Wafer Heaters Market Insights

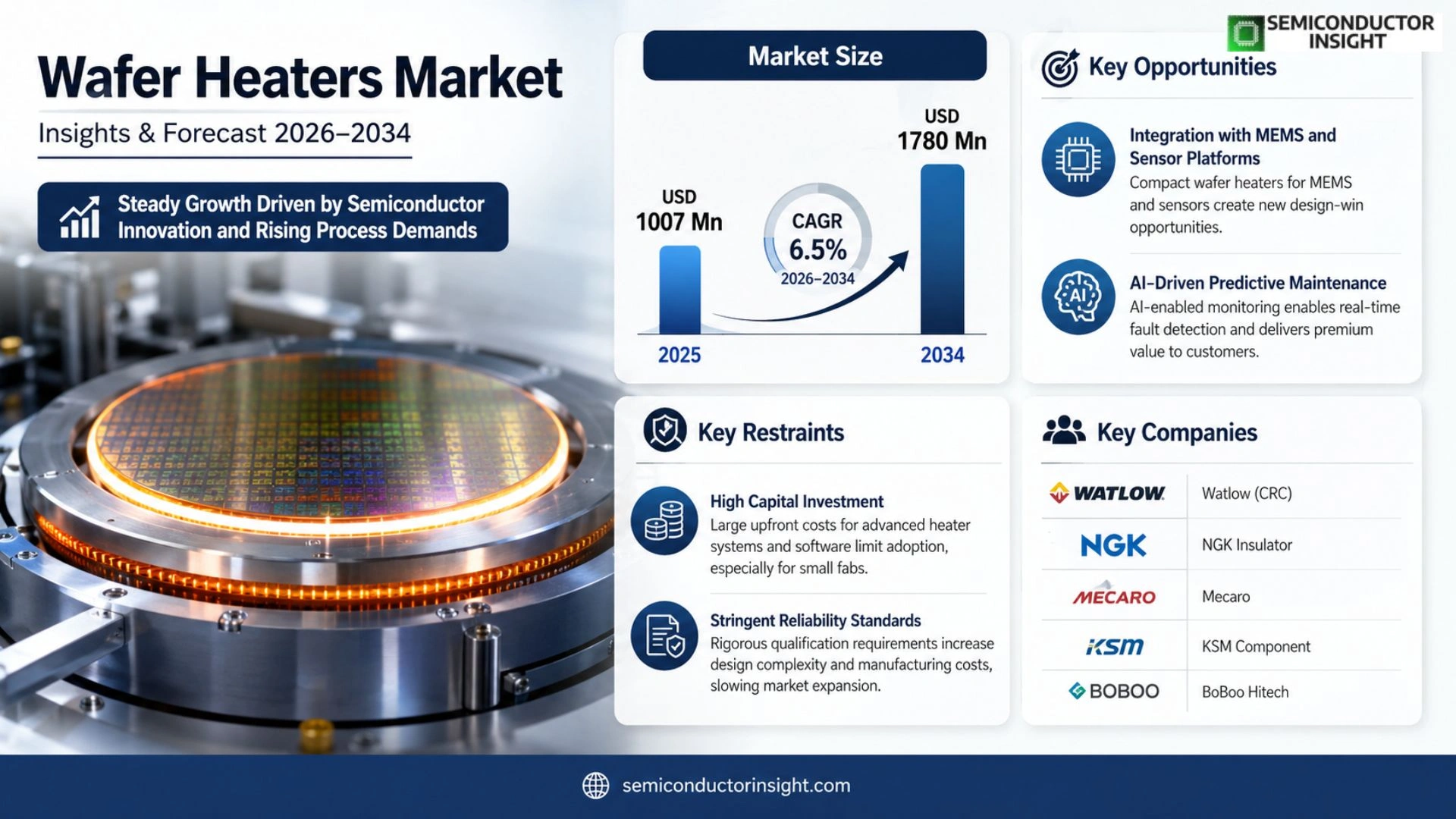

Wafer Heaters market size was valued at USD 1007 million in 2025 and is projected to reach USD 1780 million by 2034, exhibiting a CAGR of 6.5 % during the forecast period.

Wafer heaters are integral components of semiconductor wafer processing equipment, delivering uniform thermal energy during chemical vapor deposition (CVD) and etch operations to maintain process stability and film uniformity. They function as carriers for wafer handling and serve as lower electrodes for radio‑frequency circuits. Typically positioned beneath the silicon wafer,either directly or via chucks,within reaction chambers such as thin‑film deposition tools, their temperature uniformity directly influences deposition quality. Cleanliness of the heater surface governs contaminant levels while outgassing behavior affects vacuum stability.

