Zoned Namespace (ZNS) SSD Controller Market Insights

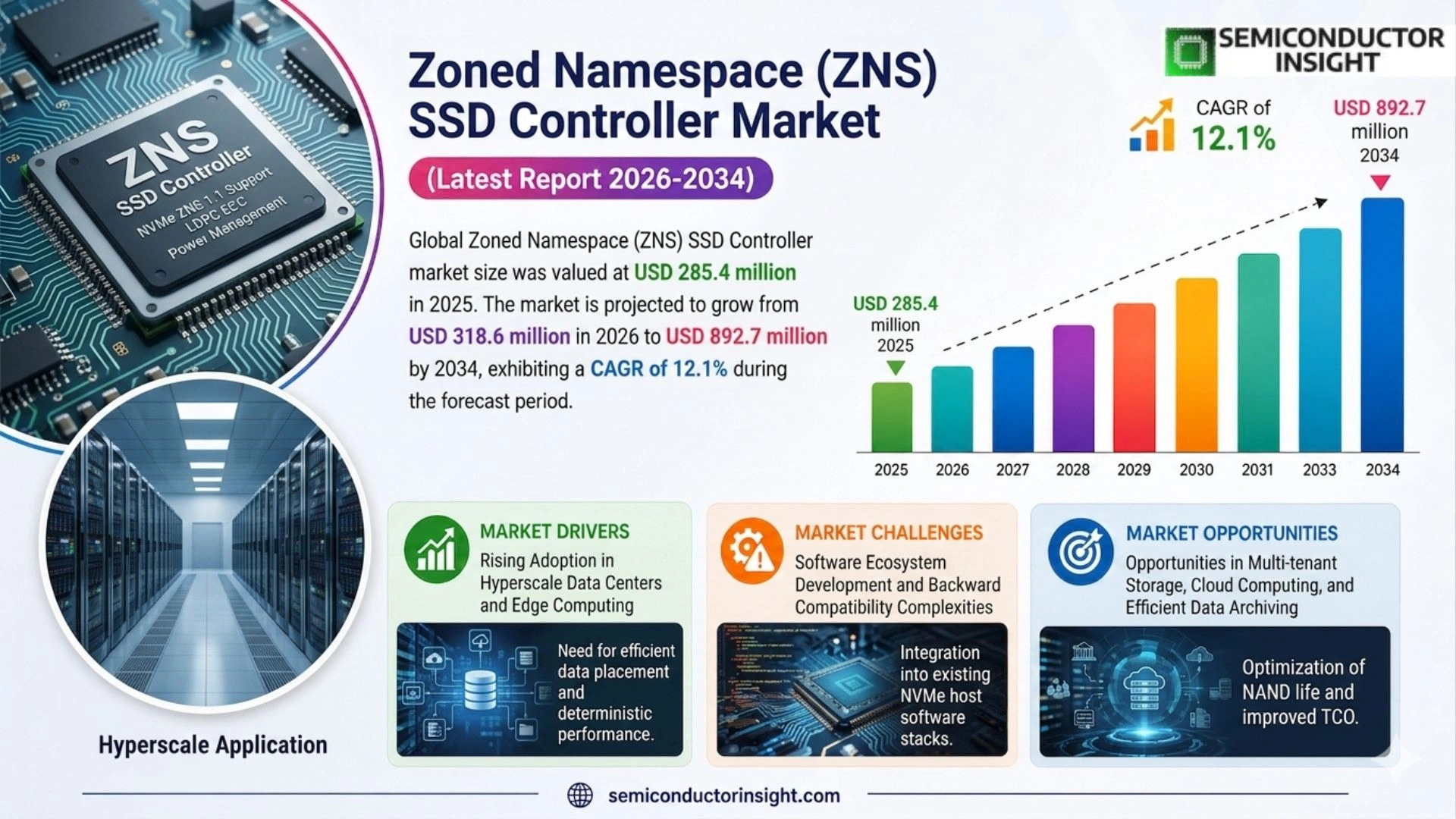

Zoned Namespace (ZNS) SSD Controller Market size was valued at USD 285.4 million in 2025. The market is projected to grow from USD 318.6 million in 2026 to USD 892.7 million by 2034, exhibiting a CAGR of 12.1% during the forecast period.

