3.2T Optical Module Market Insights

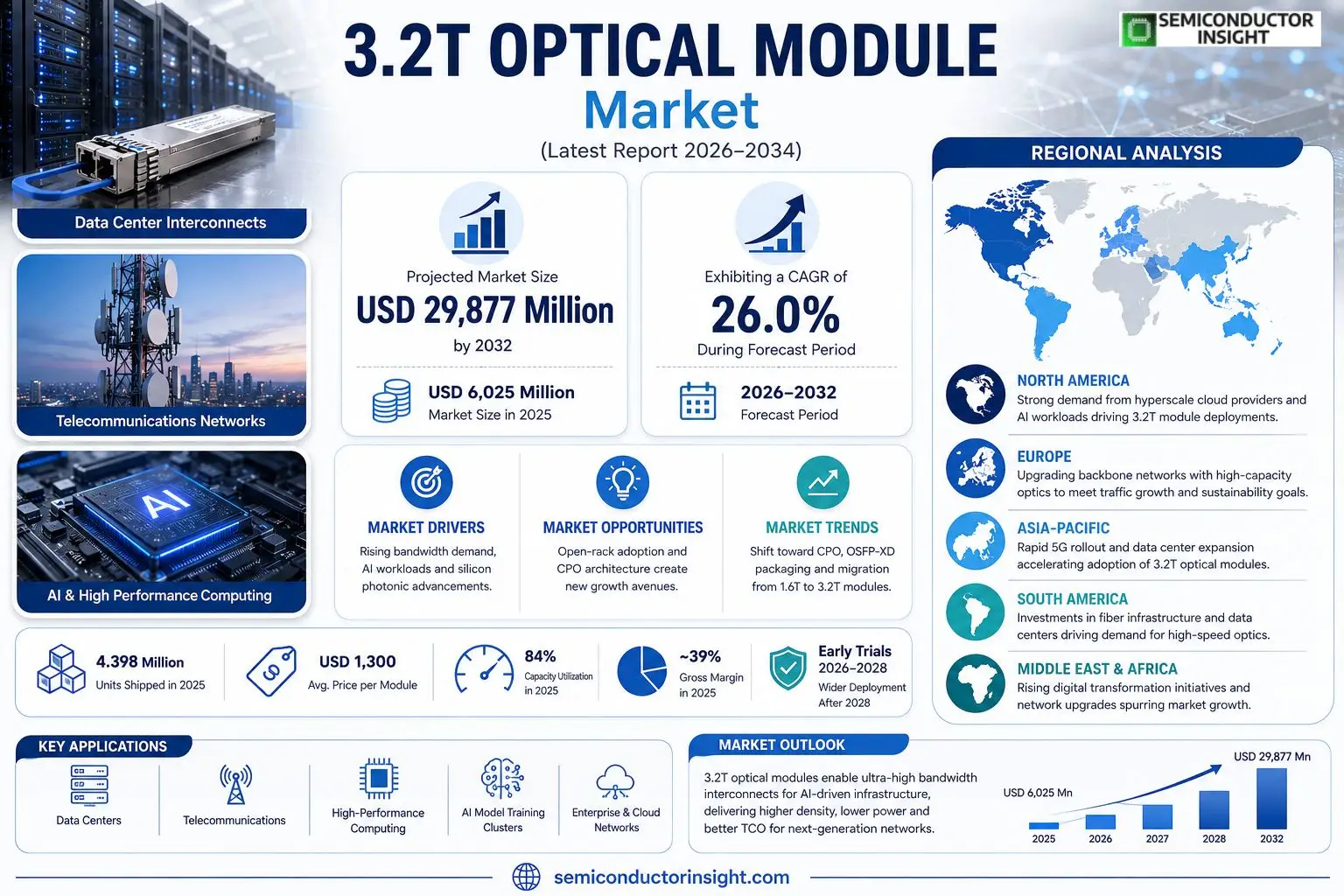

Global 3.2T Optical Module market size was USD 6,025 million in 2025 and will rise to USD 29,877 million by 2034, reflecting a CAGR of 26.0 % over the forecast horizon.

