RF Sampling ADC (Direct RF) for SDR Market Insights

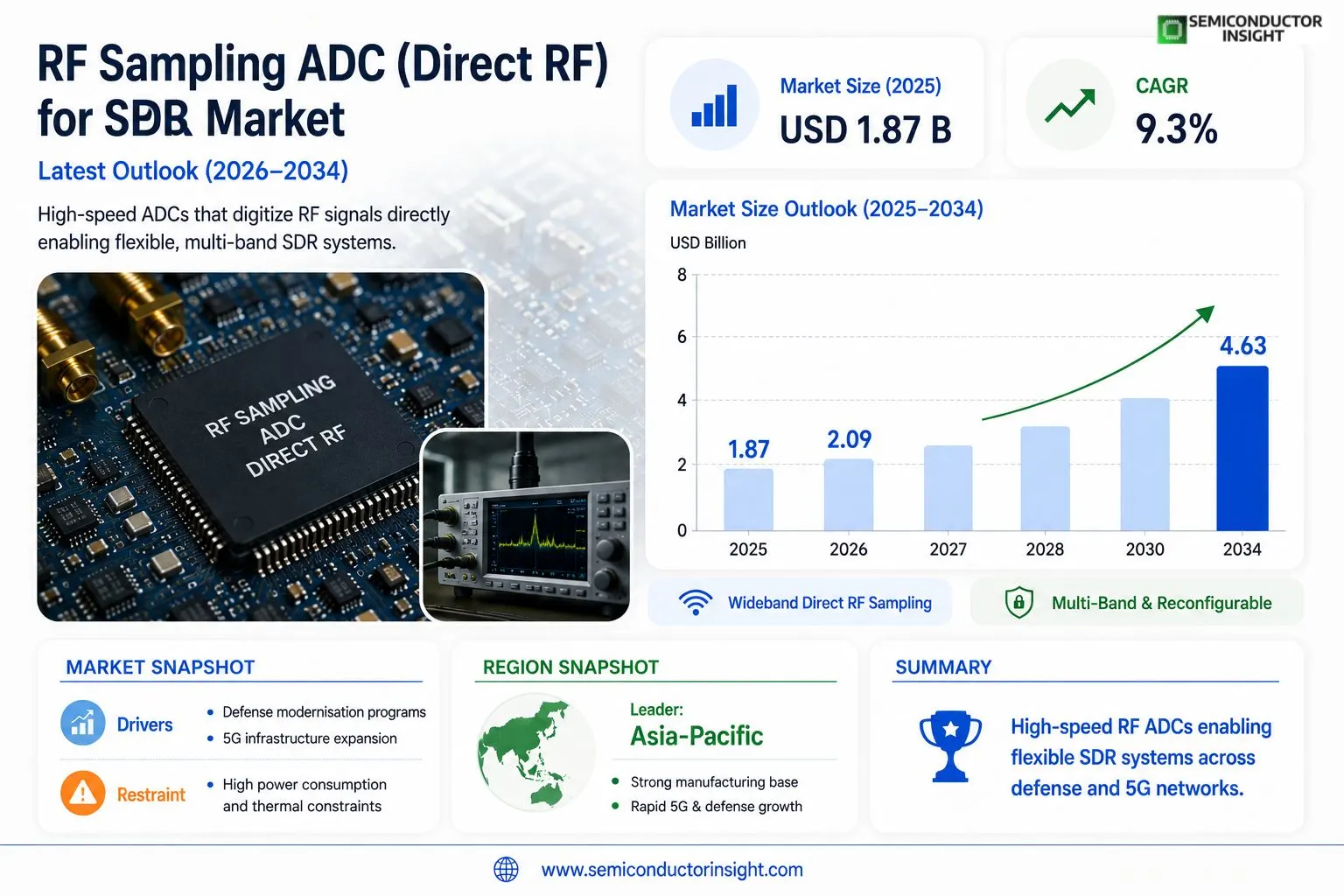

Global RF Sampling ADC (Direct RF) for SDR market size was valued at USD 1.87 billion in 2025. The market is projected to grow from USD 2.09 billion in 2026 to USD 4.63 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

