Neurostimulation (DBS, SCS, VNS) SoC Market Insights

Neurostimulation (DBS, SCS, VNS) SoC Market size was valued at USD 1.87 billion in 2025. The market is projected to grow from USD 2.03 billion in 2026 to USD 4.21 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period.

Neurostimulation System-on-Chip (SoC) solutions are highly integrated semiconductor devices purpose-built to power implantable and wearable neurostimulation therapies, including Deep Brain Stimulation (DBS), Spinal Cord Stimulation (SCS), and Vagus Nerve Stimulation (VNS). These SoCs consolidate critical functions , such as programmable pulse generation, real-time neural sensing, wireless telemetry, and power management , onto a single chip, enabling the miniaturization and energy efficiency demanded by next-generation implantable medical devices.

The market is experiencing robust growth driven by the rising global prevalence of neurological disorders, including Parkinson’s disease, epilepsy, treatment-resistant depression, and chronic pain conditions, all of which are primary indications for neurostimulation therapies. Furthermore, rapid advancements in closed-loop stimulation architectures, where the SoC both senses neural biomarkers and adaptively delivers therapy in real time, are significantly expanding the clinical value proposition of these devices. Key industry participants such as Medtronic plc, Abbott Laboratories, and Boston Scientific Corporation continue to invest heavily in next-generation SoC platforms to support their expanding neurostimulation device portfolios.

MARKET DRIVERS

Rising Global Burden of Neurological Disorders Fueling Demand for Neurostimulation SoC Solutions

The increasing global prevalence of neurological conditions such as Parkinson’s disease, epilepsy, chronic pain, and treatment-resistant depression is one of the most significant drivers propelling Neurostimulation (DBS, SCS, VNS) SoC Market. As healthcare systems worldwide face mounting pressure to address these conditions with long-term, minimally invasive solutions, implantable neurostimulation devices incorporating advanced System-on-Chip (SoC) architectures have emerged as a clinically preferred intervention. The World Health Organization estimates that neurological disorders collectively affect hundreds of millions of people globally, creating a substantial and growing patient pool that demands sophisticated, miniaturized electronic solutions embedded within deep brain stimulation, spinal cord stimulation, and vagus nerve stimulation platforms.

Technological Advancements in Low-Power SoC Architectures Accelerating Device Miniaturization

Rapid innovation in ultra-low-power SoC design is a critical catalyst for Neurostimulation (DBS, SCS, VNS) SoC Market. Semiconductor manufacturers and medical device OEMs are collaborating to develop next-generation SoCs that integrate signal processing, wireless communication, power management, and closed-loop feedback capabilities into a single chip. These advancements directly address the clinical need for smaller, lighter, and longer-lasting implantable pulse generators (IPGs). The transition from open-loop to closed-loop adaptive neurostimulation , enabled by intelligent SoC platforms capable of real-time neural signal sensing and dynamic parameter adjustment , has been a defining technological milestone, particularly in DBS systems for movement disorders.

➤ The integration of closed-loop feedback mechanisms within neurostimulation SoCs represents a paradigm shift in neuromodulation therapy, enabling devices to automatically adapt stimulation parameters in response to real-time physiological signals, thereby improving therapeutic efficacy while reducing side effects and extending battery longevity.

Favorable reimbursement landscapes in major markets, including the United States and select European Union member states, have further strengthened adoption of neurostimulation therapies. Regulatory approvals for next-generation DBS, SCS, and VNS systems by agencies such as the U.S. FDA have validated the clinical utility of SoC-enabled devices, encouraging increased capital investment from leading medical device companies. This regulatory and commercial momentum continues to reinforce the growth trajectory of Neurostimulation (DBS, SCS, VNS) SoC Market across both established and emerging geographies.

MARKET CHALLENGES

High Development Complexity and Stringent Regulatory Requirements Posing Barriers to SoC Commercialization

The development of application-specific SoCs for implantable neurostimulation devices is an extraordinarily complex engineering undertaking that demands simultaneous optimization across power consumption, biocompatibility, electromagnetic compatibility, and long-term reliability. Unlike consumer-grade semiconductor products, neurostimulation SoCs must comply with rigorous international standards including ISO 14708 for implantable devices and IEC 60601 for medical electrical equipment. The extensive pre-clinical and clinical validation timelines , often spanning several years , combined with the high cost of regulatory submissions present formidable commercialization barriers, particularly for smaller semiconductor firms and emerging device startups seeking to enter Neurostimulation (DBS, SCS, VNS) SoC Market.

