Cockpit Domain Controller (CDC) SoC Market Insights

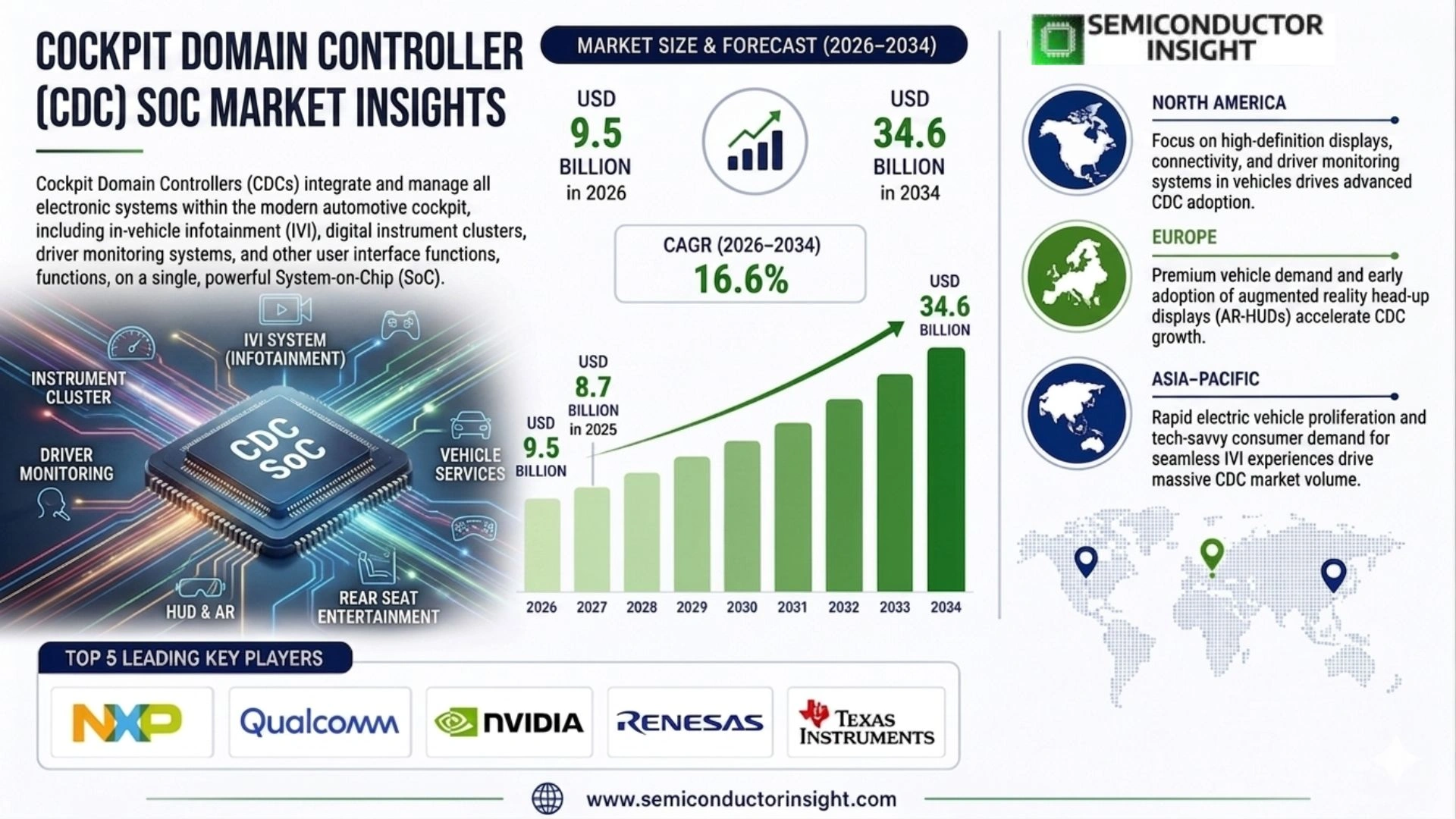

Cockpit Domain Controller (CDC) SoC Market size was valued at USD 8.7 billion in 2025. The market is projected to grow from USD 9.5 billion in 2026 to USD 34.6 billion by 2034, exhibiting a CAGR of 16.6% during the forecast period.