RF Sampling ADCs, commonly referred to as Direct RF analog-to-digital converters, are high-speed semiconductor devices that enable direct digitization of radio frequency signals without the need for traditional intermediate frequency (IF) downconversion stages. These devices are fundamental to Software Defined Radio (SDR) architectures, where signal processing is performed digitally rather than through conventional analog hardware. The technology encompasses wideband RF sampling converters, multi-gigasample-per-second ADCs, and integrated RF data converter solutions supporting a broad range of frequency bands from HF through millimeter-wave spectrum.

The market is experiencing robust growth driven by escalating demand for flexible, reconfigurable radio platforms across defense, telecommunications, and aerospace sectors. The rapid global rollout of 5G infrastructure and the growing need for multi-band, multi-mode communication systems have significantly accelerated adoption of direct RF sampling architectures. Furthermore, increasing defense budgets worldwide , with U.S. defense spending exceeding USD 886 billion in fiscal year 2024 , continue to drive investment in advanced SDR platforms for electronic warfare, signals intelligence, and tactical communications. Key industry participants including Texas Instruments Inc., Analog Devices Inc., and Xilinx (AMD) are actively expanding their RF data converter portfolios to address the evolving needs of next-generation SDR deployments.

MARKET DRIVERS

Growing Adoption of Software-Defined Radio Architectures Across Defense and Telecommunications

RF Sampling ADC (Direct RF) for SDR Market is experiencing significant momentum driven by the accelerating shift from traditional superheterodyne radio architectures to fully digital, software-defined radio platforms. Defense agencies, telecommunications operators, and wireless infrastructure providers are increasingly deploying SDR systems that rely on high-speed, wideband RF sampling analog-to-digital converters capable of directly digitizing signals at radio frequencies. This architectural transition eliminates the need for multiple analog mixing and filtering stages, substantially reducing hardware complexity and enabling greater flexibility in waveform reconfiguration through software. The convergence of advanced CMOS fabrication processes with high-dynamic-range ADC design has made direct RF sampling increasingly viable across a wider range of frequency bands, including S-band, C-band, and emerging millimeter-wave segments.

Defense Modernization Programs and Multi-Mission Radio Requirements Fueling Demand

Government-led defense modernization initiatives across North America, Europe, and Asia-Pacific are among the most consequential demand drivers for RF Sampling ADC (Direct RF) for SDR Market. Military programs increasingly require radios capable of simultaneously handling communications, electronic warfare, radar sensing, and signals intelligence on a single hardware platform. Direct RF sampling ADCs enable this multi-mission capability by providing the instantaneous bandwidth and linearity required to process complex, densely packed signal environments. Programs such as the U.S. Army’s Integrated Tactical Network and NATO interoperability mandates are directly accelerating procurement of SDR platforms built around wideband RF sampling data converters. The ability to upgrade radio functionality through firmware and software updates , without hardware replacement , represents a compelling total cost of ownership advantage that defense procurement agencies increasingly prioritize.

➤ The transition from analog-heavy radio architectures to direct RF sampling platforms is fundamentally reshaping the SDR value chain, positioning high-speed ADC suppliers as critical enablers of next-generation wireless capability across both defense and commercial segments.

On the commercial side, Global rollout of 5G NR networks and the densification of small cell infrastructure are creating parallel demand streams for RF Sampling ADC (Direct RF) technology within base station and radio access network equipment. Massive MIMO antenna architectures, which require simultaneous digitization of signals across dozens of antenna elements, are pushing system designers toward highly integrated, power-efficient direct RF sampling solutions. Additionally, the emergence of open RAN (O-RAN) frameworks is incentivizing the disaggregation of radio hardware, further elevating the strategic importance of flexible, software-programmable RF front-end digitization enabled by advanced sampling ADC devices.