3.2T optical modules are ultra‑high‑speed optical communication devices delivering a single‑port bandwidth of 3.4 Tbps (400G/lane × 8). Their typical architecture uses OSFP‑XD or other high‑density packages and integrates ultra‑fast DSP chips, silicon‑photonic ICs, high‑performance EML or CW lasers and rapid photodetectors—providing higher bandwidth density while lowering power per unit area.The expansion of AI model training workloads and increasing GPU cluster density have accelerated demand for rack‑level interconnects that exceed the capabilities of existing 1.6T solutions; consequently manufacturers such as HGTech, Sanan Optoelectronics, InnoLight Technology and Lumentum are expanding production capacity and advancing packaging technologies. Early prototype trials are slated for 2026–2028, with broader deployment anticipated after 2028.

MARKET DRIVERS

Increasing Bandwidth Demands in Core Networks

The surge in hyperscale cloud services and AI‑intensive workloads forces operators to double‑digit capacity upgrades every 18‑24 months. 3.2T Optical Module Market solutions deliver roughly twice the payload of legacy 100G transceivers, allowing carriers to meet traffic spikes without multiplying fiber plant. Cost per gigabit declines sharply when single‑module throughput rises, prompting network planners to prioritize high‑density optics.

Advances in Silicon Photonics Integration

Recent breakthroughs in silicon photonic drivers and low‑loss waveguides have trimmed module footprints by 30% while preserving power efficiency. These engineering gains translate into tighter rack densities and lower cooling loads, which are decisive factors for data‑center operators seeking to squeeze more capacity into existing footprints. Manufacturers that lock in silicon‑photonic platforms early gain a competitive edge in 3.2T Optical Module Market.

➤ 45% of Tier‑1 operators have already trialed 3.2T modules in backbone deployments, reporting up to 28% reduction in OPEX.

From a financial perspective, the ability to replace three 100G links with a single 3.2T unit reshapes CAPEX models. Investment cycles shorten, and the amortization horizon improves, encouraging both incumbents and new entrants to allocate budget toward next‑generation optics.

MARKET CHALLENGES

Thermal Management Constraints

High‑density 3.2T modules concentrate more electrical power within a compact casing, pushing junction temperatures close to design limits. Data‑center engineers must redesign airflow patterns or adopt liquid‑cooling solutions, both of which inflate deployment costs and complicate retrofit projects. Without effective thermal strategies, reliability can suffer, leading to higher warranty claims.

Other Challenges

Manufacturing Yield Issues

Silicon photonics production still grapples with wafer‑level defect rates that exceed 5% for the most aggressive designs. Yield shortfalls translate into higher unit prices and longer lead times, which can deter cost‑sensitive carriers from committing to large‑scale rollouts.

MARKET RESTRAINTS

High Capital Expenditure for Upgrade Cycles

Replacing entrenched 100G or 200G infrastructure with 3.2T optics demands upfront spending on transceivers, chassis adaptations, and monitoring software. Many service providers operate under multi‑year budgeting constraints, making it difficult to earmark the necessary funds in a single fiscal period. These budgetary pressures slow adoption rates, especially among operators with legacy asset bases.Furthermore, the economics of scale remain uneven; only a limited number of large‑volume customers can negotiate price breaks that bring 3.2T modules into parity with lower‑rate alternatives. Smaller operators therefore face a cost premium that restricts market penetration.

MARKET OPPORTUNITIES

Emergence of Open‑Rack Architectures

Open‑rack designs standardize power, cooling, and optical interfaces, creating a uniform platform for high‑capacity transceivers. As more carriers adopt these racks, the pathway for 3.2T Optical Module Market products becomes smoother, reducing integration complexity and cost. Vendors that certify their modules for open‑rack specifications stand to capture a sizable share of forthcoming deployments.The convergence of 400G Ethernet standards with 3.2T module capabilities also opens avenues in hyperscale data centers seeking to future‑proof their fabric. By positioning 3.2T optics as a drop‑in upgrade path for emerging 400G‑plus protocols, manufacturers can differentiate their portfolios and lock in long‑term service contracts.

