UFS (Universal Flash Storage) Controller Market Insights

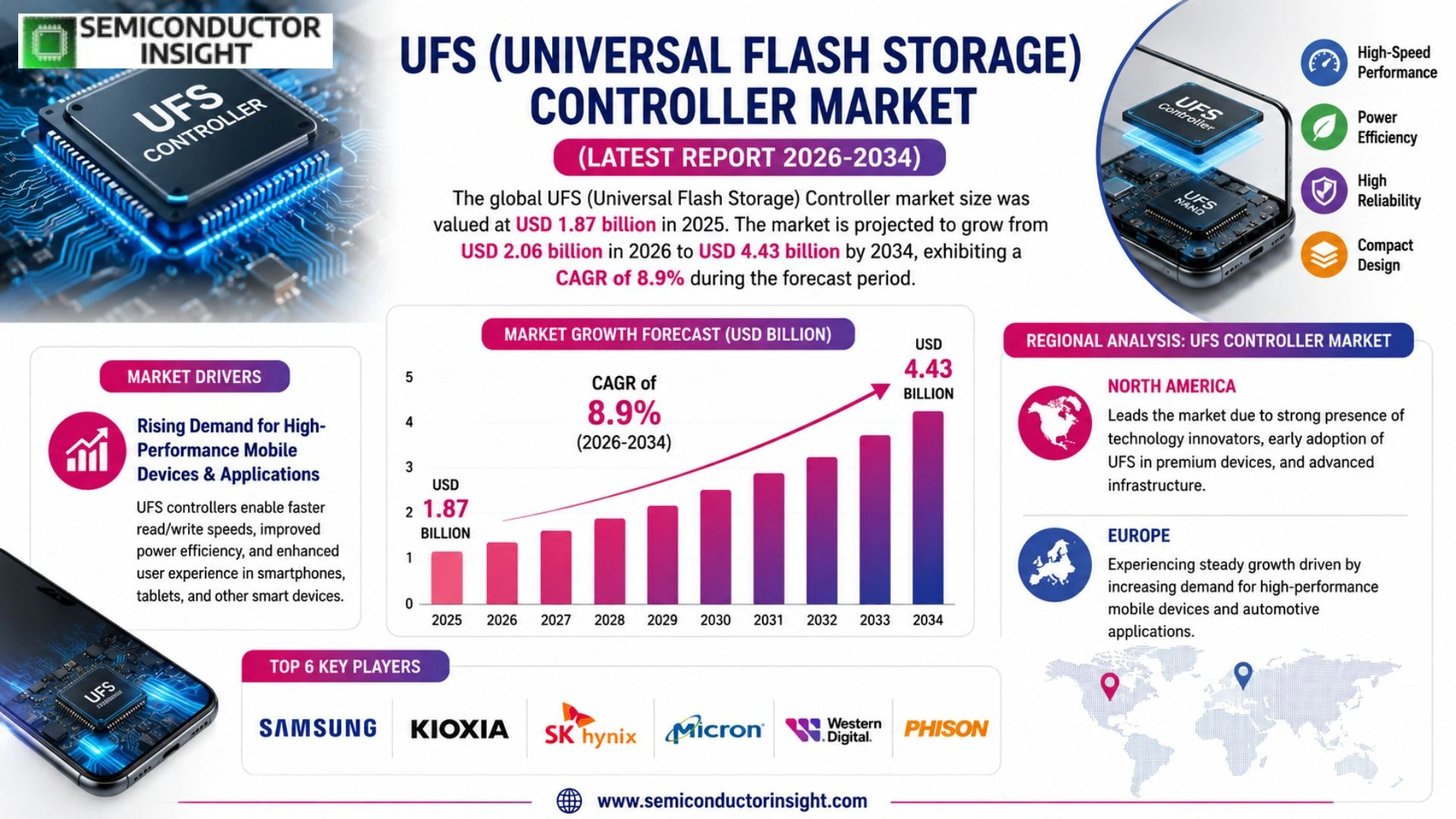

UFS (Universal Flash Storage) Controller Market size was valued at USD 1.87 billion in 2025. The market is projected to grow from USD 2.06 billion in 2026 to USD 4.43 billion by 2034, exhibiting a CAGR of 8.9% during the forecast period.

