X-Band Radar (Defense) RF Chip Market Insights

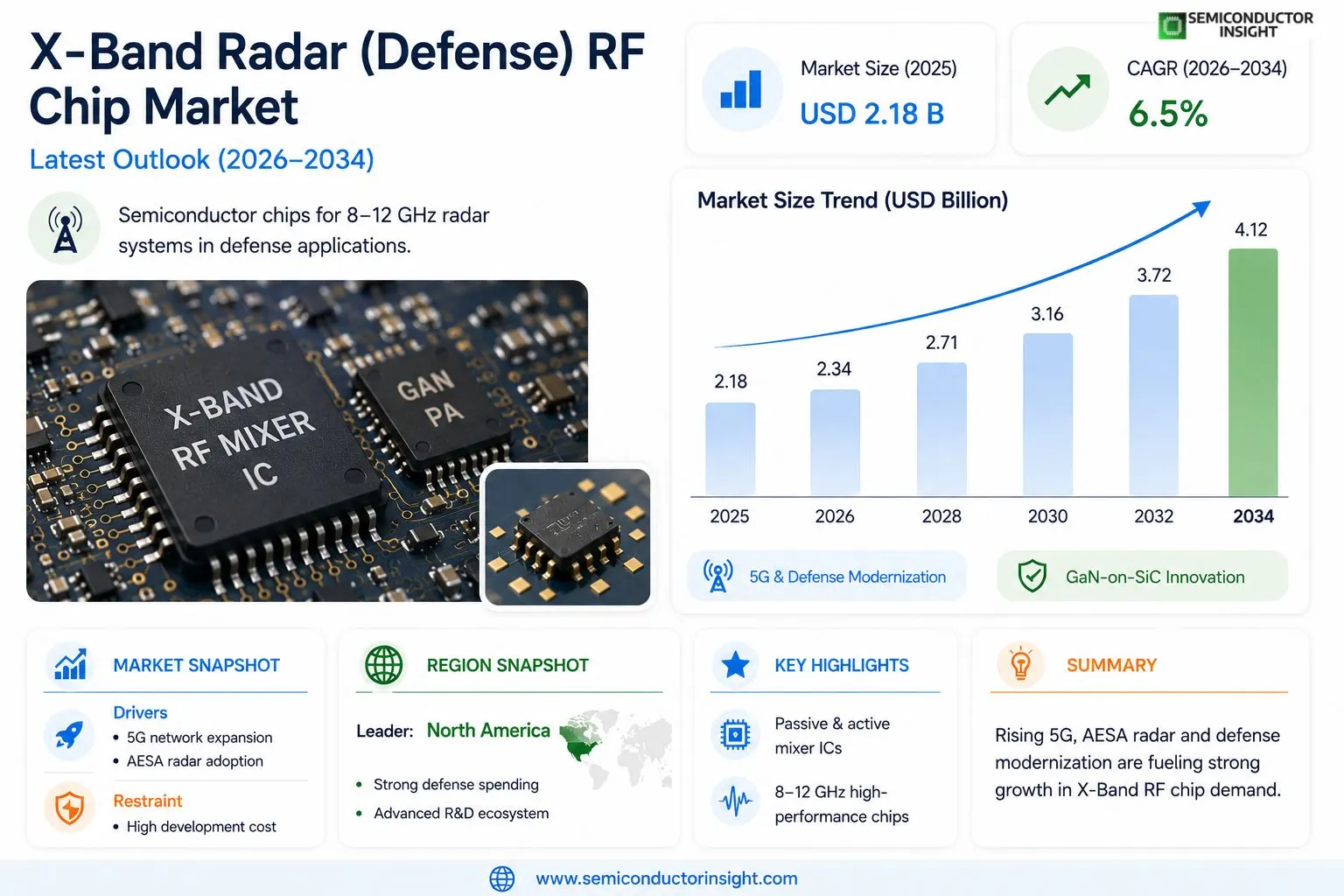

Global X-Band Radar (Defense) RF Chip Market size was valued at USD 2.18 billion in 2025. The market is projected to grow from USD 2.34 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

X-Band radar RF chips are specialized semiconductor components engineered to operate within the 8–12 GHz frequency range, making them integral to a wide array of defense radar systems. These chips are fundamental to applications including airborne early warning systems, naval surface search radars, ground-based air defense networks, and precision-guided munitions. The RF chip category encompasses monolithic microwave integrated circuits (MMICs), gallium nitride (GaN)-based power amplifiers, gallium arsenide (GaAs) components, transmit/receive (T/R) modules, and phased array radar chipsets, among others.