MARKET DRIVERS

Rising Demand in Advanced Semiconductor Fabrication

Wafer Heaters Market benefits from the surge in high‑performance logic and memory chips that require tightly controlled thermal environments. As manufacturers move toward finer process nodes, the tolerance for temperature variation narrows, prompting fabs to adopt heaters capable of delivering rapid, precise heating across 200‑mm and 300‑mm wafers.

Energy‑Efficient Temperature Regulation

Recent upgrades in equipment design prioritize lower power draw without sacrificing thermal uniformity. Modern wafer heaters exploit thin‑film ceramic elements and advanced PID controllers, allowing plants to cut utility costs by up to 12 % while maintaining the temperature stability demanded by 3D‑IC and heterogeneous integration projects.

➤ “Operators that switched to low‑thermal‑mass heaters reported a 9 % reduction in cycle time, directly translating into higher fab throughput.”

These efficiencies are not merely cost‑centric; they also support sustainability goals that many global semiconductor producers have embedded into their corporate roadmaps, reinforcing the strategic relevance of Wafer Heaters Market.

MARKET CHALLENGES

Thermal Uniformity Across Large‑Diameter Wafers

Maintaining a consistent temperature profile on 300‑mm wafers remains technically demanding. Slight deviations can induce stress gradients that jeopardize device yields, especially for specialty processes such as silicon‑photonic integration where waveguide dimensions are highly temperature‑sensitive.

Other Challenges

Manufacturing Complexity

The fabrication of heater elements involves multiple deposition and patterning steps, each adding to cycle time and defect risk. Suppliers must balance high‑precision lithography with cost‑effective throughput, a trade‑off that often constrains price competitiveness.

Furthermore, end‑users frequently require custom heater footprints to match atypical wafer handling equipment, stretching engineering resources and extending lead times.

MARKET RESTRAINTS

High Capital Investment for Upgrading Heater Systems

Deploying next‑generation wafer heaters entails sizable upfront expenditures for both the hardware and the associated control software. Smaller fabs, especially those operating on thin margins, often defer such upgrades, limiting overall market penetration.

Stringent Reliability and Qualification Standards

Semiconductor equipment qualifies under rigorous reliability protocols (e.g., ISO 26262, IEC 60730). Heater modules that fail to meet extended mean‑time‑between‑failure (MTBF) targets are rejected, driving manufacturers to over‑engineer components and inflate bill‑of‑materials costs.

These constraints collectively temper the speed at which new heater technologies achieve widespread adoption, despite evident performance benefits.

MARKET OPPORTUNITIES

Integration with MEMS and Sensor Platforms

Emerging MEMS‑based sensing solutions increasingly require localized heating to stabilize resonant frequencies. Providing compact, low‑mass wafer heaters tailored for these platforms opens a niche where Wafer Heaters Market can capture additional design‑win revenue.

Adoption of AI‑Driven Predictive Maintenance

Embedding data analytics into heater control units enables real‑time fault detection and preemptive service scheduling. Companies that bundle AI‑enabled monitoring with their heater offerings stand to differentiate themselves and command premium pricing.

Wafer Heaters Market Trends

Dominance of Ceramic Technology

The shift toward ceramic‑based heaters is reshaping Wafer Heaters Market. Ceramic units deliver a tighter temperature envelope, reduce metal particle fallout and maintain stability across the high‑temperature cycles required for modern deposition and etch steps. Their longer service life and intrinsic safety profile allow fabs to extend maintenance intervals, translating into higher equipment uptime. Industry surveys indicate that more than two‑thirds of new wafer heater orders will be ceramic by the early 2030s, reflecting the alignment of ceramic properties with the tighter process windows of advanced nodes. Japan hosts the majority of specialist ceramic manufacturers, creating a geographic concentration that forms a de facto barrier to entry for newcomers. Furthermore, the adoption of low‑contamination ceramic composites aligns with the industry’s move toward 3‑nm and sub‑5‑nm patterning, where even trace metal residues can impair yield. The supply chain for high‑purity alumina and silicon nitride has become a strategic asset, prompting major fabs to qualify multiple vendors to avoid single‑source risk.