UFS controllers are specialized semiconductor chips that manage data transfer between the host processor and NAND flash memory in UFS-based storage solutions. These controllers govern critical operations including error correction, wear leveling, data encryption, and high-speed serial interface management, supporting the JEDEC UFS standard across versions such as UFS 2.x, UFS 3.x, and the more recent UFS 4.0, which delivers sequential read speeds of up to 4,200 MB/s.

The market is witnessing strong momentum driven by the widespread adoption of UFS storage in smartphones, automotive infotainment systems, and industrial IoT devices. The rapid rollout of 5G-enabled smartphones has significantly elevated demand for high-performance flash storage solutions, as UFS controllers offer considerably faster data throughput compared to legacy eMMC alternatives. Furthermore, automotive applications are emerging as a high-growth vertical, with UFS 3.1 and UFS 4.0 controllers increasingly deployed in advanced driver-assistance systems (ADAS) and in-vehicle infotainment platforms. Key players operating in the UFS Controller market include Samsung Semiconductor, Silicon Motion Technology, Phison Electronics, Synopsys, and Cadence Design Systems, each maintaining competitive portfolios across the evolving UFS controller landscape.

MARKET DRIVERS

Surging Smartphone Adoption and Premium Device Demand Fueling UFS Controller Growth

UFS (Universal Flash Storage) Controller Market is experiencing robust expansion, primarily driven by the rapid proliferation of smartphones and high-performance consumer electronics. As original equipment manufacturers increasingly integrate UFS 3.1 and UFS 4.0 storage interfaces into flagship and mid-range devices, demand for advanced controller chips has accelerated significantly. The transition away from older eMMC-based architectures toward UFS solutions continues to gain momentum, as UFS controllers deliver substantially higher sequential read and write speeds critical for modern mobile applications, gaming, and AI-driven workloads.

5G Network Expansion and Advanced Mobile Computing Amplifying Storage Controller Requirements

The global rollout of 5G infrastructure is acting as a significant catalyst for the UFS controller market. As 5G-enabled devices generate and process increasingly large volumes of data in real time, the need for high-bandwidth, low-latency flash storage solutions has intensified. UFS controllers, capable of supporting multi-lane operation and high queue depths, are well-positioned to meet these evolving requirements. Device manufacturers across Asia-Pacific and North America are actively incorporating next-generation UFS controller architectures to ensure their platforms remain competitive in a rapidly evolving connectivity landscape.

➤ The widespread adoption of UFS 4.0-based controllers in flagship Android smartphones, offering sequential read speeds exceeding 4,200 MB/s, underscores the critical role of UFS controller innovation in sustaining mobile performance benchmarks.

Beyond smartphones, the automotive electronics and industrial IoT segments are emerging as meaningful secondary drivers for the UFS controller market. Advanced driver-assistance systems (ADAS), in-vehicle infotainment platforms, and connected industrial devices increasingly require reliable, high-speed embedded storage, and UFS controllers are proving to be a technically viable and scalable solution across these diverse end-use categories.

MARKET CHALLENGES

Technical Complexity in UFS Controller Design Posing Significant Engineering Challenges

Despite strong market momentum, UFS (Universal Flash Storage) Controller Market faces considerable technical challenges related to the design and validation of next-generation controller silicon. Developing controllers compatible with the latest JEDEC UFS 4.0 and upcoming UFS 5.0 specifications demands substantial R&D investment, advanced process node expertise, and rigorous firmware development capabilities. Smaller semiconductor companies face barriers in competing with established players that possess deep intellectual property portfolios and longstanding relationships with NAND flash manufacturers, creating an uneven competitive landscape.

Other Challenges

Supply Chain Volatility and NAND Flash Market Interdependence

The UFS controller market is closely tied to the cyclical nature of the global NAND flash memory industry. Periods of NAND oversupply or shortage directly influence controller procurement strategies among device OEMs, creating demand unpredictability for controller vendors. Additionally, geopolitical tensions affecting semiconductor supply chains and advanced packaging capacity constraints continue to introduce procurement risk and lead time variability across the value chain.

