Thermal Infrared (IR) Bolometer Market Insights

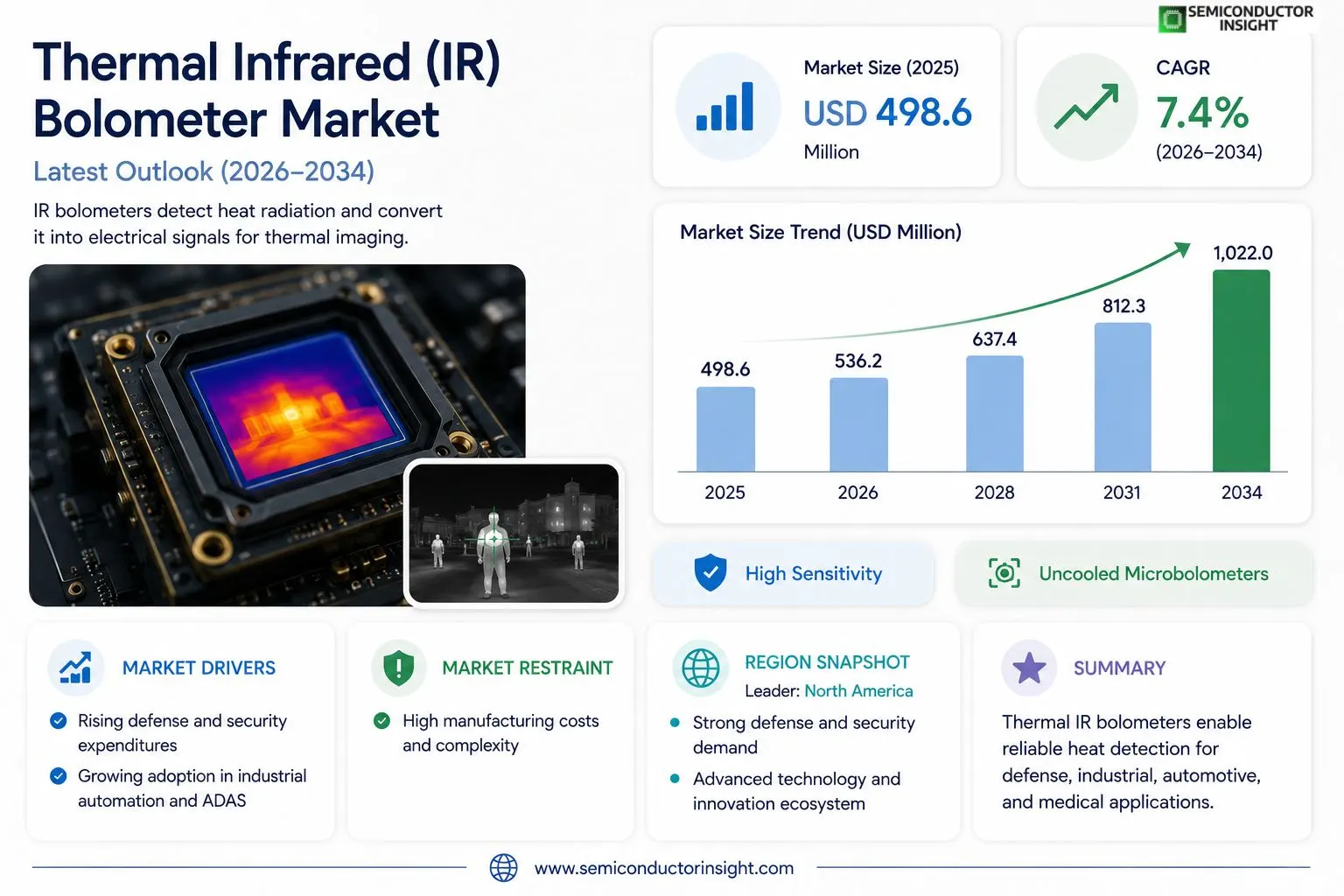

Global Thermal Infrared (IR) Bolometer market size was valued at USD 498.6 million in 2025. The market is projected to grow from USD 536.2 million in 2026 to USD 1.02 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period.

