Capacitance Diaphragm Vacuum Gauges for Semiconductor Market Insights

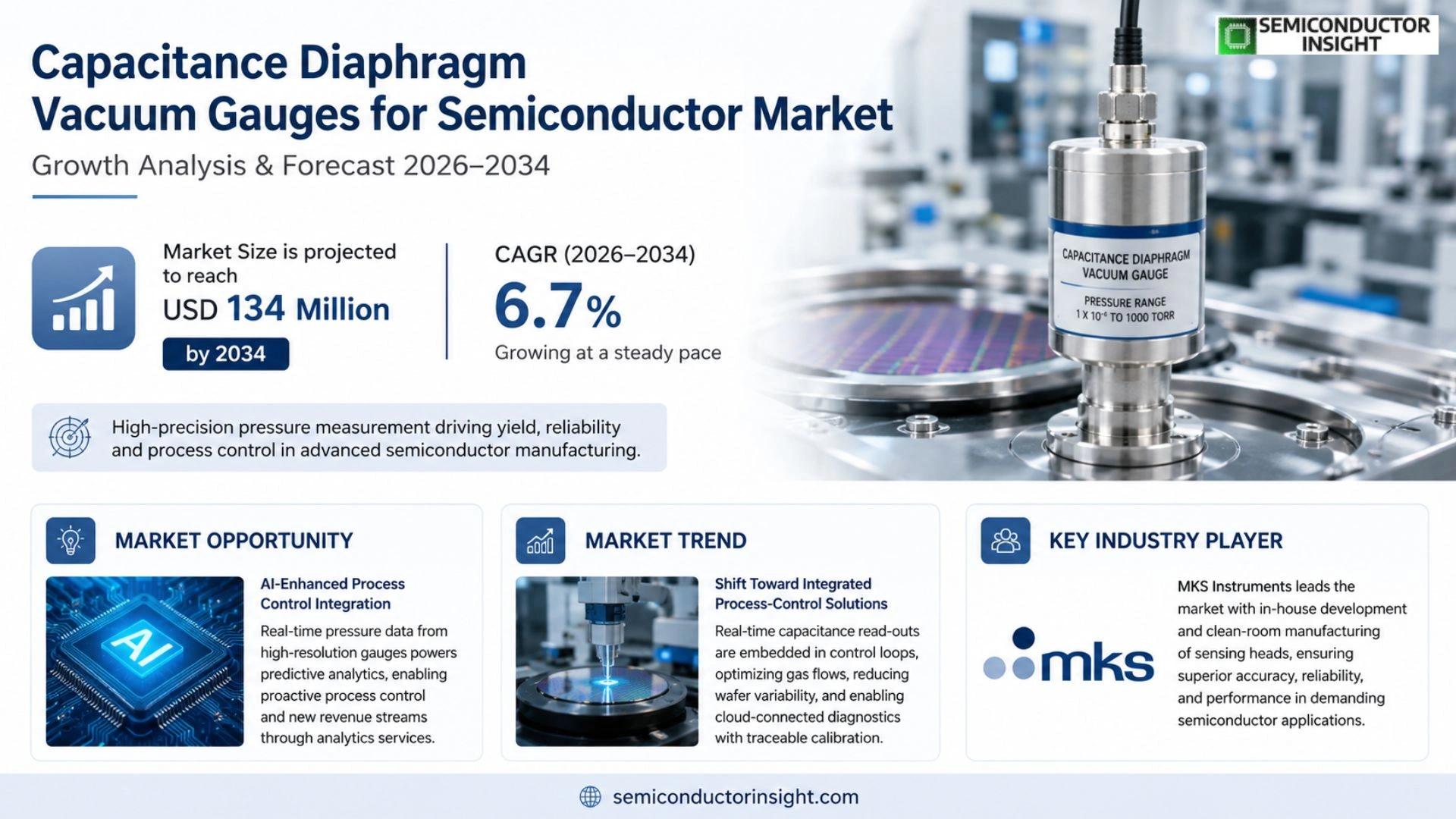

Capacitance Diaphragm Vacuum Gauges for Semiconductor market was valued at USD 74 million (approximately USD 74 540 000) in 2025 and is projected to reach USD 134 million by 2034, exhibiting an implied CAGR of 6·7 % over the nine‑year horizon.