Other Trends

Material Cost vs Performance Trade‑off

Metal heaters continue to occupy a niche defined by cost sensitivity and extreme temperature capability. Their construction relies on inexpensive alloys that can sustain temperatures beyond 800 °C, making them attractive for high‑volume production lines where the marginal savings on each heater accumulate rapidly. However, the metallic surface contributes to particle generation and higher outgassing rates, which can jeopardize vacuum integrity in sensitive thin‑film tools. Consequently, equipment suppliers often recommend metal units for mature process nodes or for applications where absolute temperature uniformity is less critical, while reserving ceramic solutions for leading‑edge platforms that demand the cleanest environment. In addition, the thermal inertia of metal heaters can be advantageous for batch processes that benefit from slower cooldown cycles, allowing manufacturers to fine‑tune annealing steps without additional hardware.

Integration with Advanced Process Equipment

Integration of the heater directly into the wafer chuck is emerging as a decisive trend for Wafer Heaters Market. By mounting the heating element beneath the chuck, manufacturers achieve a more direct thermal path, reducing temperature gradients across the wafer surface. This configuration also simplifies chamber cleaning because the heater is isolated from the process gas flow, thereby limiting contaminant redeposition. As process nodes shrink, the tolerance for temperature deviation narrows, prompting fabs to demand heaters that can be calibrated in situ and that exhibit minimal outgassing during ramp‑up. Suppliers responding with modular, easily replaceable ceramic modules are positioned to capture contracts tied to next‑generation deposition equipment, while those that cling to legacy designs risk marginalisation. Finally, the trend toward digital temperature control, leveraging embedded sensors and AI‑based feedback loops, is pushing heater manufacturers to embed smart electronics within the ceramic module, opening a new revenue stream tied to service contracts.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Wafer Heaters Market

Wafer heater arena is dominated by a handful of multinational manufacturers whose combined share exceeds two‑thirds of global revenue. Watlow (CRC) and NGK Insulator sit at the apex, leveraging extensive product portfolios that span both metal and ceramic technologies. Their scale permits aggressive pricing, deep R&D investment, and the ability to supply large‑scale thin‑film deposition equipment across North America, Europe, and Asia‑Pacific. The concentration of market power enables these leaders to set technical standards for temperature uniformity and outgassing performance, compelling downstream fab operators to align their equipment specifications with the capabilities offered by the top tier.

Beyond the headline players, a dense cluster of specialist firms occupies niche segments, particularly in the high‑purity ceramic space. Companies such as Mecaro, KSM Component, and Spirax Group (Durex & Thermocoax) concentrate production in Japan and Taiwan, where legacy expertise in advanced ceramics translates into superior lifespan and contamination control. Metal‑heater specialists like Cast Aluminum Solutions and Tempco Electric Heater focus on cost‑sensitive applications, yet they face increasing pressure as fabs migrate toward sub‑7 nm nodes that demand the thermal stability of ceramic solutions. The competitive friction stems from the trade‑off between price advantage and the stringent thermal performance required for next‑generation process nodes, creating a clear incentive for smaller firms to differentiate through material innovation and customized engineering services.

List of Key Wafer Heaters Companies Profiled

- Watlow (CRC)

- NGK Insulator

- Mecaro

- KSM Component

- BoBoo Hitech

- Spirax Group (Durex & Thermocoax)

- NHK Spring Co., Ltd.

- Sumitomo Electric

- NTK Ceratec

- Kyocera

- CoorsTek

- Momentive Technologies

- Sprint Precision Technologies Co., Ltd.

- Backer AB

- Sanyue Semiconductor Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ceramic Heaters are emerging as the preferred choice because they offer superior thermal stability, lower metal contamination, and faster heat up times. Key qualitative drivers include:

|

| By Application |

|

CVD dominates usage because process uniformity and precise temperature control are critical for high‑quality thin‑film deposition. Qualitative observations highlight:

|

| By End User |

|

Semiconductor Fabrication Equipment Vendors drive market direction by demanding heaters that integrate seamlessly with advanced process tools. Their qualitative priorities include:

|

| By [Segment Category 3]] |

|

Ceramic continues to gain preference for its low contaminant profile and precision heating, while metal options remain valuable for cost‑sensitive applications. Observed qualitative trends:

|

| By [Segment Category 4]] |

|

300mm Wafer Heaters are increasingly favored as the industry moves toward larger wafer formats, delivering higher throughput and uniformity. Qualitative observations include:

|

Regional Analysis: Wafer Heaters Market

North America

A dense cluster of heater‑module manufacturers resides around the Great Lakes and Silicon Valley, creating a competitive environment that accelerates product iteration. Proximity to leading fabs enables rapid prototyping, short feedback loops, and the co‑development of custom heater geometries tailored to emerging lithography techniques. This localized supply chain advantage sustains the region’s market share.