Other Challenges

Cybersecurity and Data Privacy Risks in Connected Neurostimulation Devices

The increasing incorporation of wireless connectivity features such as Bluetooth Low Energy and proprietary RF protocols within neurostimulation SoC platforms introduces significant cybersecurity vulnerabilities. Implantable neurostimulation devices that transmit patient physiological data to external programmers or cloud-based monitoring platforms are potential targets for unauthorized access or signal interference. Regulatory bodies including the U.S. FDA have issued specific guidance on cybersecurity requirements for medical devices, and compliance with these evolving frameworks adds both cost and complexity to SoC development cycles withNeurostimulation (DBS, SCS, VNS) SoC Market.

Limited Availability of Specialized Engineering Talent

The intersection of neurophysiology, analog circuit design, embedded firmware development, and biomedical engineering required to design neurostimulation SoCs represents a highly specialized skill set that is in limited supply globally. This talent scarcity elongates development timelines and increases labor costs for device manufacturers and semiconductor partners, creating operational bottlenecks that challenge sustained innovation withNeurostimulation (DBS, SCS, VNS) SoC Market ecosystem.

MARKET RESTRAINTS

Elevated Device Cost and Limited Patient Access in Low- and Middle-Income Countries

One of the foremost restraints facing Neurostimulation (DBS, SCS, VNS) SoC Market is the substantial total cost associated with neurostimulation therapies, encompassing the implantable device, surgical procedure, post-operative programming, and long-term follow-up care. The sophisticated SoC components embedded within DBS, SCS, and VNS systems contribute significantly to device bill-of-materials costs, which are ultimately reflected in the high price point of commercially available systems. In low- and middle-income countries where neurological care infrastructure is underdeveloped and out-of-pocket healthcare expenditure remains the dominant payment mechanism, cost remains a prohibitive barrier that substantially limits the addressable patient population for neurostimulation therapies.

MRI Compatibility Constraints and Long-Term Device Reliability Concerns

Despite significant engineering progress, MRI compatibility remains a persistent technical and regulatory challenge for implantable neurostimulation systems containing metallic SoC packaging, leads, and electrodes. Many patients implanted with neurostimulation devices require periodic MRI imaging for ongoing neurological monitoring or for diagnosis of unrelated comorbid conditions. The risk of device heating, induced currents, and image artifact generation limits the use of standard MRI protocols in these patients, creating a clinical disadvantage relative to pharmacological alternatives. Although MRI-conditional labeling has been achieved for select DBS and SCS systems, the stringent conditions under which MRI scans are permitted continue to constrain clinical utility and may influence physician and patient preference decisions withNeurostimulation (DBS, SCS, VNS) SoC Market.

MARKET OPPORTUNITIES

Expansion of Closed-Loop and AI-Integrated SoC Platforms Opening New Therapeutic Frontiers

The convergence of artificial intelligence, machine learning, and advanced SoC design is creating transformative opportunities withNeurostimulation (DBS, SCS, VNS) SoC Market. Next-generation neurostimulation platforms are increasingly being designed around AI-capable SoC architectures that can analyze neural biomarkers in real time and autonomously optimize stimulation parameters without requiring manual clinician intervention. This capability is particularly relevant for applications in treatment-resistant depression and obsessive-compulsive disorder treated via DBS, where individualized, adaptive therapy delivery has demonstrated meaningful improvements in patient outcomes in clinical studies. Investment in AI-integrated neurostimulation SoC development is accelerating among both established medical device conglomerates and venture-backed neurotechnology startups.

Emerging Market Penetration and Expanding Therapeutic Indications Creating Untapped Revenue Potential

Regulatory and clinical expansion of approved indications for DBS, SCS, and VNS therapies presents a substantial long-term growth opportunity for Neurostimulation (DBS, SCS, VNS) SoC Market. Ongoing clinical investigations are evaluating the utility of neurostimulation across indications including Alzheimer’s disease, post-traumatic stress disorder, hypertension, heart failure, and inflammatory bowel disease , all of which could dramatically expand the commercial addressable market if supported by robust clinical evidence and subsequent regulatory approval. Simultaneously, improving economic conditions and expanding private and public health insurance coverage in high-growth markets across Asia-Pacific and Latin America are progressively improving patient access to neurostimulation therapies, creating new geographic revenue streams for SoC developers and device manufacturers operating in this space.