Power Consumption and Thermal Management in Compact Form Factors

As UFS controllers are increasingly deployed in thermally constrained environments such as ultra-thin smartphones and wearables, managing power efficiency without compromising throughput performance remains a persistent engineering challenge. Balancing active power draw, standby consumption, and thermal dissipation within tight physical envelopes requires continuous innovation in controller architecture and advanced low-power design methodologies, adding to overall development complexity and time-to-market pressure.

MARKET RESTRAINTS

High Development Costs and Consolidation Among NAND Vendors Limiting Market Participation

One of the foremost restraints UFS (Universal Flash Storage) Controller Market is the high cost associated with controller development, particularly as specifications advance toward UFS 4.0 and beyond. Tape-out costs on advanced process nodes, combined with the extensive validation cycles required by major OEM customers, create significant capital requirements that limit the number of viable independent controller suppliers. This consolidation dynamic favors vertically integrated NAND manufacturers , such as Samsung, SK Hynix, and Kioxia , that develop controllers in-house, potentially constraining opportunities for dedicated fabless controller companies.

Prolonged Device Replacement Cycles and Market Saturation in Mature Smartphone Segments

Slowing smartphone unit growth in mature markets such as Western Europe and North America represents a structural restraint on near-term UFS controller demand. As consumers extend device replacement cycles and overall handset shipment growth moderates, the volume uplift that historically accompanied each generational transition in mobile storage standards has become less pronounced. While premium tier devices continue to adopt the latest UFS controller generations, the broader mid-range and entry-level segments exhibit more conservative upgrade trajectories, tempering the overall volume opportunity for high-end controller solutions in the short to medium term.

MARKET OPPORTUNITIES

Automotive and Industrial IoT Sectors Opening Substantial New Addressable Markets for UFS Controllers

The expanding deployment of UFS-based storage in automotive and industrial applications represents one of the most compelling long-term opportunities for the UFS controller market. The automotive segment, in particular, is transitioning toward UFS solutions qualified under AEC-Q100 standards for use in ADAS, digital cockpit systems, and over-the-air update infrastructure. As vehicle architectures grow more software-defined and data-intensive, the performance and reliability characteristics of UFS controllers make them highly suitable for these demanding environments, opening a diversified revenue stream beyond consumer electronics.

UFS 4.0 Adoption Wave and Emerging UFS 5.0 Standardization Creating Technology Upgrade Cycles

The ongoing industry transition to UFS 4.0, with its doubled bandwidth compared to UFS 3.1, is creating a meaningful technology upgrade cycle across smartphone OEMs and consumer electronics manufacturers. Controller vendors that have successfully brought UFS 4.0-compliant solutions to market are well-positioned to capture design wins in the current device generation. Simultaneously, early standardization work around UFS 5.0 is expected to generate fresh investment in next-generation controller R&D, providing technology-forward suppliers with an opportunity to establish early ecosystem partnerships and secure long-term supply agreements with leading device manufacturers across global markets.

AI-Integrated Edge Devices and Wearable Technology Driving Incremental UFS Controller Demand

The proliferation of on-device artificial intelligence capabilities in smartphones, AR/VR headsets, and advanced wearables is generating incremental demand for high-performance UFS controller solutions. AI inference workloads at the edge require rapid model loading, high random read performance, and sustained write endurance , attributes intrinsic to well-designed UFS controllers. As semiconductor companies and device OEMs invest in purpose-built AI edge platforms, the UFS controller market stands to benefit from a new wave of storage performance requirements that align closely with the technical strengths of the latest UFS controller generations.

Trends

Rising Adoption of UFS 4.0 Standard Reshaping the UFS Controller Landscape

UFS (Universal Flash Storage) Controller Market is undergoing a significant technological shift as device manufacturers and chipmakers accelerate the transition toward UFS 4.0, the latest iteration of the JEDEC UFS standard. UFS 4.0 delivers sequential read speeds of up to 4,200 MB/s, representing a substantial leap over its predecessors and enabling next-generation performance in flagship smartphones, automotive platforms, and industrial-grade embedded systems. As original equipment manufacturers prioritize higher data throughput and lower power consumption in their designs, the demand for advanced UFS controllers compatible with UFS 4.0 continues to intensify across multiple end-use verticals.

