MEMS Mirror (Lidar Scanning, Projection) Market Insights

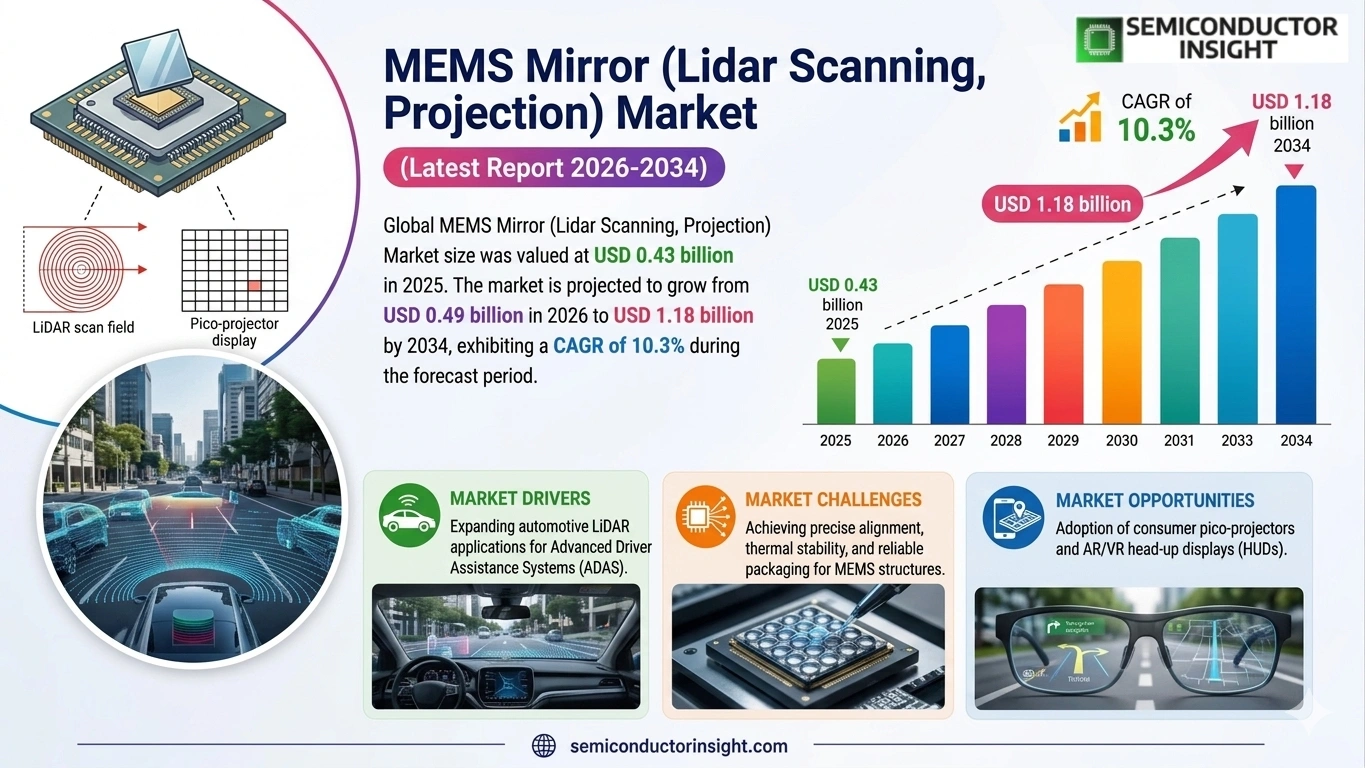

MEMS Mirror (Lidar Scanning, Projection) Market size was valued at USD 0.43 billion in 2025. The market is projected to grow from USD 0.49 billion in 2026 to USD 1.18 billion by 2034, exhibiting a CAGR of 10.3% during the forecast period.

MEMS mirrors are micro-electromechanical systems-based optical components that enable precise, high speed beam steering for applications in LiDAR scanning, laser projection, and optical sensing. These miniaturized mirror devices utilize electrostatic, electromagnetic, or piezoelectric actuation mechanisms to deflect light beams with exceptional accuracy. Key product types include 1D scanning mirrors, 2D scanning mirrors, and gimbal-based mirror arrays, which serve a broad range of end-use applications spanning autonomous vehicles, consumer electronics, industrial automation, and augmented reality displays.