TrendsClosed-Loop Stimulation Architecture Emerging as a Defining Trend in Neurostimulation SoC Development

One of the most transformative trends shaping Neurostimulation (DBS, SCS, VNS) SoC Market is the rapid adoption of closed-loop stimulation architectures. Unlike conventional open-loop systems that deliver fixed stimulation parameters, closed-loop SoC platforms are engineered to simultaneously sense neural biomarkers and adaptively modulate therapy delivery in real time. This bidirectional capability , integrating high-resolution neural recording circuits alongside programmable pulse generators on a single chip , is redefining the clinical efficacy of Deep Brain Stimulation, Spinal Cord Stimulation, and Vagus Nerve Stimulation therapies. As neurological conditions such as Parkinson’s disease, epilepsy, and treatment-resistant depression demand increasingly personalized therapeutic responses, closed-loop SoC solutions are becoming the preferred design paradigm among leading device manufacturers and semiconductor developers alike.

Other Trends

Miniaturization and Power Efficiency Driving Next-Generation SoC Design

The push toward smaller, more energy-efficient implantable neurostimulation devices is placing extraordinary demands on SoC design engineering. Manufacturers are consolidating multiple critical functions , including programmable pulse generation, wireless telemetry, real-time neural sensing, and power management , onto a single highly integrated chip. This level of integration directly supports device miniaturization, extending battery longevity and improving patient comfort for long-term implantable applications. As a result, the Neurostimulation SoC market is witnessing a strong design trend toward ultra-low-power semiconductor architectures that maintain high functional performance within strict size and energy constraints.

Expanding Therapeutic Indications Broadening Market Scope

The addressable application space for Neurostimulation (DBS, SCS, VNS) SoC platforms is expanding considerably beyond historically established indications. While Parkinson’s disease, chronic pain, and epilepsy remain primary drivers, growing clinical evidence supporting neurostimulation in treatment-resistant depression, obsessive-compulsive disorder, and cardiac applications through VNS is broadening the commercial opportunity for SoC developers. This diversification of indications is encouraging semiconductor companies and medical device OEMs to develop more versatile, multi-modality SoC platforms capable of supporting varied stimulation protocols across a single hardware architecture.

Strategic Investment by Key Market Participants Accelerating SoC Innovation

Leading neurostimulation device companies, including Medtronic plc, Abbott Laboratories, and Boston Scientific Corporation, are making substantial investments in next-generation SoC platforms to maintain competitive differentiation in the evolving neurostimulation landscape. These investments are directed toward advancing wireless connectivity standards, improving sensing resolution, and enabling cloud-based remote programming capabilities , all of which place new technical requirements on underlying SoC designs. This sustained commitment from major industry participants is expected to continue driving innovation cycles withNeurostimulation (DBS, SCS, VNS) SoC Market, accelerating the commercialization of more capable and clinically intelligent implantable neurostimulation solutions.

COMPETITIVE LANDSCAPEKey Industry Players

Neurostimulation (DBS, SCS, VNS) SoC Market: Competitive Dynamics and Leading Innovators Shaping the Future of Implantable Neural Therapy Platforms

The global Neurostimulation (DBS, SCS, VNS) System-on-Chip (SoC) market is characterized by a concentrated yet rapidly evolving competitive landscape, where a handful of dominant medical device corporations command significant market share alongside a growing cohort of specialized semiconductor and neurotechnology firms. Medtronic plc remains the preeminent force in this space, leveraging its vertically integrated SoC development capabilities to power its Percept PC and next-generation DBS platforms with embedded sensing and closed-loop stimulation architectures. Abbott Laboratories, through its Neuromodulation division, has established a strong competitive position with its proprietary SoC solutions underpinning the Proclaim and Eterna SCS systems, while Boston Scientific Corporation continues to accelerate investment in adaptive neurostimulation SoC platforms to support its Vercise DBS and WaveWriter SCS portfolios. These three industry leaders collectively drive substantial R&D expenditure directed at miniaturized, ultra-low-power SoC designs capable of supporting real-time neural biomarker sensing, wireless telemetry, and rechargeable or primary cell power management within highly constrained implantable form factors.