MARKET CHALLENGES

Power Consumption and Thermal Management Complexity in Wideband Direct RF Sampling Deployments

Despite its architectural advantages, RF Sampling ADC (Direct RF) for SDR Market faces substantial technical and operational challenges that continue to constrain broader adoption, particularly in size, weight, and power-sensitive (SWaP) applications. Direct RF sampling ADCs operating at multi-gigasample-per-second rates inherently consume significantly higher power than their narrowband, intermediate-frequency counterparts. This elevated power draw creates compounding thermal management challenges, especially in compact airborne, shipborne, and dismounted soldier radio platforms where passive or active cooling capacity is severely limited. Designers must balance ADC sampling bandwidth against power budgets, often requiring complex trade-offs that can limit the full utilization of the device’s wideband digitization capability in fielded systems.

Other Challenges

Digital Interface and Data Throughput Bottlenecks

High-speed RF sampling ADCs generate enormous volumes of raw digital data that must be transported, processed, and stored in real time. The JESD204B and JESD204C serial interface standards, while widely adopted, introduce design complexity and latency considerations that require careful system-level management. FPGAs and digital signal processors downstream of the ADC must be capable of sustaining the required processing throughput, which drives up system cost and power consumption. For SDR platforms operating across wide instantaneous bandwidths, the data movement challenge between the ADC and the digital processing back-end remains a significant engineering and cost barrier.

Spurious-Free Dynamic Range and Harmonic Distortion Limitations

Achieving the spurious-free dynamic range (SFDR) and signal-to-noise-and-distortion ratio (SINAD) performance required for demanding electronic warfare and signals intelligence applications remains technically challenging for direct RF sampling ADCs operating at the highest frequency bands. Harmonic and intermodulation distortion products generated within the ADC can mask weak signals of interest, requiring additional digital post-processing to mitigate , adding latency and computational load. As SDR systems are increasingly called upon to detect and characterize low-observable emitters in congested spectral environments, the dynamic range ceiling of currently available RF sampling ADC devices represents a persistent technical constraint for high-performance SDR market segments.

MARKET RESTRAINTS

High Device Cost and Complex System Integration Requirements Limiting Broader Market Penetration

RF Sampling ADC (Direct RF) for SDR Market is restrained by the relatively high unit cost of state-of-the-art wideband RF sampling data converters compared to conventional narrowband ADC solutions. Leading-edge devices offering multi-gigahertz input bandwidth, high resolution, and low noise spectral density are predominantly manufactured using advanced BiCMOS or FinFET process nodes, contributing to elevated wafer and packaging costs. For cost-sensitive commercial wireless infrastructure applications, the economic case for direct RF sampling must compete against mature, lower-cost superheterodyne receiver designs that remain adequate for less demanding operational scenarios. This cost differential continues to slow adoption in segments where performance requirements do not clearly justify the premium associated with direct RF digitization architectures.

Export Control Regulations and Supply Chain Constraints Affecting Global Market Accessibility

High-performance RF sampling ADCs deployed in defense-oriented SDR platforms are frequently subject to export control regulations, including the U.S. International Traffic in Arms Regulations (ITAR) and Export Administration Regulations (EAR), as well as equivalent frameworks maintained by the European Union and other jurisdictions. These regulatory constraints restrict the geographic availability of the most advanced direct RF sampling devices and create compliance overhead for both suppliers and system integrators operating in international markets. Furthermore, the concentration of advanced RF ADC manufacturing capability among a limited number of specialized semiconductor suppliers introduces supply chain concentration risk, as demonstrated by periodic component allocation challenges that have affected SDR platform production schedules across both defense and commercial customer segments.

