Memory Controller IP (DDR, LPDDR, HBM) Market Insights

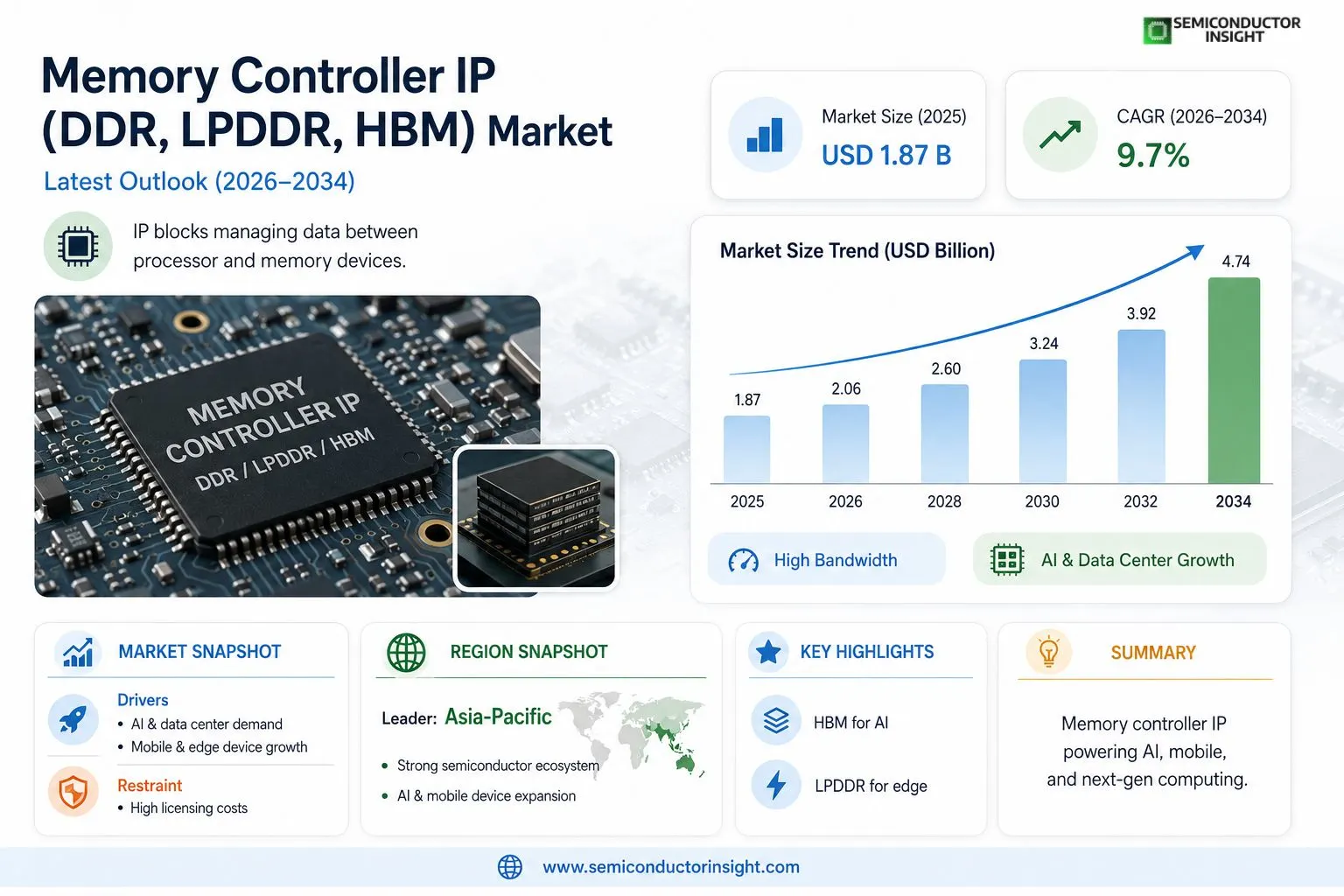

Global Memory Controller IP (DDR, LPDDR, HBM) Market size was valued at USD 1.87 billion in 2025. The market is projected to grow from USD 2.06 billion in 2026 to USD 4.74 billion by 2034, exhibiting a CAGR of 9.7% during the forecast period.