Zoned Namespace (ZNS) SSDs represent a significant architectural advancement in solid-state storage technology, enabling host software to manage data placement across defined zones within the drive. Unlike conventional SSDs, ZNS controllers eliminate the need for a large device-side DRAM buffer and reduce write amplification by allowing applications to write data sequentially within designated zones. This architecture is particularly well-suited for workloads such as log-structured storage engines, key-value stores, and large-scale data center applications, where sequential write patterns are predominant.

The market is gaining strong momentum driven by the exponential growth of hyperscale data centers, rising adoption of NVMe-based storage solutions, and the increasing need for cost-efficient, high-endurance storage in cloud infrastructure. Furthermore, the standardization of the ZNS specification under the NVMe 2.0 framework by the NVM Express organization has accelerated vendor adoption and ecosystem development. Key players actively driving innovation in this space include Western Digital Corporation, Samsung Electronics, Micron Technology, Kioxia Holdings, and Silicon Motion Technology, each offering differentiated ZNS-compatible controller and SSD solutions targeting enterprise and hyperscale deployments.

MARKET DRIVERS

Surging Demand for High-Density Storage in Hyperscale Data Centers

The rapid expansion of hyperscale data centers operated by major cloud service providers has become one of the most significant forces propelling Zoned Namespace (ZNS) SSD Controller Market forward. As global data generation accelerates, enterprises require storage architectures that deliver both high throughput and improved write endurance. ZNS SSDs address this need by allowing the host system to manage data placement at a zone level, substantially reducing write amplification and extending drive longevity compared to conventional NVMe SSDs. This architectural advantage makes ZNS-based controllers a compelling proposition for large-scale storage deployments where total cost of ownership is a critical factor.

Adoption of NVMe-oF and Open-Source Storage Stacks Accelerating Controller Innovation

The growing deployment of NVMe over Fabrics (NVMe-oF) across distributed storage environments is reinforcing the relevance of the ZNS SSD Controller Market. Open-source ecosystems such as the Linux kernel’s ZNS support, RocksDB’s ZenFS plugin, and SPDK-based storage frameworks have dramatically lowered the software integration barrier for ZNS adoption. Storage controller vendors are responding by developing firmware and hardware architectures that align tightly with these software stacks, enabling more deterministic latency and improved garbage collection efficiency. The convergence of hardware innovation and open-source software momentum continues to act as a self-reinforcing driver within the market.

➤ ZNS SSD technology reduces write amplification by enabling zone-aligned sequential writes, a design principle that aligns directly with log-structured storage engines widely used in modern cloud-native applications.

Beyond cloud infrastructure, the Zoned Namespace SSD Controller ecosystem is gaining traction in content delivery networks, video surveillance platforms, and AI training storage clusters, where sequential write workloads dominate. Controller manufacturers are investing in advanced node process geometries and hardware-based zone management logic to push performance boundaries, further broadening the addressable market and reinforcing demand-side growth across multiple verticals.

MARKET CHALLENGES

Complex Host-Side Software Requirements Limiting Broader Adoption

Despite its technical merits, the Zoned Namespace SSD Controller Market faces a notable adoption barrier rooted in software complexity. Unlike traditional SSDs where the Flash Translation Layer (FTL) abstracts storage management from the host, ZNS SSDs require the host application or operating system to manage zone state, enforce sequential write ordering, and handle zone resets explicitly. This places a significant burden on software developers and storage architects who must redesign or adapt existing I/O stacks. Many enterprises, particularly mid-market organizations without dedicated storage engineering teams, find this requirement challenging to meet without substantial investment in software expertise and development resources.

Other Challenges

Limited Ecosystem Maturity Across Enterprise Applications

While hyperscale cloud providers have the engineering capacity to leverage ZNS architecture effectively, the broader enterprise segment continues to rely on conventional NVMe SSDs with full device-managed FTLs. The ZNS SSD Controller ecosystem currently lacks widespread support across popular enterprise storage operating systems, SAN/NAS platforms, and database management systems. Until independent software vendors and storage platform developers integrate native ZNS support into mainstream products, market penetration beyond cloud-native workloads will remain constrained, posing a tangible challenge to sustained revenue growth in the mid-enterprise tier.