The market is witnessing robust momentum driven by escalating global defense budgets, the accelerating shift toward active electronically scanned array (AESA) radar platforms, and the growing strategic emphasis on electronic warfare capabilities. Furthermore, the widespread adoption of GaN-on-SiC technology has significantly enhanced power density and thermal efficiency in X-Band RF chips, making them increasingly preferred in next-generation defense radar architectures. Key industry participants such as Raytheon Technologies, Northrop Grumman Corporation, Renesas Electronics, Wolfspeed (formerly Cree), and MACOM Technology Solutions maintain strong competitive positions through continuous investment in advanced semiconductor fabrication and radar system integration.

MARKET DRIVERS

Rising Defense Modernization Programs Accelerating Demand for Advanced Radar RF Chips

Global defense modernization initiatives have emerged as a primary catalyst for growth in X-Band Radar (Defense) RF Chip Market. Nations across North America, Europe, and the Asia-Pacific region are significantly increasing defense budgets to upgrade aging radar infrastructure with next-generation phased array and active electronically scanned array (AESA) systems. These modern radar platforms rely heavily on high-performance X-Band RF chips capable of operating in the 8–12 GHz frequency range, driving sustained procurement demand. Countries including the United States, India, Japan, South Korea, and several NATO member states have allocated substantial capital expenditure toward airborne, maritime, and ground-based radar system upgrades, directly translating into increased component-level demand for defense-grade RF semiconductors.

Proliferation of AESA Radar Systems Driving High-Volume RF Chip Procurement

The widespread transition from mechanically scanned array radars to Active Electronically Scanned Array (AESA) architectures has significantly amplified the volume of X-Band RF chips required per radar platform. Unlike traditional radar systems, AESA radars integrate thousands of individual transmit/receive (T/R) modules, each incorporating dedicated X-Band RF chips for signal transmission, reception, and processing. This architectural shift has multiplied per-platform chip counts considerably, creating favorable volume dynamics within the X-Band Radar Defense RF Chip Market. Fighter aircraft programs, naval destroyers, and land-based air defense systems increasingly mandate AESA-based radar, with many new platforms specifying Gallium Nitride (GaN) and Gallium Arsenide (GaAs) monolithic microwave integrated circuits (MMICs) to achieve higher power density and improved thermal management.

➤ The accelerating integration of GaN-based X-Band RF chips into defense radar platforms is redefining performance benchmarks, with power-added efficiency levels and output power densities far exceeding legacy GaAs-based solutions, prompting widespread platform qualification programs across major defense primes.

Increasing geopolitical tensions and the corresponding emphasis on air defense capabilities and border surveillance have further reinforced procurement pipelines for X-Band defense radar systems. Military programs centered on missile defense, counter-drone operations, and coastal surveillance are driving long-term, multi-year contracts for radar platforms and their underlying RF chip supply chains. This demand environment supports stable capacity investments by leading semiconductor foundries and integrated device manufacturers specializing in defense-qualified X-Band RF components.

MARKET CHALLENGES

Stringent Military Qualification Standards Extending Time-to-Market for New X-Band RF Chip Designs

One of the most significant challenges confronting suppliers in X-Band Radar (Defense) RF Chip Market is the rigorous qualification process mandated by military procurement agencies. Defense-grade RF chips must comply with MIL-PRF-38535, MIL-STD-883, and equivalent international standards, requiring extensive environmental stress screening, reliability testing, and traceability documentation. The qualification lifecycle for a new X-Band MMIC design can span several years, delaying revenue realization and increasing non-recurring engineering costs substantially. Smaller fabless design companies with limited resources face particularly acute challenges navigating these requirements, potentially restricting market participation to a concentrated group of established defense semiconductor suppliers.

Other Challenges

Geopolitical Export Controls and Supply Chain Concentration

X-Band defense RF chips are subject to stringent export control regulations including the International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR) in the United States, as well as equivalent controls in other jurisdictions. These regulatory frameworks restrict technology transfer, limit accessible customer bases for suppliers, and impose significant compliance overhead. Additionally, the specialized compound semiconductor fabrication required for high-performance GaN and GaAs X-Band chips is concentrated among a limited number of qualified defense foundries, creating potential supply chain vulnerability. Disruptions at any single foundry can materially impact production schedules for downstream radar system integrators relying on the X-Band Radar Defense RF Chip supply base.