The market is experiencing robust expansion driven by surging adoption of LiDAR technology in autonomous and advanced driver-assistance systems (ADAS), growing integration of pico-projection modules in portable devices, and rising investments in smart infrastructure. Furthermore, the increasing deployment of solid-state LiDAR solutions which rely heavily on MEMS mirror technology for compact, reliable beam scanning is accelerating demand. Key players operating in this space include Mirrorcle Technologies, Hamamatsu Photonics, STMicroelectronics, Maradin, and Preciseley Microtechnology, each maintaining diversified product portfolios addressing both scanning and projection segments.

MARKET DRIVERS

Accelerating Adoption of LiDAR in Autonomous Vehicles and Advanced Driver Assistance Systems

MEMS Mirror (Lidar Scanning, Projection) Market is experiencing robust growth momentum, driven primarily by the rapid integration of LiDAR technology in autonomous vehicles and advanced driver assistance systems (ADAS). MEMS-based scanning mirrors offer a compelling combination of compact form factor, low power consumption, and high scanning speeds that make them particularly well-suited for automotive-grade LiDAR sensors. As automakers and Tier-1 suppliers accelerate their transition toward higher levels of vehicle autonomy, the demand for reliable, miniaturized LiDAR scanning components has intensified considerably. The shift from mechanical spinning LiDAR systems to solid-state and MEMS-based architectures is a defining trend reshaping the competitive landscape of this market.

Expanding Use of Pico Projection and Augmented Reality Display Technologies

Beyond automotive applications, MEMS mirror technology is playing an increasingly critical role in the projection and display segment, particularly within laser beam scanning (LBS) projectors and augmented reality (AR) headsets. Consumer electronics manufacturers and enterprise AR solution providers are leveraging MEMS mirrors to achieve ultra-compact projection modules with high brightness and resolution. The growing consumer appetite for immersive display experiences, combined with the miniaturization requirements of wearable AR devices, is creating sustained demand for high-performance MEMS scanning mirrors. Industrial applications such as barcode scanning, 3D sensing, and medical imaging further broaden the addressable market for MEMS mirror components.

➤ The convergence of LiDAR scanning and AR projection applications is establishing MEMS mirror technology as a critical enabling component across multiple high-growth industries, reinforcing long-term demand visibility for market participants.

Government investments in smart infrastructure, autonomous mobility programs, and defense-grade sensing systems are also functioning as significant demand catalysts for MEMS Mirror (Lidar Scanning, Projection) Market. Defense and aerospace agencies are increasingly evaluating MEMS-based LiDAR scanning solutions for unmanned aerial vehicles (UAVs) and terrain-mapping applications, where size, weight, and power (SWaP) constraints are critical design parameters. This multi-sector demand diversification is reducing the market’s reliance on any single end-use industry and is contributing to a more resilient and sustained growth trajectory.

MARKET CHALLENGES

Technical Complexity in Achieving High Angular Resolution and Reliability Across Operating Conditions

One of the foremost challenges confronting MEMS Mirror (Lidar Scanning, Projection) Market is the considerable technical difficulty involved in achieving high angular resolution and consistent optical performance across a broad range of operating temperatures and environmental conditions. MEMS mirrors are susceptible to thermomechanical stress, which can introduce pointing errors and affect long-term reliability a particularly critical concern for automotive LiDAR applications where functional safety standards such as ISO 26262 mandate stringent performance guarantees. Balancing the competing requirements of scan angle, resonant frequency, mirror size, and optical flatness within tightly constrained die areas remains a non-trivial engineering challenge for MEMS foundries and system integrators alike.