Cockpit Domain Controller (CDC) SoCs are high-performance integrated circuits designed to centralize and manage multiple cockpit functions within a single computing platform. These advanced chips power the consolidation of digital instrument clusters, infotainment systems, advanced driver assistance system visualizations, head-up displays, and connectivity features. By replacing numerous discrete electronic control units with a unified architecture, CDC SoCs enable seamless multi-display interactions, real-time data processing, and enhanced human-machine interfaces in modern vehicles.

The market is experiencing rapid growth due to several factors, including the accelerating shift toward software-defined vehicles, rising consumer demand for immersive digital cockpit experiences, and increasing integration of artificial intelligence capabilities. Furthermore, the proliferation of electric vehicles and stricter safety regulations are driving automakers to adopt centralized computing solutions that support over-the-air updates and advanced personalization. Additionally, advancements in semiconductor technology, such as higher AI computing power and efficient multi-core architectures, are contributing to market expansion. Initiatives by key players in the market are also expected to fuel the market growth. For instance, leading semiconductor companies continue to launch next-generation platforms featuring elevated TOPS ratings for AI workloads. Qualcomm Technologies, NVIDIA Corporation, and NXP Semiconductors are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Rising Demand for Software-Defined Vehicles and Digital Cockpit Experiences

Cockpit Domain Controller (CDC) SoC Market is experiencing robust growth driven by the automotive industry’s shift toward software-defined vehicles (SDVs). CDC SoCs consolidate multiple functions including infotainment, digital instrument clusters, driver monitoring, and advanced HMI into a centralized high-performance computing platform. This consolidation reduces wiring complexity, lowers overall vehicle weight, and enables seamless over-the-air (OTA) updates, which are increasingly demanded by consumers and OEMs alike.

Advancements in AI Integration and Electrification

Proliferation of electric vehicles and integration of AI-powered features such as voice assistants, personalized user experiences, and real-time ADAS visualization are accelerating adoption of powerful CDC SoCs. Leading semiconductor providers are delivering automotive-grade SoCs with multi-core architectures and high TOPS capabilities to support these demanding workloads. Market penetration of domain controller architectures in new passenger vehicle platforms has significantly increased in recent years.

➤ Consumer expectations for premium, immersive in-cabin digital experiences continue to push OEMs toward centralized CDC solutions that support multi-display setups and hyper-personalization.

The transition to zonal and centralized architectures further amplifies the need for scalable, high-performance CDC SoCs capable of handling mixed-criticality workloads efficiently while maintaining functional safety compliance.

MARKET CHALLENGES

High Development Costs and System Complexity

Developing and validating advanced Cockpit Domain Controller (CDC) SoC solutions involves substantial R&D investment due to the need for functional safety (ASIL) certification, cybersecurity robustness, and real-time performance across diverse operating conditions. OEMs and Tier-1 suppliers face challenges in balancing performance requirements with power consumption and thermal management in compact vehicle environments.

Other Challenges

Semiconductor Supply Chain Vulnerabilities

Reliance on a concentrated base of high-performance automotive SoC suppliers creates risks of supply disruptions, which can impact production timelines for next-generation vehicles featuring integrated digital cockpits.

Integration with Legacy Systems and Software Fragmentation

Ensuring compatibility between new CDC platforms and existing vehicle architectures while managing multiple software ecosystems and operating systems adds layers of engineering complexity and validation overhead.