Thermal infrared bolometers are highly sensitive radiation detectors that measure the power of incident electromagnetic radiation by absorbing the radiation and converting it into a measurable change in electrical resistance. These devices operate across the infrared spectrum and are widely used in applications including thermal imaging, night vision systems, surveillance, medical diagnostics, and scientific instrumentation. Key product types include uncooled microbolometers and cooled bolometers, with uncooled variants gaining significant traction due to their compact size, lower cost, and ease of integration.

The market is witnessing robust growth driven by rising defense and security expenditures, growing adoption of thermal cameras in industrial automation, and expanding use of IR sensing technologies in the automotive sector for advanced driver assistance systems (ADAS). Furthermore, increasing deployment in border surveillance and firefighting applications continues to broaden demand. FLIR Systems (now part of Teledyne Technologies), Leonardo DRS, and Lynred are among the prominent players operating in this market with diversified and technologically advanced product portfolios.

MARKET DRIVERS

Rising Defense and Security Expenditure Accelerating Demand for Thermal Infrared Bolometer Systems

Thermal Infrared (IR) Bolometer Market is experiencing robust growth driven primarily by escalating defense budgets across North America, Europe, and Asia-Pacific. Governments worldwide are increasingly investing in advanced night-vision systems, border surveillance, and soldier modernization programs that rely on uncooled thermal infrared bolometer technology. The ability of bolometer-based sensors to detect heat signatures without requiring cryogenic cooling makes them operationally superior and cost-effective for military field deployment. Nations are procuring thermal imaging systems at an accelerated pace, citing the need to counter asymmetric threats and improve situational awareness in complex battlefield environments.

Expanding Commercial and Industrial Applications Broadening the Thermal IR Bolometer Addressable Market

Beyond defense, the thermal infrared bolometer market is witnessing strong adoption across commercial verticals including building energy audits, predictive maintenance in manufacturing, automotive driver-assistance systems, and medical thermography. Industrial facilities are leveraging bolometer-enabled thermal cameras to identify electrical faults, insulation failures, and equipment overheating before costly breakdowns occur. In the automotive sector, original equipment manufacturers are integrating uncooled IR bolometer sensors into advanced driver-assistance systems (ADAS) to enhance pedestrian detection in low-visibility conditions. This broadening application base is a significant structural driver sustaining long-term market expansion.

➤ The convergence of miniaturization in microelectromechanical systems (MEMS) technology and advances in vanadium oxide (VOx) and amorphous silicon (a-Si) detector materials has substantially lowered production costs for uncooled thermal IR bolometers, making them accessible to a wider range of end-use industries.

The proliferation of smart infrastructure and the Internet of Things (IoT) is further propelling Thermal Infrared (IR) Bolometer Market, as connected thermal sensors are increasingly embedded in smart buildings for occupancy detection, fire prevention, and HVAC optimization. The steady decline in per-unit cost of uncooled bolometer arrays, combined with improvements in pixel resolution and thermal sensitivity (NETD), continues to attract new end-users who previously found thermal imaging economically prohibitive.

MARKET CHALLENGES

High Development Costs and Technical Complexity Posing Barriers for New Entrants in Thermal IR Bolometer Market

Despite favorable growth dynamics, Thermal Infrared (IR) Bolometer Market faces considerable challenges related to the high capital investment required for wafer-level fabrication, cleanroom infrastructure, and specialized MEMS processing equipment. Developing high-performance bolometer arrays with low noise-equivalent temperature difference (NETD) and uniform pixel response demands significant R&D expenditure, which creates substantial barriers to entry for smaller manufacturers. Additionally, achieving consistent yield rates in volume production remains technically demanding, contributing to elevated per-unit costs that can restrict adoption in highly price-sensitive application segments.

Other Challenges

Export Control Regulations and Trade Compliance

Thermal infrared bolometer technology is classified as a dual-use item subject to stringent export control regimes including the Wassenaar Arrangement and U.S. Export Administration Regulations (EAR). Manufacturers face complex compliance obligations when exporting bolometer-based systems to foreign customers, particularly in defense and aerospace sectors. Navigating these regulatory frameworks increases administrative overhead, lengthens sales cycles, and can limit market access in certain geographies, acting as a meaningful commercial constraint for globally-oriented suppliers.

