RF Power Amplifier (GaAs, GaN) for Cellular Market Insights

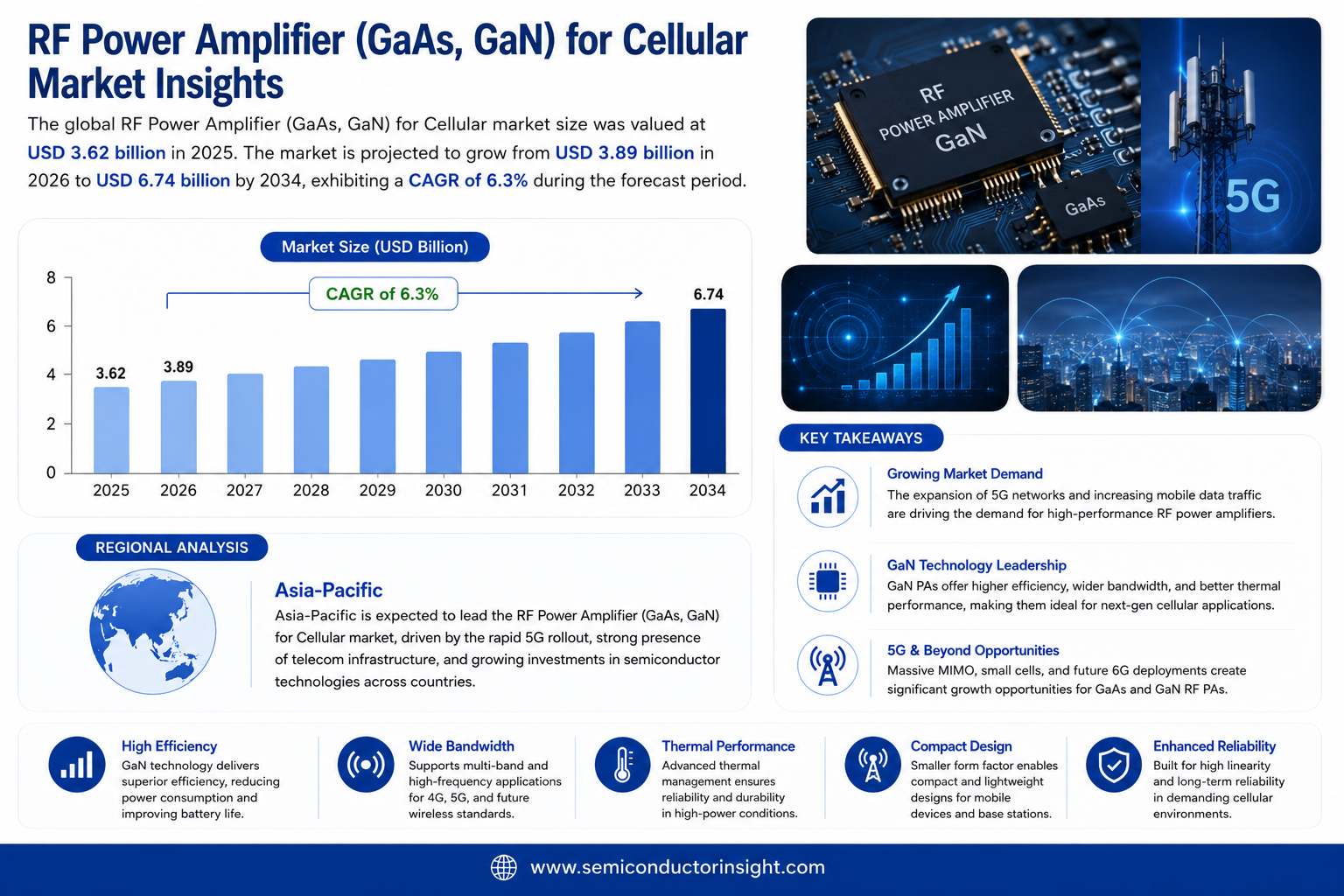

RF Power Amplifier (GaAs, GaN) for Cellular Market size was valued at USD 3.62 billion in 2025. The market is projected to grow from USD 3.89 billion in 2026 to USD 6.74 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

RF power amplifiers based on Gallium Arsenide (GaAs) and Gallium Nitride (GaN) semiconductor technologies are critical components in cellular communication infrastructure and mobile devices. These amplifiers are responsible for boosting radio frequency signals to the power levels required for reliable wireless transmission across cellular networks. The product category encompasses a broad range of devices including front-end modules (FEMs), multi-mode multi-band (MMMB) amplifiers, envelope tracking amplifiers, and Doherty amplifiers, serving applications across 4G LTE, 5G sub-6 GHz, and 5G mmWave cellular deployments.

