Multi-Patterning (LELE, SADP, SAQP) Market Insights

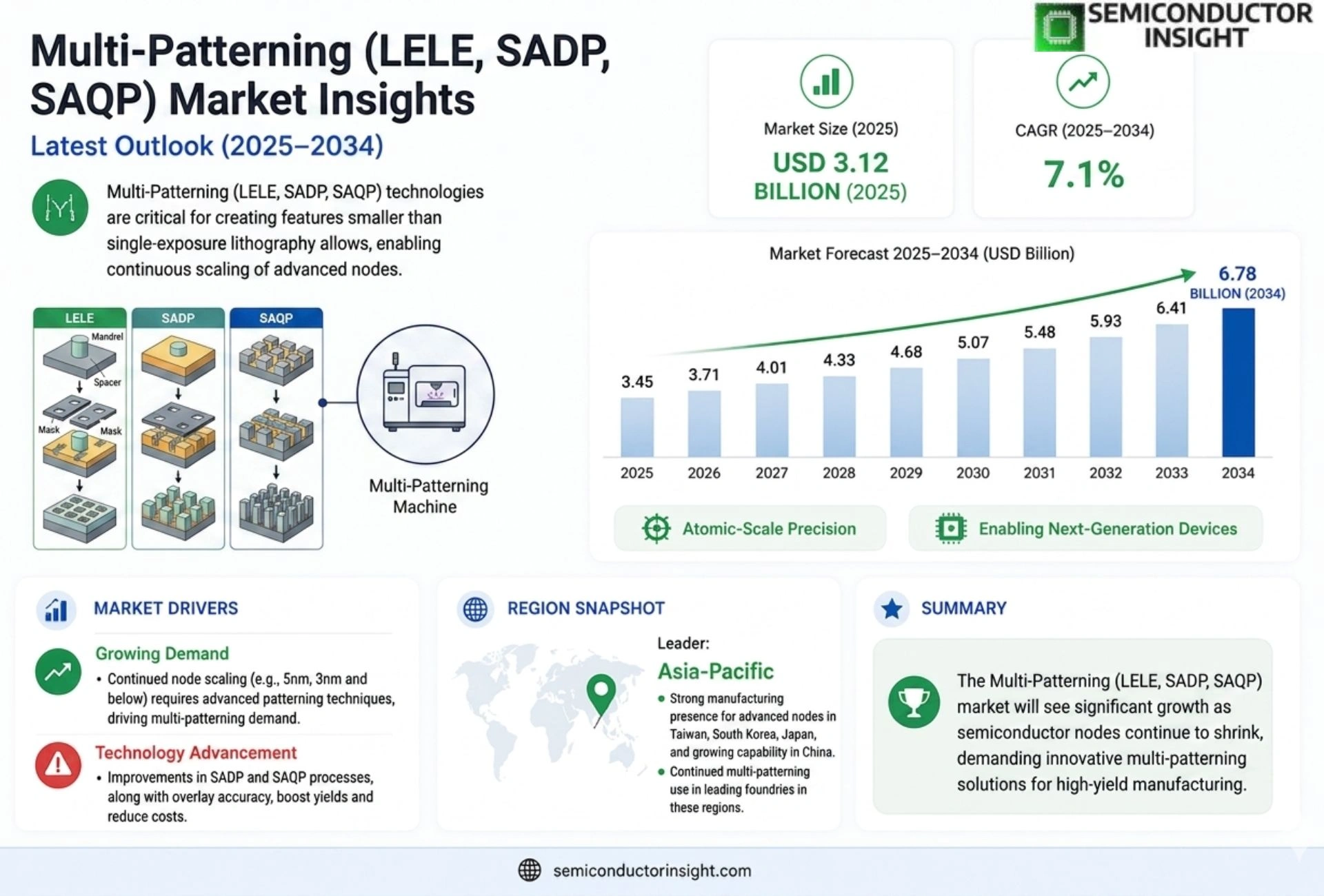

Global Multi-Patterning (LELE, SADP, SAQP) market size was valued at USD 3.12 billion in 2025. The market is projected to grow from USD 3.45 billion in 2025 to USD 6.78 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Multi-patterning comprises advanced lithographic techniques,Litho‑Epitaxy‑Litho‑Epitaxy (LELE), Self‑Aligned Double Patterning (SADP), and Self‑Aligned Quadruple Patterning (SAQP),that enable sub‑10 nm feature placement on semiconductor wafers by sequentially stacking patterned layers.