Other Challenges

High Fabrication and Testing Costs

The specialized cleanroom processes required for MEMS mirror fabrication, including deep reactive-ion etching (DRIE) and wafer-level packaging, contribute to elevated per-unit costs at lower production volumes. Achieving the economies of scale necessary to make MEMS-based LiDAR commercially viable for mass-market automotive deployment requires significant capital investment and close collaboration between semiconductor foundries and system-level OEMs. The cost of comprehensive optical and reliability testing further adds to overall production expenses, creating margin pressure particularly for smaller market entrants.

Ecosystem Fragmentation and Standardization Gaps

MEMS Mirror (Lidar Scanning, Projection) Market currently lacks unified performance benchmarks and interface standards, resulting in fragmented supply chains and interoperability challenges. LiDAR system integrators often need to develop highly customized driver electronics and control algorithms tailored to specific MEMS mirror suppliers, increasing design-in complexity and time-to-market. The absence of widely adopted industry standards for key parameters such as scan linearity, mirror flatness specifications, and failure mode definitions complicates procurement decisions for OEMs seeking to qualify multiple sources.

MARKET RESTRAINTS

Competition from Alternative Solid-State LiDAR Scanning Architectures

A significant restraint on MEMS Mirror (Lidar Scanning, Projection) Market is the intensifying competition from alternative solid-state scanning technologies, including optical phased arrays (OPAs) and Flash LiDAR systems. OPA-based LiDAR platforms, while still largely in the research and early commercialization phase, promise beam steering without any moving parts, which is an appealing proposition for automotive and industrial customers prioritizing long-term mechanical reliability. Flash LiDAR systems, which illuminate an entire scene simultaneously rather than scanning point-by-point, offer different performance trade-offs that may be preferred in certain short-range sensing applications. The existence of these competing architectures introduces uncertainty into procurement decisions and may constrain the pace of MEMS mirror adoption in some segments.

Supply Chain Vulnerabilities and Semiconductor Capacity Constraints

MEMS Mirror (Lidar Scanning, Projection) Market is also restrained by ongoing vulnerabilities in the global semiconductor supply chain. MEMS mirror fabrication relies on specialized process nodes and equipment that are concentrated among a limited number of foundry partners worldwide. Periodic capacity constraints, geopolitical trade tensions affecting semiconductor supply chains, and the long qualification cycles required for automotive-grade MEMS components can create supply disruptions that impede market scalability. Fabless MEMS mirror companies face particular exposure to these risks, as they are dependent on third-party foundry partners for manufacturing capacity. These structural supply chain considerations represent a persistent, if manageable, restraint on the market’s near-to-medium term growth potential.

MARKET OPPORTUNITIES

Growth of Industrial Automation, Robotics, and Smart Factory Applications

The accelerating adoption of industrial automation, collaborative robotics, and smart factory solutions presents a substantial and underexploited opportunity for MEMS Mirror (Lidar Scanning, Projection) Market. Factory automation platforms increasingly rely on LiDAR-based environment perception for mobile robot navigation, obstacle detection, and precision assembly operations. MEMS scanning mirrors, with their compact dimensions and programmable scan patterns, are well-positioned to address the diverse sensing requirements of next-generation industrial robotics platforms. As manufacturers across automotive, electronics, logistics, and pharmaceutical sectors continue to invest in automation infrastructure, the industrial segment is expected to emerge as a meaningful incremental demand driver for MEMS mirror components.

Integration of MEMS LiDAR in Consumer Electronics and Smart Home Devices

The consumer electronics sector represents a nascent but promising opportunity for MEMS mirror technology, particularly as smart home devices, robotic vacuum cleaners, and gaming peripherals begin incorporating LiDAR-based spatial sensing for enhanced functionality. The cost-reduction trajectory of MEMS mirror components, driven by increasing production volumes and ongoing process optimization, is gradually making LiDAR integration economically viable in mid-range consumer devices. Additionally, the growing deployment of AR-enabled smart glasses and heads-up display systems by consumer technology companies is expected to generate sustained demand for high-performance MEMS scanning mirrors optimized for laser beam scanning projection engines, creating a parallel high-growth opportunity stream alongside the automotive and industrial segments of MEMS Mirror (Lidar Scanning, Projection) Market.