The market is experiencing robust growth driven by the accelerating global rollout of 5G networks, rising smartphone penetration, and increasing demand for higher data throughput and spectral efficiency. GaN-based amplifiers, in particular, are gaining significant traction in base station infrastructure due to their superior power density, thermal performance, and efficiency at higher frequencies. Meanwhile, GaAs technology continues to dominate handset power amplifier applications owing to its proven linearity and low-noise characteristics. Strategic collaborations among leading semiconductor companies , including Broadcom Inc., Qorvo Inc., Skyworks Solutions, and Murata Manufacturing , are further shaping the competitive landscape through continuous product innovation and capacity expansion.

MARKET DRIVERS

Global 5G Rollout Accelerating Demand for Advanced RF Power Amplifiers

The rapid global expansion of 5G networks has emerged as one of the most significant drivers for RF Power Amplifier (GaAs, GaN) for Cellular Market . Telecom operators worldwide are investing heavily in densifying their network infrastructure, deploying massive MIMO base stations and small cells that require high-performance RF front-end components. GaN-based RF power amplifiers, in particular, have gained strong traction in 5G base station applications owing to their superior power density, higher efficiency at elevated frequencies, and robust thermal performance compared to legacy technologies. As sub-6 GHz and mmWave spectrum deployments accelerate across North America, Asia-Pacific, and Europe, demand for both GaAs and GaN RF power amplifiers continues to grow at a sustained pace.

Proliferation of Connected Devices Driving RF Component Integration

The exponential growth in smartphone penetration, IoT-enabled devices, and connected consumer electronics is placing increasing pressure on cellular network capacity and quality. This, in turn, is driving OEMs and network equipment manufacturers to source more sophisticated RF power amplifier solutions. GaAs RF power amplifiers continue to dominate handset and user equipment applications due to their excellent linearity, low noise characteristics, and mature manufacturing ecosystem. The ongoing transition to multi-band, multi-mode devices further reinforces the need for highly integrated RF front-end modules incorporating GaAs-based amplification stages optimized for cellular frequency bands including LTE, 5G NR, and legacy 4G standards.

➤ GaN-based RF power amplifiers are increasingly preferred for macro base station deployments given their ability to deliver higher output power at millimeter-wave frequencies, offering network operators improved total cost of ownership and reduced energy consumption per transmitted watt , two critical considerations as cellular infrastructure scales to meet growing data traffic demands.

Government-backed spectrum allocation programs and national broadband initiatives across emerging economies are further propelling investments in cellular infrastructure modernization. Countries across Southeast Asia, Latin America, and the Middle East are actively licensing new frequency bands and mandating network upgrades, creating a sustained pipeline of opportunities for RF power amplifier suppliers serving both the base station and handset segments of the cellular market.

MARKET CHALLENGES

Thermal Management and Device Reliability Constraints in High-Power GaN Amplifier Designs

Despite the clear performance advantages of GaN-based RF power amplifiers in cellular infrastructure, thermal management remains a persistent engineering challenge. GaN devices operating at high power densities generate significant heat, and inadequate thermal dissipation can lead to accelerated device degradation, reduced mean time between failures, and compromised signal integrity. Designing reliable packaging solutions and heat sink architectures that maintain junction temperatures within acceptable limits , particularly for outdoor macro base station deployments exposed to variable environmental conditions , adds complexity and cost to the overall system design, challenging both amplifier manufacturers and network equipment OEMs.

Other Challenges

Supply Chain Concentration and Substrate Availability

RF Power Amplifier (GaAs, GaN) for Cellular Market is exposed to supply chain risks associated with the concentration of compound semiconductor substrate manufacturing. GaAs and GaN wafer production relies on a relatively limited number of specialized foundries and epitaxial wafer suppliers, creating potential bottlenecks during periods of elevated demand or geopolitical disruption. Fluctuations in substrate availability and pricing can compress margins for amplifier manufacturers and introduce lead time uncertainty for cellular OEM customers relying on consistent component supply.