Interoperability and Standardization Gaps

The NVMe ZNS specification, while managed under the NVMe Express industry consortium, continues to evolve, and early-generation ZNS SSD controllers exhibit varying levels of compliance with emerging specification revisions. This creates interoperability concerns when mixing controller generations or integrating ZNS drives with diverse host adapters and PCIe switch fabrics. Storage architects evaluating the Zoned Namespace SSD Controller Market must account for qualification overhead and potential firmware dependency risks, factors that can elongate procurement cycles and increase validation costs in mission-critical deployment environments.

MARKET RESTRAINTS

High Development Cost and Specialized Engineering Resources Required for ZNS Integration

One of the primary restraints shaping the trajectory of Zoned Namespace (ZNS) SSD Controller Market is the elevated cost associated with developing and integrating ZNS-compatible controller silicon. Designing a ZNS SSD controller demands specialized ASIC engineering expertise, deep familiarity with the NVMe ZNS specification, and extensive co-design collaboration between controller firmware teams and host-side software developers. For smaller semiconductor firms and emerging storage startups, the capital expenditure required to bring a competitive ZNS controller to market represents a significant financial barrier, effectively concentrating product development activity among a limited number of well-resourced incumbents and constraining broader competitive diversity within the supply landscape.

Transition Risk and Installed Base Inertia in Legacy Storage Environments

Enterprise and service provider storage environments often operate with substantial installed bases of conventional NVMe and SATA SSDs, supported by mature management toolchains, backup frameworks, and monitoring platforms. The migration to ZNS SSD Controller-based architectures requires not only hardware replacement but also parallel updates to software-defined storage layers, data protection policies, and operational runbooks. This transition complexity introduces risk and disruption that procurement and operations teams are often reluctant to accept, particularly in environments where storage uptime obligations are governed by stringent service level agreements. The resulting inertia acts as a meaningful restraint on near-term market expansion, even where the long-term economic case for ZNS adoption is well established.

MARKET OPPORTUNITIES

Expansion of AI and Machine Learning Workloads Creating New Demand Vectors for ZNS Controllers

The proliferation of AI model training and large-scale inference infrastructure presents a compelling growth opportunity for Zoned Namespace (ZNS) SSD Controller Market. AI and ML pipelines generate highly sequential, append-dominant I/O patterns that align naturally with ZNS storage architecture. As GPU and accelerator clusters scale to support increasingly large foundation models, the associated storage tier must deliver consistent throughput with minimal latency variance. ZNS SSD controllers, by eliminating unpredictable garbage collection pauses inherent in conventional FTL-managed drives, are well positioned to serve as the storage substrate for high-performance AI training clusters, representing a structurally growing demand vector that controller vendors can address with purpose-built product lines.

Emerging Computational Storage and CSD Architectures Enabling ZNS Controller Differentiation

The convergence of computational storage device (CSD) architectures with ZNS principles offers a differentiated product opportunity for ZNS SSD Controller vendors capable of embedding programmable processing elements within the controller silicon. By enabling near-data processing of zone-structured datasets , such as key-value compaction, data filtering, or compression offload , next-generation ZNS controllers can deliver measurable reductions in host CPU utilization and memory bus contention. This capability is particularly attractive to hyperscale operators seeking to improve rack-level efficiency metrics. Controller vendors that invest in CSD-ZNS hybrid architectures stand to capture premium market segments and establish durable competitive differentiation within the broader Zoned Namespace SSD Controller Market over the coming years.

Zoned Namespace (ZNS) SSD Controller Market Trends

Hyperscale Data Center Expansion Accelerating ZNS SSD Controller Adoption

Zoned Namespace (ZNS) SSD Controller Market is witnessing robust momentum as hyperscale data centers increasingly prioritize storage efficiency and total cost of ownership. The exponential growth in cloud infrastructure deployments has prompted data center operators to evaluate ZNS-based storage architectures as a practical alternative to conventional SSDs. ZNS controllers eliminate the need for large device-side DRAM buffers and significantly reduce write amplification by enabling host software to manage data placement within sequentially written zones. This architectural advantage translates directly into improved drive endurance and reduced operational expenditure, making ZNS SSD controllers an increasingly attractive option for large-scale cloud and enterprise deployments.