High Development and Production Costs Constraining Market Accessibility

The fabrication of defense-grade X-Band RF chips on compound semiconductor processes such as GaN-on-SiC involves substantially higher wafer costs compared to commercial CMOS processes. Combined with the low production volumes characteristic of defense applications and the engineering investment required to meet military performance specifications, the total cost of ownership for X-Band defense RF chips remains elevated. This cost structure can create affordability pressure in defense procurement programs operating under fixed budgets, while also limiting the ability of emerging players to compete without significant capital backing or government-sponsored research and development funding.

MARKET RESTRAINTS

Limited Qualified Foundry Capacity for Defense-Grade Compound Semiconductor Fabrication

A structural restraint on X-Band Radar (Defense) RF Chip Market is the constrained availability of fabrication capacity at foundries certified to produce defense-qualified compound semiconductor wafers. GaN-on-SiC and GaAs processes used for high-power X-Band radar chips require specialized epitaxial growth equipment, cleanroom environments, and process controls that are not broadly replicated across Global semiconductor manufacturing ecosystem. The relatively small total addressable market for defense RF chips discourages large-scale capacity expansions by commercial foundries, while existing qualified defense foundries operate with limited surge capacity. This dynamic can result in extended lead times during periods of heightened demand, constraining the ability of radar system integrators to scale production in response to accelerated procurement timelines.

Technological Transition Risks Associated with Shifting from Legacy GaAs to GaN Platforms

While GaN-based X-Band RF chips offer compelling performance advantages over legacy GaAs solutions, the transition introduces qualification and integration risks that can restrain near-term market adoption. Defense programs with existing radar platforms qualified on GaAs-based components face significant re-qualification burdens when upgrading to GaN alternatives, including thermal management redesigns, bias circuit modifications, and system-level electromagnetic compatibility validation. Programs with long operational service lives may defer technology transitions to avoid qualification cost and schedule risk, temporarily sustaining demand for mature GaAs X-Band chips while slowing penetration of next-generation GaN devices. This technology transition dynamic creates a bifurcated demand environment within the X-Band Radar Defense RF Chip Market that complicates long-term capacity planning for suppliers.

MARKET OPPORTUNITIES

Expansion of Unmanned and Autonomous Defense Platforms Creating New X-Band RF Chip Application Areas

The rapid proliferation of unmanned aerial vehicles (UAVs), unmanned surface vessels (USVs), and autonomous ground vehicles in defense applications presents a substantial growth opportunity for X-Band Radar (Defense) RF Chip Market. These platforms increasingly incorporate miniaturized, low-power X-Band radar systems for terrain avoidance, target acquisition, sense-and-avoid functionality, and battlefield situational awareness. The design constraints of unmanned platforms , including strict size, weight, and power (SWaP) requirements , are driving demand for highly integrated X-Band RF chip solutions that consolidate multiple radar front-end functions into compact monolithic or multi-chip module formats. Semiconductor suppliers capable of delivering SWaP-optimized X-Band defense RF chips with competitive power efficiency are well-positioned to capture design wins across a rapidly expanding addressable platform base.

Government Investment in Domestic Defense Semiconductor Supply Chains Supporting Market Expansion

Strategic government initiatives to strengthen domestic defense semiconductor supply chains represent a meaningful tailwind for the X-Band Radar RF Chip Market. Programs such as the U.S. CHIPS and Science Act and analogous industrial policy measures in Europe, Japan, South Korea, and India are directing funding toward the expansion of domestic compound semiconductor fabrication capabilities relevant to defense radar applications. Subsidized foundry capacity expansions and government-sponsored research programs focused on next-generation RF materials, including GaN-on-Diamond and advanced silicon carbide substrates, are expected to improve supply chain resilience while reducing long-term production costs. These investments are anticipated to attract new entrants to the defense RF chip sector, broaden the qualified supplier base, and support the development of higher-performance X-Band components aligned with emerging radar requirements across air, land, sea, and space domains.