Design Complexity and Integration Costs

The transition to advanced 5G waveforms such as massive MIMO and carrier aggregation demands RF power amplifiers with increasingly stringent linearity, bandwidth, and efficiency specifications. Meeting these requirements while simultaneously reducing form factor and bill-of-materials cost presents significant design challenges. Digital pre-distortion techniques and advanced packaging approaches such as flip-chip and wafer-level packaging add engineering overhead and development expenditure, particularly for smaller RF component suppliers competing against vertically integrated semiconductor companies with greater R&D resources.

MARKET RESTRAINTS

High Capital Expenditure Requirements for GaN and GaAs Wafer Fabrication

The capital-intensive nature of compound semiconductor fabrication represents a meaningful restraint on the broader RF Power Amplifier (GaAs, GaN) for Cellular Market. Establishing or expanding GaN-on-SiC or GaAs PHEMT fabrication capacity requires substantial investment in specialized MOCVD equipment, cleanroom infrastructure, and process development, creating high barriers to entry and limiting the number of qualified foundry partners available to amplifier designers. This concentration of manufacturing capability can constrain supply responsiveness during demand surges and reduces competitive pressure on established foundry players, potentially sustaining elevated wafer pricing that flows through to end-market RF amplifier costs.

Competitive Pressure from Silicon-Based Alternatives in Select Cellular Applications

While GaAs and GaN technologies maintain clear performance advantages in the majority of cellular RF power amplifier applications, advances in CMOS and SiGe BiCMOS processes are enabling silicon-based RF solutions to encroach on the lower power, lower frequency segments of the cellular market. Silicon RF power amplifiers offer the advantage of integration with digital baseband circuitry on a single die, reducing component count and potentially lowering system cost for certain handset and small cell applications. As silicon process nodes continue to shrink and RF performance improves, GaAs-based amplifier suppliers serving the consumer handset segment face incremental competitive pressure that could moderate long-term revenue growth in specific product categories.

MARKET OPPORTUNITIES

Open RAN Architecture Creating New Demand for Flexible RF Power Amplifier Solutions

The accelerating global adoption of Open RAN (O-RAN) architecture by cellular network operators presents a compelling growth opportunity for RF Power Amplifier (GaAs, GaN) for Cellular Market . O-RAN disaggregates the radio access network into standardized, interoperable components, enabling operators to source radio units , including the critical RF front-end incorporating power amplifiers , from a diversified supplier base rather than relying on integrated solutions from a single vendor. This architectural shift is expanding the addressable market for independent RF power amplifier manufacturers and is stimulating development of wideband, reconfigurable GaN-based amplifier modules capable of supporting multiple frequency bands and radio standards within a single platform.

Energy Efficiency Mandates Elevating GaN RF Power Amplifier Adoption in Base Stations

Growing regulatory and corporate sustainability pressures on mobile network operators to reduce energy consumption are creating a structural tailwind for high-efficiency GaN RF power amplifiers in cellular base station applications. GaN-based Doherty and envelope-tracking amplifier architectures deliver materially higher power-added efficiency compared to older GaAs or LDMOS solutions, enabling operators to reduce electricity costs and carbon emissions per base station site. As mobile operators publicly commit to net-zero targets and energy cost management becomes a strategic priority, procurement decisions increasingly favor GaN RF power amplifiers that demonstrate superior efficiency metrics, opening sustained replacement cycle opportunities for GaN amplifier suppliers across both new deployments and retrofit upgrades of existing cellular infrastructure.

Emerging Markets Infrastructure Build-Out Expanding the Cellular RF Amplifier Addressable Market

Accelerating cellular network build-out across high-growth emerging markets in Sub-Saharan Africa, South Asia, and Southeast Asia is broadening the addressable market for RF power amplifier manufacturers serving the cellular segment. Many of these regions are executing leapfrog deployments, transitioning directly to 4G LTE and early 5G NR infrastructure rather than upgrading through legacy 2G and 3G generations, driving proportionally higher demand for advanced GaAs and GaN RF power amplifier components suited to modern cellular radio standards. The combination of rising mobile broadband penetration, expanding middle-class consumer segments, and government-supported universal connectivity programs positions these geographies as high-growth incremental demand sources for RF Power Amplifier (GaAs, GaN) for Cellular Market over the coming years.