Beyond the established device giants, a number of specialized semiconductor companies and emerging neurotechnology innovators are carving meaningful niches within the Neurostimulation SoC ecosystem. Firms such as Nevro Corp and Integer Holdings Corporation contribute specialized SoC and ASIC design competencies tailored to high-frequency SCS therapy delivery. LivaNova PLC occupies a distinctive position in the VNS segment, with proprietary SoC integration supporting its Symmetry platform for epilepsy and treatment-resistant depression indications. Meanwhile, semiconductor-focused players including Analog Devices, Inc. and Texas Instruments Incorporated supply critical mixed-signal front-end and power management SoC components extensively utilized by implantable neurostimulation device manufacturers. Emerging companies such as Nalu Medical and Saluda Medical are introducing differentiated closed-loop SoC architectures targeting next-generation SCS applications, intensifying competitive pressure on incumbent device makers and accelerating the pace of SoC innovation across the broader neurostimulation therapy landscape.

List of Key Neurostimulation (DBS, SCS, VNS) SoC Companies Profiled

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- LivaNova PLC

- Nevro Corp

- Integer Holdings Corporation

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Nalu Medical

- Saluda Medical

- Synaptics Incorporated

- Microchip Technology Inc.

- Nordic Semiconductor ASA

- Inomed Medizintechnik GmbH

- Aleva Neurotherapeutics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Deep Brain Stimulation (DBS) SoC holds a leading position within the neurostimulation SoC market owing to its increasing adoption in managing complex neurological conditions such as Parkinson’s disease and treatment-resistant depression.

|

| By Application |

|

Chronic Pain Management emerges as a dominant application segment for neurostimulation SoCs, particularly driven by the expansive use of Spinal Cord Stimulation in addressing refractory chronic pain conditions that are unresponsive to conventional pharmacological therapies.

|

| By End User |

|

Hospitals & Neurology Centers represent the primary end-user segment for neurostimulation SoC-powered devices, serving as the principal sites for implantation procedures, post-operative programming, and long-term therapeutic management.

|

| By Architecture |

|

Closed-Loop (Adaptive) SoC is rapidly gaining prominence as the most transformative and clinically differentiated architecture within the neurostimulation SoC landscape, reflecting a paradigm shift from static to dynamic, biomarker-responsive therapy delivery.

|

| By Device Type |

|

Fully Implantable Devices constitute the dominant device type segment, driven by their established clinical track record, superior patient convenience, and the increasing miniaturization capabilities enabled by advanced SoC integration.

