Key-Value SSD (KVS) Controller Market Insights

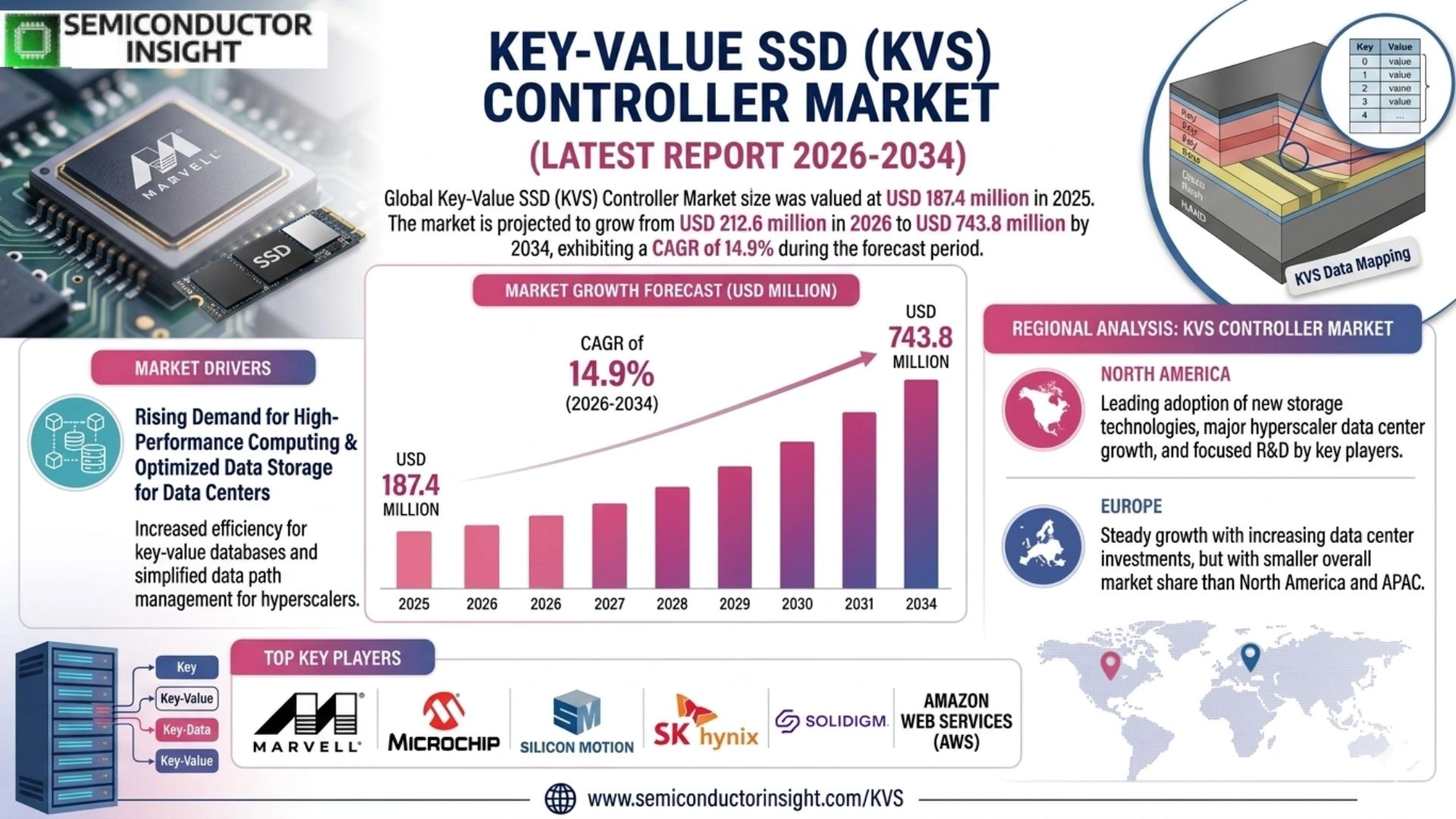

Key-Value SSD (KVS) Controller Market size was valued at USD 187.4 million in 2025. The market is projected to grow from USD 212.6 million in 2026 to USD 743.8 million by 2034, exhibiting a CAGR of 14.9% during the forecast period.