The market is accelerating because semiconductor manufacturers are pushing toward sub‑7 nm nodes while seeking cost‑effective alternatives to extreme ultraviolet (EUV). Moreover, rising demand for high‑performance computing and AI accelerators fuels adoption of LELE and SADP processes. Recent collaborations such as the March 2024 partnership between Samsung Foundry and imec on EUV‑assisted multi-patterning illustrate industry momentum. Key players,including ASML Holding, TEL (Tokyo Electron), and TSMC,continue expanding their portfolios through technology licensing and equipment upgrades.

MARKET DRIVERS

Advancements in Lithography Technology

The ongoing shift to sub‑10 nm nodes has intensified demand for Multi-Patterning (LELE, SADP, SAQP) Market solutions that can extend the capabilities of existing immersion lithography equipment. Recent introductions of high‑NA EUV sources have created a hybrid environment where advanced patterning techniques remain essential for cost‑effective volume production.

Rising Semiconductor Demand

Growth in high‑performance computing, AI accelerators, and 5G infrastructure is driving wafer counts upward, compelling manufacturers to adopt Multi-Patterning (LELE, SADP, SAQP) Market workflows that improve yield and pattern fidelity on dense logic layers.

➤ “Adoption of SADP and SAQP is projected to exceed 60 % of logic device productions by 2028, reinforcing their strategic importance.”

These drivers collectively reinforce the economic case for investing in robust multiple‑patterning stacks, positioning Multi-Patterning (LELE, SADP, SAQP) Market for sustained expansion.

MARKET CHALLENGES

Complex Process Integration

Integrating multiple‑patterning steps adds overlay complexity and stochastic variations, requiring sophisticated metrology and defect control. Companies often face steep learning curves to align process windows across LELE, SADP, and SAQP stages without compromising throughput.

Other Challenges

Cost Management

The additional masks and process steps increase per‑wafer costs, forcing fabs to balance price competitiveness with the performance gains offered by Multi-Patterning (LELE, SADP, SAQP) Market.

MARKET RESTRAINTS

Equipment Capital Expenditure

High upfront investment for dedicated imprint and etch tools limits rapid adoption, especially among smaller foundries. The need to amortize equipment over sufficient volume can restrain market momentum until production ramps reach economically viable levels.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging

Advanced packaging technologies such as fan‑out wafer‑level packaging (FOWLP) and 3D‑IC stacking are creating new patterning requirements. Leveraging Multi-Patterning (LELE, SADP, SAQP) Market expertise in these domains offers a pathway to diversify revenue streams and capture growth beyond traditional logic nodes.

Trends

Accelerated Adoption Fueled by Sub‑7 nm Node Demand

The semiconductor industry is rapidly moving toward sub‑7 nm process nodes, and advanced lithographic stacks such as LELE, SADP and SAQP have become essential enablers. By sequentially applying patterned layers, these techniques maintain critical dimension control while avoiding the steep cost of extreme‑ultraviolet (EUV) tools. Leading foundries report that the shift to multi‑patterning reduces cycle time for high‑density designs, allowing design teams to meet aggressive performance targets for AI accelerators and high‑performance computing platforms. As a result, Multi-Patterning (LELE, SADP, SAQP) Market is experiencing a noticeable lift in new equipment orders and technology licensing agreements throughout 2024‑2025.

Other Trends

Technology Collaboration Highlights

Strategic partnerships are accelerating knowledge transfer across the ecosystem. In March 2024, Samsung Foundry and imec announced a joint program that integrates EUV‑assisted patterning with traditional multi‑patterning flows, shortening the validation period for new nodes. Similar collaborations between ASML and TSMC focus on next‑generation exposure systems that improve overlay accuracy for SAQP steps. These alliances not only streamline R&D costs but also create a shared pool of best practices that speed up industrial adoption, reinforcing the overall health of the market.