Trends

Accelerating 5G Deployment Driving Demand for Advanced RF Power Amplifiers

RF Power Amplifier (GaAs, GaN) for Cellular Market is undergoing a significant transformation, primarily fueled by the accelerating global rollout of 5G networks. As mobile network operators expand 5G infrastructure across sub-6 GHz and mmWave frequency bands, the demand for high-performance RF power amplifiers capable of delivering superior efficiency and power density has intensified. GaN-based amplifiers are emerging as the technology of choice for base station deployments, offering compelling advantages in thermal management and power handling at elevated frequencies. This shift is prompting semiconductor manufacturers to scale production capacity and invest in next-generation GaN device architectures tailored for massive MIMO and beamforming applications in 5G base stations.

Other Trends

GaAs Technology Retains Dominance in Handset Applications

Despite the growing adoption of GaN in infrastructure, GaAs technology continues to hold a commanding position in handset power amplifier applications. GaAs-based amplifiers remain preferred for mobile devices due to their well-established linearity, low-noise performance, and compatibility with compact front-end module designs. As smartphone manufacturers pursue thinner form factors and multi-band connectivity, GaAs-based multi-mode multi-band amplifiers and envelope tracking solutions are being refined to meet increasingly stringent efficiency and form factor requirements. Leading suppliers including Broadcom Inc., Qorvo Inc., Skyworks Solutions, and Murata Manufacturing are actively advancing GaAs front-end module integration to address the evolving demands of 4G LTE and 5G-enabled handsets.

Strategic Collaborations and Product Innovation Reshaping the Competitive Landscape

RF Power Amplifier (GaAs, GaN) for Cellular Market is witnessing a wave of strategic partnerships and product development initiatives among key semiconductor players. Companies are focusing on expanding their portfolios to encompass Doherty amplifiers, envelope tracking amplifiers, and integrated front-end modules designed specifically for 5G network equipment and advanced mobile platforms. These collaborative efforts are aimed at addressing the dual imperatives of power efficiency and spectral efficiency as cellular networks evolve toward denser, higher-capacity architectures.

Rising Smartphone Penetration and Data Throughput Requirements Sustaining Long-Term Growth

Continued growth in global smartphone penetration, combined with escalating consumer demand for higher data throughput, is reinforcing long-term momentum RF Power Amplifier (GaAs, GaN) for Cellular Market . As cellular networks transition to support bandwidth-intensive applications, RF power amplifiers that balance high efficiency with reliable signal amplification across diverse frequency bands are becoming indispensable. This sustained demand trajectory is encouraging ongoing investment in both GaAs and GaN semiconductor technologies, positioning the market for steady advancement through the coming decade.

COMPETITIVE LANDSCAPE

Key Industry Players

RF Power Amplifier (GaAs, GaN) for Cellular Market: Competitive Dynamics and Leading Semiconductor Companies Shaping the Global Landscape

RF Power Amplifier (GaAs, GaN) for Cellular Market is characterized by intense competition among a concentrated group of vertically integrated semiconductor companies with deep expertise in compound semiconductor design and manufacturing. Broadcom Inc., Qorvo Inc., and Skyworks Solutions collectively command a significant share of the handset power amplifier segment, leveraging their advanced GaAs process technologies to deliver highly integrated front-end modules (FEMs) and multi-mode multi-band (MMMB) amplifiers optimized for 4G LTE and 5G sub-6 GHz smartphones. Murata Manufacturing further strengthens its position through strategic module integration capabilities, combining RF power amplifiers with filters and switches to offer compact, high-performance front-end solutions for leading mobile OEMs. These dominant players continue to invest heavily in research and development, capacity expansion, and supply chain consolidation to maintain their technological edge and meet surging demand driven by the accelerating global 5G network rollout.

Beyond the handset segment, the base station infrastructure space has attracted a distinct set of competitors specializing in GaN-based RF power amplifiers, where superior power density, thermal resilience, and efficiency at higher frequencies are critical differentiators. Wolfspeed (formerly Cree RF), Ampleon, and NXP Semiconductors are recognized leaders in GaN-on-SiC and GaN-on-Si power amplifier solutions targeting macro base stations and Massive MIMO deployments. Analog Devices and MACOM Technology Solutions have also carved out meaningful positions in the 5G infrastructure amplifier space, offering wideband GaN devices suited for both sub-6 GHz and mmWave applications. Meanwhile, companies such as Mitsubishi Electric, Sumitomo Electric Device Innovations, and Toshiba Electronic Devices maintain strong presences in the Asia-Pacific region, supplying GaAs and GaN amplifier components to cellular infrastructure OEMs. Emerging players including Microchip Technology and Integrated Device Technology (now part of Renesas Electronics) are expanding their RF portfolios to capture incremental share as 5G densification accelerates globally.