Recent geopolitical tensions have prompted North American firms to diversify raw‑material sources for ceramic substrates, incorporating domestic producers to mitigate disruption risk. The resulting buffer not only steadies lead times but also positions OEMs as reliable partners for fabs that cannot tolerate thermal‑module shortages during high‑volume production cycles.

Energy‑efficiency standards introduced by the Department of Energy incentivize the adoption of low‑loss heater designs. Companies that embed compliance into early R&D stages see faster qualification with customers, translating into shortened sales cycles and stronger market penetration.

The rise of silicon‑photonic foundries and quantum‑dot display manufacturing creates niche demand for heaters that can sustain ultra‑stable temperatures over long runtimes. North American innovators are already filing patents that address these niche requirements, giving them a first‑mover edge.

Europe

European wafer‑heater suppliers benefit from a mature ecosystem centered around Germany, the Netherlands, and France, where precision engineering traditions dovetail with strong research universities. The region’s emphasis on modular, retro‑fittable heater designs caters to legacy fabs seeking to extend the life of 28 nm lines while meeting stringent EU environmental directives. Collaborative programs between industry consortia and the European Commission have accelerated the development of standards for thermally stable process modules, prompting OEMs to embed compliance as a selling point. Although cost pressures are more pronounced than in North America, European firms leverage high‑value engineering services to justify premium pricing, maintaining a respectable share of Wafer Heaters Market.

Asia‑Pacific

Asia‑Pacific stands out for its rapid capacity expansion, particularly in Taiwan, South Korea, and increasingly China. The region’s aggressive fab build‑out strategy fuels demand for scalable heater solutions that can be mass‑produced without sacrificing accuracy. Local manufacturers capitalize on lower labor costs and vertically integrated supply chains, enabling aggressive pricing that appeals to cost‑sensitive fabs. However, the market is fragmented; divergent quality standards across jurisdictions create a hurdle for firms seeking cross‑border contracts. Strategic alliances with local distributors and joint‑venture R&D centers are becoming common ways to bridge these gaps and secure footholds in the fastest‑growing segment of Wafer Heaters Market.

South America

South America’s wafer‑heater activity remains confined to a handful of pilot lines in Brazil and Chile, where government‑sponsored semiconductor incubators aim to seed a domestic supply chain. The limited scale translates into a focus on adaptable heater platforms that can serve both micro‑electronics and emerging sensor applications. Investors are watching closely as regional policy shifts toward high‑tech incentives, which could trigger a modest uplift in demand for temperature‑control modules. For now, market players view the continent as a long‑term growth horizon rather than an immediate revenue driver.

Middle East & Africa

In the Middle East & Africa, Wafer Heaters Market is shaped by nascent semiconductor initiatives in the United Arab Emirates and Kenya. These projects prioritize technology transfer and local workforce development, resulting in a preference for turnkey heater packages that simplify integration. While overall volume remains low, the willingness of sovereign wealth funds to finance high‑tech infrastructure creates a niche for premium‑grade heater solutions that can demonstrate reliability in harsh climatic conditions. Companies that establish early partnerships with regional development agencies are likely to capture the first wave of demand as these ecosystems mature.

Report Scope

This market research report provides a comprehensive analysis of the Wafer Heaters Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Wafer Heaters Market?

-> Wafer Heaters market size is projected to reach USD 1780 million by 2034, exhibiting a CAGR of 6.5 %

Which key companies operate in Wafer Heaters Market?

-> Key players include NGK Insulator, MiCo Ceramics, Watlow (CRC), Mecaro, KSM Component, BoBoo Hitech, Spirax Group (Durex and Thermocoax), NHK Spring Co., Ltd., Sprint Precision Technologies Co., Ltd., Sanyue Semiconductor Technology, Sumitomo Electric, NTK Ceratec, Kyocera, CoorsTek, Momentive Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced semiconductor manufacturing processes such as CVD and Etch, the need for precise temperature uniformity and low contamination, and the industry shift toward ceramic heaters that offer longer lifespan, higher safety, and faster heating.

Which region dominates the market?

-> Asia dominates Wafer Heaters market, driven by a high concentration of ceramic heater manufacturers in Japan and strong semiconductor fabrication activities across China, South Korea, and Taiwan.

What are the emerging trends?

-> Emerging trends include rapid adoption of ceramic heaters (projected to account for 71.51% of the market by 2031), focus on low metal contamination, enhanced thermal stability, and tighter temperature control to meet the requirements of advanced process nodes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...