MARKET RESTRAINTS

High Cost of Azvanced Electronics Limiting Mass-Market Adoption

The elevated costs associated with high-performance CDC SoCs, supporting memory, connectivity modules, and associated software stacks continue to restrain widespread adoption, particularly in cost-sensitive vehicle segments. While premium and EV models readily integrate these technologies, broader penetration in entry-level and mid-range vehicles remains gradual due to bill-of-materials pressures.

Regulatory and Cybersecurity Compliance Burdens

Stringent functional safety standards, evolving cybersecurity regulations, and regional data privacy requirements add significant compliance costs and extend development cycles for CDC SoC platforms. Ensuring long-term upgradability and security throughout the vehicle lifecycle presents ongoing technical and financial challenges for market participants.

MARKET OPPORTUNITIES

Transition to Zonal Architectures and Cockpit-Driving Integration

Significant opportunities exist in the evolution from traditional domain controllers toward zonal computing architectures and integrated cockpit-driving-parking solutions. Next-generation CDC SoCs that support these consolidated platforms can deliver substantial efficiency gains, enabling OEMs to reduce ECU count while enhancing overall system performance and scalability.

Expansion in Emerging Markets and AI-Enabled Features

Rapid growth in electric vehicle adoption in Asia-Pacific regions, coupled with increasing demand for AI-driven personalization and advanced driver monitoring, creates expansive opportunities for innovative CDC SoC providers. Partnerships between semiconductor firms and automotive suppliers are accelerating the deployment of cost-effective, high-compute solutions tailored for both premium and volume markets.

Trends

Centralized Computing Architecture in Modern Vehicles

Cockpit Domain Controller (CDC) SoC Market is witnessing significant momentum driven by the automotive industry’s transition toward centralized computing platforms. Cockpit Domain Controller (CDC) SoCs serve as high-performance integrated circuits that consolidate multiple cockpit functions into a single unified system. These solutions effectively manage digital instrument clusters, infotainment systems, advanced driver assistance system visualizations, head-up displays, and various connectivity features within vehicles.

Other Trends

Shift Toward Software-Defined Vehicles

Automakers are increasingly adopting software-defined vehicle architectures, where Cockpit Domain Controller (CDC) SoC solutions play a pivotal role in enabling flexible system updates and enhanced functionality. This centralization approach replaces multiple discrete electronic control units with a streamlined computing platform, facilitating seamless multi-display interactions, real-time data processing, and superior human-machine interfaces across diverse vehicle models.

Integration of Artificial Intelligence Capabilities

Advancements in semiconductor technology are propelling Cockpit Domain Controller (CDC) SoC Market forward, particularly through higher AI computing power and efficient multi-core architectures. Leading semiconductor companies continue to develop next-generation platforms optimized for demanding AI workloads, supporting sophisticated features such as real-time personalization and advanced safety visualizations in the vehicle cockpit.

Growth Drivers in Electric Vehicles and Safety Regulations

The proliferation of electric vehicles combined with stricter safety regulations is accelerating the adoption of Cockpit Domain Controller (CDC) SoC technologies. These solutions enable over-the-air updates and advanced personalization options that align with evolving consumer expectations for immersive digital cockpit experiences. Key industry participants including Qualcomm Technologies, NVIDIA Corporation, and NXP Semiconductors maintain robust portfolios that address these emerging requirements through continuous innovation in cockpit domain computing solutions. As vehicle architectures become more integrated, Cockpit Domain Controller (CDC) SoC Market continues to evolve with emphasis on performance optimization and system-level efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Cockpit Domain Controller (CDC) SoC Market Competitive Analysis

Cockpit Domain Controller (CDC) SoC Market is led by a select group of semiconductor giants and Tier-1 automotive suppliers who dominate through advanced high-performance computing platforms. Qualcomm Technologies stands out as a frontrunner with its Snapdragon Cockpit series, offering exceptional AI capabilities and multi-display support that enable software-defined vehicle architectures. The market exhibits moderate consolidation, with leading players leveraging scalable SoC designs, real-time processing, and seamless integration of infotainment, instrument clusters, and ADAS visualizations to capture significant share amid the transition to centralized vehicle computing.