Competition from Alternative Thermal Sensing Technologies

Thermal IR Bolometer Market contends with competition from alternative sensing modalities such as cooled photon detectors, thermopile arrays, and pyroelectric sensors in specific use cases. Cooled infrared detectors continue to outperform uncooled bolometers in high-sensitivity, long-range surveillance applications, limiting bolometer penetration in premium defense segments. Manufacturers must continuously invest in pixel-pitch reduction and sensitivity improvements to defend market share against these competing technologies.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Raw Material Dependencies Constraining Thermal IR Bolometer Market Growth

Thermal Infrared (IR) Bolometer Market is restrained by dependencies on specialized raw materials and semiconductor-grade substrates used in the fabrication of resistive bolometer elements. Vanadium oxide and amorphous silicon, the two dominant detector materials, require tightly controlled deposition processes and high-purity precursors that are sourced from a limited number of qualified suppliers globally. Disruptions in semiconductor supply chains, as demonstrated during recent global chip shortages, can delay production schedules and inflate input costs for bolometer manufacturers, ultimately affecting product availability and delivery timelines for end customers.

Limited Pixel Resolution Compared to Visible-Light Sensors Restricting High-Definition Application Penetration

While uncooled thermal infrared bolometer technology has advanced significantly, the achievable pixel resolution of commercial bolometer focal plane arrays (FPAs) still lags behind visible-light image sensors. For applications requiring fine spatial detail,such as long-range aerial reconnaissance or high-precision industrial inspection,this resolution gap remains a functional restraint. The physics of long-wave infrared diffraction imposes inherent limitations on pixel pitch miniaturization, making it challenging to match the megapixel densities routinely available in conventional optical cameras. This technical ceiling moderates the addressable market for premium bolometer-based imaging in resolution-critical applications.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning Creating Transformative Growth Opportunities in Thermal IR Bolometer Market

The integration of artificial intelligence (AI) and machine learning (ML) algorithms with thermal infrared bolometer imaging systems presents one of the most significant growth opportunities in the market. AI-powered image processing can compensate for the inherent resolution limitations of bolometer FPAs through super-resolution techniques, enhance target detection accuracy, and enable real-time automated threat identification in security and surveillance deployments. System integrators and end-users are actively seeking bolometer-enabled smart thermal cameras capable of edge computing, driving demand for higher-value, software-enriched product offerings that command improved margins for manufacturers.

Emerging Demand from Healthcare, Autonomous Vehicles, and Smart City Infrastructure Unlocking New Revenue Streams

Thermal Infrared (IR) Bolometer Market stands at the threshold of substantial expansion into next-generation application domains. In healthcare, contactless fever screening and vascular imaging applications are driving procurement of compact bolometer modules in clinical and public health settings. The autonomous vehicle industry represents a compelling long-term opportunity, as thermal bolometer sensors can detect pedestrians, animals, and road hazards in complete darkness and adverse weather conditions where visible-light cameras and lidar performance degrades. Concurrently, smart city initiatives across Asia-Pacific, the Middle East, and Europe are deploying thermal imaging networks for traffic management, public safety monitoring, and energy efficiency programs, collectively representing a substantial and growing incremental demand base for the thermal infrared bolometer market.

Trends

Rising Defense and Security Expenditures Fueling Demand for Thermal Infrared Bolometer Technologies

One of the most prominent trends shaping Thermal Infrared (IR) Bolometer Market is the sustained increase in defense and security spending across both developed and emerging economies. Governments worldwide are prioritizing advanced surveillance, border protection, and situational awareness capabilities, driving procurement of high-performance thermal imaging systems that rely on bolometer-based sensors. Thermal Infrared (IR) Bolometer Market has benefited considerably from the integration of these detectors into night vision equipment, perimeter monitoring platforms, and airborne reconnaissance systems deployed by military forces globally. As geopolitical tensions persist, demand for reliable infrared detection solutions is expected to remain a key growth catalyst throughout the forecast period.