Memory controller IP refers to silicon intellectual property blocks that manage data flow between a processor and memory devices, encompassing standardized interfaces such as DDR (Double Data Rate), LPDDR (Low Power Double Data Rate), and HBM (High Bandwidth Memory). These IP cores are essential components integrated into system-on-chip (SoC) designs across applications ranging from mobile and consumer electronics to high-performance computing and artificial intelligence accelerators. DDR and LPDDR variants serve mainstream and mobile computing needs, while HBM addresses the extreme bandwidth demands of AI, data center GPUs, and advanced networking platforms.

The market is witnessing strong momentum driven by the accelerating adoption of AI workloads, the proliferation of data centers, and the rapid expansion of edge computing infrastructure. Furthermore, the growing complexity of SoC designs across automotive, 5G, and high-performance computing segments is fueling demand for licensable memory controller IP. Cadence Design Systems, Synopsys, and Rambus are among the prominent players offering a broad portfolio of verified, silicon-proven memory controller IP solutions catering to diverse application requirements.

MARKET DRIVERS

Surging Demand for High-Bandwidth Memory in AI and Data Center Applications

Memory Controller IP (DDR, LPDDR, HBM) Market is experiencing robust growth driven by the accelerating deployment of artificial intelligence, machine learning, and high-performance computing workloads. As AI model complexity increases, the need for memory subsystems capable of delivering high bandwidth with low latency has become a critical architectural requirement. HBM-based memory controller IP has emerged as a preferred solution for GPU and AI accelerator designs, where memory bandwidth directly constrains training and inference throughput. Semiconductor design teams are increasingly licensing advanced memory controller IP blocks to reduce time-to-market and mitigate the engineering risk associated with developing proprietary solutions.

Proliferation of Mobile and Edge Devices Driving LPDDR Controller IP Adoption

The rapid expansion of the smartphone, tablet, and edge computing device ecosystem continues to serve as a primary growth driver for the LPDDR memory controller IP segment. Modern mobile SoCs require tightly optimized LPDDR5 and LPDDR5X controller IP to balance performance with stringent power budgets. As OEMs push for thinner devices with longer battery life, IP vendors are innovating around power management features embedded directly within the controller architecture. The growing adoption of on-device AI inference in edge hardware is further intensifying demand for LPDDR-based memory controller solutions capable of handling bursty, latency-sensitive workloads.

➤ The transition from DDR4 to DDR5 in server and client computing platforms is compelling system-on-chip designers to adopt next-generation DDR memory controller IP, creating a significant upgrade cycle across the semiconductor IP licensing market.

Beyond mobile and data center applications, the automotive sector is emerging as a notable demand driver for Memory Controller IP (DDR, LPDDR, HBM) Market. Advanced driver-assistance systems (ADAS) and autonomous driving platforms require memory subsystems that comply with functional safety standards such as ISO 26262, while simultaneously delivering the bandwidth required for real-time sensor fusion. Automotive-grade DDR and LPDDR controller IP with built-in error correction and safety diagnostics is gaining traction among Tier-1 suppliers and automotive SoC vendors alike, broadening the addressable market for IP licensing companies.

MARKET CHALLENGES

Rising Design Complexity and Verification Burden of Advanced Memory Controller IP

One of the most significant challenges confronting Memory Controller IP (DDR, LPDDR, HBM) Market is the escalating complexity of designing and verifying memory controller IP that complies with successive JEDEC standards. Each new memory generation,DDR5, LPDDR5X, HBM3, and the forthcoming HBM3E,introduces more intricate timing parameters, multi-channel architectures, and advanced PHY requirements. Verification of memory controller IP now demands extensive simulation environments, formal verification methodologies, and silicon-proven test infrastructure, significantly raising the engineering investment required from both IP developers and licensees. Smaller fabless companies often lack the internal resources to independently validate complex memory subsystems, making them dependent on IP vendors for comprehensive verification IP (VIP) packages.

Other Challenges

Interoperability and Standards Compliance

Ensuring seamless interoperability between licensed memory controller IP and third-party PHY solutions, memory devices from multiple DRAM vendors, and diverse SoC fabric architectures presents a persistent technical challenge. Variations in DRAM device behavior across manufacturers can expose edge-case timing violations that are difficult to detect pre-silicon, increasing the risk of costly re-spins. IP vendors must continuously update their controller IP to maintain compliance with evolving JEDEC specifications while supporting backward compatibility with existing memory ecosystems.