MARKET OPPORTUNITIES

Expansion of Cognitive Radio and Spectrum Monitoring Applications Creating New Revenue Streams

RF Sampling ADC (Direct RF) for SDR Market stands to benefit substantially from the rapid expansion of cognitive radio systems and automated spectrum monitoring infrastructure worldwide. Regulatory bodies and spectrum management agencies are investing in wideband spectrum sensing networks capable of continuously monitoring large swaths of radio frequency spectrum for interference detection, unauthorized transmissions, and dynamic spectrum access coordination. Direct RF sampling ADCs are uniquely suited to these applications by virtue of their ability to digitize broad frequency ranges simultaneously, enabling comprehensive spectrum awareness without the sequential tuning required by conventional narrowband receivers. Global push toward more efficient, dynamic spectrum utilization , including shared spectrum frameworks such as the Citizens Broadband Radio Service (CBRS) band in the United States , is expected to sustain demand growth for wideband RF sampling solutions in this segment.

Integration with Artificial Intelligence and Machine Learning Platforms for Adaptive Signal Processing

An emerging and high-value opportunity for RF Sampling ADC (Direct RF) for SDR Market lies in the integration of direct RF digitization front-ends with artificial intelligence and machine learning-based signal processing back-ends. The rich, wideband digital data streams produced by RF sampling ADCs provide the observational depth required to train and deploy neural network models capable of automatic modulation classification, emitter identification, adaptive interference cancellation, and spectrum anomaly detection. Defense and intelligence community customers, as well as commercial spectrum operators, are actively investing in AI-enabled SDR platforms that leverage the full spectral observability afforded by direct RF sampling architectures. This convergence of high-speed data conversion with AI-driven signal processing represents a structurally differentiated market segment with above-average growth potential and barriers to competitive entry.

Low Earth Orbit Satellite Communications and Non-Terrestrial Network Infrastructure as an Emerging Demand Vector

The proliferation of low Earth orbit (LEO) satellite constellations and the broader development of non-terrestrial network (NTN) infrastructure represent a compelling emerging opportunity for suppliers of RF Sampling ADC (Direct RF) technology targeting the SDR market. Satellite ground terminals and on-board payload processors increasingly require flexible, software-reconfigurable radio architectures capable of adapting to evolving waveforms, frequency plans, and communication protocols across multiple orbital systems. Direct RF sampling ADCs enable the multi-band, multi-waveform agility that next-generation satellite communication terminals demand, while the continued improvement in device power efficiency supports deployment in both ground-based and space-qualified configurations. As LEO constellation operators expand global coverage and interoperability requirements grow, the demand for high-performance direct RF sampling solutions within the broader SDR ecosystem is expected to represent a meaningful incremental growth opportunity through the latter half of this decade.

RF Sampling ADC (Direct RF) for SDR Market Trends

Rising Adoption of Direct RF Sampling Architectures in Next-Generation SDR Platforms

RF Sampling ADC (Direct RF) for SDR Market is witnessing a significant shift in system design philosophy, as engineers and system architects increasingly move away from traditional superheterodyne receiver architectures toward direct RF digitization. This transition is largely driven by the demand for flexible, reconfigurable radio platforms that can operate across multiple frequency bands without hardware modifications. Direct RF sampling ADCs eliminate the need for intermediate frequency downconversion stages, reducing system complexity, lowering component count, and enabling broader instantaneous bandwidth coverage. Defense agencies, telecommunications operators, and aerospace integrators are among the primary adopters accelerating this architectural evolution across their next-generation SDR deployments.

Other Trends

5G Infrastructure Rollout Fueling Demand for Wideband RF Data Converters

The rapid global deployment of 5G networks has emerged as a pivotal demand driver for RF Sampling ADC (Direct RF) for SDR Market. Multi-band, multi-mode base station architectures require high-speed analog-to-digital converters capable of simultaneously processing signals across diverse frequency ranges, from sub-6 GHz to millimeter-wave spectrum. Direct RF sampling solutions support these requirements with greater efficiency than conventional multi-stage conversion chains. Equipment manufacturers are integrating wideband RF sampling converters into massive MIMO antenna systems and open RAN infrastructure, reflecting growing industry confidence in direct digitization as the standard approach for advanced wireless base station design.