3.2T Optical Module Market Trends

AI‑Centric Bandwidth Expansion

3.2T Optical Module Market recorded a revenue of US$ 6,025 million in 2025, reflecting the rapid uptake of ultra‑high‑speed interfaces in hyperscale data centers. Production hit roughly 4.398 million units that year, with an average selling price near US$1,300 per module. This pricing level, combined with a gross profit margin of about 39 %, signals that manufacturers have achieved a balanced cost‑performance equation. The surge is directly tied to the exponential growth of large‑scale AI model training, where each GPU cluster demands bandwidth beyond the 1.6 Tbps ceiling. As 800 G and 1.6 T solutions saturate early deployments, operators are compelled to adopt 3.2 Tbps interconnects to keep latency growth in check and to sustain the scaling of transformer‑style networks.

Other Trends

Supply‑Chain Consolidation

Upstream silicon‑photonic foundries and high‑speed DSP/SerDes providers are converging into a tighter ecosystem, driven by the need for consistent performance across the entire module stack. Companies such as HGTech and Sanan Optoelectronics have entered joint‑development agreements that lock in wafer capacity for the next five years, reducing the risk of component shortages that plagued earlier generations. Mid‑stream manufacturers are standardising on OSFP‑XD and emerging high‑density packages, which simplifies testing protocols and accelerates time‑to‑market. Down‑stream, cloud giants like AWS and Google Cloud are issuing multi‑year procurement contracts that lock in pricing and volume, encouraging suppliers to invest in dedicated production lines capable of delivering the 5.48 million‑unit capacity target projected for 2028. This vertical alignment not only improves forecast accuracy but also creates entry barriers for new entrants lacking integrated supply channels.

Transition Toward Co‑Packaged Optics (CPO)

The long‑term roadmap for 3.2T Optical Module Market points to a migration from discrete transceiver architectures to co‑packaged optics, where lasers and DSPs sit on the same silicon substrate as the switching ASIC. Early prototypes demonstrated a 15 % reduction in power per terabit, a metric critical for data‑center operators facing stringent PUE targets. By 2030, large‑scale deployments are expected to incorporate CPO designs, effectively reshaping rack‑level topology and reducing the number of optical fibers required per node. This shift also opens opportunities for silicon‑photonic integration firms to capture a larger share of the value chain, as they become indispensable to the next wave of network equipment. The strategic implication for incumbents is clear: those who master CPO integration will dictate the pricing baseline for future interconnect solutions, while laggards risk being sidelined as customers gravitate toward higher‑density, lower‑energy alternatives.

COMPETITIVE LANDSCAPEKey Industry Players

3.2T Optical Module Market – Competitive Overview

The market’s hierarchy is anchored by a handful of manufacturers that have leveraged deep expertise in silicon‑photonics integration and high‑speed DSP design to command the majority of revenue in 2025. HGTech, for example, converted its early lead in 400G module packaging into a vertically integrated platform that now supplies both upstream chip makers and downstream hyperscale data‑center operators. Its ability to scale production to 5.48 million units while maintaining a gross margin close to 40 % has pressured rivals to pursue joint ventures or acquire niche asset portfolios. The company’s aggressive rollout of OSFP‑XD form‑factor modules aligns with the current shift toward denser rack designs, allowing it to capture a sizeable portion of the premium‑price tier and set pricing benchmarks for the entire segment.Beyond the dominant tier, a diverse group of specialists advances the ecosystem through differentiated technology or regional focus. Sanan Optoelectronics and InnoLight Technology have concentrated on SiPh foundry services, enabling smaller OEMs to access advanced laser sources without the capital outlay of a full fab. Meanwhile, European and Japanese incumbents such as Nokia, Cisco and Lumentum differentiate through ecosystem integration, bundling optical modules with networking software that simplifies deployment for AI‑focused cloud providers. Smaller players—including Anpioe, Eoptolink Technology, POET Technologies, and Accelink—target niche applications such as low‑latency interconnects for financial trading or edge‑AI clusters, where custom form‑factors and rapid prototype cycles outweigh economies of scale. This tiered competitive structure creates clear pressure points: large integrators must defend against margin erosion, while niche firms must continuously innovate to stay relevant in a market that rewards both volume and specialization.

