Optoelectronic Transducers Market Insights

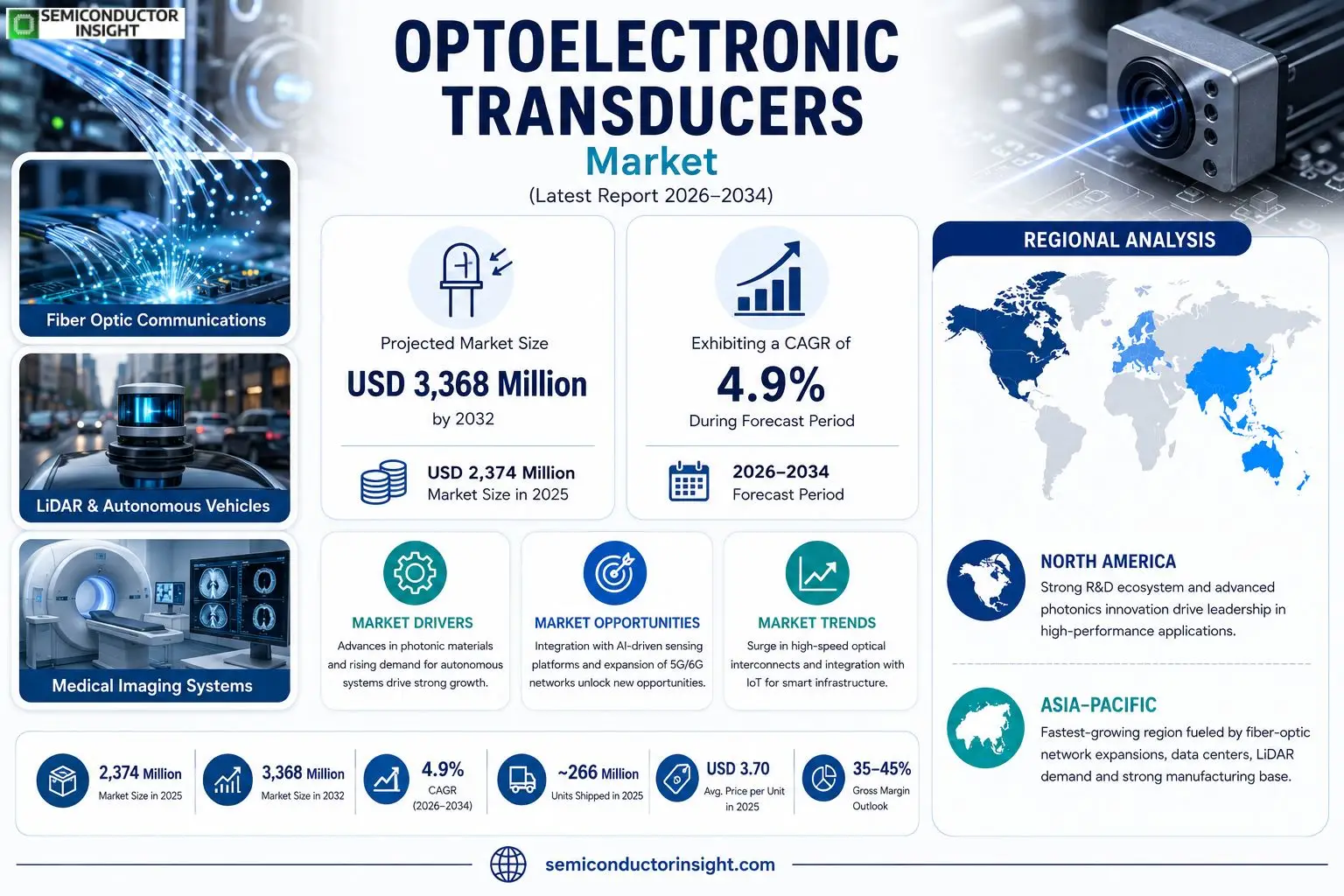

Optoelectronic Transducers market was valued at USD 2,374 million in 2025. The market is projected to grow from USD 2,374 million in 2025 to USD 3,368 million by 2032, exhibiting a CAGR of 4.9% during the forecast period.