Key-Value SSD (KVS) controllers are specialized hardware components designed to manage storage operations using a key-value data model rather than the traditional block-based interface. These controllers enable direct key-value storage access at the device level, significantly reducing I/O amplification, lowering CPU overhead, and improving overall data retrieval efficiency. The technology encompasses a range of controller architectures supporting NVMe-based key-value command sets, firmware-integrated mapping layers, and hardware-accelerated hashing engines optimized for cloud-scale workloads.

The market is experiencing robust momentum driven by the surging demand for high-performance storage in cloud computing, hyperscale data centers, and AI-driven applications. Furthermore, the widespread adoption of NoSQL databases and in-memory computing frameworks has created a compelling need for storage solutions that natively support key-value semantics. Industry initiatives are also playing a pivotal role — for instance, Samsung Electronics and the NVM Express (NVMe) consortium have actively advanced the standardization of the Key-Value Command Set specification, accelerating ecosystem adoption. KIOXIA Corporation, Micron Technology, and ScaleFlux are among the prominent players operating in this market with increasingly competitive KVS controller portfolios.

MARKET DRIVERS

Surging Demand for High-Performance Storage in Data-Intensive Applications

Key-Value SSD (KVS) Controller Market is experiencing robust growth driven by the exponential increase in unstructured data generated across cloud computing, artificial intelligence, and big data analytics platforms. Traditional block-based storage interfaces introduce software translation overhead that degrades latency and throughput in workloads that natively operate on key-value data models. KVS controllers eliminate the key-value to block translation layer, enabling applications to interact directly with flash storage using semantic key-value commands, which significantly reduces CPU utilization and end-to-end access latency in hyperscale environments.

Rapid Expansion of Hyperscale Data Centers and Cloud Infrastructure

Hyperscale cloud providers and colocation data center operators are actively evaluating Key-Value SSD controller architectures as a means to improve storage efficiency and reduce total cost of ownership. As workloads such as in-memory databases, object storage backends, and real-time analytics engines scale to petabyte levels, the inefficiencies of legacy NVMe block interfaces become increasingly pronounced. KVS controllers address this by supporting variable-length object storage natively within the drive firmware, reducing write amplification and improving flash endurance, which are critical considerations for large-scale fleet management.

➤ The growing adoption of computational storage and near-data processing architectures is further positioning Key-Value SSD controllers as a foundational technology for next-generation disaggregated storage systems, where reducing data movement between host and storage is a primary design objective.

Standardization efforts led by bodies such as the NVM Express (NVMe) Working Group have further accelerated adoption by defining interoperable command sets for key-value storage, reducing fragmentation across vendor implementations. This growing ecosystem of standardized KVS interfaces is enabling a broader set of enterprise software vendors to integrate natively with Key-Value SSD (KVS) Controller technology, reinforcing the commercial viability of the market and driving procurement decisions at scale across North America, Europe, and Asia-Pacific data center markets.

MARKET CHALLENGES

Application Ecosystem Maturity and Software Stack Compatibility Barriers

Despite strong architectural advantages, Key-Value SSD (KVS) Controller Market faces meaningful challenges related to software ecosystem readiness. A large proportion of enterprise storage applications, databases, and operating system I/O stacks are architected around block-based abstractions, and migrating these to natively leverage KVS controller interfaces requires significant software re-engineering effort. Development teams must modify storage engines or adopt new libraries to issue key-value commands directly to the drive, creating adoption friction particularly for organizations with legacy infrastructure and limited engineering bandwidth allocated to storage layer modernization.