List of Key 3.2T Optical Module Companies Profiled

- HGTech

- Cisco

- Sanan Optoelectronics

- Anpioe

- Eoptolink Technology

- InnoLight Technology

- Lumentum

- Nokia

- Ciena

- NEC

- POET Technologies

- OE Solutions

- LITE-ON

- Accelink

- Coherent Corp

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CPO

|

| By Application |

|

Data Centers

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

OSFP‑XD

|

| By Market Positioning |

|

Early Adopters

|

Regional Analysis: 3.2T Optical Module Market

Europe

The EU’s 2025 carbon‑neutral networking agenda allocates subsidies for energy‑efficient transceivers, making 3.2T modules attractive for operators seeking to lower OPEX while meeting sustainability targets.

European OEMs are forging joint ventures with silicon photonics firms to shorten lead times, ensuring that demand spikes for 3.2T solutions are met without extensive import delays.

Large‑scale data centers in Frankfurt and Paris are deploying 3.2T optics to consolidate rack density, a move that reduces physical footprint and simplifies power distribution architectures.

European research consortia are influencing the next wave of IEC standards, positioning the continent as a reference market for interoperability testing of 3.2T modules.

North America

North American carriers are navigating a distinct set of market forces. The United States, with its extensive subsea cable footprint, views 3.2T optical modules as a lever to maximize capacity without laying new conduit. Service providers are leveraging the modules to bundle multiple 400 Gbps lanes into a single chassis, a tactic that accelerates rollout timelines for hyperscale cloud providers. In Canada, the emphasis is on resilience; operators integrate 3.2T devices into redundant ring topologies to meet stringent service‑level agreements for financial and health‑care data streams. The competitive landscape pushes vendors to offer flexible firmware updates, allowing customers to adapt to evolving traffic patterns without hardware swaps.

Asia‑Pacific

The Asia‑Pacific region presents a heterogeneous adoption curve. In Japan and South Korea, mature telecom ecosystems are already piloting 3.2T modules within 5G backhaul networks to ensure that mobile traffic can sustain ultra‑low latency demands. Conversely, emerging markets such as Vietnam and Indonesia prioritize cost‑effectiveness, opting for hybrid deployments where 3.2T optics complement legacy 100 Gbps equipment. This dual‑strategy fuels a niche for modular transceivers that can coexist with older platforms, driving an ecosystem of integration services and field engineering expertise.

South America

South American operators confront both infrastructural constraints and escalating data consumption. Brazil’s major carriers are channeling capital into coastal fiber corridors, selecting 3.2T modules to achieve long‑haul capacity in a single fiber pair, thereby sidestepping the expense of additional dark fiber. In Argentina, public‑private partnerships aim to bridge urban‑rural gaps, and the high spectral efficiency of 3.2T optics becomes a decisive factor in meeting universal broadband commitments while maintaining affordable tariffs.

Middle East & Africa

The Middle East & Africa region is at an inflection point where sovereign wealth funds and telecom ministries are funding ambitious network upgrades. Gulf Cooperation Council (GCC) nations, leveraging their strategic position along global internet exchange points, deploy 3.2T modules to attract data‑center investments. In Sub‑Saharan Africa, the focus shifts to rapid capacity scaling; 3.2T optics enable a “one‑fiber‑many‑services” model that reduces the need for extensive trenching projects, thus aligning with budgetary realities while delivering the bandwidth required for emerging e‑commerce and e‑government platforms.

Report Scope

This market research report provides a comprehensive analysis of the 3.2T Optical Module Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3.2T Optical Module Market?

-> 3.2T Optical Module Market was valued at USD 6,025 million in 2025 and is expected to reach USD 29,877 million by 2034, growing at a CAGR of 26.0% during the forecast period.

Which key companies operate in 3.2T Optical Module Market?

-> Key players include HGTech, Sanan Optoelectronics, Anpioe, Eoptolink Technology, InnoLight Technology, Coherent Corp, Lumentum, Cisco, Nokia, Ciena, among others.

What are the key growth drivers?

-> Key growth drivers include the exponential increase in AI computing power, rising bandwidth demand in data centers, the need to alleviate rack‑level bandwidth bottlenecks, and the transition toward CPO architecture for higher integration.

Which region dominates the market?

-> The provided reference does not specify a dominant region for 3.2T Optical Module Market.

What are the emerging trends?

-> Emerging trends include adoption of high‑density OSFP‑XD packaging, integration of silicon photonics (SiPh) with DSP chips, migration from 1.6T to 3.2T modules, and the development of CPO‑based network architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...