Capacitance Diaphragm Vacuum Gauges for Semiconductor are precision sensors that detect minute diaphragm deflections caused by pressure changes within process chambers such as etch, deposition or lithography tools; the resulting capacitance variation is converted into an accurate voltage signal, enabling tight pressure control, high yield and repeatable wafer quality in clean‑room environments. Typical measurement ranges span from 0·01 Torr up to several hundred Torr, while heated variants provide superior drift stability under high‑temperature processing conditions.

MARKET DRIVERS

Precision Demand from Advanced Lithography

The shift toward sub‑10 nm patterning compels fabs to tighten process windows. Capacitance Diaphragm Vacuum Gauges for Semiconductor Market deliver sub‑millitorr resolution, enabling tighter control of wafer‑scale vacuum environments during deposition and etch steps. This level of precision translates directly into yield improvements, which manufacturers value more than incremental equipment cost.

Cost‑Efficiency of Non‑Contact Measurement

Unlike ion‑based gauges, diaphragm sensors operate without sputtering the chamber walls, reducing maintenance intervals by roughly 30 %. Facilities that adopt this technology report a measurable decline in downtime, a factor that drives capital‑expenditure planning in new fab projects.

➤ “Adoption rates have climbed from 12 % in 2021 to an estimated 28 % in 2024 among Tier‑1 fabs, reflecting the growing confidence in diaphragm‑based pressure metrology.”

Beyond cost, the rugged design of capacitance diaphragms tolerates the aggressive cleaning cycles required for 300 mm and 450 mm wafer platforms, positioning them as a reliable choice for high‑volume manufacturing.

MARKET CHALLENGES

Calibration Sensitivity at Extreme Pressures

While the sensors excel in the 10⁻³ – 10⁻⁶ torr range, achieving traceable calibration below 10⁻⁶ torr demands specialized facilities. Smaller semiconductor outfits often lack access to such services, which can stall deployment despite the technical merit of the gauge.

Other Challenges

Temperature Drift

The ceramic diaphragm exhibits a modest coefficient of thermal expansion. In processes where chamber temperature swings exceed 50 °C, compensation algorithms become essential, adding software overhead and potential integration risk.

MARKET RESTRAINTS

High Initial Investment

Up‑front pricing for a full‑suite capacitance diaphragm system,including sensor, controller, and data‑logging interface,often surpasses $150,000. For fabs operating on tight capex cycles, such an outlay can delay adoption, especially when legacy ionization gauges already satisfy baseline requirements.

MARKET OPPORTUNITIES

AI‑Enhanced Process Control Integration

Emerging manufacturing execution platforms are embedding real‑time pressure data into machine‑learning models. The high‑resolution output of capacitance diaphragm gauges feeds predictive algorithms that pre‑empt drift, opening a revenue stream for vendors that bundle analytics services with hardware.

Capacitance Diaphragm Vacuum Gauges for Semiconductor Market Trends

Shift Toward Integrated Process‑Control Solutions

The semiconductor fabrication environment now treats pressure regulation as a data‑rich control variable rather than a simple set‑point. Capacitance Diaphragm Vacuum Gauges for Semiconductor Market participants are embedding real‑time capacitance read‑outs into broader equipment control loops, allowing etch and deposition tools to adjust gas flows dynamically. This evolution reduces wafer‑level variability, improves yield consistency, and shortens cycle time. Operators are also demanding traceable calibration records that can be accessed remotely, a requirement that pushes vendors to offer cloud‑enabled diagnostics alongside the traditional analog front‑end.