Other Trends

Uncooled Microbolometer Adoption Gaining Significant Traction

Within Thermal Infrared (IR) Bolometer Market, uncooled microbolometers are emerging as the preferred technology over their cooled counterparts. Their compact form factor, lower manufacturing cost, and simplified integration requirements make them highly attractive for commercial and industrial applications. Industries ranging from building diagnostics to automotive safety systems are increasingly deploying uncooled variants, broadening the addressable market considerably beyond traditional defense use cases.

Expansion in Automotive ADAS Applications

The automotive sector represents a rapidly growing end-use segment for Thermal Infrared (IR) Bolometer Market. As vehicle manufacturers accelerate the integration of Advanced Driver Assistance Systems (ADAS), infrared bolometer sensors are being incorporated to enhance pedestrian detection, collision avoidance, and low-visibility driving capabilities. This trend is reinforcing demand for miniaturized, cost-effective bolometer modules that can be seamlessly embedded into next-generation vehicle architectures.

Industrial Automation and Predictive Maintenance Use Cases

Growing adoption of thermal cameras within industrial automation environments is another defining trend in Thermal Infrared (IR) Bolometer Market. Manufacturers are leveraging bolometer-based thermal imaging for real-time equipment monitoring, predictive maintenance, and quality control processes. This shift toward smart manufacturing is expanding the commercial footprint of IR bolometer technologies beyond historically dominant defense and scientific instrumentation verticals.

Firefighting and Border Surveillance Broadening Market Demand

Deployment of thermal infrared bolometer systems in firefighting operations and border surveillance missions continues to widen Thermal Infrared (IR) Bolometer Market’s demand base. First responders rely on bolometer-equipped thermal imagers to detect heat signatures through smoke and low-visibility conditions, improving operational safety. Simultaneously, border security agencies across multiple regions are deploying fixed and mobile infrared surveillance platforms incorporating bolometer sensors, further diversifying application areas and supporting sustained market expansion. Leading industry participants including FLIR Systems, now part of Teledyne Technologies, Leonardo DRS, and Lynred continue to advance product portfolios to address these evolving requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Thermal Infrared (IR) Bolometer Market: Competitive Dynamics and Leading Manufacturer Profiles

Global Thermal Infrared (IR) Bolometer market is characterized by a moderately consolidated competitive landscape, with a handful of technologically advanced players commanding significant market share. Teledyne FLIR (formerly FLIR Systems, acquired by Teledyne Technologies) stands as the dominant force in the market, leveraging its extensive portfolio of uncooled microbolometer-based thermal cameras and sensors across defense, industrial, and commercial segments. The company’s deep integration across the value chain , from detector fabrication to end-system delivery , provides a substantial competitive moat. Lynred (formerly Sofradir and CEA-Leti’s ULIS), a leading European detector manufacturer, is another key incumbent, supplying high-performance uncooled and cooled bolometer arrays to OEMs worldwide. Leonardo DRS, a subsidiary of Leonardo S.p.A., maintains a strong foothold particularly in defense-grade cooled and uncooled IR detector solutions. The competitive intensity is further amplified by significant R&D investment among players to enhance detector sensitivity, reduce noise equivalent temperature difference (NETD), and miniaturize sensor form factors for ADAS and consumer applications.

Beyond the tier-one players, a number of specialized and regionally significant manufacturers contribute to the competitive fabric of Thermal IR Bolometer Market. BAE Systems and L3Harris Technologies maintain established positions in defense-centric bolometer systems, while Axis Communications and Opgal Optronic Industries cater to commercial surveillance and security segments. Chinese manufacturers such as Guide Infrared (Wuhan Guide Infrared Co., Ltd.) and Dali Technology have gained considerable traction in Asia-Pacific and emerging markets, offering cost-competitive uncooled microbolometer solutions. IRay Technology, another China-based player, has rapidly expanded its global footprint with a broad range of thermal imaging modules. ULIS (now integrated into Lynred) and Xenics (Belgium) address niche scientific and industrial sensing requirements, while Seek Thermal and Opgal serve growing consumer and professional thermal imaging segments. Collectively, these players are intensifying competition through product differentiation, strategic partnerships, and geographic expansion across North America, Europe, and Asia-Pacific.