Geopolitical and Supply Chain Pressures

Export restrictions on advanced semiconductor technology and escalating geopolitical tensions affecting DRAM supply chains have introduced new uncertainties into Memory Controller IP (DDR, LPDDR, HBM) Market. Restrictions on the transfer of advanced IP to certain regions are reshaping licensing strategies and compelling some IP vendors to reassess their global go-to-market approaches. Additionally, consolidation among DRAM manufacturers limits the diversity of memory devices that controller IP must support, while simultaneously concentrating market power in ways that can influence IP pricing and partnership dynamics.

MARKET RESTRAINTS

High Licensing Costs and Royalty Structures Limiting Adoption Among Emerging Fabless Players

The cost structure associated with licensing advanced memory controller IP represents a meaningful restraint for the broader Memory Controller IP (DDR, LPDDR, HBM) Market, particularly for emerging and early-stage fabless semiconductor companies. HBM controller IP licensing fees, in particular, can be substantial given the engineering investment required to develop and maintain compliance with HBM3 and HBM3E specifications. For startups targeting AI inference or edge computing applications, the capital required to license, integrate, and tape out with best-in-class memory controller IP can compress design budgets and delay product roadmaps. This dynamic can inadvertently favor larger, well-capitalized system semiconductor vendors that can either develop in-house controller IP or negotiate more favorable licensing terms at volume.

In-House IP Development by Large Semiconductor Vendors Constraining Third-Party Market Growth

A structural restraint affecting Memory Controller IP (DDR, LPDDR, HBM) Market is the trend among hyperscaler-affiliated chip design teams and leading fabless semiconductor companies to develop proprietary memory controller IP internally. Companies with sufficient engineering scale increasingly view memory controller design as a strategic differentiator, particularly for custom AI accelerators and cloud computing ASICs. In-house DDR and HBM controller development reduces reliance on third-party IP vendors for critical path components, thereby limiting the addressable market available to commercial IP licensors. While this trend is most pronounced at the leading edge, it exerts competitive pressure on IP vendors to continuously demonstrate measurable performance, power, and area advantages that justify ongoing licensing relationships.

MARKET OPPORTUNITIES

Expansion of HBM Controller IP Demand Fueled by Next-Generation AI Accelerator Proliferation

The sustained investment in large-scale AI infrastructure represents a compelling long-term opportunity for Memory Controller IP (DDR, LPDDR, HBM) Market, particularly within the HBM controller segment. As hyperscalers and cloud service providers develop custom AI training and inference chips, the demand for silicon-proven HBM3 and HBM3E memory controller IP with demonstrated power efficiency and signal integrity is expected to intensify. IP vendors capable of delivering pre-verified, process-portable HBM controller solutions with comprehensive support for advanced packaging technologies,including 2.5D and chiplet-based architectures,are well positioned to capture expanding licensing revenues as the AI accelerator market continues its growth trajectory.

Automotive and Industrial Segments Offering Incremental Revenue Streams for Memory Controller IP Vendors

The electrification of vehicles, the expansion of industrial automation, and the emergence of smart infrastructure applications are collectively opening new addressable markets for Memory Controller IP (DDR, LPDDR, HBM) Market beyond traditional consumer electronics and data center verticals. Automotive-grade LPDDR and DDR controller IP that meets AEC-Q100 qualification standards and incorporates functional safety features aligned with ISO 26262 ASIL-B and ASIL-D requirements is commanding premium licensing valuations. IP vendors that proactively invest in safety-certified memory controller portfolios and establish relationships with automotive SoC design teams can differentiate their offerings and build recurring royalty streams with longer product lifecycle characteristics than those typical in consumer semiconductor markets.

LPDDR5X and Emerging Memory Standards Creating New IP Refresh and Licensing Cycles

The ongoing evolution of JEDEC memory standards provides a structural opportunity for recurring IP refresh cycles within Memory Controller IP (DDR, LPDDR, HBM) Market. The ratification of LPDDR5X and the anticipated progression toward LPDDR6 specifications are expected to prompt semiconductor design teams to re-evaluate existing memory controller IP selections, creating new licensing opportunities for vendors with updated, silicon-validated IP portfolios. Similarly, the maturation of DDR5 RDIMM and LRDIMM server memory ecosystems is generating demand for controller IP tailored to enterprise and cloud computing platforms. Vendors that maintain close alignment with JEDEC standardization activities and deliver early-access IP compliant with emerging specifications will be positioned to capture design wins at the outset of each new memory generation’s adoption curve.