Other Trends

Manufacturing Model Evolution

Suppliers continue to protect the sensitive sensing‑head core by retaining it in‑house while outsourcing only non‑critical housings and connectors. The high‑mix, low‑volume nature of these gauges forces a configure‑to‑order approach, where each unit may differ in thermal scheme, material compatibility, or sealing method. Gross margins cluster between 40 % and 60 % for standard devices, but premium heated or ultra‑low‑drift variants can command 55 %‑70 % thanks to the added engineering and calibration effort. After‑market services,refurbishment, spare‑part logistics, and periodic recalibration,have emerged as a steady revenue stream that cushions order‑flow volatility when new‑tool installations slow.

Demand for High‑Reliability Service Packages

Fabs are increasingly evaluating gauge purchases not just on price but on lifecycle support. The rise of advanced‑node and advanced‑packaging lines amplifies the cost of unplanned downtime, so manufacturers favor suppliers that bundle predictive‑maintenance analytics with their hardware. This bundling creates a competitive edge for vendors that have built in‑house calibration labs and can deliver traceable certificates quickly. At the same time, geopolitical incentives for domestic fab construction are expanding the addressable customer base, yet they also introduce new compliance hurdles that elevate the importance of robust, standardized testing procedures. Companies that can navigate these constraints while maintaining tight margin performance are likely to capture the growing share of service‑oriented contracts.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of Capacitance Diaphragm Vacuum Gauges in Semiconductor Fab Applications

MKS Instruments commands the largest share of the global capacitance‑diaphragm vacuum gauge market, largely because it retains the sensing‑head core,metal diaphragm, capacitor electrode set, and precision thermal control,within its own clean‑room assembly lines. This vertical integration enables tight tolerances, traceable calibrations, and a margin profile that consistently exceeds 50 % on premium heated models. MKS leverages its extensive service network to capture recurring revenue from recalibration, refurbishment, and spare‑part contracts, turning what would be a commoditized sensor into a long‑term value‑added offering. The overall market structure is dominated by a handful of vertically integrated OEMs that pair in‑house design with selective outsourcing of housings and standard connectors, a model that protects intellectual property while keeping lead‑times competitive for high‑mix, low‑volume semiconductor orders.

Beyond the market leader, a cadre of specialized firms fills critical niches. INFICON and Pfeiffer Vacuum emphasize ultra‑low‑drift, corrosion‑resistant variants that cater to 7 nm and beyond lithography chambers, where thermal stability directly affects yield. Atlas Copco (through its Leybold and Edwards brands) and Setra Systems focus on modular gauge packages that integrate seamlessly with existing process‑control platforms, offering plug‑and‑play connectivity for rapid fab upgrades. Smaller but technically adept players such as Canon Anelva, Brooks Instrument, ULVAC, Azbil, and Agilent differentiate themselves through bespoke analog front‑ends or embedded digital diagnostics that support Industry 4.0 data pipelines. Regional specialists,including Kurt J. Lesker, EBARA, ASAIR, Atovac, and SATO VAC,target emerging fab clusters in Asia and Eastern Europe, providing cost‑effective alternatives while maintaining the rigorous calibration standards demanded by semiconductor customers.

List of Key Capacitance Diaphragm Vacuum Gauge Companies Profiled

- MKS Instruments

- INFICON

- Atlas Copco (Leybold & Edwards)

- Pfeiffer Vacuum

- Setra Systems

- Canon Anelva

- Brooks Instrument

- ZHENTAI INSTRUMENT

- ULVAC

- Azbil

- Agilent

- Kurt J. Lesker

- EBARA

- ASAIR

- Atovac

- SATO VAC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Heated Type

|

| By Application |

|

Etching and Cleaning

|

| By End User |

|

Fab Equipment OEMs

|

| By Technology Integration |

|

Digital Connectivity

|

| By Service Model |

|

Refurbishment & Calibration Services

|

Regional Analysis: Capacitance Diaphragm Vacuum Gauges for Semiconductor Market

Asia‑Pacific

Taiwan’s integrated circuit parks, South Korea’s advanced device fabs, and China’s emerging front‑end sites host a concentration of vacuum gauge assemblers. Proximity to end‑users enables real‑time feedback loops, which shorten product development cycles and foster bespoke gauge configurations that align with process nuances.