MEMS Mirror (Lidar Scanning, Projection) Market Trends

Rising Adoption of LiDAR Technology in Autonomous Vehicles and ADAS Drives MEMS Mirror Demand

MEMS Mirror (Lidar Scanning, Projection) Market is experiencing a significant upward trajectory, largely propelled by the accelerating integration of LiDAR systems within autonomous vehicles and advanced driver-assistance systems (ADAS). MEMS mirror technology offers compact form factors, high scanning speeds, and precise beam deflection capabilities attributes that are essential for next-generation automotive sensing platforms. As vehicle manufacturers and technology developers intensify their focus on safety and automation, demand for reliable, miniaturized beam-steering solutions continues to strengthen across the automotive value chain.

Other Trends

Shift Toward Solid-State LiDAR Solutions

A notable trend reshaping MEMS Mirror (Lidar Scanning, Projection) Market is the growing industry preference for solid-state LiDAR architectures. Unlike traditional mechanical LiDAR systems, solid-state variants depend on MEMS mirrors for compact, durable, and cost-effective beam scanning. This transition is encouraging manufacturers to invest in advanced MEMS fabrication processes, including electrostatic and piezoelectric actuation mechanisms, to achieve higher angular resolution and improved thermal stability in scanning mirror devices.

Expansion of Pico-Projection Modules in Consumer Electronics

The growing integration of pico-projection modules within smartphones, wearables, and portable devices represents another influential trend in MEMS Mirror (Lidar Scanning, Projection) Market. Miniaturized 2D scanning mirrors are increasingly embedded within laser projection engines to enable compact display solutions for augmented reality headsets and portable projectors. Consumer electronics manufacturers are collaborating with MEMS component suppliers to optimize optical performance while maintaining low power consumption, reflecting a broader industry push toward multifunctional, space-efficient devices.

Growing Investments in Smart Infrastructure and Industrial Automation

Beyond automotive and consumer segments, the MEMS Mirror market is witnessing rising demand from industrial automation and smart infrastructure applications. MEMS-based optical scanning systems are being deployed in machine vision, 3D mapping, and object detection platforms used across manufacturing and logistics environments. Investments in Industry 4.0 initiatives are fostering broader adoption of LiDAR-enabled sensing technologies, where MEMS mirrors serve as a critical enabler for precision and reliability.

Augmented Reality Displays Emerging as a High-Growth Application Segment

Augmented reality display systems are emerging as a compelling growth avenue within MEMS Mirror (Lidar Scanning, Projection) Market. Gimbal-based mirror arrays and 2D scanning mirrors are finding increasing application in AR waveguide displays and holographic projection systems. Key players such as Mirrorcle Technologies, Hamamatsu Photonics, STMicroelectronics, Maradin, and Preciseley Microtechnology are actively expanding their product portfolios to address both scanning and projection segments, ensuring the market remains well-positioned to capitalize on evolving end-user requirements across multiple industries.

COMPETITIVE LANDSCAPE

Key Industry Players

MEMS Mirror (LiDAR Scanning, Projection) Market Competitive Dynamics and Leading Manufacturer Profiles

The global MEMS Mirror market for LiDAR scanning and projection applications is characterized by a moderately consolidated competitive landscape, with a mix of specialized MEMS component manufacturers, photonics conglomerates, and vertically integrated semiconductor firms vying for strategic positioning. Hamamatsu Photonics and STMicroelectronics stand out as dominant incumbents, leveraging their expansive R&D infrastructure, established global distribution networks, and broad optical and semiconductor portfolios to capture significant market share across both the LiDAR scanning and laser projection segments. These companies benefit from long-standing relationships with Tier-1 automotive suppliers and consumer electronics OEMs, providing a durable competitive advantage as demand for solid-state LiDAR and compact projection modules accelerates.