Cost‑Effective Alternatives to EUV

Despite the promise of EUV, many fab operators consider it a capital‑intensive option for mid‑range product lines. Multi‑patterning provides a pragmatic path by leveraging existing deep‑ultraviolet (DUV) infrastructure while still achieving sub‑10 nm feature placement. Equipment upgrades that enhance resist sensitivity and improve alignment precision have lowered the total cost of ownership for LELE and SADP processes. Consequently, manufacturers are extending the lifecycle of their DUV suites, balancing profitability with technological relevance. This cost‑driven momentum is expected to sustain demand for multi‑patterning solutions well into the next decade, underpinning a stable trajectory for the overall market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in Multi-Patterning (LELE, SADP, SAQP)

The global Multi-Patterning (LELE, SADP, SAQP) market was valued at approximately USD 3.12 billion in 2025 and is projected to expand to USD 6.78 billion by 2034, reflecting a robust CAGR of 7.1 percent. This growth is propelled by semiconductor manufacturers’ relentless push toward sub‑7 nm nodes, where extreme‑ultraviolet (EUV) lithography remains cost‑prohibitive for many customers. Multi‑patterning techniques,Litho‑Epitaxy‑Litho‑Epitaxy (LELE), Self‑Aligned Double Patterning (SADP), and Self‑Aligned Quadruple Patterning (SAQP),deliver sub‑10 nm critical dimensions by stacking patterned layers, enabling high‑performance computing and AI accelerator production. The market leadership is anchored by a handful of equipment and service providers that combine mature process know‑how with aggressive technology licensing. ASML Holding’s advanced exposure tools, paired with its EUV‑assisted multi‑patterning roadmap, remain a decisive advantage, while Tokyo Electron (TEL) leverages its extensive portfolio of etch and deposition platforms to support end‑to‑end LELE and SADP flows. TSMC’s scale and early adoption of SAQP for advanced logic nodes further reinforce the oligopolistic structure, encouraging downstream fabs to align their roadmaps with these tier‑one innovators.

Competitive pressure intensifies as foundries such as Samsung Foundry and imec deepen collaborations to accelerate EUV‑assisted multi‑patterning, exemplified by their March 2024 partnership that combines Samsung’s high‑volume manufacturing capacity with imec’s process‑integration expertise. Intel and GlobalFoundries are investing heavily in in‑house multi‑patterning R&D to reduce reliance on external tool suppliers, while Applied Materials and Lam Research differentiate through novel deposition and etch chemistries that improve overlay accuracy and yield. Smaller but technically agile players,including Nikon, Canon Nanotechnologies, UMC, SMIC, IBM Semiconductor, and Micron Technology,focus on niche segments such as 3D‑IC packaging and specialty memory, where tailored multi‑patterning solutions can command premium pricing. The overall landscape suggests a tiered ecosystem: tier‑one equipment giants dominate technology licensing, tier‑two foundries drive volume adoption, and niche innovators capture specialized applications, all converging on a market trajectory that is likely to outpace the broader semiconductor equipment sector.

List of Key Multi-Patterning Companies Profiled

- ASML Holding

- Tokyo Electron (TEL)

- Samsung Foundry

- imec

- TSMC

- Intel

- GlobalFoundries

- Applied Materials

- Lam Research

- Nikon

- Canon Nanotechnologies

- UMC

- SMIC

- IBM Semiconductor

- Micron Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

LELE

|

| By Application |

|

Logic Devices

|

| By End User |

|

Foundries

|

| By Process Node |

|

Sub‑7nm

|

| By Industry Vertical |

|

AI Accelerators

|

Regional Analysis:

United States

The electronics sector in the US is a primary driver for Multi-Patterning (LELE, SADP, SAQP) adoption, with increasing demand for smaller, more efficient components. This trend necessitates advanced patterning techniques to achieve the required precision and performance levels.