Optoelectronic transducers are devices that convert light signals (photons) into electrical signals (electrons) or vice versa, forming the essential bridge between optical and electronic systems. The family includes photodetectors such as photodiodes, phototransistors and avalanche photodiodes; photoemitters like LEDs and laser diodes; and integrated modules such as optical receivers and transimpedance amplifiers. Performance is judged by responsivity (A/W), quantum efficiency, dark current, bandwidth and noise‑equivalent power.The market is seeing steady expansion because fiber‑optic communication networks are being upgraded worldwide, LiDAR demand for autonomous vehicles continues to rise, and medical imaging increasingly relies on high‑performance photodetectors. Advances in III‑V semiconductor processing have lowered costs while boosting quantum efficiency. Notable recent activity includes a March 2024 partnership between a leading silicon‑photonics company and an automotive supplier to develop high‑speed APD arrays for next‑generation driver‑assist systems. Established players such as ams‑OSRAM AG, Broadcom Inc., Hamamatsu Photonics K.K., Honeywell International Inc., Infineon Technologies AG and others are broadening portfolios through new product launches and strategic acquisitions.

MARKET DRIVERS

Advances in Photonic Materials

The emergence of low‑loss silicon‑based photonic platforms has lowered the barrier to integrate optical and electronic functions on a single chip. As a result, system designers are substituting legacy electro‑mechanical converters with faster, more reliable optoelectronic devices, pushing the Optoelectronic Transducers Market toward higher volume adoption in telecommunications and data‑center equipment.

Growth of Autonomous Systems

Autonomous vehicles and industrial robots rely on precise distance and velocity sensing. Modern lidar modules now embed optoelectronic transducers that deliver nanosecond response times, enabling more accurate obstacle detection. Manufacturers are therefore allocating a larger share of R&D budgets to these components, creating a solid revenue engine for suppliers.

➤ In 2023, shipments of optoelectronic transducer modules rose by 14 % year‑over‑year, reflecting heightened demand from both consumer‑grade and industrial applications.

Concurrently, the push toward energy‑efficient data transmission has accelerated interest in optical interconnects that replace copper links. Optoelectronic transducers, acting as the bridge between electrical signals and light, are uniquely positioned to meet the bandwidth and power‑consumption targets set by hyperscale data centers, cementing their role as a growth catalyst.

MARKET CHALLENGES

Cost Competitiveness Pressures

While performance metrics have improved, the unit cost of high‑frequency optoelectronic transducers remains above that of mature electro‑mechanical counterparts. Price‑sensitive OEMs in the automotive sector are therefore hesitant to replace legacy sensors without clear total‑cost‑of‑ownership proof points.

Other Challenges

Regulatory Hurdles

Stringent electromagnetic compatibility (EMC) standards in aerospace and medical devices compel manufacturers to invest heavily in compliance testing, prolonging time‑to‑market and eroding margins for smaller players.

MARKET RESTRAINTS

Supply‑Chain Volatility

Raw‑material shortages for indium‑gallium‑arsenide (InGaAs) and specialty optical fibers have introduced lead‑time extensions that can exceed six months. End users planning multi‑year projects are forced to maintain larger safety stocks, which dampens new procurement cycles.Furthermore, the concentration of wafer‑fab capacity among a handful of fabs raises the risk of production bottlenecks when demand spikes unexpectedly. Companies that lack direct access to these fabs often resort to higher‑cost secondary sources, impacting overall market profitability.Lastly, the escalating geopolitical tensions affecting semiconductor equipment export controls create an environment where long‑term capacity planning becomes fraught with uncertainty, discouraging aggressive expansion strategies.

MARKET OPPORTUNITIES

Integration with AI‑Driven Sensing Platforms

Artificial‑intelligence algorithms demand high‑resolution, low‑latency data streams. Embedding optoelectronic transducers directly into AI‑enabled sensor arrays allows real‑time preprocessing of optical signals, opening a revenue channel for vendors that can certify AI‑ready modules.Another promising avenue lies in the expansion of 5G and emerging 6G networks, where optical front‑ends are required to handle terabit‑per‑second traffic. Companies that can co‑design transducers with photonic integrated circuits (PICs) stand to capture a sizable share of network‑infrastructure upgrades.Finally, the medical imaging sector is exploring hybrid optical‑acoustic techniques for deeper tissue visualization. Optoelectronic transducers capable of converting laser pulses into ultrasonic waves present a differentiated product line that could command premium pricing.