Other Challenges

Limited Vendor Ecosystem and Supply Chain Concentration

The commercial supply of Key-Value SSD controller silicon and integrated drives remains concentrated among a relatively small number of specialized semiconductor companies and vertically integrated storage vendors. This limited competitive landscape constrains pricing flexibility and may expose enterprise buyers to single-source dependency risks. Broader market penetration will require increased fabless semiconductor participation and expanded reference design availability to encourage system integrators and OEM drive manufacturers to incorporate KVS controller technology across a wider range of product tiers.

Performance Benchmarking and Qualification Complexity

Standardized benchmarking methodologies for evaluating Key-Value SSD (KVS) controller performance remain less mature compared to those established for conventional NVMe block SSDs. Enterprise procurement teams and data center architects encounter difficulty in conducting like-for-like performance comparisons across vendor offerings, which prolongs qualification cycles and delays purchasing decisions. The absence of universally accepted KVS-specific performance metrics covering variable key-value object sizes, mixed read-write ratios, and garbage collection behavior under sustained load represents a practical barrier to wider enterprise deployment.

MARKET RESTRAINTS

High Initial Development and Integration Costs Limiting Broad Adoption

One of the primary restraints affecting Key-Value SSD (KVS) Controller Market is the elevated upfront investment required for both hardware development and application-level integration. Designing and validating a production-grade KVS controller involves complex firmware engineering for garbage collection, wear leveling, and key-value indexing within the drive, resulting in longer product development cycles and higher NRE (non-recurring engineering) costs compared to conventional SSD controller development. These cost dynamics limit the number of commercially viable KVS controller products available in the market and create a pricing premium that restricts adoption to high-value hyperscale and enterprise use cases.

Organizational Inertia and Risk Aversion in Enterprise Storage Procurement

Enterprise IT organizations demonstrate significant institutional inertia when evaluating storage technology transitions that require changes to application software architecture. Procurement and infrastructure teams at large enterprises typically prioritize proven, widely deployed technologies with established support ecosystems, vendor certification programs, and long-term supply commitments. The relative novelty of Key-Value SSD controller solutions, combined with limited deployment reference cases outside of hyperscale environments, contributes to a cautious adoption posture among mid-market and large enterprise buyers, moderating the overall pace of market expansion beyond the leading cloud and internet platform operators.

MARKET OPPORTUNITIES

Emergence of AI and Machine Learning Workloads as a Catalyst for KVS Adoption

The accelerating deployment of artificial intelligence and machine learning inference infrastructure presents a significant commercial opportunity for Key-Value SSD (KVS) Controller Market. AI training pipelines and large-scale model serving platforms generate high-frequency access patterns to feature stores, embedding tables, and model checkpoints that map naturally to key-value data structures. KVS controller architectures that enable low-latency, high-throughput direct storage access for these workloads can deliver measurable performance improvements and infrastructure cost reductions for AI platform operators, creating a compelling value proposition that is gaining recognition among leading technology companies investing in purpose-built AI storage infrastructure.

Growth in Edge Computing and Distributed Storage Deployments

Beyond centralized data centers, the expansion of edge computing infrastructure offers an emerging opportunity for Key-Value SSD (KVS) controller adoption in resource-constrained environments where minimizing host CPU overhead is a critical design constraint. Edge nodes deployed for telecommunications, autonomous systems, and industrial IoT applications require efficient local storage for telemetry data, configuration state, and cached content — all of which align with key-value access semantics. As edge hardware platforms mature and NVMe-based storage becomes standard at the edge tier, KVS controller solutions optimized for low power consumption and compact form factors are well-positioned to capture a growing share of this distributed storage segment over the coming years.