Memory Controller IP (DDR, LPDDR, HBM) Market Trends

Accelerating AI Adoption Driving Demand for High-Bandwidth Memory Controller IP

Memory Controller IP (DDR, LPDDR, HBM) Market is experiencing robust growth momentum, primarily driven by the rapid scaling of artificial intelligence workloads across data centers and edge computing environments. As AI model complexity intensifies, system architects are increasingly turning to High Bandwidth Memory (HBM) controller IP to meet the extreme memory throughput requirements of GPU accelerators and AI inference platforms. The proliferation of large language models and generative AI applications has further amplified demand for silicon-proven HBM controller IP blocks that can be seamlessly integrated into advanced SoC designs. Leading IP vendors including Cadence Design Systems, Synopsys, and Rambus continue to expand their portfolios of verified memory controller IP solutions to address these evolving performance requirements across both cloud and on-premise deployments.

Other Trends

Rising Adoption of LPDDR IP in Mobile and Edge Applications

Low Power Double Data Rate (LPDDR) memory controller IP is witnessing heightened adoption across mobile computing, automotive systems, and edge AI devices. As smartphone SoC designs become increasingly sophisticated, LPDDR controller IP plays a critical role in balancing high data throughput with stringent power constraints. The expansion of 5G-enabled devices and the growing deployment of advanced driver-assistance systems (ADAS) in automotive platforms are key contributors to this trend, as both segments demand licensable LPDDR IP cores that deliver performance efficiency without compromising thermal budgets.

Growing Complexity of SoC Designs Spurring DDR IP Integration

The escalating complexity of system-on-chip architectures across high-performance computing, networking, and industrial applications continues to reinforce demand for DDR memory controller IP. As chip designers prioritize faster time-to-market and reduced verification risk, the reliance on pre-validated, silicon-proven DDR controller IP cores has grown considerably. This trend is particularly evident in data center server SoCs and networking ASICs, where DDR5 controller IP adoption is accelerating to support higher bandwidth and improved power efficiency compared to prior generations.

Expansion of Data Center Infrastructure Reinforcing HBM Controller IP Demand

The ongoing global expansion of hyperscale data center infrastructure is a defining trend shaping Memory Controller IP (DDR, LPDDR, HBM) Market. As cloud service providers scale their GPU clusters and AI accelerator deployments, HBM controller IP has emerged as a foundational component enabling the memory bandwidth required for parallel processing workloads. Simultaneously, the maturation of chiplet-based design methodologies and advanced packaging technologies is broadening the applicability of HBM controller IP beyond traditional GPU use cases, opening new integration opportunities in custom AI silicon and high-performance networking platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Memory Controller IP (DDR, LPDDR, HBM) Market: Competitive Dynamics and Leading Innovators

The global Memory Controller IP (DDR, LPDDR, HBM) market is characterized by a moderately consolidated competitive landscape, with a handful of established semiconductor IP vendors commanding significant market share alongside a growing cohort of specialized challengers. Synopsys and Cadence Design Systems collectively dominate the market, leveraging decades of silicon-proven IP expertise, comprehensive verification environments, and deep integration with their respective EDA ecosystems. Both companies offer broad portfolios covering DDR4, DDR5, LPDDR4, LPDDR5, and HBM2/HBM3 controller IP, enabling SoC designers across AI accelerator, data center, automotive, and mobile segments to accelerate time-to-market. Rambus further reinforces the top-tier competitive position, distinguished by its patented memory interface technologies and a robust licensing model that extends across high-bandwidth memory solutions tailored for GPU and HPC applications. The accelerating adoption of AI workloads and the rapid expansion of data center infrastructure continue to intensify competition among these leading players, as hyperscalers and fabless chip companies seek silicon-proven, PPA-optimized memory controller IP to address extreme bandwidth and power efficiency requirements.