Other Trends

5G Smartphone Proliferation Driving High-Performance Flash Storage Demand

The rapid global rollout of 5G networks has emerged as a key demand driver for UFS (Universal Flash Storage) Controller Market. Fifth-generation smartphones require significantly faster internal storage to handle the increased data rates, higher-resolution media, and multitasking workloads associated with 5G connectivity. UFS controllers offer considerably superior data throughput compared to legacy eMMC alternatives, making them the preferred choice among leading smartphone OEMs. This trend has pushed key players such as Samsung Semiconductor, Silicon Motion Technology, and Phison Electronics to expand and refine their UFS controller portfolios to meet evolving device requirements.

Automotive Applications Emerging as a High-Growth Vertical

Automotive platforms are increasingly adopting UFS 3.1 and UFS 4.0 controllers within advanced driver-assistance systems (ADAS) and in-vehicle infotainment systems. The automotive sector demands storage solutions that combine high-speed data access with reliability under extreme temperature and vibration conditions. UFS controllers address these requirements effectively, positioning UFS (Universal Flash Storage) Controller Market for robust expansion within the automotive electronics segment as vehicle electrification and autonomous driving features become more mainstream across global automotive production lines.

Industrial IoT Deployments Broadening the UFS Controller Application Base

Beyond consumer electronics and automotive platforms, industrial Internet of Things (IoT) deployments are contributing to the expanding footprint of UFS (Universal Flash Storage) Controller Market. Industrial IoT devices increasingly require compact, high-performance, and durable storage solutions capable of sustained read and write operations in demanding environments. UFS controllers, with their robust error correction, wear leveling, and data encryption capabilities, are well-suited to meet these industrial-grade requirements. Companies such as Synopsys and Cadence Design Systems are actively supporting this trend by offering IP and design solutions that facilitate UFS controller integration across diverse embedded and connected device architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

UFS Controller Market , Competitive Dynamics and Leading Semiconductor Innovators

Global UFS (Universal Flash Storage) Controller Market is characterized by a concentrated yet progressively competitive landscape, with a handful of well-established semiconductor companies commanding significant market share. Samsung Semiconductor stands out as the dominant force, leveraging its vertically integrated capabilities in both NAND flash manufacturing and controller design to deliver tightly optimized UFS storage solutions across UFS 2.x, UFS 3.x, and the high-performance UFS 4.0 standard, which supports sequential read speeds of up to 4,200 MB/s. Silicon Motion Technology and Phison Electronics have similarly entrenched their positions as leading fabless controller specialists, supplying UFS controller intellectual property and silicon to a broad base of OEMs and module manufacturers serving the smartphone, automotive, and industrial IoT segments. The rapid proliferation of 5G-enabled devices and the surge in demand for advanced driver-assistance systems (ADAS) have further intensified competitive investment in next-generation UFS controller architectures, compelling all major players to accelerate their product roadmaps.

Beyond the top-tier players, the UFS Controller market features a set of strategically significant participants operating across IP licensing, controller chip design, and verification tooling. Synopsys and Cadence Design Systems play a pivotal role by providing UFS controller IP cores and protocol verification environments that enable semiconductor companies and system-on-chip designers to integrate JEDEC-compliant UFS interfaces efficiently. Marvell Technology and Kioxia have also maintained notable positions by developing proprietary UFS controller solutions tailored to enterprise and mobile storage applications. Meanwhile, emerging and regional competitors such as Shenzhen BIWIN Storage Technology and Longsys are expanding their UFS controller portfolios to address the growing demand within China’s domestic smartphone and automotive supply chains, reflecting the increasingly global nature of competition in this market.

List of Key UFS Controller Companies Profiled

- Samsung Semiconductor

- Silicon Motion Technology Corporation

- Phison Electronics Corporation

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Marvell Technology, Inc.