The US boasts a strong presence in the optical and photonics industry, where Multi-Patterning (LELE, SADP, SAQP) plays a crucial role in creating high-performance optical devices and components. Research into advanced materials and fabrication processes is fueling innovation in this segment.

Multi-Patterning (LELE, SADP, SAQP) techniques are increasingly utilized in the development of specialty coatings with enhanced properties. This application area is driven by the demand for tailored surface functionalities and improved material performance.

The aerospace and defense sectors in the US are exploring the potential of Multi-Patterning (LELE, SADP, SAQP) for advanced components and systems, focusing on reliability and performance under extreme conditions.

Europe

Europe presents a mature and technologically advanced market for Multi-Patterning (LELE, SADP, SAQP). Driven by stringent quality standards and a focus on sustainable manufacturing, the adoption of these technologies is steadily increasing across various industries. The region’s strong chemical and materials science base provides a fertile ground for innovation and development in this area. Businesses are actively investing in research and development to optimize Multi-Patterning (LELE, SADP, SAQP) processes for enhanced efficiency and cost-effectiveness. The emphasis on environmental regulations also influences the development of more eco-friendly patterning solutions. Europe’s commitment to advanced manufacturing further reinforces its position as a key market for these sophisticated techniques.

Asia-Pacific

The Asia-Pacific region, particularly countries like China, Japan, and South Korea, is emerging as a rapidly growing market for Multi-Patterning (LELE, SADP, SAQP). This growth is fueled by the expansion of electronics manufacturing, increasing investment in research and development, and a supportive government environment. The demand for smaller, more powerful electronic devices is driving the adoption of advanced patterning technologies. Businesses in the region are focusing on cost-effective solutions while maintaining high performance standards. The Asia-Pacific market is characterized by intense competition and a dynamic innovation landscape, presenting both opportunities and challenges for players in the Multi-Patterning (LELE, SADP, SAQP) space.

South America

South America represents a developing market for Multi-Patterning (LELE, SADP, SAQP), with significant potential for growth in the coming years. The expansion of the electronics and manufacturing sectors in countries like Brazil and Argentina is driving demand for these advanced patterning solutions. While adoption rates are currently lower compared to other regions, the market is expected to witness increasing investment in research and development and infrastructure development. Businesses are focusing on providing tailored solutions to meet the specific needs of the regional market, with an emphasis on cost-effectiveness and local support.

Middle East & Africa

The Middle East and Africa region presents a nascent but promising market for Multi-Patterning (LELE, SADP, SAQP). The growth of the technology sector, coupled with increasing investments in infrastructure development, is creating opportunities for the adoption of these advanced patterning technologies. While the market is still in its early stages of development, the potential for growth is significant, particularly in industries like aerospace, defense, and specialty materials. Businesses are expected to focus on establishing partnerships and providing customized solutions to cater to the specific requirements of this emerging market.

Report Scope

This market research report provides a comprehensive analysis of the Multi-Patterning (LELE, SADP, SAQP) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Multi-Patterning (LELE, SADP, SAQP) Market?

-> Multi-Patterning (LELE, SADP, SAQP) market size was valued at USD 3.12 billion in 2025. The market is projected to grow from USD 3.45 billion in 2025 to USD 6.78 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Which key companies operate Multi-Patterning (LELE, SADP, SAQP) Market?

-> Key players include ASML Holding, Tokyo Electron (TEL), and TSMC, among others.

What are the key growth drivers?

-> Key growth drivers include the push toward sub‑7 nm nodes, the search for cost‑effective alternatives to EUV lithography, and rising demand for high‑performance computing and AI accelerators.

Which region dominates the market?

-> The reference does not specify a single dominant region; market activity is strongly linked to major semiconductor hubs worldwide.

What are the emerging trends?

-> Emerging trends include EUV‑assisted multi‑patterning collaborations, integration of AI‑driven process optimization, and the development of advanced LELE, SADP, and SAQP techniques for sub‑10 nm patterning.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...