X-Band Radar (Defense) RF Chip Market Trends

Accelerating Shift Toward Active Electronically Scanned Array (AESA) Radar Platforms

One of the most defining trends reshaping X-Band Radar (Defense) RF Chip Market is the accelerating transition from mechanically scanned to active electronically scanned array (AESA) radar architectures. Defense forces worldwide are prioritizing AESA-based systems for their superior beam agility, multi-mission capability, and enhanced electronic counter-countermeasure (ECCM) performance. X-Band RF chips, particularly phased array chipsets and transmit/receive (T/R) modules operating in the 8–12 GHz frequency range, are central to these next-generation platforms. The growing deployment of AESA radars across airborne early warning systems, naval surface search radars, and ground-based air defense networks is directly fueling demand for high-performance X-Band semiconductor components. Leading defense contractors such as Raytheon Technologies and Northrop Grumman Corporation continue to invest heavily in AESA integration, reinforcing the strategic importance of advanced RF chip development within this market.

Other Trends

Widespread Adoption of GaN-on-SiC Technology

X-Band Radar (Defense) RF Chip Market is experiencing a significant technological shift with the widespread adoption of gallium nitride on silicon carbide (GaN-on-SiC) technology. Compared to legacy gallium arsenide (GaAs) components, GaN-on-SiC-based power amplifiers deliver substantially higher power density, improved thermal efficiency, and greater reliability under demanding operational conditions. These characteristics make GaN-based X-Band RF chips increasingly preferred in modern defense radar architectures. Companies such as Wolfspeed (formerly Cree) and MACOM Technology Solutions are at the forefront of advancing GaN semiconductor fabrication, enabling more compact and power-efficient radar system designs across both airborne and ground-based defense applications.

Escalating Global Defense Budgets Driving Procurement

Rising geopolitical tensions across multiple regions have prompted governments to substantially increase defense spending, directly benefiting X-Band Radar (Defense) RF Chip Market. Expanded procurement of radar-equipped platforms , including precision-guided munitions, naval vessels, and advanced fighter aircraft , is creating sustained demand for monolithic microwave integrated circuits (MMICs) and phased array chipsets optimized for X-Band frequencies. This budgetary momentum is encouraging domestic semiconductor manufacturers and defense electronics suppliers to scale production capacity and accelerate research and development in advanced RF chip fabrication.

Growing Strategic Emphasis on Electronic Warfare Capabilities

Electronic warfare (EW) has emerged as a critical dimension of modern defense strategy, and this trend is having a direct impact on X-Band Radar (Defense) RF Chip Market. Military organizations are increasingly integrating X-Band radar systems with electronic attack and electronic protection functionalities, necessitating RF chips capable of operating effectively in highly contested electromagnetic environments. This requirement is driving innovation in chip design, particularly in the development of wideband, low-noise, and high-linearity components. Industry participants such as Renesas Electronics and MACOM Technology Solutions are actively expanding their X-Band RF portfolios to address the complex signal processing and frequency agility demands inherent to next-generation electronic warfare and radar system integration.

COMPETITIVE LANDSCAPE

Key Industry Players

X-Band Radar (Defense) RF Chip Market: Competitive Dynamics and Leading Innovators Shaping Next-Generation Defense Radar Systems

Global X-Band Radar (Defense) RF Chip Market is characterized by a concentrated yet highly innovative competitive environment, where a handful of technologically advanced defense electronics and semiconductor companies command significant market share. Raytheon Technologies remains a dominant force, leveraging its deep integration across AESA radar platforms, airborne early warning systems, and naval radar architectures. The company’s sustained investment in GaN-on-SiC-based monolithic microwave integrated circuits (MMICs) and transmit/receive (T/R) modules positions it as the benchmark competitor in this space. Northrop Grumman Corporation similarly holds a formidable position, driven by its advanced phased array radar programs and electronic warfare systems that rely heavily on proprietary X-Band RF chipsets. MACOM Technology Solutions and Wolfspeed (formerly Cree) are recognized leaders in GaN-based power amplifiers, with both companies supplying high-efficiency RF components widely adopted across ground-based air defense and precision-guided munitions applications. The market’s projected expansion from USD 2.34 billion in 2026 to USD 4.12 billion by 2034, at a CAGR of 6.5%, underscores the intensifying competitive race to develop higher power density, thermally efficient, and frequency-agile X-Band RF chips for next-generation defense platforms.