- Kioxia Holdings Corporation

- SK Hynix Inc.

- Micron Technology, Inc.

- Western Digital Corporation

- Shenzhen BIWIN Storage Technology Co., Ltd.

- Longsys Electronics Co., Ltd.

- Greenliant Systems

- Apex Microelectronics Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

UFS 4.0 Controllers represent the most advanced and rapidly gaining segment within the UFS controller market, driven by their exceptional sequential read capabilities and superior data throughput compared to previous generations.

|

| By Application |

|

Smartphones and Mobile Devices constitute the dominant application segment for UFS controllers, underpinned by the global proliferation of 5G-capable handsets that demand high-speed, reliable flash storage solutions.

|

| By End User |

|

Consumer Electronics Manufacturers represent the largest end-user segment, as major smartphone OEMs and tablet makers continue to integrate high-performance UFS controllers across their product portfolios to meet escalating user expectations for device responsiveness and app loading speeds.

|

| By Interface Standard |

|

JEDEC UFS Standard Controllers dominate this segment, as broad industry alignment with the JEDEC UFS standard ensures interoperability across a wide range of host processors and storage modules, making it the preferred choice for both consumer and commercial-grade product development.

|

| By Feature Capability |

|

Controllers with Advanced Error Correction (ECC) lead this segment, as the growing density of NAND flash cells in modern storage solutions has made robust error correction an indispensable capability for ensuring data integrity across the product lifetime.

|

Regional Analysis: UFS (Universal Flash Storage) Controller Market

Asia-Pacific

Asia-Pacific’s dominance in the UFS Controller Market is deeply rooted in its vertically integrated semiconductor supply chains. The region hosts the majority of global NAND flash fabrication capacity, enabling controller developers to co-optimize firmware and hardware with memory vendors. This proximity between controller designers and memory manufacturers accelerates product qualification cycles and enhances time-to-market advantages unavailable in other regions.

The Asia-Pacific region generates the world’s highest volume of smartphones, tablets, and wearable devices , all primary end-use platforms for UFS controllers. Rapid upgrade cycles among urban consumers in China, India, and Southeast Asia sustain continuous demand for next-generation UFS solutions. OEM brands headquartered across the region consistently specify the latest UFS controller standards to differentiate flagship product lines.

National semiconductor strategies across China, South Korea, Taiwan, and India are channeling substantial resources into domestic chip design and fabrication capabilities. These policies directly benefit UFS controller developers by funding R&D infrastructure, reducing import dependence, and incentivizing local adoption. Regulatory frameworks increasingly favor homegrown UFS controller intellectual property, reinforcing the region’s long-term competitive positioning in the global market.

Beyond mobile devices, Asia-Pacific is witnessing accelerating UFS controller adoption in automotive infotainment systems, AI edge devices, and industrial automation platforms. Japanese and South Korean automotive suppliers are integrating UFS controllers into advanced driver-assistance systems, while Chinese AI hardware developers leverage UFS architectures for compact, high-throughput storage in embedded inference platforms, broadening the regional market scope considerably.

North America

North America represents one of the most technologically advanced and innovation-driven regions within the global UFS Controller Market. The United States hosts a significant proportion of leading fabless semiconductor design firms that contribute foundational intellectual property to UFS controller architectures, protocol optimization, and security feature development. Strong enterprise and data center demand further shapes the regional market, as UFS-based storage solutions extend into edge computing and ruggedized industrial applications. The presence of major cloud hyperscalers and technology conglomerates creates a pull effect for premium UFS controller solutions capable of supporting high-throughput workloads. Canada’s growing semiconductor design ecosystem adds supplementary capacity to the regional talent pool. North American regulatory emphasis on supply chain security and data sovereignty is prompting OEMs to diversify their UFS controller sourcing strategies, opening opportunities for domestically designed controller solutions. The region’s automotive sector, particularly EV manufacturers integrating advanced digital cockpit systems, is also emerging as a meaningful growth avenue for UFS controller adoption through the forecast horizon of 2034.

