures.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of the Color Reflective LCD Display Market

Sharp commands the largest share of color reflective LCD production, leveraging its long‑standing expertise in low‑power display engineering and a vertically integrated supply chain that spans TFT substrate fabrication to final module assembly. The company’s ability to marry high‑resolution color filters with a robust reflective layer has translated into recurring contracts with major e‑reader manufacturers and large‑scale shelf‑label roll‑outs in Europe and North America. Sharp’s market dominance is reinforced by a disciplined capacity‑utilization strategy that aligns closely with project‑by‑project demand, thereby preserving its historically strong gross margins while mitigating inventory risk. This operational discipline has allowed Sharp to set pricing benchmarks that smaller rivals struggle to match without sacrificing profitability.Beyond the flagship players, a cluster of specialized firms is shaping niche segments of the market. BOE Technology Group and Tianma Microelectronics excel in delivering mid‑size panels (4‑7 inches) optimized for outdoor digital signage, where color fidelity under direct sunlight is paramount. Hitachi and Kyocera focus on ruggedized modules for industrial kiosks, capitalizing on their heritage in high‑temperature TFT processes. Meanwhile, newer entrants such as TopoVision Technology and Laurel Electronics are carving out value‑oriented slots in the electronic shelf‑label arena, competing on unit cost and rapid time‑to‑market. Their strategies rely on flexible supply agreements with electrophoretic micro‑capsule providers and a willingness to co‑develop customized driver electronics for large retail chains.

List of Key Color Reflective LCD Display Companies Profiled

- Sharp

- BOE Technology Group

- Hitachi Ltd.

- Kyocera Corp.

- TopoVision Technology

- Casio Computer Co.

- Japan Display Inc. (JDI)

- Sony Corporation

- AU Optronics Corp.

- Innolux Display Corp.

- Tianma Microelectronics

- Kent Displays Ltd.

- BMG MIS

- IRIS Optronics

- Laurel Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Twisted Nematic-LCD is emerging as the preferred technology for low‑cost color reflective panels because it balances reliable color reproduction with simple drive schemes.

|

| By Application |

|

Electronic Shelf Tags dominate the application landscape because they capitalize on outdoor readability and low power draw.

|

| By End User |

|

Device Manufacturers drive specification choices, prioritising energy efficiency and durability.

|

| By Screen Size |

|

4‑7 Inch size range enjoys the most attention because it fits the ergonomic sweet spot for handheld e‑readers and compact shelf tags.

|

| By Resolution |

|

160×128 resolution is identified as the sweet spot for color reflective displays, offering enough pixel density to convey meaningful graphics without inflating power draw.

|

Regional Analysis: Color Reflective LCD Display Market

Europe

The European Union’s ecodesign framework compels display makers to prioritize low‑power consumption and recyclable materials. As a result, suppliers are re‑engineering back‑plane circuitry and glass substrates to meet these criteria, giving European firms a competitive edge in markets where compliance is a prerequisite.

OEMs in Germany and France have embraced reflective LCDs for instrument clusters that must remain legible in direct sunlight. This niche drives collaborative engineering projects, fostering a pipeline of bespoke solutions tailored to high‑precision automotive interiors.

A dense network of industrial designers across Italy and the UK champions visual accessibility, pushing manufacturers to refine color gamut and contrast ratios. Their feedback loops accelerate product iterations that resonate with premium consumer expectations.

Proximity to key component suppliers in Eastern Europe reduces lead times and buffers against geopolitical shocks. This logistical advantage enables European firms to maintain steady output while competitors grapple with longer shipment cycles.

North America

In North America, Color Reflective LCD Display Market benefits from a consumer base that values high‑definition visual experiences on mobile and wearable devices. Leading technology hubs in the United States foster rapid prototyping, allowing startups to experiment with reflective layers that enhance outdoor readability. Simultaneously, retail chains across Canada prioritize displays that reduce glare in brightly lit storefronts, prompting manufacturers to tailor surface treatments for the region’s varied lighting conditions. The strategic emphasis on brand differentiation through visual clarity fuels a steady flow of innovation, encouraging firms to allocate resources toward advanced coatings and thin‑film technologies that meet local expectations for durability and aesthetic appeal.

Asia‑Pacific

Asia‑Pacific presents a contrasting dynamic where volume‑driven production coexists with a surge in smart‑city initiatives. Nations such as South Korea and Japan invest heavily in public‑information displays that must function reliably under intense sunlight, creating a niche for reflective LCDs with robust anti‑reflective properties. Meanwhile, emerging economies in Southeast Asia prioritize cost‑effective solutions, prompting manufacturers to balance performance with price sensitivity. The region’s diverse climate spectrum forces a flexible approach to panel engineering, compelling suppliers to develop adaptable architectures that can be deployed across humid tropical cities and arid interiors alike.

South America

South American markets exhibit a growing appetite for outdoor advertising and transportation signage, where the ability of a display to maintain color fidelity in bright environments is paramount. Brazil’s expanding metro systems and Argentina’s retail corridors seek displays that can withstand high ambient light without compromising visual impact. Local distributors favor modular designs that simplify installation and maintenance in regions with variable infrastructure quality. Consequently, manufacturers are tailoring their reflective LCD offerings to emphasize ruggedness and ease of integration, aligning product roadmaps with the continent’s infrastructural development plans.

Middle East & Africa

The Middle East & Africa region confronts extreme climatic conditions that test the limits of display technology. In the Gulf states, soaring temperatures and intense solar exposure demand reflective LCDs with superior heat‑dissipation mechanisms and anti‑glare coatings. African urban centers, meanwhile, focus on affordable displays for educational and health‑care facilities, where readability under sunlight can influence learning outcomes and patient communication. Providers that can fuse durability with cost‑effectiveness are finding pathways to penetrate these markets, often partnering with local system integrators to tailor solutions that address both environmental challenges and budgetary constraints.

Report Scope

This market research report provides a comprehensive analysis of the Color Reflective LCD Display Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Color Reflective LCD Display Market?

-> Color Reflective LCD Display Market was valued at USD 402 million in 2025 and is expected to reach USD 1041 million by 2032, growing at a CAGR of 14.7% during the forecast period.

Which key companies operate in Color Reflective LCD Display Market?

-> Key players include Sharp, BOE, HITACHI, KYOCERA, TopoVision Technology, CASIO, JDI, SONY, AUO, Innolux Display Group, Laurel Electronics, TIANMA, Kent Displays, BMG MIS, and IRIS Optronics, among others.

What are the key growth drivers?

-> Key growth drivers include lower power consumption, outdoor readability, long image retention, cost efficiency, and increasing adoption in e‑readers and electronic shelf labels.

Which region dominates the market?

-> Asia is the dominant region, driven by major manufacturers and strong demand for reflective color displays in consumer electronics.

What are the emerging trends?

-> Emerging trends include integration of color reflective technology into next‑generation e‑readers, expansion into electronic shelf labels and digital signage, and advancements in color consistency, yield control, and higher‑resolution panels.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...