Key-Value SSD (KVS) Controller Market Trends

Rising Adoption of NVMe-Based Key-Value Command Sets Reshaping Storage Architecture

Key-Value SSD (KVS) Controller Market is undergoing a significant transformation as the industry moves away from traditional block-based storage interfaces toward native key-value data models implemented directly at the device level. This architectural shift is largely being accelerated by the formal standardization of the Key-Value Command Set specification under the NVM Express (NVMe) consortium, with active contributions from leading semiconductor manufacturers such as Samsung Electronics. By enabling storage devices to natively interpret key-value operations, these controllers eliminate the translation overhead inherent in conventional storage stacks, resulting in measurably lower CPU utilization and reduced I/O amplification across enterprise and hyperscale environments.

Hyperscale data center operators are increasingly evaluating KVS controller-equipped SSDs as a strategic solution to address the growing mismatch between application-layer data semantics and physical storage interfaces. As cloud infrastructure scales to support billions of concurrent transactions, the efficiency gains offered by hardware-accelerated hashing engines and firmware-integrated mapping layers embedded within KVS controllers present a compelling operational advantage.

Other Trends

Surging Demand from NoSQL Databases and In-Memory Computing Frameworks

The widespread enterprise adoption of NoSQL databases and in-memory computing platforms is creating direct demand for storage solutions that natively align with key-value semantics. Applications built on distributed caching systems and high-throughput transactional databases benefit substantially from KVS controller architectures, as these components reduce software-layer complexity and deliver more predictable latency profiles. This trend is reinforcing product development priorities among key market participants including KIOXIA Corporation, Micron Technology, and ScaleFlux, all of which have expanded their KVS controller portfolios to serve cloud-native and AI-driven workload requirements.

AI and Machine Learning Workloads Driving Storage Innovation

Artificial intelligence and machine learning pipelines increasingly depend on rapid, low-latency access to large feature stores and embedding databases that are fundamentally organized as key-value structures. The alignment between KVS controller capabilities and AI inference infrastructure requirements is emerging as a notable market catalyst. Storage architects at hyperscale cloud providers are exploring KVS-enabled SSDs to optimize data retrieval performance in training and inference workflows, further broadening the addressable use cases for Key-Value SSD controller technology beyond traditional database applications.

Ecosystem Standardization Strengthening Long-Term Market Confidence

Ongoing collaboration between industry bodies and hardware vendors to standardize the NVMe Key-Value Command Set is instilling greater confidence among enterprise buyers and system integrators evaluating KVS controller deployments. As interoperability improves across controller architectures and host software stacks, adoption barriers are expected to diminish, enabling broader integration of Key-Value SSD controllers into next-generation storage infrastructure across cloud, telecommunications, and high-performance computing segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Key-Value SSD (KVS) Controller Market — Competitive Dynamics and Leading Innovators

Global Key-Value SSD (KVS) Controller Market is characterized by a concentrated yet rapidly evolving competitive landscape, with a handful of technologically advanced players commanding significant influence. Samsung Electronics stands at the forefront, having played a pivotal role in advancing the NVMe Key-Value Command Set specification in collaboration with the NVM Express consortium. The company’s deep vertical integration — spanning NAND flash manufacturing, controller design, and firmware development — provides a formidable competitive advantage. ScaleFlux has also emerged as a specialized and highly recognized player, offering computational storage drives with native key-value interfaces tailored for cloud-scale and hyperscale data center deployments. KIOXIA Corporation and Micron Technology continue to strengthen their KVS controller portfolios, leveraging extensive semiconductor expertise and strategic partnerships to address the growing demand from NoSQL database operators and AI-driven workloads. The competitive intensity is further amplified by aggressive R&D investments aimed at reducing I/O amplification, minimizing CPU overhead, and optimizing hardware-accelerated hashing engines.