Defense Sector Investment Driving Advanced SDR Development

Sustained and growing defense expenditures globally continue to represent a major growth catalyst for RF Sampling ADC (Direct RF) for SDR Market. The United States alone allocated over USD 886 billion in defense spending during fiscal year 2024, with significant portions directed toward electronic warfare systems, signals intelligence platforms, and tactical communications upgrades. Modern military SDR platforms require high-performance direct RF ADCs capable of wide instantaneous bandwidth, high dynamic range, and rapid frequency agility. These operational requirements are pushing semiconductor manufacturers to develop multi-gigasample-per-second ADC solutions with integrated digital downconversion and signal conditioning capabilities tailored specifically for defense-grade SDR applications.

Portfolio Expansion by Leading Semiconductor Manufacturers

Key industry participants including Texas Instruments Inc., Analog Devices Inc., and Xilinx (AMD) are actively expanding their RF data converter product portfolios to address the broadening application landscape of RF Sampling ADC (Direct RF) for SDR Market. These companies are investing in integrated RF data converter solutions that combine high-speed ADCs, digital-to-analog converters, and digital signal processing blocks within single-chip architectures. Such integration reduces board space, power consumption, and system design complexity, making direct RF sampling more accessible to a wider range of commercial and government SDR programs. This trend toward higher levels of integration is expected to further accelerate adoption across telecommunications, aerospace, and defense verticals in the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

RF Sampling ADC (Direct RF) for SDR Market: Competitive Dynamics and Leading Innovators Shaping Next-Generation Radio Architectures

Global RF Sampling ADC (Direct RF) for SDR market is characterized by a concentrated competitive landscape dominated by a handful of vertically integrated semiconductor giants with extensive RF and mixed-signal expertise. Analog Devices Inc. (ADI) maintains a commanding market presence through its high-performance RF data converter portfolio, including the AD9081 and AD9082 MxFE platform solutions, which offer multi-gigasample-per-second sampling rates and integrated digital signal processing capabilities tailored for wideband SDR deployments. Texas Instruments Inc. similarly holds a significant share, leveraging its deep analog semiconductor heritage to deliver direct RF sampling ADC solutions targeting defense electronics, telecommunications infrastructure, and test and measurement applications. AMD (formerly Xilinx), following its acquisition of Xilinx, has emerged as a critical player by combining its RFSoC device family , which integrates RF-class ADCs and DACs directly alongside FPGA fabric , with high-capacity programmable logic, enabling system designers to implement complete direct RF sampling SDR platforms on a single device. This highly integrated approach has proven particularly compelling for aerospace, defense, and 5G massive MIMO applications, where size, weight, and power constraints are paramount.

Beyond the dominant tier-one suppliers, several specialized and emerging players contribute meaningfully to the RF Sampling ADC ecosystem for SDR. Microchip Technology, through its acquisition of Microsemi, offers radiation-hardened and high-reliability RF converter solutions suited to space and defense-grade SDR platforms. Renesas Electronics Corporation provides high-speed ADC products addressing wideband signal capture requirements across military communications and electronic warfare. NXP Semiconductors targets the cellular infrastructure segment with RF data converter components supporting direct sampling architectures in massive MIMO base stations. Infineon Technologies AG and STMicroelectronics round out the European competitive contingent, supplying RF-capable mixed-signal semiconductors for industrial and communications SDR use cases. On the FPGA-integrated front, Intel (via its Agilex and Stratix FPGA families with integrated transceiver blocks) competes with AMD/Xilinx RFSoC in offering programmable platforms amenable to direct RF signal processing. Smaller, innovation-focused firms such as Teledyne e2v and Cobalt Digital supply ultra-high-speed ADC devices targeting specialized defense signals intelligence and electronic warfare SDR applications, where sampling rates extending beyond 6 GSPS are required. The competitive intensity is expected to increase as the market grows from USD 2.09 billion in 2026 toward USD 4.63 billion by 2034 at a CAGR of 9.3%, attracting both established players expanding their RF data converter portfolios and new entrants pursuing niche high-performance segments.