Europe

Europe’s position in the UFS Controller Market is characterized by its strengths in automotive-grade electronics, industrial applications, and high-reliability embedded systems. Germany, in particular, serves as a pivotal market where automotive OEMs and Tier-1 suppliers are transitioning legacy storage architectures toward UFS controller-based solutions to support next-generation ADAS, digital instrument clusters, and in-vehicle infotainment platforms. The European Union’s strategic initiatives to strengthen regional semiconductor manufacturing capabilities , most notably through the European Chips Act , are gradually fostering a more self-reliant UFS controller ecosystem. France, the Netherlands, and Sweden contribute meaningful semiconductor IP and embedded software expertise that supports UFS controller integration across specialized industrial and medical device markets. European data protection regulations and functional safety standards such as ISO 26262 are influencing the development of UFS controllers that meet stringent qualification and compliance benchmarks, effectively differentiating European-grade solutions in the global competitive landscape.

South America

South America occupies an emerging position in the global UFS Controller Market, with growth primarily driven by expanding smartphone penetration, increasing digitization across Brazil and Mexico, and gradual modernization of consumer electronics retail infrastructure. Brazil, as the region’s largest economy, anchors demand for mid-range and affordable smartphones equipped with UFS-based storage, as cost-conscious OEMs seek to deliver improved user experiences without significant price premiums. Local assembly operations supported by government tax incentive programs are beginning to incorporate UFS controller-equipped modules into domestically sold devices. While South America currently lacks indigenous UFS controller design capabilities, regional importers and distributors of UFS-enabled devices are proliferating. The gradual rollout of higher-speed mobile networks across urban centers is also catalyzing consumer appetite for storage-intensive applications, indirectly reinforcing demand for advanced UFS controller solutions sourced from global manufacturers and distributed through the region’s growing electronics retail channels.

Middle East & Africa

The Middle East and Africa region represents a nascent but progressively significant frontier in the global UFS Controller Market. Rapid mobile network infrastructure expansion across Gulf Cooperation Council countries, Nigeria, South Africa, and Kenya is driving demand for smartphones and connected devices equipped with capable UFS storage solutions. The UAE and Saudi Arabia, bolstered by ambitious national digital transformation agendas, are prioritizing smart city projects, AI-driven public services, and advanced consumer electronics ecosystems , all of which create indirect demand for UFS controller-enabled devices. Africa’s youthful and digitally engaged population continues to drive volume demand for affordable smartphones, pushing manufacturers to adopt cost-optimized UFS controller designs that balance performance with price sensitivity. While the region does not yet host significant UFS controller manufacturing activity, strategic investments in electronics assembly and technology parks across Israel, the UAE, and South Africa suggest a gradual progression toward deeper integration within the global UFS Controller Market value chain over the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the UFS (Universal Flash Storage) Controller Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of UFS (Universal Flash Storage) Controller Market?

-> Global UFS (Universal Flash Storage) Controller Market was valued at USD 1.87 billion in 2025 and is projected to grow from USD 2.06 billion in 2026 to USD 4.43 billion by 2034, exhibiting a CAGR of 8.9% during the forecast period.

Which key companies operate UFS (Universal Flash Storage) Controller Market?

-> Key players include Samsung Semiconductor, Silicon Motion Technology, Phison Electronics, Synopsys, and Cadence Design Systems, among others.

What are the key growth drivers?

-> Key growth drivers include widespread adoption of UFS storage in smartphones, rapid rollout of 5G-enabled devices, growing automotive infotainment and ADAS applications, and rising demand from industrial IoT devices. UFS controllers offer significantly faster data throughput compared to legacy eMMC alternatives, further accelerating adoption.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by strong consumer electronics manufacturing and 5G deployment, while North America remains a significant market supported by automotive technology and semiconductor innovation.

What are the emerging trends?

-> Emerging trends include adoption of UFS 4.0 delivering sequential read speeds of up to 4,200 MB/s, deployment of UFS 3.1 and UFS 4.0 controllers in ADAS platforms, integration of advanced error correction and data encryption features, and expanding use of UFS solutions in automotive in-vehicle infotainment systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...