The region’s diversified component base, from ceramic diaphragm producers to precision electronics firms, cushions the gauge market against single‑source disruptions. Multi‑tiered logistics networks and cross‑border trade agreements further reinforce continuity for manufacturers.

Harmonized standards across key economies simplify certification pathways. Joint technical committees in the region regularly update safety and performance guidelines, ensuring that new gauge models meet globally recognized criteria without redundant testing.

Collaborative R&D programs between gauge makers and semiconductor designers accelerate the incorporation of AI‑enabled diagnostics. These initiatives translate process data into predictive maintenance insights, extending gauge uptime and enhancing overall fab efficiency.

North America

North America remains a strong secondary market for Capacitance Diaphragm Vacuum Gauges for Semiconductor Market, buoyed by legacy fabs in the United States and emerging facilities in Canada. The ecosystem is characterized by deep financial resources and a mature engineering talent pool that prioritizes high‑reliability instrumentation. While the region’s emphasis on sustainability pushes manufacturers toward gauges with lower power consumption, the stringent certification regime demands rigorous testing, which can lengthen time‑to‑market but also guarantees premium quality for end users.

Europe

European demand reflects a blend of mature semiconductor clusters in Germany, the Netherlands, and France, where precision engineering culture drives meticulous process control. Regulatory bodies impose exacting environmental and safety standards, prompting gauge suppliers to embed advanced monitoring features. Collaborative research consortia funded by the EU encourage cross‑border innovation, leading to hybrid gauge models that combine traditional capacitance measurement with emerging optical diagnostics, thereby widening the functional envelope for semiconductor manufacturers.

South America

In South America, the market is still nascent, yet rising investment in microelectronics foundries in Brazil and Colombia creates a foothold for gauge providers. Local manufacturers focus on cost‑effective designs that do not compromise core accuracy, catering to fabs that balance volume production with limited capital expenditure. Partnerships with regional universities are cultivating a pipeline of engineers versed in vacuum technology, which should gradually elevate the sophistication of gauge applications across the continent.

Middle East & Africa

The Middle East & Africa region exhibits modest yet growing interest, driven primarily by high‑tech industrial parks in the United Arab Emirates and emerging semiconductor initiatives in South Africa. Governmental diversification strategies aim to reduce reliance on oil revenues, fostering incentives for advanced manufacturing. Gauge suppliers entering this market often adopt a localized support model, offering training and on‑site calibration services to overcome the scarcity of specialized technical talent and to build confidence among early adopters.

Report Scope

This market research report provides a comprehensive analysis of the Capacitance Diaphragm Vacuum Gauges for Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Capacitance Diaphragm Vacuum Gauges for Semiconductor Market?

-> Capacitance Diaphragm Vacuum Gauges for Semiconductor market is projected to reach USD 134 million by 2034.

Which key companies operate in Capacitance Diaphragm Vacuum Gauges for Semiconductor Market?

-> Key players include MKS Instruments, INFICON, Atlas Copco (Leybold and Edwards), Pfeiffer Vacuum+Fab Solutions, Setra Systems, Canon Anelva, Brooks Instrument, ZHENTAI INSTRUMENT, ULVAC, Azbil, Agilent, Kurt J. Lesker, EBARA, ASAIR, Atovac, SATO VAC, among others.

What are the key growth drivers?

-> Key growth drivers include advanced‑node and advanced‑packaging expansions, productivity upgrades in existing fabs, strong semiconductor pull on vacuum metrology, and government incentives such as U.S. CHIPS and EU Chips Act programmes.

Which region dominates the market?

-> Asia accounts for the largest share of demand, driven by rapid fab build‑outs in China, Japan, and South Korea, while North America and Europe remain significant secondary markets.

What are the emerging trends?

-> Emerging trends include network‑enabled CDGs with digital connectivity and remote diagnostics, premium heated and corrosion‑resistant designs, and an increasing share of aftermarket services such as recalibration and refurbishment.

What is the projected compound annual growth rate (CAGR) for the market?

-> The market is projected to grow at a CAGR of 6.7%% over the forecast period.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...