List of Key RF Sampling ADC (Direct RF) for SDR Companies Profiled

- Analog Devices Inc. (ADI)

- Texas Instruments Inc.

- AMD (Xilinx)

- Intel Corporation

- Microchip Technology Inc.

- Renesas Electronics Corporation

- NXP Semiconductors

- Infineon Technologies AG

- STMicroelectronics

- Teledyne e2v

- Cobalt Digital

- Microsemi Corporation (Microchip)

- Maxim Integrated (Analog Devices)

- Samtec Inc.

- Pentek Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Wideband RF Sampling ADCs represent the leading segment within the By Type category, driven by their unparalleled ability to capture and digitize broad swaths of the radio frequency spectrum in a single acquisition step.

|

| By Application |

|

Electronic Warfare (EW) & Signals Intelligence (SIGINT) stands as the leading application segment, reflecting the critical and growing role of RF Sampling ADCs in modern defense ecosystems.

|

| By End User |

|

Defense & Government Agencies constitute the dominant end-user segment in the RF Sampling ADC for SDR market, underpinned by sustained and mission-critical procurement of advanced radio frequency technologies.

|

| By Frequency Band |

|

L-Band & S-Band emerge as the leading frequency band segment owing to their widespread use across both commercial telecommunications and defense communication systems globally.

|

| By Platform |

|

Ground-Based Platforms lead the By Platform segment, driven by the extensive deployment of direct RF sampling SDR systems across fixed and mobile terrestrial infrastructure spanning both defense and commercial sectors.

|

Regional Analysis: RF Sampling ADC (Direct RF) for SDR Market

North America

North America’s defense sector remains the primary catalyst for RF Sampling ADC adoption within SDR platforms. Military modernization initiatives demand direct RF sampling solutions that eliminate analog mixing stages, reducing system weight and power consumption in airborne and shipborne radio systems. Procurement agencies are increasingly specifying wideband direct digitization capabilities as a baseline requirement for next-generation tactical communication and electronic intelligence platforms.

The region hosts a concentration of world-class semiconductor design firms and fabless innovators actively advancing direct RF sampling ADC architectures. Strong collaboration between national laboratories, research universities, and private industry ensures a continuous pipeline of performance improvements in sampling speed, dynamic range, and power efficiency , all critical parameters for software-defined radio applications serving both commercial and defense end markets.

Beyond defense, North America’s rapid rollout of advanced wireless infrastructure has created new commercial demand for RF Sampling ADC-enabled SDR platforms. Telecom operators and network equipment vendors are exploring direct RF digitization to simplify base station radio unit architectures, enabling software-reconfigurable multi-band operation. This commercial momentum complements defense-driven growth and broadens the overall market opportunity across the region.

Proactive spectrum management policies by North American regulatory bodies have accelerated the deployment of cognitive and software-defined radio systems that leverage direct RF sampling ADC technology. Spectrum sharing frameworks and dynamic access rules create a favorable environment for SDR-based solutions, encouraging investment from both established vendors and emerging technology companies targeting flexible, wideband radio digitization products.

Europe

Europe represents a significant and steadily evolving region within RF Sampling ADC (Direct RF) for SDR Market, underpinned by strong collaborative research frameworks, well-funded defense modernization programs, and a mature telecommunications industry committed to network innovation. Countries such as Germany, France, the United Kingdom, and Sweden are at the forefront of adopting direct RF sampling architectures, particularly within joint defense communication programs coordinated through multinational alliances. European research initiatives continue to foster university-industry partnerships that accelerate the development of advanced SDR platforms. The region’s emphasis on open radio access network principles and spectrum efficiency further stimulates demand for flexible, software-reconfigurable radio front ends enabled by high-performance RF Sampling ADC solutions. Regulatory harmonization across member states also simplifies cross-border deployment, enhancing market scalability for vendors offering direct RF digitization products tailored to the European defense and commercial wireless sectors.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region in RF Sampling ADC (Direct RF) for SDR Market, propelled by large-scale investments in defense communication modernization, the proliferation of advanced wireless networks, and the rapid expansion of domestic semiconductor manufacturing capabilities. Nations including China, Japan, South Korea, India, and Australia are actively integrating direct RF sampling ADC technologies into both military and commercial radio systems to achieve greater signal chain simplicity and spectral agility. Government-backed initiatives targeting indigenous defense electronics development are driving local design and production of SDR platforms with embedded direct RF sampling front ends. Additionally, Asia-Pacific’s dynamic consumer electronics and telecom ecosystem accelerates the commercialization of RF Sampling ADC innovations, creating diverse application avenues beyond traditional defense and positioning the region as a critical growth engine for Global market through 2034.

