Graphics DRAM (GDDR6, GDDR7) Market Insights

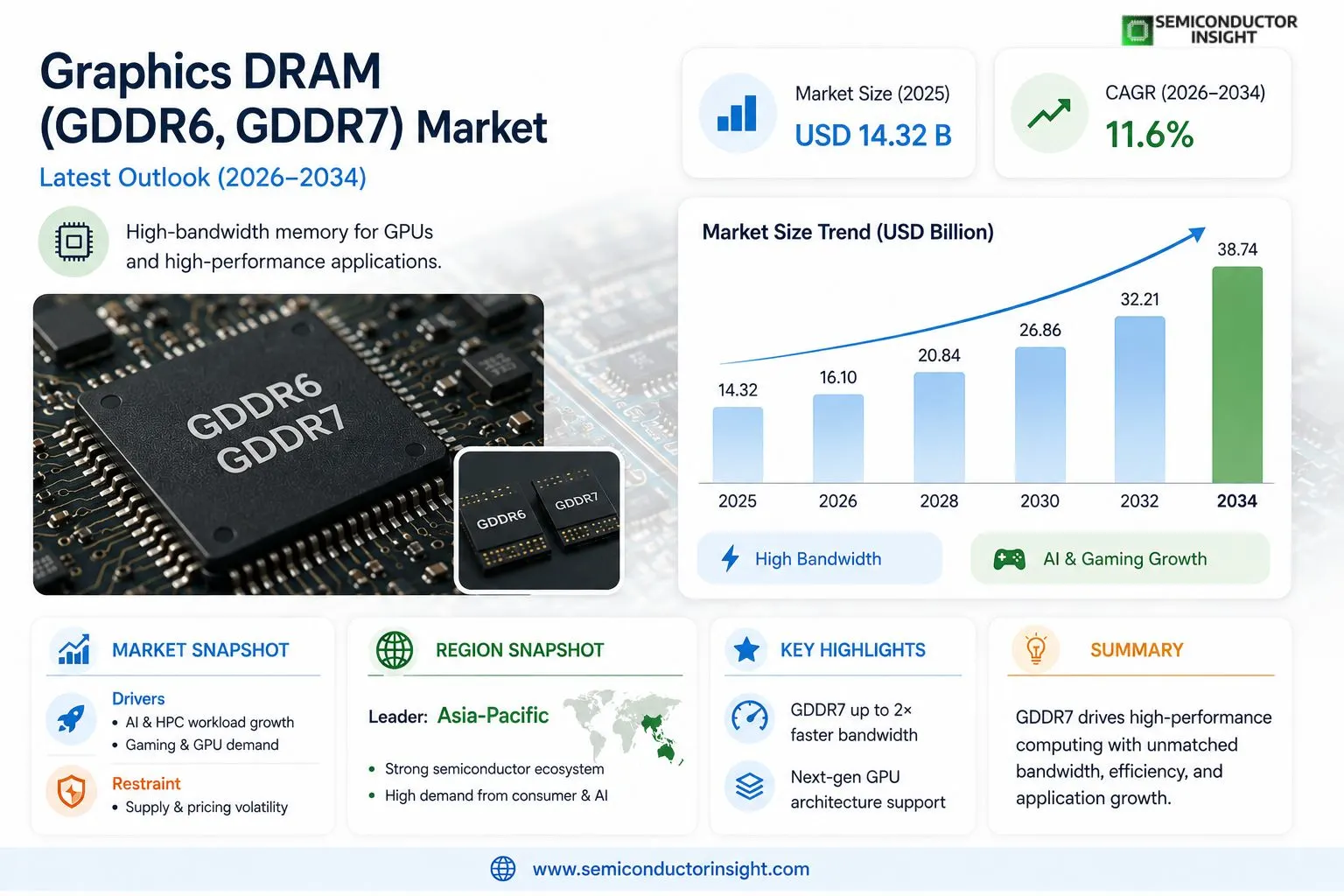

Global Graphics DRAM (GDDR6, GDDR7) market size was valued at USD 14.32 billion in 2025. The market is projected to grow from USD 16.10 billion in 2026 to USD 38.74 billion by 2034, exhibiting a CAGR of 11.6% during the forecast period.