List of Key Thermal Infrared (IR) Bolometer Companies Profiled

- Teledyne FLIR (Teledyne Technologies)

- Lynred

- Leonardo DRS

- BAE Systems

- L3Harris Technologies

- Guide Infrared (Wuhan Guide Infrared Co., Ltd.)

- IRay Technology Co., Ltd.

- Dali Technology

- Xenics

- Seek Thermal

- Axis Communications

- Opgal Optronic Industries

- INO (Institut National d’Optique)

- Sierra-Olympic Technologies

- Raytheon Technologies (RTX Corporation)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Uncooled Microbolometers dominate Thermal IR Bolometer Market and continue to consolidate their leadership position across both commercial and defense applications.

|

| By Application |

|

Thermal Imaging & Surveillance represents the most expansive application segment, underpinned by persistent global demand for advanced security and monitoring infrastructure.

|

| By End User |

|

Defense & Military remains the anchor end-user segment for Thermal IR Bolometers, serving as the primary catalyst for technological advancement and large-scale procurement programs globally.

|

| By Technology |

|

Vanadium Oxide (VOx) Based technology holds the foremost position in the bolometer market, characterized by its mature manufacturing ecosystem and well-established performance credentials.

|

| By Detector Format |

|

Standard Format Arrays constitute the dominant detector format segment, offering a well-balanced combination of imaging capability, system integration flexibility, and cost efficiency that resonates broadly across the market.

|

Regional Analysis: Thermal Infrared (IR) Bolometer Market

North America

North America’s defense establishment remains the single largest consumer of thermal infrared bolometer systems, with demand driven by next-generation surveillance platforms, unmanned aerial vehicles, and soldier-worn systems. Continued modernization programs and allied defense cooperation agreements sustain a predictable and high-volume procurement cycle that underpins the region’s leadership in this specialized market segment.

Beyond defense, North American industries including oil and gas, electrical utilities, and manufacturing are integrating thermal infrared bolometer sensors into predictive maintenance and process monitoring workflows. The growing use of these sensors in smart building technologies and fire detection systems reflects a broadening commercial base that diversifies revenue streams and reduces the region’s reliance on defense-only demand cycles.

The United States hosts a dense concentration of university research centers, national laboratories, and technology incubators focused on advancing microbolometer array resolution, pixel miniaturization, and sensor integration. This innovation infrastructure consistently yields patent filings and technology licensing agreements that shape the competitive dynamics of Global Thermal Infrared (IR) Bolometer Market and attract sustained venture and institutional capital.

Robust export control frameworks and a mature domestic supply chain give North American manufacturers a strategic advantage in managing component availability and technology security. Established relationships between prime contractors and government procurement agencies create long-term visibility into demand, enabling manufacturers to invest confidently in capacity expansion and next-generation bolometer sensor development programs.

Europe

Europe represents a strategically significant region within Global Thermal Infrared (IR) Bolometer Market, underpinned by a combination of strong defense spending among NATO member states, progressive environmental monitoring mandates, and a well-developed industrial base in precision photonics and sensor technologies. Countries such as France, Germany, and the United Kingdom are at the forefront of both military and civilian thermal imaging applications, with national defense agencies actively funding next-generation bolometer sensor programs. The European Union’s emphasis on energy efficiency and building decarbonization has opened a substantial commercial pathway for thermal infrared technology in smart building diagnostics and grid infrastructure monitoring. Additionally, the region’s aerospace sector, which serves both civil and defense markets, is a growing consumer of high-performance bolometer sensors integrated into surveillance satellites and airborne reconnaissance platforms. European manufacturers are also investing in supply chain resilience initiatives to reduce strategic dependencies and ensure uninterrupted access to critical infrared detector components, strengthening the region’s competitive standing in Thermal Infrared (IR) Bolometer Market through 2034.