Other significant players include established automotive electronics firms and specialized SoC providers carving niches in regional markets and next-generation solutions. Companies such as NVIDIA, NXP Semiconductors, and emerging Chinese suppliers like Desay SV bring differentiated strengths in AI acceleration, functional safety, and cost-optimized platforms tailored for electric vehicles and premium applications. This dynamic ecosystem fosters innovation in multi-core architectures and OTA-capable systems while intensifying competition around performance-per-watt metrics and ecosystem partnerships with automakers.

List of Key Cockpit Domain Controller (CDC) SoC Companies Profiled

- Qualcomm Technologies, Inc.

- NVIDIA Corporation

- Continental AG

- Robert Bosch GmbH

- Visteon Corporation

- Aptiv PLC

- NXP Semiconductors

- Harman International (Samsung)

- Denso Corporation

- Desay SV Automotive

- Infineon Technologies AG

- Marelli

- Panasonic Corporation

- ECARX

- Renesas Electronics Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI-Accelerated SoCs represent the leading segment due to their ability to handle complex real-time AI workloads for intelligent human-machine interfaces. These solutions excel in processing sensor fusion data and delivering personalized user experiences. Their advanced architecture supports seamless over-the-air updates, enabling continuous feature enhancements without hardware changes. Manufacturers prioritize these chips for next-generation vehicles requiring robust computational capabilities for voice recognition, gesture control, and predictive analytics. |

| By Application |

|

Infotainment System emerges as the dominant application segment as consumers increasingly demand immersive, connected in-cabin experiences. These SoCs facilitate smooth integration of navigation, multimedia streaming, and smartphone connectivity while maintaining high graphical fidelity across multiple displays. The centralized processing power allows for dynamic content sharing between driver and passenger screens, creating cohesive digital environments. Enhanced security features within these controllers protect against cyber threats while supporting extensive app ecosystems and real-time traffic updates. |

| By End User |

|

Passenger Vehicles lead this segment through widespread adoption of advanced digital cockpits in mainstream models. These controllers enable automakers to differentiate their offerings with unified interfaces that enhance driver comfort and safety awareness. The technology supports extensive personalization options tailored to individual preferences, fostering greater user engagement. Integration with vehicle ecosystems allows for predictive maintenance alerts and seamless connectivity features that improve overall ownership satisfaction. |

| By Vehicle Type |

|

Electric Vehicles stand out as the leading category in this segmentation. CDC SoCs play a vital role in optimizing energy management displays and providing intuitive range information alongside entertainment features. Their efficient architecture aligns perfectly with the software-defined nature of modern EVs, supporting sophisticated battery monitoring visualizations and autonomous driving aids. These controllers facilitate the creation of calming, information-rich interfaces that reduce driver cognitive load while maximizing the unique capabilities of electric powertrains. |

| By Architecture |

|

Centralized Computing architecture leads due to its superior efficiency in resource allocation and simplified system design. This approach minimizes latency between cockpit functions while reducing overall wiring complexity and weight. It enables powerful cross-domain data fusion essential for advanced safety features and contextual awareness. The unified platform architecture also streamlines development cycles for automakers, allowing faster deployment of new software features across entire vehicle fleets through centralized processing capabilities. |

Regional Analysis: Cockpit Domain Controller (CDC) SoC Market

Asia-Pacific

Asia-Pacific benefits from dense clusters of automotive and semiconductor talent that drive breakthroughs in Cockpit Domain Controller (CDC) SoC integration. Collaborative R&D centers focus on optimizing multi-core architectures for superior graphics rendering and sensor fusion, enabling smoother transitions between driving modes and entertainment systems while maintaining strict automotive-grade reliability.

The region’s vertically integrated supply chains allow for faster iteration of CDC SoC designs with reduced lead times. Proximity of foundries, packaging specialists, and display manufacturers supports cost-effective production of high-performance domain controllers tailored for diverse vehicle segments prevalent in Asian markets.