Graphics DRAM refers to high-performance, high-bandwidth memory specifically engineered for use in graphics processing units (GPUs) and other visually intensive computing applications. GDDR6 (Graphics Double Data Rate 6) and the next-generation GDDR7 represent the leading standards in this segment, offering significantly enhanced data transfer rates, improved power efficiency, and greater bandwidth compared to their predecessors. These memory technologies are integral to modern discrete graphics cards, gaming consoles, workstation GPUs, and AI accelerators, supporting applications that demand rapid, parallel data processing at scale.

The market is experiencing robust growth driven by surging demand for high-performance computing, the rapid proliferation of AI and machine learning workloads, and the expanding global gaming industry. Furthermore, the transition from GDDR6 to GDDR7 , which offers data transfer speeds exceeding 32 Gbps per pin , is accelerating adoption across premium GPU platforms. Initiatives by leading semiconductor companies are also shaping the competitive landscape. For instance, Samsung Electronics and SK Hynix have both announced mass production milestones for GDDR7 memory, targeting next-generation GPU architectures from NVIDIA and AMD. Samsung Electronics Co., Ltd., SK Hynix Inc., and Micron Technology, Inc. are among the key players operating in the market with extensive product portfolios spanning both GDDR6 and GDDR7 memory solutions.

MARKET DRIVERS

Surging Demand from AI, Gaming, and High-Performance Computing Applications

Graphics DRAM Market, encompassing GDDR6 and GDDR7 technologies, is experiencing robust growth driven by accelerating demand across artificial intelligence workloads, gaming GPUs, and high-performance computing infrastructure. As AI model training and inference tasks increasingly rely on memory-intensive GPU clusters, the need for high-bandwidth, low-latency graphics memory has become a core requirement for data center deployments worldwide. GDDR6, with its wide adoption across consumer and professional GPU segments, continues to serve as the backbone of most discrete graphics cards, while the emerging GDDR7 standard promises significantly improved bandwidth and power efficiency, positioning it as the next-generation solution for flagship GPU platforms.

Rapid Expansion of the Discrete GPU Market and Next-Generation Console Ecosystem

The sustained expansion of the discrete GPU market, fueled by both consumer gaming and professional visualization, is a primary driver for Graphics DRAM demand. GPU vendors continue to ramp production of high-end cards that rely on GDDR6 and increasingly on GDDR7 memory, as gamers and creators seek higher frame rates, ray tracing capabilities, and 4K to 8K rendering performance. Simultaneously, the embedded memory requirements within gaming consoles and automotive computing platforms are expanding the addressable market for graphics DRAM beyond traditional PC segments. The growing integration of advanced GPU architectures within edge AI and autonomous driving systems further reinforces this structural demand trend in Graphics DRAM (GDDR6, GDDR7) market.

➤ GDDR7 delivers up to 1.5× to 2× the bandwidth of GDDR6 at comparable power envelopes, making it a transformative upgrade for next-generation GPU architectures targeting AI inferencing, 8K gaming, and real-time ray tracing workloads.

The proliferation of generative AI applications, large language model deployments, and machine learning pipelines requiring GPU acceleration is creating a sustained, multi-year pull on Graphics DRAM supply chains. Hyperscale cloud providers and enterprise AI infrastructure operators are procuring GPUs in unprecedented volumes, each unit incorporating multiple GDDR6 modules. As GDDR7 qualification and mass production ramp through 2024 and beyond, the transition is expected to drive further revenue growth for leading Graphics DRAM suppliers, given the higher per-unit average selling prices associated with the newer specification.

MARKET CHALLENGES

Supply Chain Complexities and Advanced Node Manufacturing Constraints

Despite favorable demand dynamics, Graphics DRAM Market faces meaningful challenges rooted in the complexity of manufacturing advanced memory at scale. GDDR6 and GDDR7 are produced on leading-edge DRAM process nodes, requiring substantial capital investment, precise process control, and long qualification cycles before new capacity becomes commercially viable. The concentration of GDDR manufacturing capacity among a small number of suppliers creates inherent supply vulnerability, particularly during periods of sudden demand acceleration. Any disruption to fab operations, raw material availability, or advanced packaging supply chains can trigger allocation constraints that ripple across GPU vendors and their customers.

Other Challenges

Pricing Volatility and Margin Pressure

Graphics DRAM segment is subject to cyclical pricing dynamics that can compress margins for both memory suppliers and GPU manufacturers. During periods of oversupply, average selling prices for GDDR6 modules have declined sharply, eroding profitability even as unit volumes expand. Conversely, supply tightness during demand surges can strain GPU vendors’ bill-of-materials cost management. Balancing inventory levels, long-term supply agreements, and spot market exposure remains a persistent operational challenge for participants across Graphics DRAM (GDDR6, GDDR7) market value chain.