Optoelectronic Transducers Market Trends

Surge in High‑Speed Optical Interconnects

The push for ultra‑low latency in hyperscale data centers and AI compute clusters is reshaping the demand profile for optoelectronic components. Manufacturers are tightening tolerances on bandwidth and responsivity to meet the stringent requirements of 400‑Gb/s and higher transceivers. This pressure is prompting a shift toward monolithic integration of photodetectors with silicon photonics, which reduces insertion loss and simplifies assembly. As telecom operators upgrade backbone networks, the volume of transceiver modules incorporating these transducers is climbing, translating into a noticeable lift in unit shipments. The trend also nudges suppliers to revisit wafer‑scale economics, favoring III‑V epitaxy processes that balance performance with cost. For customers, the result is a more predictable bill of materials and shorter time‑to‑market for next‑generation edge services.

Other Trends

Expansion of Photodiode Sensor Applications

Photodiodes are becoming indispensable across a broader set of verticals, from medical diagnostics to industrial safety systems. The avalanche variant, with its internal gain, is especially attractive for long‑haul fiber links and emerging LiDAR platforms, where signal‑to‑noise margins remain critical. In the Asia‑Pacific region, rapid rollout of broadband infrastructure and aggressive automotive electrification policies are amplifying demand for these sensors. Companies are responding by investing in low‑dark‑current epitaxial layers and leveraging compound‑semiconductor supply chains to secure volume discounts. The cumulative effect is a steady rise in average selling price stability despite fluctuating raw‑material costs, and a widening of the addressable market for OEMs seeking higher reliability in harsh environments.

Emergence of Integrated Sensing for IoT and Smart Infrastructure

IoT deployments are increasingly embedding optoelectronic transducers directly into building‑automation panels, structural‑health‑monitoring nodes, and edge‑analytics devices. By co‑locating photodetectors with wireless transceivers, system architects can extract real‑time optical signaturessuch as ambient light fluctuations or infrared emissivitywithout adding separate sensing modules. This convergence reduces overall bill of materials and shortens product cycles, encouraging smaller firms to adopt sophisticated optical sensing capabilities. For the Optoelectronic Transducers Market, the shift signifies a diversification beyond traditional telecom and defense customers, opening revenue streams tied to smart‑city initiatives and predictive‑maintenance services. Vendors that streamline integration workflows and certify their devices for rugged IoT standards are likely to capture a growing slice of this nascent opportunity.

COMPETITIVE LANDSCAPEKey Industry Players

Optoelectronic Transducers Market – Competitive Overview

Broadcom Inc. dominates the high‑speed photodiode segment, leveraging its extensive silicon‑photonic portfolio and deep ties with data‑center OEMs. The company’s ability to co‑design transceiver modules with hyperscale operators secures a disproportionate share of the $3.70‑average unit price pool, while its in‑house epitaxial capacity reduces reliance on third‑party wafer suppliers. This vertical integration pushes margins toward the upper end of the 35‑45 % band and forces smaller firms to differentiate through niche wavelengths or ultra‑low dark‑current designs. In parallel, Infineon Technologies AG’s focus on automotive‑grade avalanche photodiodes has created a de‑facto standard for LiDAR‑grade receivers, granting the German group a foothold in a segment where reliability certifications outweigh pure cost considerations.Beyond the two market leaders, a cluster of specialized manufacturers competes on performance metrics rather than scale. Hamamatsu Photonics K.K. excels in scientific‑grade UV and SWIR detectors, capitalising on its legacy in precision measurement equipment. Sony Group Corporation provides high‑volume LED‑based emitters that feed consumer‑electronics and smart‑city IoT deployments, while STMicroelectronics N.V. and Texas Instruments Inc. supply integrated optoelectronic modules that combine transimpedance amplifiers with photodiodes for industrial automation. Vishay Intertechnology Inc., ROHM Co., Ltd. and LITE‑ON Technology Corporation address mid‑range market tiers through cost‑effective packaging solutions, whereas emerging players such as Eoptolink Technology Inc. and ams‑OSRAM AG target niche applications in biomedical imaging and quantum‑efficiency‑enhanced photodetectors. The overall landscape reveals a tiered competitive structure where scale‑driven firms secure bulk communication contracts and a suite of agile innovators capture high‑performance, application‑specific opportunities.

List of Key Optoelectronic Transducers Companies Profiled

- Broadcom Inc.

- Infineon Technologies AG

- Hamamatsu Photonics K.K.

- Sony Group Corporation

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Vishay Intertechnology, Inc.

- ROHM Co., Ltd.

- LITE-ON Technology Corporation

- Eoptolink Technology Inc.