Other Trends

NVMe 2.0 Standardization Driving Ecosystem Development

The formal inclusion of the ZNS specification within the NVMe 2.0 framework by the NVM Express organization has been a pivotal catalyst for broader vendor participation and ecosystem maturation. Standardization has reduced interoperability concerns and enabled storage software developers, operating system vendors, and hardware manufacturers to align their roadmaps around a common ZNS interface. This has accelerated the development of ZNS-compatible firmware, file systems, and storage management tools, collectively strengthening the commercial viability of Zoned Namespace (ZNS) SSD Controller Market across enterprise and hyperscale segments.

Growing Suitability for Log-Structured and Key-Value Workloads

ZNS SSD controllers are gaining traction in environments where log-structured storage engines and key-value stores are prevalent. Because these workloads naturally generate sequential write patterns, they align well with the zone-based write model enforced by ZNS architecture. Database and storage software communities have begun optimizing their stacks specifically for ZNS interfaces, further reinforcing demand. Leading technology companies operating large-scale distributed storage systems are evaluating ZNS controllers as a means to improve throughput consistency and reduce garbage collection overhead compared to conventional flash storage solutions.

Competitive Innovation Among Key Market Participants

Major players Zoned Namespace (ZNS) SSD Controller Market, including Western Digital Corporation, Samsung Electronics, Micron Technology, Kioxia Holdings, and Silicon Motion Technology, are actively advancing differentiated controller and SSD solutions tailored for enterprise and hyperscale deployments. These companies are investing in ZNS-compatible controller architectures that balance performance, endurance, and cost efficiency. The competitive landscape is intensifying as vendors seek to capture design wins at hyperscale cloud providers, where storage procurement decisions are driven by rigorous performance benchmarking and total cost analysis. Continued innovation across firmware, controller logic, and host integration is expected to define competitive positioning withZoned Namespace (ZNS) SSD Controller Market through the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Zoned Namespace (ZNS) SSD Controller Market: Competitive Dynamics and Leading Innovators

Zoned Namespace (ZNS) SSD Controller Market is characterized by the strong presence of vertically integrated storage giants and specialized semiconductor companies competing across controller design, firmware optimization, and end-to-end ZNS-compatible SSD solutions. Western Digital Corporation, Samsung Electronics, Kioxia Holdings, and Micron Technology collectively dominate a significant share of the market, leveraging their deep expertise in NAND flash manufacturing alongside proprietary ZNS controller development. These hyperscale-focused vendors have been early movers in aligning their product portfolios with the NVMe 2.0 ZNS specification, enabling them to capture enterprise and cloud data center design wins. Silicon Motion Technology has also emerged as a critical enabler in the ecosystem by supplying ZNS-capable controller silicon to a wide range of SSD OEMs and module makers, reinforcing its position as a key merchant controller supplier in this evolving landscape.

Beyond the tier-one players, several specialized and emerging companies are carving out competitive niches within the ZNS SSD Controller market. Marvell Technology has gained traction with its Bravera and Fascia series of NVMe controllers that support ZNS workloads targeting enterprise storage and cloud infrastructure. Phison Electronics, a leading merchant controller provider, has actively developed ZNS-compliant controller platforms aimed at both client and enterprise SSD segments. INNOGRIT and Maxio Technology are emerging fabless controller companies gaining visibility through competitive ZNS controller designs for enterprise-grade applications. ScaleFlux offers computational storage drives with ZNS support, addressing data-intensive workloads in hyperscale environments. Meanwhile, open-source firmware initiatives such as OpenChannel and the SPDK ecosystem from the Linux Foundation have further enriched the competitive environment by enabling software-defined ZNS optimization at the host layer, prompting broader ecosystem participation from storage software vendors and cloud operators alike.

List of Key Zoned Namespace (ZNS) SSD Controller Companies Profiled

- Western Digital Corporation

- Samsung Electronics Co., Ltd.