Thermal Management and Power Density Constraints

As memory bandwidth requirements scale with each successive GPU generation, the thermal and power density challenges associated with high-speed GDDR operation intensify. GDDR6 operating at maximum data rates generates significant heat, requiring advanced PCB design, thermal interface materials, and cooling solutions to maintain reliability. While GDDR7’s architecture incorporates efficiency improvements, the higher absolute bandwidth targets introduce new thermal design challenges, particularly in compact form-factor applications such as laptops, automotive modules, and edge inference accelerators where thermal budgets are tightly constrained.

MARKET RESTRAINTS

Competition from Alternative Memory Architectures Including HBM and Integrated Solutions

A significant restraint on Graphics DRAM Market’s growth trajectory is the increasing adoption of High Bandwidth Memory (HBM) in premium data center GPU and AI accelerator platforms. HBM offers substantially higher aggregate bandwidth and better energy efficiency per bit transferred compared to GDDR6, making it the preferred choice for high-end AI training accelerators and professional compute cards where performance-per-watt is paramount. As HBM adoption expands beyond flagship AI chips into broader professional GPU segments, the total addressable market for GDDR6 and GDDR7 in the high-performance compute segment faces structural pressure, limiting upside potential in some of the market’s highest-value application areas.

Geopolitical Risks and Export Control Regulations Affecting Market Access

Geopolitical tensions and the evolving landscape of semiconductor export controls represent a meaningful restraint on Graphics DRAM Market. Regulatory restrictions on the export of advanced GPU and associated memory technologies to certain markets have created demand uncertainty for both GPU vendors and GDDR suppliers. Trade policy shifts, tariff impositions, and technology transfer restrictions can alter procurement strategies, redirect supply chains, and suppress end-market demand in affected regions. These externalities introduce planning complexity for memory manufacturers executing multi-year capacity investment decisions in Graphics DRAM (GDDR6, GDDR7) ecosystem, and can dampen overall market growth relative to baseline demand fundamentals.

MARKET OPPORTUNITIES

GDDR7 Adoption Across Consumer GPU and Edge AI Platforms Opens New Revenue Streams

The commercial introduction and ongoing ramp of GDDR7 represents one of the most significant near-term growth opportunities in Graphics DRAM Market. With leading GPU vendors beginning to qualify GDDR7 for their next-generation discrete graphics product lines, memory suppliers are positioned to capture higher average selling prices and improved margins relative to mature GDDR6 products. The performance leap offered by GDDR7 , including higher per-pin data rates and improved signal integrity , makes it well-suited not only for flagship gaming GPUs but also for emerging edge AI inference cards, professional workstation GPUs, and advanced driver assistance system processors, meaningfully expanding the addressable application landscape for Graphics DRAM technology.

Automotive and Industrial Computing Segments Emerging as High-Growth End Markets

The automotive sector is emerging as a structurally significant growth opportunity for Graphics DRAM suppliers. The proliferation of advanced driver assistance systems, in-vehicle infotainment platforms, and autonomous driving compute modules is driving adoption of automotive-grade GDDR6 memory, with qualifications for automotive GDDR7 expected to follow. Automotive-grade memory commands premium pricing due to stringent quality, reliability, and longevity requirements, offering memory suppliers an opportunity to diversify revenue streams beyond the cyclical consumer GPU segment. As vehicle architectures evolve toward centralized compute domain controllers handling perception, mapping, and rendering workloads simultaneously, the per-vehicle Graphics DRAM content is expected to rise substantially, supporting long-term demand growth in Graphics DRAM (GDDR6, GDDR7) market.

Expansion of Cloud Gaming and GPU-as-a-Service Infrastructure Driving Sustained Procurement Cycles

Cloud gaming platforms and GPU-as-a-service offerings represent a growing and relatively stable demand channel for Graphics DRAM. Unlike consumer hardware cycles, which are tied to irregular product refresh schedules, cloud gaming infrastructure operators pursue continuous capacity expansion to support subscriber growth and maintain competitive performance benchmarks. This creates a more predictable, multi-year procurement pattern for GDDR6-equipped GPUs, benefiting memory suppliers with greater demand visibility. As streaming resolutions increase and latency requirements tighten, cloud gaming operators are expected to transition toward GDDR7-equipped hardware at an accelerating pace, further supporting the revenue outlook for next-generation Graphics DRAM products across the broader market ecosystem.