Beyond the dominant players, a number of specialized and emerging companies are carving out significant niches within the Key-Value SSD Controller ecosystem. Western Digital and SK Hynix are actively investing in next-generation NVMe-based controller architectures that natively support key-value semantics, targeting hyperscale cloud operators and enterprise storage integrators. Marvell Technology and Phison Electronics, both established controller silicon vendors, are incorporating key-value command set support into their firmware and hardware roadmaps. Additionally, Innogrit and Silicon Motion are gaining traction by offering cost-competitive KVS controller solutions optimized for mid-tier cloud and edge deployments. Ambient Scientific and NGD Systems (now part of Seagate’s computational storage division) represent further innovation vectors, pushing the boundaries of in-storage processing to enable low-latency key-value retrieval at the device level. As the market is projected to grow at a CAGR of 14.9% from USD 212.6 million in 2026 to USD 743.8 million by 2034, competitive differentiation is increasingly centered on NVMe compliance, firmware-integrated mapping layer efficiency, and total cost of ownership advantages for cloud-native storage architectures.

List of Key Key-Value SSD (KVS) Controller Companies Profiled

- Samsung Electronics Co., Ltd.

- ScaleFlux

- KIOXIA Corporation

- Micron Technology, Inc.

- Western Digital Corporation

- SK Hynix Inc.

- Marvell Technology, Inc.

- Phison Electronics Corporation

- Silicon Motion Technology Corporation

- Innogrit Corporation

- NGD Systems (Seagate Computational Storage)

- Ambient Scientific

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

NVMe-Based KVS Controllers represent the leading segment within the type category, benefiting from the active standardization of the Key-Value Command Set specification championed by the NVM Express consortium and industry leaders such as Samsung Electronics.

|

| By Application |

|

Cloud Storage and Object Stores dominate the application landscape, driven by the explosive expansion of hyperscale data center deployments and the inherent alignment between key-value semantics and object storage architectures.

|

| By End User |

|

Hyperscale Data Center Operators constitute the dominant end-user segment, as the structural demands of operating at massive scale make the efficiency advantages of KVS controllers particularly impactful.

|

| By Interface Standard |

|

NVMe over PCIe leads the interface standard segment, underpinned by its broad compatibility with contemporary server architectures and its well-established ecosystem of driver support and management tooling.

|

| By Deployment Mode |

|

Cloud-Native Deployment represents the leading and fastest-evolving deployment mode, reflecting the broader industry transition toward cloud-first infrastructure strategies across both enterprise and service provider segments.

|

Regional Analysis: Key-Value SSD (KVS) Controller Market

Asia-Pacific

Asia-Pacific hosts the world’s most advanced semiconductor fabrication facilities, enabling rapid prototyping and mass production of Key-Value SSD controller chips. Integrated supply chains connecting NAND flash producers with controller designers reduce time-to-market significantly, giving regional players a decisive competitive edge over counterparts in other geographies.

The proliferation of hyperscale data centers across China, India, Japan, and Southeast Asia is generating substantial demand for high-performance Key-Value SSD controllers. Cloud service providers and internet platform companies in the region are rapidly deploying KVS-optimized storage architectures to meet the performance requirements of AI, big data, and real-time transactional workloads.

National semiconductor strategies in China, South Korea, Japan, and Taiwan are channeling significant investment into advanced storage controller research and development. Subsidies, tax incentives, and public-private partnership frameworks are enabling domestic firms to accelerate KVS controller design capabilities, reducing dependence on foreign intellectual property and strengthening regional self-sufficiency.

Asia-Pacific’s aggressive rollout of artificial intelligence applications, autonomous systems, and edge computing infrastructure is creating new and expanding demand vectors for Key-Value SSD controllers. The need for deterministic low-latency access to unstructured data at the edge and in AI training clusters makes KVS-based storage a preferred architectural choice for leading technology firms across the region.

North America

North America represents the second most influential region Key-Value SSD (KVS) Controller Market, anchored by the presence of globally recognized hyperscale cloud providers, cutting-edge semiconductor design houses, and a mature enterprise IT ecosystem with strong appetite for next-generation storage technologies. The United States, in particular, serves as a critical hub for KVS controller intellectual property development, with prominent fabless chip companies and research institutions actively contributing to open-standard initiatives such as NVMe-KV. Increasing adoption of AI-driven workloads, distributed NoSQL databases, and object storage platforms across North American enterprises is fueling organic demand for Key-Value SSD solutions. The region’s well-established venture capital environment continues to fund startups specializing in computational storage and KVS controller architectures, further enriching the innovation landscape and accelerating commercialization of differentiated storage solutions across the forecast period.