- Kioxia Holdings Corporation

- Micron Technology, Inc.

- Silicon Motion Technology Corporation

- Marvell Technology, Inc.

- Phison Electronics Corporation

- INNOGRIT Corporation

- Maxio Technology (Hangzhou) Co., Ltd.

- ScaleFlux, Inc.

- SK Hynix Inc.

- Solidigm (formerly Intel NAND Solutions Group)

- Yangtze Memory Technologies Co., Ltd. (YMTC)

- Sage Microelectronics Corp.

- Starblaze Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Integrated ZNS SSD Controllers represent the leading segment within the By Type category, driven by the strong preference among enterprise storage vendors and hyperscale operators to embed zone management logic directly into the storage device.

|

| By Application |

|

Hyperscale Data Centers emerge as the dominant application segment, reflecting the broader industry shift toward cost-efficient, high-endurance storage solutions that can sustain the relentless write demands of modern internet-scale workloads.

|

| By End User |

|

Cloud Service Providers constitute the leading end-user segment within the ZNS SSD Controller market, underpinned by their insatiable demand for storage solutions that combine high endurance, reduced operational overhead, and seamless compatibility with software-defined storage architectures.

|

| By Interface Protocol |

|

NVMe-based ZNS Controllers lead this segment decisively, reflecting the foundational role that the NVMe protocol plays in enabling the full capabilities of the ZNS architecture as defined under the NVMe 2.0 specification framework.

|

| By NAND Flash Technology |

|

QLC (Quad-Level Cell) NAND-paired ZNS controllers are emerging as a highly strategic segment, as the combination of QLC NAND’s high storage density with the endurance-preserving properties of ZNS controller architecture creates a uniquely compelling value proposition for capacity-optimized storage deployments.

|

Regional Analysis: Zoned Namespace (ZNS) SSD Controller Market

North America

North America’s hyperscale cloud operators represent the most significant demand catalyst for Zoned Namespace (ZNS) SSD Controller Market. Companies building exabyte-scale storage infrastructure are prioritizing ZNS-compatible controllers to reduce write amplification overhead and optimize flash endurance, enabling leaner, cost-efficient data center operations at unprecedented scale across the United States.

The region actively shapes the NVMe and ZNS standards ecosystem through participation of leading semiconductor and systems companies in industry consortia. This standards influence ensures that North American ZNS SSD controller developers maintain a first-mover advantage in product certification, interoperability validation, and go-to-market readiness, keeping the regional supply chain ahead of global competitors.

Beyond hyperscale, North American enterprises across healthcare, financial services, and media are beginning to evaluate ZNS SSD controllers for on-premise and edge deployments. The drive to manage latency-sensitive workloads more efficiently is pushing enterprise IT buyers to pilot ZNS-based storage solutions, gradually expanding the addressable market well beyond pure cloud infrastructure applications.

Domestic semiconductor manufacturing incentives and research funding in the United States are creating favorable conditions for ZNS SSD controller chip development and localized supply chains. These policy-driven investments are attracting both established players and emerging fabless designers to deepen their ZNS controller portfolios, strengthening the region’s long-term competitive position in the global market.

Europe

Europe represents a steadily growing market for Zoned Namespace (ZNS) SSD Controller technology, anchored by the region’s expanding digital infrastructure and its strong regulatory emphasis on data sovereignty. Countries such as Germany, the Netherlands, and the United Kingdom are investing heavily in next-generation data center capacity, with colocation and cloud operators increasingly evaluating ZNS-compatible storage solutions to meet escalating performance and sustainability benchmarks. European enterprises are particularly attracted to the energy efficiency benefits inherent in ZNS SSD controller architectures, aligning with the region’s ambitious carbon neutrality goals. The European Union’s push for digital resilience and homegrown technology adoption is also encouraging regional semiconductor firms to explore ZNS controller development capabilities. While the European market trails North America in early adoption velocity, the combination of regulatory tailwinds, sustainability imperatives, and growing enterprise digitalization creates a compelling growth environment for the Zoned Namespace SSD Controller Market throughout the forecast period extending to 2034.