Trends

Accelerating Transition from GDDR6 to GDDR7 Reshaping Graphics DRAM Market

Graphics DRAM (GDDR6, GDDR7) market is undergoing a significant generational shift as the industry transitions from GDDR6 to the next-generation GDDR7 standard. GDDR7 delivers data transfer speeds exceeding 32 Gbps per pin, representing a substantial leap over GDDR6 capabilities. This performance advancement is accelerating adoption across premium GPU platforms from leading manufacturers. Samsung Electronics and SK Hynix have both announced mass production milestones for GDDR7 memory, specifically targeting next-generation GPU architectures developed by NVIDIA and AMD. This competitive momentum among leading semiconductor firms is fundamentally reshaping product roadmaps and supply chain strategies within Graphics DRAM (GDDR6, GDDR7) market.

Other Trends

Surging Demand from AI and Machine Learning Workloads

One of the most prominent trends influencing Graphics DRAM (GDDR6, GDDR7) market is the rapid proliferation of artificial intelligence and machine learning applications. AI accelerators and high-performance computing systems increasingly rely on high-bandwidth graphics memory to manage the parallel data processing demands of modern workloads. Both GDDR6 and GDDR7 are integral to AI-optimized GPU architectures, enabling faster model training and inference. As enterprises and cloud providers continue scaling their AI infrastructure, the demand for advanced graphics memory solutions is expected to remain a key growth driver across the forecast period.

Expanding Role in Gaming Consoles and Discrete Graphics Cards

Global gaming industry continues to serve as a foundational demand pillar for Graphics DRAM (GDDR6, GDDR7) market. Modern discrete graphics cards and gaming consoles depend heavily on high-performance graphics memory to deliver immersive visual experiences at high resolutions and frame rates. GDDR6 remains widely deployed across mid-range and high-end gaming GPU segments, while GDDR7 adoption is gaining traction in flagship product lines. The ongoing development of visually intensive gaming titles and the growth of cloud gaming platforms are further sustaining demand for advanced graphics memory technologies.

Competitive Landscape and Key Player Strategies Driving Market Dynamics

The competitive dynamics of Graphics DRAM (GDDR6, GDDR7) market are largely shaped by the strategic initiatives of leading memory manufacturers. Samsung Electronics Co., Ltd., SK Hynix Inc., and Micron Technology, Inc. operate with extensive product portfolios spanning both GDDR6 and GDDR7 memory solutions. These companies are investing heavily in manufacturing capacity, process node advancements, and collaborative engagements with GPU designers to secure design wins for next-generation platforms. Their ability to scale production of GDDR7 at competitive yields will be a critical determinant of market positioning as premium GPU adoption broadens across workstation, data center, and consumer segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Graphics DRAM (GDDR6, GDDR7) Market: Competitive Dynamics and Leading Semiconductor Players Shaping Next-Generation Memory Standards

Global Graphics DRAM (GDDR6, GDDR7) market is highly consolidated, dominated by a small number of vertically integrated semiconductor giants with the fabrication expertise and capital investment necessary to develop and manufacture cutting-edge high-bandwidth memory. Samsung Electronics Co., Ltd. holds a commanding position in this space, having achieved mass production milestones for GDDR7 memory and supplying leading GPU architects including NVIDIA and AMD. SK Hynix Inc. stands as another dominant force, having announced its own GDDR7 mass production rollout targeting next-generation discrete GPU platforms. Micron Technology, Inc. rounds out the primary tier of market leaders, offering a comprehensive portfolio of GDDR6 and GDDR7 solutions designed for gaming GPUs, AI accelerators, and workstation-class graphics hardware. Together, these three companies command the vast majority of global Graphics DRAM supply, benefiting from established wafer fabrication infrastructure, deep R&D pipelines, and long-term supply agreements with major GPU designers. The ongoing transition from GDDR6 to GDDR7 , with data transfer speeds exceeding 32 Gbps per pin , is intensifying competition among these players as they race to capture premium GPU platform design wins.

Beyond the leading trio, several other companies contribute meaningfully to the broader Graphics DRAM ecosystem through GPU design, memory controller integration, and platform enablement. NVIDIA Corporation and Advanced Micro Devices (AMD), while primarily GPU architects, exert significant influence over the competitive landscape by dictating memory interface specifications and qualification requirements for GDDR6 and GDDR7 adoption. Intel Corporation has also entered the discrete GPU arena with its Arc graphics lineup, creating incremental demand for GDDR6 memory. On the memory supply chain side, companies such as Winbond Electronics, CXMT (ChangXin Memory Technologies), and Nanya Technology maintain relevance in adjacent DRAM segments and are monitoring the high-bandwidth memory space for future expansion opportunities. Equipment and IP suppliers including Cadence Design Systems and Synopsys play enabling roles in the development of GDDR7-compliant memory controller IP, further shaping how swiftly GPU vendors can adopt next-generation memory standards across consumer, professional, and AI-accelerated computing platforms.