|

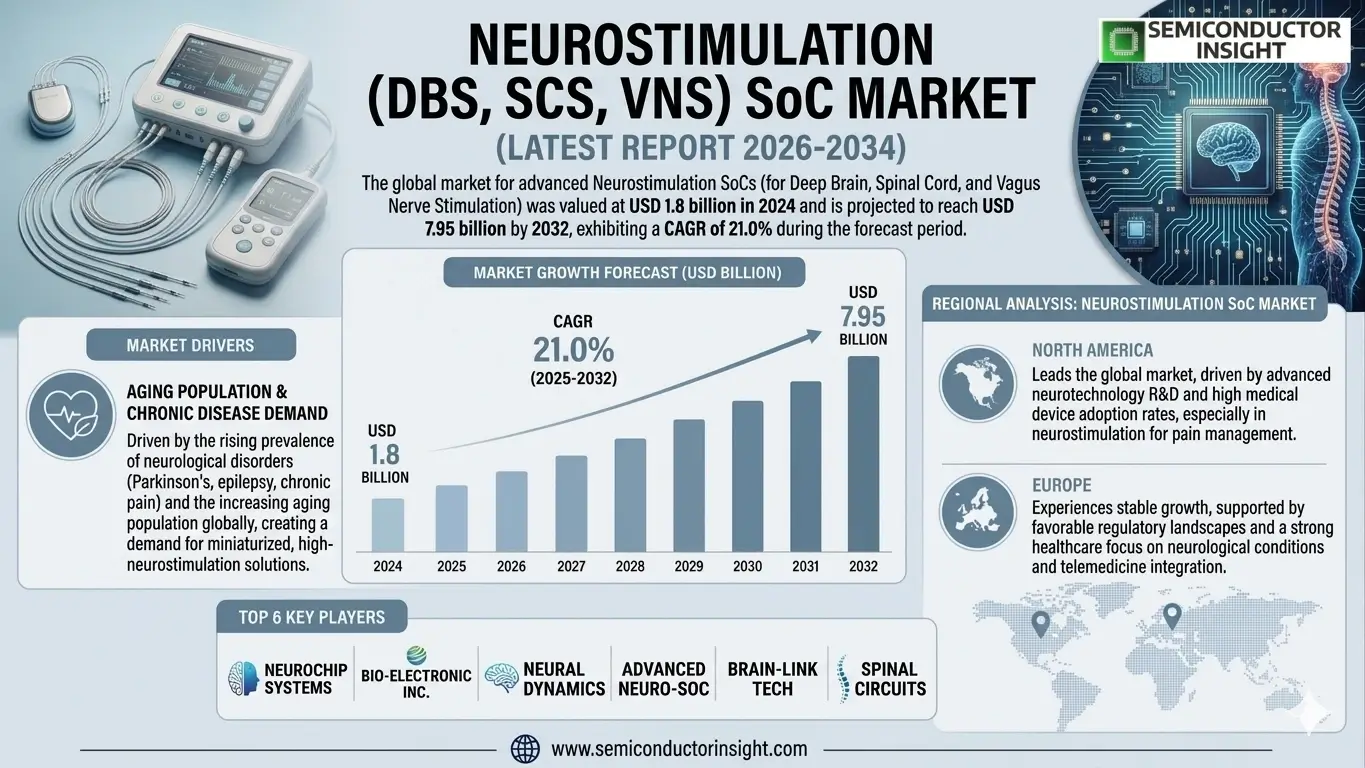

Regional Analysis: Neurostimulation (DBS, SCS, VNS) SoC Market

North America

North America’s well-structured regulatory environment, led by the FDA’s breakthrough device designation program, provides neurostimulation SoC developers with an accelerated approval route. Comprehensive Medicare and private insurance reimbursement policies for DBS, SCS, and VNS procedures significantly reduce financial barriers for patients, sustaining consistent clinical adoption and driving steady demand for advanced implantable SoC platforms across the region.

The region hosts a dense concentration of neurotechnology startups, established medtech corporations, and university-affiliated research centers actively advancing closed-loop neurostimulation architectures. Collaborative initiatives between semiconductor developers and device manufacturers are yielding ultra-low-power SoC designs capable of real-time neural signal processing, positioning North America as the primary source of technological breakthroughs Global Neurostimulation (DBS, SCS, VNS) SoC Market.

Rising prevalence of neurological conditions including Parkinson’s disease, chronic refractory pain, and drug-resistant epilepsy is fueling patient-driven demand for neurostimulation therapies across North America. Increased neurologist engagement, expanded patient advocacy networks, and digital health awareness campaigns are collectively shortening the diagnostic-to-treatment timeline, accelerating implantation rates of DBS, SCS, and VNS devices embedded with advanced SoC components.

North America’s Neurostimulation (DBS, SCS, VNS) SoC Market is characterized by a wave of strategic mergers, acquisitions, and co-development agreements between semiconductor firms and neuromodulation device makers. These alliances are enabling rapid integration of wireless connectivity, on-chip machine learning algorithms, and adaptive stimulation capabilities into next-generation implantable systems, reinforcing the region’s long-term competitive advantage in the global marketplace.