Beyond the market leaders, a number of niche and regionally significant players are actively capturing design wins across targeted verticals. Arasan Chip Systems has established a strong presence in mobile and IoT-oriented LPDDR controller IP, while Northwest Logic (now part of Rambus) has historically contributed proven DDR subsystem IP to a wide range of SoC programs. Dolphin Technology, SmartDV Technologies, and Mobiveil offer competitive memory controller IP solutions aimed at cost-sensitive and mid-tier SoC designs. IP vendors such as Alphawave Semi and Arteris IP are extending their portfolios toward high-speed memory interfaces to capture emerging HBM and next-generation DDR opportunities. Additionally, Open-Silicon and CAST Inc. serve specialized segments with configurable controller IP targeting FPGAs and ASICs. The market also sees participation from vertically integrated semiconductor companies, including Marvell Technology and Microchip Technology, which develop proprietary memory controller IP for internal SoC programs while selectively licensing solutions externally. As DDR5 and HBM3 adoption accelerates through 2034, competitive differentiation is increasingly centered on power efficiency, protocol compliance, silicon maturity, and comprehensive customer support ecosystems.

List of Key Memory Controller IP (DDR, LPDDR, HBM) Companies Profiled

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Rambus Inc.

- Arasan Chip Systems

- Alphawave Semi

- Dolphin Technology

- SmartDV Technologies

- Mobiveil Inc.

- Northwest Logic (Rambus)

- Arteris IP

- CAST Inc.

- Marvell Technology, Inc.

- Microchip Technology Inc.

- Open-Silicon (Aricent)

- Lattice Semiconductor Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

DDR Memory Controller IP holds a commanding position as the most widely deployed interface type across server, desktop, and embedded computing platforms, owing to its broad ecosystem maturity and compatibility with mainstream SoC architectures.

|

| By Application |

|

Artificial Intelligence & Machine Learning Accelerators have emerged as the most transformative application segment, fundamentally reshaping the memory controller IP landscape and catalyzing unprecedented demand for high-bandwidth, low-latency memory interface solutions.

|

| By End User |

|

Fabless Semiconductor Companies represent the dominant end-user constituency for licensable memory controller IP, as their design model inherently relies on acquiring silicon-proven, pre-verified IP blocks to accelerate time-to-market and mitigate development risk across complex SoC programs.

|

| By Interface Standard Generation |

|

DDR5 / LPDDR5 controller IP is rapidly establishing itself as the leading generational standard, driven by the widespread industry transition toward next-generation memory architectures that deliver meaningfully superior bandwidth, improved signal integrity, and enhanced power management capabilities relative to their predecessors.

|

| By Deployment Mode |

|

Hard IP dominates the deployment preference for production-grade memory controller implementations, particularly in high-volume applications where predictable timing closure, guaranteed performance at specific process nodes, and reduced physical verification burden are essential considerations for tapeout success.

|

Regional Analysis: Memory Controller IP (DDR, LPDDR, HBM) Market

Asia-Pacific

South Korea and Taiwan anchor the Asia-Pacific memory controller IP landscape. South Korea’s dominance in HBM stacked memory production creates sustained demand for high-bandwidth memory controller IP optimized for AI and graphics workloads. Taiwan’s dense fabless ecosystem enables rapid integration of DDR and LPDDR controller IP into SoC designs, supporting mobile, networking, and edge computing applications with exceptional design velocity.

China’s memory controller IP market is shaped by national self-sufficiency initiatives driving investment in indigenous DDR and LPDDR IP development. Domestic chip designers are increasingly licensing and developing proprietary memory interface solutions to reduce external dependencies. Growing data center infrastructure and the expansion of domestic AI chip programs are amplifying demand for scalable, high-performance memory controller IP tailored to local manufacturing processes.

Asia-Pacific’s vast consumer electronics manufacturing base generates persistent demand for LPDDR memory controller IP. Smartphone OEMs across China, South Korea, and India require highly power-efficient LPDDR solutions as handset performance expectations continue rising. The transition to LPDDR5 and LPDDR5X interfaces in flagship and mid-tier devices is creating sustained IP licensing opportunities for vendors serving this rapidly evolving segment.

The proliferation of AI training and inference workloads across hyperscale and edge data centers in Asia-Pacific is substantially accelerating demand for HBM and DDR5 memory controller IP. Regional cloud providers and AI chip startups are integrating advanced memory subsystems to maximize compute efficiency. This trend positions Asia-Pacific as the fastest-evolving market for high-bandwidth memory controller IP innovation through the forecast period.