- ams-OSRAM AG

- Honeywell International Inc.

- Renesas Electronics Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Photodiodes

|

| By Application |

|

Fiber Optic Communications

|

| By End User |

|

Telecommunications Service Providers

|

| By [Segment Category 3]] |

|

III‑V Compound Semiconductors

|

| By [Segment Category 4]] |

|

Hybrid Integrated Modules

|

Regional Analysis: Optoelectronic Transducers Market

North America

Early adoption of silicon‑photonic platforms has accelerated product cycles, enabling manufacturers to embed transducers directly into CMOS wafers. This integration lowers assembly complexity and opens pathways for high‑density sensor arrays in wearables and industrial IoT devices.

Companies are diversifying component sources, establishing regional fabs to cushion against trans‑Pacific logistics shocks. This strategy not only shortens delivery windows but also aligns with customer expectations for rapid prototyping.

Harmonized standards across FDA and FAA channels simplify certification for dual‑use transducers, reducing time‑to‑market for products that serve both civilian and defense sectors.

Strategic acquisitions of niche photonic firms allow larger players to absorb specialized IP, creating end‑to‑end solution portfolios that address complex customer specifications.

Europe

European manufacturers benefit from a collaborative R&D environment fostered by Horizon‑Europe programmes, which subsidize cross‑border projects on high‑precision optical sensing. The emphasis on sustainability has spurred the development of low‑power transducers for smart‑grid monitoring, aligning with EU energy‑efficiency directives. While funding mechanisms are strong, market growth is moderated by fragmented procurement practices across member states, prompting firms to adopt a pan‑European sales strategy to achieve scale.

Asia‑Pacific

The Asia‑Pacific region showcases a fast‑moving consumer electronics sector that increasingly incorporates optoelectronic transducers into smartphones and AR headsets. Governments in China, South Korea, and Taiwan prioritize semiconductor self‑reliance, channeling resources into photonics foundries. However, the nascent stage of high‑end medical applications creates a divergence between mass‑market demand and specialised device adoption, encouraging manufacturers to balance volume production with niche‑focused R&D.

South America

In South America, market momentum originates from telecommunications upgrades and emerging renewable‑energy projects that require precise optical metrology. Brazil’s innovation hubs are beginning to attract multinational partnerships, yet the region faces challenges related to import tariffs and limited local expertise, which pushes firms to establish joint‑venture models to bridge capability gaps.

Middle East & Africa

Middle East & Africa investors are channeling capital into smart‑city initiatives that rely on optical sensing for traffic management and environmental monitoring. The United Arab Emirates, in particular, funds pilot programs that test rugged transducers in desert conditions. Limited manufacturing infrastructure means most solutions are imported, creating opportunities for suppliers willing to offer localized support and training.

Report Scope

This market research report provides a comprehensive analysis of the Optoelectronic Transducers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optoelectronic Transducers Market?

-> Optoelectronic Transducers Market was valued at USD 2374 million in 2025 and is expected to reach USD 3368 million by 2032, growing at a CAGR of 4.9% during the forecast period.

Which key companies operate in Optoelectronic Transducers Market?

-> Key players include ams-OSRAM AG, Broadcom Inc., Hamamatsu Photonics K.K., Honeywell International Inc., Infineon Technologies AG, LITE-ON Technology Corporation, Mitsubishi Electric Corporation, ON Semiconductor Corporation, Renesas Electronics Corporation, ROHM Co., Ltd., Sony Group Corporation, STMicroelectronics N.V., Texas Instruments Incorporated, Vishay Intertechnology, Inc., and Eoptolink Technology Inc.

What are the key growth drivers?

-> Key growth drivers include the rapid adoption of optical technologies in telecommunications, the expanding demand for high‑speed fiber‑optic communications, growth of data‑center and AI compute infrastructure, increasing deployment of LiDAR for autonomous driving, and the rising use of photodiode sensors across industrial automation and biomedical instrumentation.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing and largest regional market, driven by robust fiber‑optic network roll‑outs, high‑speed data transmission needs, and strong manufacturing bases for semiconductor components.

What are the emerging trends?

-> Emerging trends include advancements in short‑wave infrared photodetectors for industrial inspection and medical imaging, improvements in quantum efficiency and reduction of dark current through advanced epitaxial structures, and the integration of optoelectronic transducers with IoT platforms for smart building automation and structural health monitoring.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...