List of Key RF Power Amplifier (GaAs, GaN) for Cellular Companies Profiled

- Broadcom Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Murata Manufacturing Co., Ltd.

- Wolfspeed, Inc. (formerly Cree RF)

- Ampleon Netherlands B.V.

- NXP Semiconductors N.V.

- Analog Devices, Inc.

- MACOM Technology Solutions Holdings, Inc.

- Mitsubishi Electric Corporation

- Sumitomo Electric Device Innovations, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Microchip Technology Inc.

- Renesas Electronics Corporation (Integrated Device Technology)

- WIN Semiconductors Corp.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GaAs RF Power Amplifiers currently hold a dominant position in the overall RF power amplifier market, particularly for handset and mobile device applications. Key qualitative factors driving this leadership include:

|

| By Application |

|

5G Sub-6 GHz Networks represent the leading application segment for RF power amplifiers, driven by the aggressive global rollout of 5G infrastructure across major economies. Key qualitative insights include:

|

| By End User |

|

Telecom Infrastructure Providers stand as the dominant end-user segment in the RF power amplifier market, given the scale and complexity of 5G base station deployments globally. Key qualitative drivers include:

|

| By Technology Architecture |

|

Front-End Modules (FEMs) represent the leading technology architecture segment, particularly within consumer cellular devices, as they integrate multiple RF functions into a compact, highly optimized package. Key insights include:

|

| By Frequency Band |

|

Mid-Band (1 GHz – 6 GHz) is the leading frequency band segment for RF power amplifiers in the cellular market, reflecting the widespread operator preference for mid-band spectrum as the primary workhorse for 5G network coverage and capacity. Key qualitative insights include:

|

Regional Analysis: RF Power Amplifier (GaAs, GaN) for Cellular Market

Asia-Pacific

Asia-Pacific’s cellular operators are aggressively deploying massive MIMO base stations and small cells that rely heavily on GaN-based RF power amplifiers for their superior efficiency and power handling. China’s nationwide 5G buildout, one of the most expansive globally, continues to generate sustained demand for high-frequency, high-linearity RF front-end solutions tailored specifically for sub-6 GHz and millimeter-wave cellular bands.

The region hosts a critical mass of GaAs and GaN wafer fabrication facilities, particularly in Taiwan, Japan, and China, enabling vertically integrated supply chains for RF power amplifier production. This manufacturing proximity reduces lead times, supports design-to-production cycles, and allows regional chipmakers to iterate rapidly on next-generation cellular amplifier architectures while maintaining competitive cost structures.

Government-backed semiconductor development programs across China, South Korea, Japan, and India are channeling substantial funding into GaN power amplifier research and indigenous cellular chipset development. These policy initiatives aim to reduce reliance on foreign RF component suppliers, fostering a self-reliant ecosystem that strengthens the region’s long-term competitive position in the global cellular RF amplifier landscape.

Beyond the established leaders, India’s accelerating 5G rollout and Southeast Asia’s expanding mobile broadband infrastructure are creating new demand pockets for GaAs and GaN RF power amplifiers. Telecom operators in these markets are scaling up base station deployments at a rapid pace, presenting significant commercial opportunities for both regional and global RF amplifier suppliers targeting high-growth cellular markets.

North America

North America represents a strategically vital region RF Power Amplifier (GaAs, GaN) for Cellular Market , underpinned by a robust innovation ecosystem, leading defense-to-commercial technology transfer pathways, and advanced 5G network deployments. The United States is home to several globally recognized RF semiconductor companies that have pioneered GaN-on-SiC and GaN-on-Si technologies, with substantial application in both cellular base stations and handset RF front-end modules. Major U.S. carriers have invested heavily in mid-band and mmWave 5G infrastructure, generating sustained demand for high-efficiency GaN power amplifiers capable of meeting stringent spectral requirements. The region also benefits from strong government support through defense and national security programs that have historically accelerated GaN technology maturity, which subsequently transitions into commercial cellular applications. Canada contributes through its advanced photonics and compound semiconductor research institutions. North America’s deep integration between R&D, fabless design houses, and global foundry partnerships ensures continued technological leadership in next-generation RF power amplifier development through the forecast period.