With strong momentum in electric vehicle platforms, Asia-Pacific manufacturers prioritize CDC SoCs that efficiently manage power distribution alongside rich cockpit functionalities. This synergy creates opportunities for domain controllers that enhance range optimization through intelligent HMI systems and predictive user interfaces.

Leading players in the region pursue both domestic scaling and global exports of CDC SoC technologies. Strategic alliances with international OEMs facilitate technology transfer while adapting solutions to meet varying regulatory requirements across different geographies.

North America

North America demonstrates robust growth Cockpit Domain Controller (CDC) SoC Market through its emphasis on premium vehicle segments and software-defined architectures. The United States leads with technology companies and automakers investing heavily in centralized computing platforms that power immersive digital cockpits. Focus areas include seamless integration of cloud services, voice assistants, and advanced driver monitoring within compact SoC designs. Canadian and Mexican manufacturing hubs contribute through specialized component production, supporting the regional push toward highly customizable cockpit experiences that prioritize passenger comfort and safety features. The market here benefits from a mature ecosystem of software developers who enhance the functional capabilities of CDC SoCs beyond traditional hardware boundaries.

Europe

Europe maintains a strong position Cockpit Domain Controller (CDC) SoC Market by prioritizing sustainability, safety compliance, and luxury vehicle innovations. German automakers and their suppliers excel in developing domain controllers that meet stringent functional safety requirements while delivering sophisticated human-machine interfaces. The region emphasizes energy-efficient SoC solutions suitable for both traditional and electric powertrains, integrating advanced cybersecurity measures to protect connected cockpit systems. Collaborative projects across EU nations accelerate standardization efforts, enabling smoother adoption of next-generation CDC technologies. Premium brands drive demand for high-end graphics processing and multi-display synchronization capabilities within these domain controllers.

South America

South America is gradually expanding its footprint Cockpit Domain Controller (CDC) SoC Market as local automotive assembly grows alongside rising consumer expectations for modern vehicle interiors. Brazil and Argentina serve as key markets where international OEMs introduce vehicles featuring entry-level to mid-range CDC SoC solutions. The focus remains on cost-effective implementations that improve basic connectivity and infotainment without compromising core reliability. Regional strategies involve technology partnerships to adapt global CDC designs for challenging operating environments and diverse user preferences. This approach supports steady market development through localized assembly and service networks that ensure long-term performance of cockpit domain systems.

Middle East & Africa

The Middle East and Africa region shows emerging potential Cockpit Domain Controller (CDC) SoC Market fueled by infrastructure modernization and luxury vehicle imports. Gulf countries invest in smart mobility initiatives that incorporate advanced cockpit technologies in premium and fleet vehicles. South Africa contributes through its established automotive manufacturing base, adapting CDC SoC solutions for regional climate conditions and connectivity challenges. Market dynamics center on technology leapfrogging, where newer vehicle models arrive equipped with integrated domain controllers offering enhanced navigation and entertainment features. Strategic distribution partnerships help bridge gaps in local technical expertise while preparing the ground for broader future adoption of sophisticated cockpit domain controller architectures.

Report Scope

This market research report provides a comprehensive analysis of the Cockpit Domain Controller (CDC) SoC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Cockpit Domain Controller (CDC) SoC Market?

-> Cockpit Domain Controller (CDC) SoC Market was valued at USD 8.7 billion in 2025 and is expected to reach USD 34.6 billion by 2034.

Which key companies operate Cockpit Domain Controller (CDC) SoC Market?

-> Key players include Qualcomm Technologies, NVIDIA Corporation, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include shift toward software-defined vehicles, rising consumer demand for immersive digital cockpit experiences, and increasing integration of artificial intelligence capabilities.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include AI-powered cockpit platforms, multi-display consolidation, and over-the-air update capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...