South America

South America occupies a developing but increasingly relevant position in RF Sampling ADC (Direct RF) for SDR Market. Brazil leads regional adoption, leveraging its expanding telecommunications infrastructure and growing defense electronics ambitions to integrate software-defined radio platforms with direct RF sampling capabilities into national communication and surveillance systems. Other markets including Argentina and Colombia are gradually recognizing the operational advantages of direct RF digitization for border security and public safety radio networks. While budget constraints and limited domestic semiconductor manufacturing present near-term challenges, ongoing technology transfer agreements and international defense partnerships are gradually improving access to advanced RF Sampling ADC components. Over the forecast period, increased infrastructure investment and a rising focus on spectrum management modernization are expected to steadily elevate South America’s contribution to Global RF Sampling ADC for SDR market.

Middle East & Africa

The Middle East and Africa region presents a nuanced and gradually evolving opportunity within RF Sampling ADC (Direct RF) for SDR Market. Gulf Cooperation Council nations, particularly Saudi Arabia and the United Arab Emirates, are investing substantially in defense and telecommunications modernization programs that increasingly specify advanced SDR platforms utilizing direct RF sampling architectures. These investments are aligned with broader national transformation visions that emphasize technological self-reliance and indigenous defense industrial capability. In Africa, select markets are beginning to explore software-defined radio solutions for public safety, border monitoring, and rural connectivity applications, where the spectral flexibility of direct RF sampling ADC-enabled platforms offers practical deployment advantages. While the region collectively faces challenges related to technology import dependency and financing capacity, long-term growth prospects remain positive as defense procurement budgets expand and commercial wireless infrastructure investment accelerates across key markets.

Report Scope

This market research report provides a comprehensive analysis of the RF Sampling ADC (Direct RF) for SDR Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Sampling ADC (Direct RF) for SDR Market?

-> Global RF Sampling ADC (Direct RF) for SDR Market was valued at USD 1.87 billion in 2025 and is projected to grow from USD 2.09 billion in 2026 to USD 4.63 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Which key companies operate in RF Sampling ADC (Direct RF) for SDR Market?

-> Key players include Texas Instruments Inc., Analog Devices Inc., and Xilinx (AMD), among others, all of whom are actively expanding their RF data converter portfolios to address the evolving needs of next-generation SDR deployments.

What are the key growth drivers?

-> Key growth drivers include the rapid global rollout of 5G infrastructure, escalating demand for flexible, reconfigurable radio platforms across defense, telecommunications, and aerospace sectors, and increasing defense budgets worldwide , with U.S. defense spending exceeding USD 886 billion in fiscal year 2024 , driving investment in advanced SDR platforms for electronic warfare, signals intelligence, and tactical communications.

Which region dominates the market?

-> North America holds a significant position in the market driven by strong defense spending and advanced telecommunications infrastructure, while Asia-Pacific is among the fastest-growing regions due to rapid 5G deployment and expanding defense modernization programs.

What are the emerging trends?

-> Emerging trends include the adoption of direct RF sampling architectures eliminating traditional IF downconversion stages, integration of multi-gigasample-per-second ADCs, development of wideband RF sampling converters supporting frequency bands from HF through millimeter-wave spectrum, and growing demand for multi-band, multi-mode communication systems in next-generation SDR deployments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...