Beyond the tier-one defense primes, several specialized semiconductor and RF component manufacturers are carving out significant niches within the X-Band Radar RF Chip Market. Renesas Electronics has strengthened its defense semiconductor portfolio through strategic acquisitions and organic R&D in GaAs and GaN technologies suited for radar front-end applications. Qorvo and Analog Devices are notable for their broad MMIC product lines targeting both airborne and surface radar systems, while Microchip Technology and NXP Semiconductors contribute through high-reliability RF and mixed-signal components deployed in military-grade radar environments. Companies such as Sumitomo Electric Industries and Mitsubishi Electric are prominent in the Asia-Pacific competitive landscape, supplying GaN-based MMICs to regional defense programs. Meanwhile, emerging players including Cissoid and RFHIC Corporation are gaining traction by focusing on niche high-power GaN device segments. The competitive intensity is further amplified by ongoing government-funded R&D programs in the United States, Europe, and Asia, which continue to accelerate semiconductor innovation across the X-Band defense radar value chain.

List of Key X-Band Radar (Defense) RF Chip Companies Profiled

- Raytheon Technologies

- Northrop Grumman Corporation

- MACOM Technology Solutions

- Wolfspeed (formerly Cree)

- Renesas Electronics

- Qorvo

- Analog Devices

- Microchip Technology

- NXP Semiconductors

- Sumitomo Electric Industries

- Mitsubishi Electric Corporation

- RFHIC Corporation

- Cissoid

- BAE Systems

- Leonardo DRS

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Gallium Nitride (GaN)-Based RF Chips represent the leading and most strategically significant segment within the X-Band Radar Defense RF Chip market by type, owing to their superior material properties and performance advantages over legacy technologies.

|

| By Application |

|

Airborne Early Warning (AEW) Systems constitute the leading application segment for X-Band Radar Defense RF Chips, reflecting the growing strategic priority that defense establishments worldwide place on long-range aerial surveillance and situational awareness capabilities.

|

| By End User |

|

Air Force remains the dominant end-user segment in the X-Band Radar Defense RF Chip market, driven by the sustained modernization of combat aircraft radar suites, early warning platforms, and unmanned aerial vehicle (UAV) sensor payloads.

|

| By Technology |

|

Active Electronically Scanned Array (AESA) technology represents the most transformative and rapidly expanding segment shaping demand patterns for X-Band Radar Defense RF Chips, fundamentally redefining the performance expectations and procurement priorities of modern defense radar programs.

|

| By Platform |

|

Airborne Platforms lead the platform-based segmentation of the X-Band Radar Defense RF Chip market, as they impose the most demanding performance, miniaturization, and reliability requirements on the underlying semiconductor components.

|

Regional Analysis: X-Band Radar (Defense) RF Chip Market

North America

North America’s X-Band Radar (Defense) RF Chip Market is bolstered by robust federal procurement mechanisms. Multi-year defense authorization acts ensure consistent budgetary allocations toward radar modernization. Regulatory frameworks prioritize domestic sourcing of critical semiconductor components, reducing supply chain vulnerabilities and incentivizing local RF chip manufacturers to scale production capabilities for advanced defense radar applications.

The region hosts a dense network of defense-focused semiconductor research centers, national laboratories, and private R&D facilities advancing X-Band RF chip architectures. Innovations in wide-bandgap semiconductor materials, monolithic microwave integrated circuits (MMICs), and active electronically scanned array (AESA) radar technologies continue to originate from North American institutions, reinforcing the region’s global technological leadership.

North American demand for X-Band radar RF chips spans a broad spectrum of defense platforms, including airborne early warning systems, ship-borne fire control radars, ground-based air defense installations, and unmanned aerial systems. The increasing integration of X-Band radar into next-generation fighter aircraft and ballistic missile defense interceptor systems positions the region as a critical consumption hub for high-performance RF chip solutions.

North America’s X-Band Radar (Defense) RF Chip Market is characterized by a concentrated supplier landscape, with a handful of Tier-1 defense electronics firms holding long-standing relationships with the Department of Defense. Efforts to nearshore advanced semiconductor fabrication and reduce dependence on foreign foundries are reshaping supply chain strategies, encouraging vertical integration among leading defense RF chip developers and manufacturers.

Europe

Europe represents a strategically significant and steadily expanding region within Global X-Band Radar (Defense) RF Chip Market. Nations including the United Kingdom, France, Germany, and Italy maintain sophisticated defense electronics industries capable of designing and manufacturing high-performance radar RF chips tailored for NATO-standard platforms. Heightened geopolitical tensions along the continent’s eastern flank have accelerated defense spending across multiple European Union member states, translating into increased procurement of advanced radar systems equipped with X-Band RF chipsets. Collaborative multinational defense programs, such as those coordinated through the European Defence Agency, are fostering joint development initiatives for next-generation radar technologies. European defense contractors are also making notable investments in GaN-based RF chip capabilities to reduce strategic dependence on non-European semiconductor suppliers. The region’s strong aerospace manufacturing base and established radar system integrators ensure a consistent and growing pipeline of demand for X-Band radar RF chips across airborne, naval, and ground-based defense applications throughout the forecast period.