Europe

Europe occupies a significant position Key-Value SSD (KVS) Controller Market, characterized by strong demand from industrial IoT, automotive data management, and enterprise cloud transformation initiatives. Germany, France, the Netherlands, and the Nordic countries are emerging as active consumers of KVS-enabled storage solutions, particularly within sectors handling large volumes of unstructured and time-series data. The European Union’s emphasis on digital sovereignty and data residency compliance is encouraging regional enterprises to invest in high-performance, locally managed storage infrastructure incorporating Key-Value SSD controller technology. Additionally, Europe’s growing network of edge data centers and smart manufacturing facilities is generating specialized demand for low-latency KVS storage. Collaborative research programs between universities and industry players across the region are contributing to a gradually strengthening ecosystem of storage controller innovation and deployment expertise.

South America

South America is an emerging market in Global Key-Value SSD (KVS) Controller Market, with adoption currently driven by expanding digital transformation efforts in Brazil, Chile, and Colombia. The growth of cloud computing infrastructure, fintech platforms, and e-commerce ecosystems across the region is gradually increasing awareness and demand for advanced storage solutions, including KVS-optimized drives and controllers. While the region’s KVS controller market remains in a relatively early stage of maturity compared to Asia-Pacific and North America, improving telecommunications infrastructure and growing foreign direct investment in regional data center capacity are expected to create meaningful opportunities over the 2026–2034 period. Local system integrators and cloud service providers are beginning to evaluate Key-Value SSD deployments as a viable path toward improving storage efficiency and application performance across their platforms.

Middle East & Africa

The Middle East and Africa region represents a nascent but strategically important frontier Key-Value SSD (KVS) Controller Market. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are making substantial investments in smart city infrastructure, national cloud platforms, and AI center of excellence initiatives, all of which are anticipated to drive longer-term demand for high-performance KVS storage controller solutions. South Africa and select East African economies are witnessing steady growth in data center construction activity, supported by improving power infrastructure and increasing internet penetration. While widespread enterprise adoption of Key-Value SSD technology in this region remains at an exploratory phase, the alignment of national digitalization agendas with global storage technology trends is positioning the Middle East and Africa as a region of growing long-term potential for KVS controller vendors seeking geographic diversification.

Report Scope

This market research report provides a comprehensive analysis of the Key-Value SSD (KVS) Controller Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Key-Value SSD (KVS) Controller Market?

-> Global Key-Value SSD (KVS) Controller Market was valued at USD 187.4 million in 2025 and is expected to reach USD 743.8 million by 2034, growing at a CAGR of 14.9% during the forecast period from 2026 to 2034.

Which key companies operate Key-Value SSD (KVS) Controller Market?

-> Key players include KIOXIA Corporation, Micron Technology, ScaleFlux, and Samsung Electronics, among others. Samsung Electronics and the NVM Express (NVMe) consortium have also been instrumental in advancing the standardization of the Key-Value Command Set specification.

What are the key growth drivers?

-> Key growth drivers include surging demand for high-performance storage in cloud computing, hyperscale data centers, and AI-driven applications, as well as the widespread adoption of NoSQL databases and in-memory computing frameworks that natively support key-value semantics.

Which region dominates the market?

-> Asia-Pacific is among the fastest-growing regions, driven by rapid expansion of hyperscale data center infrastructure, while North America remains a dominant market owing to its advanced cloud computing ecosystem and early technology adoption.

What are the emerging trends?

-> Emerging trends include NVMe-based key-value command sets, firmware-integrated mapping layers, hardware-accelerated hashing engines, and the ongoing standardization efforts by the NVM Express (NVMe) consortium to accelerate ecosystem-wide adoption of KVS controller technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...