List of Key Graphics DRAM (GDDR6, GDDR7) Companies Profiled

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Micron Technology, Inc.

- NVIDIA Corporation

- Advanced Micro Devices, Inc. (AMD)

- Intel Corporation

- Winbond Electronics Corporation

- Nanya Technology Corporation

- ChangXin Memory Technologies, Inc. (CXMT)

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- JEDEC Solid State Technology Association (Standards Body)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GDDR6 currently holds the dominant position in Graphics DRAM Market, underpinned by its widespread deployment across a broad spectrum of discrete graphics cards, gaming consoles, and professional workstation GPUs.

|

| By Application |

|

Gaming Graphics Cards represent the largest and most established application segment within Graphics DRAM Market, driven by the continuously expanding global gaming industry and the relentless consumer demand for immersive, high-resolution visual experiences.

|

| By End User |

|

Consumer Electronics Manufacturers constitute the leading end-user segment, encompassing GPU card makers, gaming console developers, and personal computer OEMs who integrate Graphics DRAM into their flagship products to meet demanding consumer performance expectations.

|

| By Interface Standard |

|

GDDR6X (Extended) leads within the interface standard segmentation as it bridges the generational gap between GDDR6 and GDDR7, offering substantially elevated throughput through PAM4 (Pulse Amplitude Modulation) signaling that enables higher data rates without requiring a full architectural transition.

|

| By Capacity |

|

8 GB to 16 GB capacity range dominates Graphics DRAM Market, reflecting the mainstream GPU segment’s requirement for memory configurations that balance high performance with cost-effectiveness across a wide range of consumer and professional applications.

|

Regional Analysis: Graphics DRAM (GDDR6, GDDR7) Market

Asia-Pacific

Asia-Pacific hosts the most vertically integrated semiconductor supply chains in the world. From raw silicon wafers and advanced lithography tools to final GDDR6 and GDDR7 memory packaging, the region controls critical links in Graphics DRAM value chain. This concentration of manufacturing capability enables rapid scaling of production in response to surging demand from AI accelerators, gaming GPUs, and professional visualization workloads.

Leading memory developers across South Korea and Taiwan are aggressively investing in GDDR7 architecture research, targeting higher bandwidth efficiency and reduced power consumption. Collaborative efforts between memory designers and GPU vendors in the region are accelerating qualification timelines for next-generation Graphics DRAM, ensuring Asia-Pacific retains first-mover advantages as GDDR7 adoption expands across workstation and data center segments.

The region’s vast and growing base of gaming enthusiasts, content creators, and enterprise AI developers sustains strong domestic consumption of GDDR6-equipped discrete graphics cards. As regional cloud providers accelerate GPU cluster deployments, demand for high-density GDDR7 memory modules is gaining momentum, diversifying end-use beyond consumer gaming into professional and hyperscale computing environments across Japan, China, and Southeast Asia.

Government-led semiconductor self-sufficiency programs in China, South Korea, and Japan are channeling substantial investment into domestic Graphics DRAM ecosystems. Subsidies, tax incentives, and state-backed research consortiums are reducing dependency on external supply chains while fostering local talent pipelines. These strategic initiatives are expected to strengthen Asia-Pacific’s competitive positioning in both GDDR6 production and the accelerating transition toward GDDR7 across the forecast horizon.

North America

North America represents one of the most strategically significant regions in Graphics DRAM Market, serving as the epicenter of GPU design innovation and high-performance computing demand. The United States, in particular, is home to the world’s leading GPU architects whose product roadmaps directly dictate global GDDR6 and GDDR7 specification requirements. The region’s robust data center sector, underpinned by hyperscale cloud operators and AI infrastructure buildouts, is generating unprecedented demand for bandwidth-intensive memory solutions. The rapid proliferation of generative AI platforms and machine learning workloads has notably elevated GDDR7 evaluation activity among enterprise hardware buyers. Additionally, the U.S. defense and aerospace sector continues to drive demand for specialized Graphics DRAM configurations in high-reliability computing platforms. Semiconductor policy initiatives aimed at reshoring advanced chip manufacturing are gradually reshaping North America’s supply chain posture, with new domestic fabrication investments expected to influence regional Graphics DRAM availability and strategic sourcing decisions well into the 2030s.