Europe

Europe represents the second-largest contributor to Global Neurostimulation (DBS, SCS, VNS) SoC Market, underpinned by a mature healthcare system, favorable CE marking pathways, and strong governmental support for neuroscience research initiatives. Countries such as Germany, France, the United Kingdom, and the Netherlands are at the forefront of clinical neurostimulation adoption, supported by nationally funded brain research programs and well-resourced academic medical centers. The European market benefits from a growing aging population susceptible to neurological conditions, which is generating sustained demand for DBS, SCS, and VNS-based interventions. Additionally, the European Medical Device Regulation framework, while stringent, is fostering the development of higher-quality and safer SoC-integrated neurostimulation products. Cross-border research collaborations facilitated by EU-funded Horizon programs are further advancing miniaturized, adaptive SoC architectures. Europe’s emphasis on patient safety, device interoperability, and long-term clinical outcomes continues to shape the regional market’s innovation trajectory and competitive dynamics through 2034.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market withGlobal Neurostimulation (DBS, SCS, VNS) SoC Market, driven by rapidly expanding healthcare infrastructure, rising neurological disease burden, and increasing government investments in advanced medical technology. China, Japan, South Korea, and India are the primary growth engines, each demonstrating distinct market dynamics. China is scaling domestic neurostimulation device manufacturing capabilities and advancing indigenous SoC development programs aligned with its broader healthcare modernization agenda. Japan’s aging demographic profile and sophisticated neuro-surgical expertise create a favorable environment for premium DBS and SCS device adoption. India, while at an earlier stage of market maturity, is witnessing growing awareness among neurologists and patients regarding advanced neurostimulation therapies. Rising medical tourism, expanding private hospital networks, and favorable foreign direct investment policies across the region are collectively accelerating market penetration of neurostimulation SoC-integrated devices through the forecast period.

South America

South America occupies a developing but progressively important position Global Neurostimulation (DBS, SCS, VNS) SoC Market, with Brazil and Argentina leading regional adoption of neurostimulation therapies. Brazil’s relatively advanced private healthcare sector and growing number of specialized neurology centers are facilitating increased access to DBS and SCS procedures, primarily among higher-income patient segments. Government-led public health investments targeting chronic neurological conditions are beginning to create incremental demand for cost-effective neurostimulation SoC solutions adapted to the region’s economic realities. Regulatory harmonization efforts aligned with international medical device standards are gradually improving market entry conditions for global neurostimulation device manufacturers. However, challenges related to reimbursement limitations, economic volatility, and uneven healthcare access across rural and urban populations continue to moderate the pace of market expansion. Despite these constraints, South America presents meaningful long-term growth potential as healthcare modernization progresses across the region toward 2034.

Middle East & Africa

The Middle East & Africa region currently represents the nascent frontier of Global Neurostimulation (DBS, SCS, VNS) SoC Market, characterized by significant untapped potential alongside structural challenges in healthcare access and infrastructure development. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are leading the region’s engagement with advanced neurostimulation therapies, supported by high healthcare expenditure, medical tourism initiatives, and strategic investments in world-class hospital facilities. Vision 2030-aligned healthcare development programs in Saudi Arabia are creating a conducive environment for the adoption of sophisticated neurostimulation devices integrated with advanced SoC platforms. In contrast, sub-Saharan African markets remain at very early stages of neurostimulation awareness and clinical infrastructure development. Across the broader region, growing partnerships between governments and international medtech organizations are gradually building the clinical and regulatory foundations necessary to support wider adoption of DBS, SCS, and VNS technologies through the 2026–2034 forecast horizon.

Report Scope

This market research report provides a comprehensive analysis of the Neurostimulation (DBS, SCS, VNS) SoC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Neurostimulation (DBS, SCS, VNS) SoC Market?

-> Global Neurostimulation (DBS, SCS, VNS) SoC Market was valued at USD 1.87 billion in 2025 and is expected to reach USD 4.21 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period 2026–2034.

Which key companies operate Neurostimulation (DBS, SCS, VNS) SoC Market?

-> Key players include Medtronic plc, Abbott Laboratories, and Boston Scientific Corporation, among others, all of which continue to invest heavily in next-generation SoC platforms to support their expanding neurostimulation device portfolios.

What are the key growth drivers?

-> Key growth drivers include the rising global prevalence of neurological disorders such as Parkinson’s disease, epilepsy, treatment-resistant depression, and chronic pain conditions, along with rapid advancements in closed-loop stimulation architectures and the miniaturization enabled by highly integrated SoC solutions.

Which region dominates the market?

-> North America holds a significant share of Neurostimulation (DBS, SCS, VNS) SoC Market, while Asia-Pacific is emerging as a fast-growing region driven by increasing healthcare investments and growing awareness of neurostimulation therapies.

What are the emerging trends?

-> Emerging trends include closed-loop stimulation architectures, real-time neural sensing, wireless telemetry integration, and the consolidation of programmable pulse generation and power management onto a single chip, enabling next-generation implantable and wearable neurostimulation medical devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...