Europe

Europe occupies a significant position RF Power Amplifier (GaAs, GaN) for Cellular Market , characterized by strong academic research foundations, precision engineering capabilities, and a steady pace of 5G network infrastructure investment. Countries including Germany, France, Sweden, Finland, and the United Kingdom host leading telecom equipment vendors and specialized RF semiconductor design houses that contribute meaningfully to GaAs and GaN amplifier innovation. European cellular network operators are progressively upgrading infrastructure to support 5G standalone architectures, increasing their reliance on advanced RF power amplifier technologies for base station deployments. The European Union’s focus on digital sovereignty and domestic semiconductor supply chain resilience has spurred new funding mechanisms aimed at bolstering compound semiconductor research and manufacturing within the region. Additionally, Europe’s stringent energy efficiency regulations are driving demand for GaN-based RF power amplifiers, which offer superior power-added efficiency compared to legacy GaAs solutions, aligning well with sustainability mandates increasingly adopted by regional telecom infrastructure providers.

South America

South America represents a steadily growing market for RF Power Amplifier (GaAs, GaN) for cellular applications, with Brazil serving as the primary demand center followed by Colombia, Argentina, and Chile. The region’s cellular operators are navigating complex economic environments while simultaneously pursuing 5G spectrum auctions and early-stage network deployments, creating incremental demand for GaN and GaAs RF power amplifiers in base station and small cell configurations. Brazil’s 5G rollout, which has progressed through major urban centers, reflects the broader continental shift toward next-generation cellular connectivity. Although South America currently lags behind Asia-Pacific and North America in terms of overall RF amplifier consumption, its improving telecommunications regulatory frameworks and growing smartphone penetration rates are steadily expanding the addressable market. International RF component suppliers are increasingly targeting the region through partnerships with local telecom operators and distributors, positioning South America as a meaningful long-term growth opportunity within the global RF power amplifier market landscape.

Middle East & Africa

The Middle East and Africa region presents a diverse and evolving landscape for RF Power Amplifier (GaAs, GaN) for Cellular Market , with the Gulf Cooperation Council countries leading regional adoption of advanced 5G cellular technologies. Nations such as Saudi Arabia, the United Arab Emirates, and Qatar have emerged as early 5G adopters, driven by national digital transformation agendas and substantial telecom infrastructure investment. These deployments rely on modern GaN-based RF power amplifiers for their ability to support high-frequency, high-power cellular bands with energy efficiency that aligns with ambitious national sustainability goals. Sub-Saharan Africa, while at an earlier stage of network modernization, presents significant long-term potential as mobile network operators expand 4G coverage and begin exploratory 5G planning in urban centers. North Africa’s proximity to Europe facilitates technology and investment flows supporting cellular infrastructure upgrades. As overall network densification accelerates across the region, demand for reliable and high-performance RF power amplifier solutions based on GaAs and GaN technologies is expected to grow progressively through the 2026–2034 forecast horizon.

Report Scope

This market research report provides a comprehensive analysis of the RF Power Amplifier (GaAs, GaN) for Cellular Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Power Amplifier (GaAs, GaN) for Cellular Market?

-> RF Power Amplifier (GaAs, GaN) for Cellular Market was valued at USD 3.62 billion in 2025 and is expected to reach USD 6.74 billion by 2034, growing at a CAGR of 6.3% during the forecast period from 2026 to 2034.

Which key companies operate RF Power Amplifier (GaAs, GaN) for Cellular Market ?

-> Key players include Broadcom Inc., Qorvo Inc., Skyworks Solutions, and Murata Manufacturing, among others, who are shaping the competitive landscape through continuous product innovation and capacity expansion.

What are the key growth drivers?

-> Key growth drivers include the accelerating global rollout of 5G networks, rising smartphone penetration, increasing demand for higher data throughput and spectral efficiency, and the growing adoption of GaN-based amplifiers in base station infrastructure due to their superior power density and thermal performance.

Which region dominates the market?

-> Asia-Pacific is a key region RF Power Amplifier (GaAs, GaN) for Cellular Market , driven by rapid 5G network deployments, high smartphone adoption rates, and strong semiconductor manufacturing capabilities across the region.

What are the emerging trends?

-> Emerging trends include the increasing adoption of GaN-based amplifiers for 5G base station infrastructure, growing use of front-end modules (FEMs), multi-mode multi-band (MMMB) amplifiers, envelope tracking amplifiers, and Doherty amplifiers, as well as expanding deployments across 5G sub-6 GHz and 5G mmWave cellular networks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...