North America

North America represents the second most influential region in the Memory Controller IP market, driven by a concentration of world-leading semiconductor IP vendors, fabless chip designers, and hyperscale cloud infrastructure operators. The United States is home to prominent memory controller IP developers whose DDR, LPDDR, and HBM interface solutions are deployed in data center processors, AI accelerators, and automotive systems globally. The robust venture capital ecosystem supports IP startups innovating around next-generation memory interface standards. Demand from hyperscale data center operators pursuing maximum memory bandwidth for AI and machine learning workloads is a particularly strong growth catalyst. Additionally, government-backed initiatives aimed at strengthening domestic semiconductor design capabilities are fostering investment in advanced memory subsystem IP. The automotive sector’s shift toward software-defined vehicles requiring high-reliability DDR memory interfaces further broadens the regional demand base for memory controller IP solutions heading into 2034.

Europe

Europe occupies a strategically important position in the global Memory Controller IP market, with its strength concentrated in automotive-grade and industrial semiconductor design. Germany, the Netherlands, France, and Sweden are home to established semiconductor companies and IP design centers that develop memory controller solutions tailored to stringent automotive safety and reliability standards. The region’s automotive industry is a primary consumer of DDR and LPDDR memory controller IP as vehicle architectures evolve toward advanced driver assistance systems and autonomous driving platforms. European semiconductor policy frameworks and collaborative research programs are actively encouraging domestic IP development to reduce dependency on non-European sources. The growth of edge computing and industrial IoT applications across European manufacturing sectors is also generating incremental demand for efficient, low-power LPDDR memory controller IP solutions across the forecast horizon.

United States

Within the broader North American landscape, the United States merits focused attention as a singular force shaping global Memory Controller IP standards and commercial adoption. Silicon Valley and other domestic semiconductor hubs serve as the origin point for many of the industry’s most widely licensed DDR, LPDDR, and HBM controller IP platforms. The US market benefits from deep integration between IP providers, chip designers, and end-market customers across data center, defense, aerospace, and consumer electronics segments. Federal initiatives supporting domestic semiconductor resilience are channeling significant investment into advanced memory interface research and IP development. The country’s leading cloud and AI hardware companies are major consumers of cutting-edge HBM memory controller IP, making the United States an indispensable demand anchor for the global market through 2034.

Middle East & Africa

The Middle East and Africa region is an emerging participant in the Memory Controller IP market, currently at an earlier stage of development compared to more mature geographies. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing heavily in data center infrastructure and digital economy initiatives, which is generating nascent demand for DDR and HBM memory controller IP in cloud and AI deployments. National technology strategies focused on reducing digital infrastructure dependency are beginning to stimulate interest in domestic semiconductor design capabilities. Africa’s market remains in its early development phase, though expanding mobile penetration and fintech-driven computing growth are laying the groundwork for future LPDDR memory controller IP demand. Over the forecast period extending to 2034, increasing regional investment in technology infrastructure is expected to gradually elevate the Middle East and Africa’s role in the global Memory Controller IP market ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the Memory Controller IP (DDR, LPDDR, HBM) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Memory Controller IP (DDR, LPDDR, HBM) Market?

-> Global Memory Controller IP (DDR, LPDDR, HBM) Market size was valued at USD 1.87 billion in 2025 and is projected to grow from USD 2.06 billion in 2026 to USD 4.74 billion by 2034, exhibiting a CAGR of 9.7% during the forecast period.

Which key companies operate in Memory Controller IP (DDR, LPDDR, HBM) Market?

-> Key players include Cadence Design Systems, Synopsys, and Rambus, among others, offering a broad portfolio of verified, silicon-proven memory controller IP solutions catering to diverse application requirements.

What are the key growth drivers?

-> Key growth drivers include the accelerating adoption of AI workloads, the proliferation of data centers, and the rapid expansion of edge computing infrastructure. Additionally, the growing complexity of SoC designs across automotive, 5G, and high-performance computing segments is fueling demand for licensable memory controller IP.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by rapid semiconductor manufacturing expansion and rising demand for consumer electronics and mobile devices, while North America remains a significant market owing to its strong presence in AI, data centers, and high-performance computing.

What are the emerging trends?

-> Emerging trends include HBM adoption for AI accelerators and data center GPUs, integration of LPDDR interfaces in edge and mobile SoCs, and the increasing complexity of DDR5 and LPDDR5 memory controller IP driven by next-generation computing and 5G infrastructure demands.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...