Europe

Europe occupies a measured but increasingly important position in Global Graphics DRAM landscape, driven by its expanding technology and automotive sectors. Germany, France, and the Netherlands are key contributors to regional demand, particularly as automotive-grade GPU applications integrating GDDR6 memory gain traction in advanced driver assistance and autonomous vehicle platforms. European semiconductor policy frameworks, including the European Chips Act, are fostering greater regional investment in semiconductor design and manufacturing, which is expected to gradually strengthen local engagement with Graphics DRAM supply chains. The region’s growing cloud computing infrastructure and increasing enterprise adoption of AI-accelerated workloads are also supporting steady demand growth for GDDR6 and emerging GDDR7 solutions. Europe’s emphasis on energy-efficient computing aligns well with the improved power-to-performance characteristics of next-generation GDDR7 architectures, positioning the region as a discerning adopter as the technology matures through the forecast period.

South America

South America remains an emerging market within Global Graphics DRAM ecosystem, with demand primarily shaped by expanding consumer electronics adoption and a growing base of gaming enthusiasts, particularly in Brazil and Mexico. While the region does not host significant Graphics DRAM manufacturing activity, its role as an end-consumption market for GDDR6-equipped graphics cards is steadily expanding alongside rising disposable incomes and improved digital infrastructure. The gradual formalization of e-sports and content creation economies in major South American markets is contributing to higher-tier GPU purchases, indirectly supporting GDDR6 demand. Challenges such as import tariffs, currency volatility, and inconsistent semiconductor distribution networks continue to temper growth momentum. However, increasing internet penetration and cloud gaming platform adoption may shift some hardware demand dynamics over the medium term, creating selective opportunities for Graphics DRAM market participants targeting the region’s digitally active consumer segments.

Middle East & Africa

The Middle East and Africa region represents the nascent frontier of Graphics DRAM Market, where demand is beginning to take shape against a backdrop of ambitious digital transformation agendas. Gulf Cooperation Council nations, particularly the UAE and Saudi Arabia, are investing heavily in data center infrastructure and AI capability development, generating early-stage demand for GDDR6 and high-bandwidth memory solutions in GPU-accelerated platforms. Smart city initiatives and sovereign AI strategies are expected to progressively incorporate advanced graphics processing infrastructure, lending long-term directional support to Graphics DRAM adoption. Africa’s contribution remains modest in the near term but carries latent potential as mobile-first digital economies mature and enterprise computing investments increase. Regional distribution challenges, limited semiconductor expertise, and infrastructure gaps will need to be addressed systematically. Nevertheless, the Middle East’s proactive technology investment posture positions it as the most active growth pocket within this broader region over the 2026–2034 forecast window.

Report Scope

This market research report provides a comprehensive analysis of the Graphics DRAM (GDDR6, GDDR7) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Graphics DRAM (GDDR6, GDDR7) Market?

-> Graphics DRAM (GDDR6, GDDR7) Market was valued at USD 14.32 billion in 2025 and is expected to reach USD 38.74 billion by 2034, growing at a CAGR of 11.6% during the forecast period from 2026 to 2034.

Which key companies operate in Graphics DRAM (GDDR6, GDDR7) Market?

-> Key players include Samsung Electronics Co., Ltd., SK Hynix Inc., and Micron Technology, Inc., among others, with extensive product portfolios spanning both GDDR6 and GDDR7 memory solutions.

What are the key growth drivers?

-> Key growth drivers include surging demand for high-performance computing, rapid proliferation of AI and machine learning workloads, and the expanding global gaming industry. The transition from GDDR6 to GDDR7 , offering data transfer speeds exceeding 32 Gbps per pin , is also accelerating adoption across premium GPU platforms.

Which region dominates the market?

-> Asia-Pacific is a key region in Graphics DRAM Market, driven by leading semiconductor manufacturers and large-scale GPU production, while North America remains a significant market supported by major AI and high-performance computing demand.

What are the emerging trends?

-> Emerging trends include mass production milestones for GDDR7 memory by Samsung Electronics and SK Hynix, next-generation GPU architectures from NVIDIA and AMD, and increasing integration of graphics DRAM in AI accelerators, gaming consoles, and workstation GPUs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...