Asia-Pacific

Asia-Pacific is the fastest-growing region in Thermal Infrared (IR) Bolometer Market, propelled by escalating defense modernization programs, expanding industrial automation, and a rapidly maturing consumer electronics sector across key economies including China, Japan, South Korea, and India. China’s aggressive investment in domestic semiconductor and infrared sensor manufacturing has positioned it as both a major consumer and an increasingly competitive producer within this market. Japan and South Korea contribute through advanced materials research and high-precision manufacturing capabilities that are critical to producing next-generation uncooled bolometer arrays. India’s growing defense procurement ambitions and border surveillance requirements are generating substantial demand for thermal infrared imaging systems. The region’s industrial sectors, including automotive, electronics manufacturing, and energy, are also adopting thermal infrared bolometer solutions for quality control and equipment monitoring, creating a diverse and resilient demand base that is expected to sustain strong momentum in Thermal Infrared (IR) Bolometer Market through the forecast horizon.

South America

South America occupies an emerging position in Global Thermal Infrared (IR) Bolometer Market, with demand primarily shaped by border security imperatives, natural resource management, and expanding public safety infrastructure. Brazil leads regional adoption, supported by government investment in surveillance systems for environmental monitoring of the Amazon basin and protection of extensive national borders. Colombia, Chile, and Argentina are also gradually increasing procurement of thermal infrared imaging systems for law enforcement and critical infrastructure protection. The region’s oil and gas sector presents a compelling growth avenue for bolometer sensor deployment in pipeline monitoring and leak detection applications. While budget constraints and infrastructure gaps temper the pace of adoption relative to more mature regions, the long-term outlook for Thermal Infrared (IR) Bolometer Market in South America remains constructive, supported by improving economic conditions and growing awareness of the operational efficiencies that thermal imaging technologies can deliver across multiple industry verticals.

Middle East & Africa

The Middle East and Africa region presents a distinctive demand profile for Thermal Infrared (IR) Bolometer Market, characterized by strong defense and security spending among Gulf Cooperation Council nations, coupled with emerging adoption in sub-Saharan Africa driven by border control and wildlife conservation applications. Countries such as Saudi Arabia, the United Arab Emirates, and Israel are significant consumers of advanced thermal infrared imaging systems, integrating bolometer-based sensors into military vehicles, naval vessels, and perimeter security installations. Israel, in particular, maintains a sophisticated domestic defense technology industry with notable expertise in thermal sensor miniaturization and system integration. In Africa, humanitarian organizations and conservation agencies are beginning to utilize thermal infrared bolometer technology for anti-poaching surveillance and disaster response operations, representing an unconventional but growing application segment. As regional governments continue to prioritize national security investments and infrastructure modernization, the Middle East and Africa are expected to register steady participation in Thermal Infrared (IR) Bolometer Market through 2034.

Report Scope

This market research report provides a comprehensive analysis of the Thermal Infrared (IR) Bolometer Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Thermal Infrared (IR) Bolometer Market?

-> Global Thermal Infrared (IR) Bolometer Market was valued at USD 498.6 million in 2025 and is expected to reach USD 1.02 billion by 2034, growing at a CAGR of 7.4% during the forecast period 2026–2034.

Which key companies operate in Thermal Infrared (IR) Bolometer Market?

-> Key players include FLIR Systems (now part of Teledyne Technologies), Leonardo DRS, and Lynred, among others, with diversified and technologically advanced product portfolios.

What are the key growth drivers?

-> Key growth drivers include rising defense and security expenditures, growing adoption of thermal cameras in industrial automation, and expanding use of IR sensing technologies in the automotive sector for advanced driver assistance systems (ADAS). Additionally, increasing deployment in border surveillance and firefighting applications continues to broaden demand.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market driven by strong defense and security investments.

What are the emerging trends?

-> Emerging trends include uncooled microbolometer adoption, integration of IR sensing in ADAS, expansion of thermal imaging in medical diagnostics, and growing use of compact bolometers in scientific instrumentation and night vision systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...