Asia-Pacific

Asia-Pacific is emerging as the most rapidly evolving region in Global X-Band Radar (Defense) RF Chip Market, propelled by escalating territorial disputes, expanding naval ambitions, and aggressive military modernization programs across key nations. China, Japan, South Korea, India, and Australia are all substantially increasing defense budgets, with a pronounced emphasis on radar-centric situational awareness and precision-guided weapons systems that rely heavily on X-Band RF chip technology. China’s domestic semiconductor push is driving indigenous development of radar-grade RF chips, while Japan and South Korea are advancing their capabilities through close collaboration with U.S. defense technology partners. India’s ongoing modernization of its air defense and maritime surveillance networks is generating significant demand for X-Band radar solutions. Australia’s strategic alignment with the AUKUS partnership is further accelerating regional investment in advanced radar electronics. The competitive and security dynamics across the Indo-Pacific region are expected to sustain robust market momentum throughout the forecast period.

South America

South America occupies a comparatively nascent but gradually developing position within Global X-Band Radar (Defense) RF Chip Market. Brazil stands out as the region’s primary contributor, driven by its ambitions to modernize the Brazilian Air Force and Navy with contemporary radar surveillance capabilities. The country’s ongoing investment in border security infrastructure and aerial sovereignty monitoring is generating incremental demand for X-Band radar systems integrated with capable RF chip solutions. Argentina and Chile similarly maintain measured but consistent defense modernization agendas that include radar system upgrades. However, the region’s overall market growth is tempered by constrained defense budgets, limited domestic semiconductor manufacturing capacity, and a strong reliance on imported radar systems from North American and European suppliers. As regional defense priorities evolve and partnerships with established defense technology exporters deepen, South America’s role in X-Band Radar (Defense) RF Chip Market is anticipated to expand modestly over the forecast horizon.

Middle East & Africa

The Middle East & Africa region presents a compelling and increasingly active landscape within Global X-Band Radar (Defense) RF Chip Market, shaped by persistent regional security challenges, elevated defense procurement activity, and substantial sovereign wealth-backed military investments. Gulf Cooperation Council nations, particularly Saudi Arabia and the United Arab Emirates, are among the most prolific defense spenders globally, channeling significant resources into advanced air defense systems, early warning radar networks, and missile defense platforms that depend on sophisticated X-Band RF chip architectures. Israel maintains a world-class defense electronics industry with deep expertise in radar system development, including indigenous X-Band radar RF chip design capabilities. Africa, while currently a minor contributor, is witnessing nascent demand driven by peacekeeping, border surveillance, and counter-terrorism radar requirements. The region’s X-Band Radar (Defense) RF Chip Market is primarily supplied through foreign military sales agreements and strategic partnerships with leading North American and European defense technology exporters, with localization efforts beginning to take shape in select Middle Eastern nations.

Report Scope

This market research report provides a comprehensive analysis of the X-Band Radar (Defense) RF Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of X-Band Radar (Defense) RF Chip Market?

-> Global X-Band Radar (Defense) RF Chip Market size was valued at USD 2.18 billion in 2025 and is projected to grow from USD 2.34 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

Which key companies operate in X-Band Radar (Defense) RF Chip Market?

-> Key players include Raytheon Technologies, Northrop Grumman Corporation, Renesas Electronics, Wolfspeed (formerly Cree), and MACOM Technology Solutions, among others.

What are the key growth drivers?

-> Key growth drivers include escalating global defense budgets, the accelerating shift toward active electronically scanned array (AESA) radar platforms, growing strategic emphasis on electronic warfare capabilities, and widespread adoption of GaN-on-SiC technology that has significantly enhanced power density and thermal efficiency in X-Band RF chips.

Which region dominates the market?

-> North America remains a dominant market driven by significant defense spending and advanced radar system development, while Asia-Pacific is the fastest-growing region due to increasing defense modernization programs.

What are the emerging trends?

-> Emerging trends include GaN-on-SiC power amplifier adoption, integration of phased array radar chipsets, advancement in monolithic microwave integrated circuits (MMICs), and the growing deployment of X-Band RF chips in airborne early warning systems, naval surface search radars, and precision-guided munitions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...