Beyond the market leaders, a robust cohort of niche specialists and emerging innovators is intensifying competition across the MEMS mirror value chain. Mirrorcle Technologies has carved a strong position in high-performance 2D MEMS mirror systems targeting LiDAR and biomedical sensing applications, while Maradin and Preciseley Microtechnology focus on miniaturized scanning solutions for augmented reality and autonomous vehicle platforms. Companies such as Bosch Sensortec, Infineon Technologies, and Texas Instruments bring deep MEMS fabrication expertise and semiconductor-scale manufacturing capabilities, enabling cost-competitive volume production. Meanwhile, Sunny Optical Technology and II-VI Incorporated (now Coherent Corp.) are expanding their photonics and optical MEMS capabilities through targeted acquisitions and strategic partnerships, further elevating competitive intensity across the LiDAR and projection sub-segments.

List of Key MEMS Mirror Companies Profiled

- Hamamatsu Photonics K.K.

- STMicroelectronics

- Mirrorcle Technologies

- Maradin

- Preciseley Microtechnology Corporation

- Bosch Sensortec GmbH

- Infineon Technologies AG

- Texas Instruments Incorporated

- Coherent Corp. (formerly II-VI Incorporated)

- Sunny Optical Technology Group Co., Ltd.

- Sercalo Microtechnology Ltd.

- Opus Microsystems Corporation

- Fraunhofer IPMS

- OmniVision Technologies

- Jenoptik AG

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

2D Scanning MEMS Mirrors represent the leading segment within the product type landscape, driven by their unmatched versatility across both LiDAR scanning and projection applications.

|

| By Application |

|

LiDAR Scanning for Autonomous Vehicles and ADAS stands as the most prominent application segment, propelled by intensifying global investments in self-driving technology and smart mobility infrastructure.

|

| By End User |

|

Automotive and Transportation constitutes the dominant end-user segment for MEMS mirror technology, reflecting the accelerating global transition toward vehicle autonomy and intelligent mobility ecosystems.

|

| By Actuation Technology |

|

Electrostatic Actuation holds the leading position within the actuation technology landscape, owing to its well-established compatibility with standard semiconductor fabrication processes and its ability to deliver precise, low-power beam deflection.

|

| By Integration Level |

|

Integrated MEMS Mirror Modules represent the fastest-growing category by integration level, as system designers across automotive, AR, and industrial verticals increasingly seek ready-to-deploy optical sub-assemblies that reduce design complexity and accelerate time-to-market.

|

Regional Analysis: MEMS Mirror (Lidar Scanning, Projection) Market

North America

The United States defense sector represents a significant and stable consumer of MEMS Mirror technology for lidar-based targeting, terrain mapping, and UAV navigation systems. Defense agencies continue to fund research into ruggedized micro-mirror arrays capable of operating in extreme environmental conditions. This consistent government procurement pipeline provides North American MEMS Mirror manufacturers with a competitive advantage and a reliable revenue base.

Beyond industrial lidar scanning, North America’s consumer electronics landscape is driving adoption of MEMS Mirror projection technologies in augmented reality headsets, pico projectors, and heads-up display systems. Major technology companies headquartered in Silicon Valley are investing in next-generation display platforms that leverage micro-mirror precision to deliver superior image quality and energy efficiency for portable projection applications.

North America’s extensive university-industry collaboration network accelerates MEMS Mirror innovation through joint development programs, technology licensing agreements, and spinout ventures. Institutions across the United States and Canada are producing specialized engineering talent that continuously advances micro-electromechanical systems design. This deep innovation infrastructure ensures the region retains its technological edge in both lidar scanning precision and projection system miniaturization.