Asia-Pacific

Asia-Pacific is poised to emerge as the fastest-growing region Zoned Namespace (ZNS) SSD Controller Market, fueled by the rapid expansion of cloud infrastructure across China, Japan, South Korea, and India. The presence of globally significant NAND flash manufacturers and controller chip designers in this region creates a uniquely integrated supply chain that supports accelerated ZNS product development and commercialization. South Korea and Japan bring decades of SSD controller engineering expertise, enabling local firms to move swiftly in incorporating ZNS compliance into next-generation product lines. China’s massive data center buildout, despite geopolitical complexities, continues to drive substantial demand for advanced storage controller technologies. Meanwhile, India’s surging digital economy and government-backed data localization policies are generating fresh demand centers. Collectively, Asia-Pacific’s manufacturing depth, engineering talent, and voracious data infrastructure appetite make it an increasingly pivotal theater in the global Zoned Namespace SSD Controller competitive landscape.

South America

South America occupies a nascent but emerging position Zoned Namespace (ZNS) SSD Controller Market. Brazil leads regional interest, driven by its expanding financial services sector, growing e-commerce infrastructure, and increasing cloud adoption among mid-market and enterprise customers. While awareness and deployment of ZNS-specific storage architectures remain at early stages across the continent, the region’s ongoing digital transformation is creating foundational conditions for future adoption. Local data center operators, incentivized by falling hardware costs and rising demand for storage efficiency, are beginning to explore NVMe-based technologies including ZNS-compatible solutions. Argentina and Colombia are also experiencing gradual growth in technology infrastructure investment. However, economic volatility and limited local semiconductor manufacturing capacity present near-term constraints. South America’s participation in the Zoned Namespace SSD Controller Market is expected to gain meaningful traction in the latter stages of the 2026–2034 forecast window as ecosystem maturity and regional cloud penetration improve.

Middle East & Africa

The Middle East and Africa region represents a long-term opportunity withZoned Namespace (ZNS) SSD Controller Market, with momentum concentrated primarily in Gulf Cooperation Council nations and South Africa. The UAE and Saudi Arabia are leading ambitious smart city and national cloud infrastructure programs that necessitate advanced, high-efficiency storage solutions, creating potential entry points for ZNS SSD controller adoption. Sovereign wealth-backed technology investments across the Gulf are funding state-of-the-art data centers where performance and energy efficiency are primary design criteria, both of which ZNS controller architectures address effectively. Africa’s broader digital infrastructure gap, while a current limitation, also signals significant untapped long-term demand as connectivity and cloud penetration expand. The region’s market evolution will be closely tied to continued foreign direct investment in digital infrastructure and the pace of enterprise technology modernization, gradually integrating the Zoned Namespace SSD Controller Market into the regional storage procurement conversation.

Report Scope

This market research report provides a comprehensive analysis of the Zoned Namespace (ZNS) SSD Controller Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Zoned Namespace (ZNS) SSD Controller Market?

-> Zoned Namespace (ZNS) SSD Controller Market was valued at USD 285.4 million in 2025 and is expected to reach USD 892.7 million by 2034, growing at a CAGR of 12.1% during the forecast period from 2026 to 2034.

Which key companies operate Zoned Namespace (ZNS) SSD Controller Market?

-> Key players include Western Digital Corporation, Samsung Electronics, Micron Technology, Kioxia Holdings, and Silicon Motion Technology, among others, each offering differentiated ZNS-compatible controller and SSD solutions targeting enterprise and hyperscale deployments.

What are the key growth drivers?

-> Key growth drivers include exponential growth of hyperscale data centers, rising adoption of NVMe-based storage solutions, increasing need for cost-efficient and high-endurance storage in cloud infrastructure, and the standardization of the ZNS specification under the NVMe 2.0 framework by the NVM Express organization.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by large-scale data center expansions, while North America remains a dominant market owing to the strong presence of hyperscale cloud providers and early adoption of advanced NVMe storage technologies.

What are the emerging trends?

-> Emerging trends include host-managed storage architectures, log-structured storage engines, key-value store optimization, elimination of device-side DRAM buffers, reduced write amplification through sequential zone writing, and growing ecosystem development around the NVMe 2.0 ZNS specification.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...