Europe

Europe occupies a prominent position in the global MEMS Mirror market, driven by the region’s strong automotive manufacturing heritage and its commitment to advancing lidar scanning technologies for next-generation mobility solutions. Germany, in particular, serves as a critical hub where leading automotive OEMs and their supplier networks are actively evaluating and deploying MEMS-based lidar modules for advanced driver assistance systems and fully autonomous platforms. Beyond automotive applications, European industrial automation sectors in countries such as Switzerland, the Netherlands, and Sweden are incorporating MEMS Mirror projection and scanning systems into precision manufacturing and robotics workflows. The European Union’s sustained investment in photonics research through collaborative frameworks is nurturing a competitive ecosystem of MEMS Mirror developers. Additionally, stringent safety and environmental regulations across the region are compelling manufacturers to adopt advanced sensing technologies, indirectly supporting demand for compact and efficient MEMS lidar scanning solutions throughout the forecast period.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market for MEMS Mirror lidar scanning and projection technologies, propelled by rapid industrialization, expanding consumer electronics manufacturing, and aggressive investment in smart mobility infrastructure. China leads regional growth with substantial government support for domestic autonomous vehicle programs and lidar technology development, creating a large and increasingly self-sufficient demand base for MEMS Mirror components. Japan and South Korea contribute through their world-class semiconductor fabrication capabilities and deep expertise in precision optics, enabling high-quality micro-mirror production at scale. India is beginning to emerge as both a consumer and a research contributor, particularly within smart city and industrial automation contexts. The region’s cost-competitive manufacturing environment and growing pool of engineering talent position Asia-Pacific as a pivotal force in shaping global MEMS Mirror market dynamics through 2034.

South America

South America represents an emerging and gradually evolving market for MEMS Mirror technologies, with adoption currently concentrated within select industrial, agricultural, and infrastructure monitoring applications that benefit from lidar scanning capabilities. Brazil serves as the region’s primary market, where expanding precision agriculture programs are beginning to explore drone-mounted lidar systems equipped with MEMS Mirror scanning modules for crop monitoring and land surveying. The region’s developing automotive sector, while not yet at the forefront of autonomous vehicle deployment, is beginning to engage with advanced driver assistance technologies that incorporate micro-mirror based sensing. Challenges including economic volatility, import dependency on semiconductor components, and limited domestic MEMS fabrication infrastructure currently constrain the pace of market expansion. Nevertheless, growing awareness of lidar scanning benefits across mining, forestry, and infrastructure sectors is expected to steadily build demand momentum across South America during the forecast period.

Middle East & Africa

The Middle East and Africa region is at an early but strategically significant stage of MEMS Mirror market development, with adoption primarily driven by smart city initiatives, security and surveillance applications, and infrastructure modernization programs. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing heavily in intelligent transportation systems and autonomous urban mobility projects that require advanced lidar scanning solutions incorporating MEMS Mirror technology. These government-led transformation agendas are creating targeted procurement opportunities for international MEMS Mirror suppliers. In Africa, adoption remains nascent but is gradually gaining traction through mining sector applications where lidar-based terrain mapping improves operational safety and efficiency. The region’s reliance on technology imports and the relatively limited presence of local MEMS fabrication expertise pose near-term constraints, though partnerships with global technology providers are progressively bridging this gap and laying the foundation for longer-term market growth.

Report Scope

This market research report provides a comprehensive analysis of the MEMS Mirror (Lidar Scanning, Projection) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MEMS Mirror (Lidar Scanning, Projection) Market?

-> MEMS Mirror (Lidar Scanning, Projection) Market was valued at USD 0.43 billion in 2025 and is expected to reach USD 1.18 billion by 2034, growing at a CAGR of 10.3% during the forecast period from 2026 to 2034.

Which key companies operate ‘MEMS Mirror (Lidar Scanning, Projection) Market?

-> Key players include Mirrorcle Technologies, Hamamatsu Photonics, STMicroelectronics, Maradin, and Preciseley Microtechnology, among others, each maintaining diversified product portfolios addressing both scanning and projection segments.

What are the key growth drivers?

-> Key growth drivers include surging adoption of LiDAR technology in autonomous vehicles and advanced driver-assistance systems (ADAS), growing integration of pico-projection modules in portable devices, rising investments in smart infrastructure, and increasing deployment of solid-state LiDAR solutions that rely heavily on MEMS mirror technology for compact, reliable beam scanning.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by rapid industrialization and automotive technology adoption, while North America remains a significant market due to strong investments in autonomous vehicle development and ADAS technologies.

What are the emerging trends?

-> Emerging trends include solid-state LiDAR integration, miniaturized MEMS mirror arrays for augmented reality displays, piezoelectric actuation advancements, and expanding use of 2D scanning mirrors across industrial automation and consumer electronics applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...