Tinnitus Masking (Sound Generator) IC Market Insights

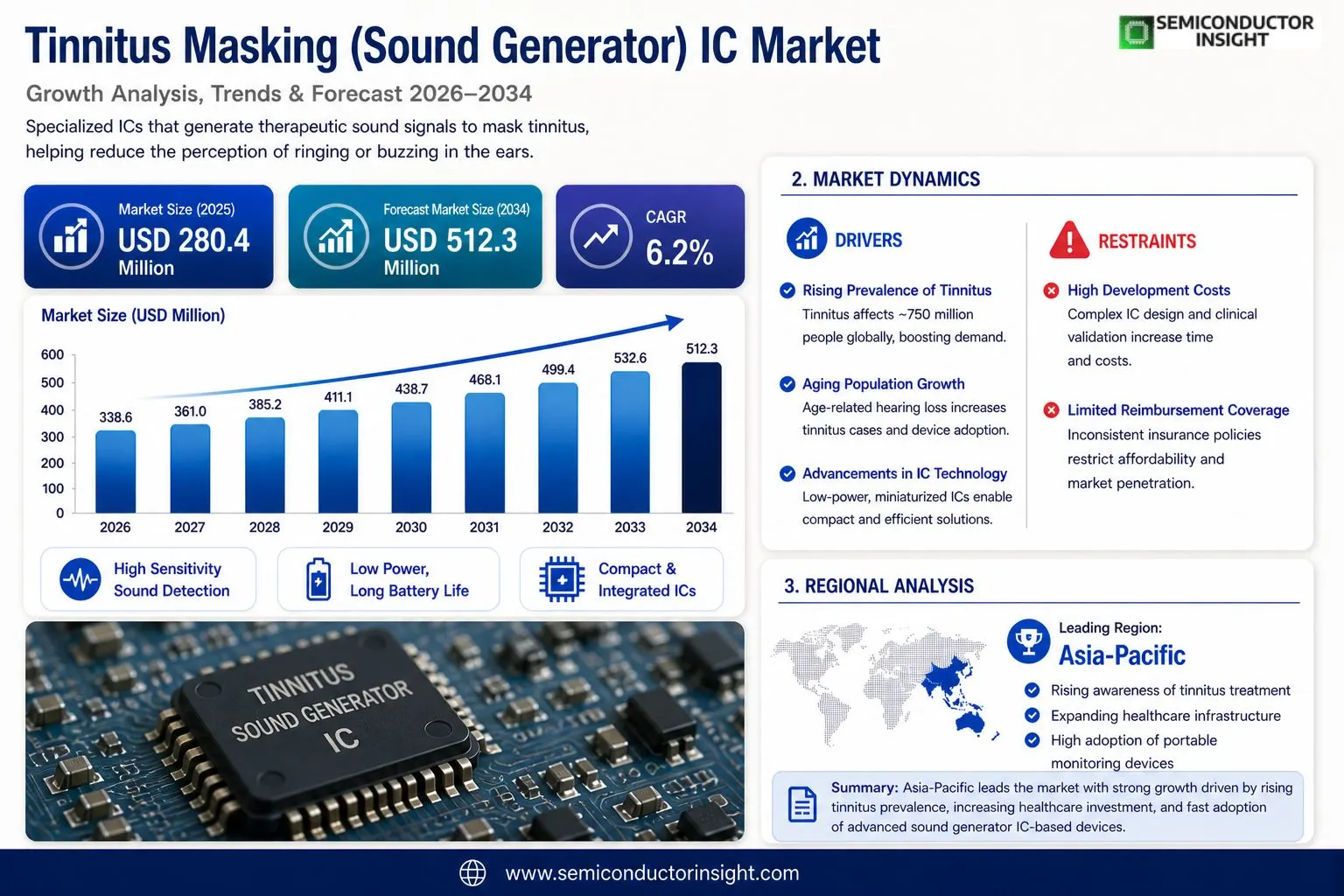

Global Tinnitus Masking (Sound Generator) IC market size was valued at USD 280.4 million in 2025. The market is projected to grow from USD 298.6 million in 2026 to USD 512.3 million by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Tinnitus masking integrated circuits (ICs) are specialized semiconductor components designed to generate therapeutic sound signals that help suppress or neutralize the perception of tinnitus , a condition characterized by persistent ringing, buzzing, or hissing sounds in the ears. These ICs serve as the core processing units within sound therapy devices, including wearable sound generators, hearing aids with masking functionality, and dedicated tinnitus relief devices. They encompass analog and digital signal generation architectures capable of producing white noise, pink noise, notched sound therapy, and customizable broadband audio outputs.

The market is gaining significant momentum, driven primarily by the rising global prevalence of tinnitus, which affects approximately 15% of the world’s population , roughly 750 million individuals , according to estimates from the World Health Organization. Furthermore, the aging global population continues to accelerate demand, as tinnitus incidence is closely correlated with age-related hearing loss. Advancements in low-power IC design and miniaturization technologies are enabling manufacturers to develop increasingly compact and energy-efficient masking solutions compatible with next-generation hearing aids and wearables. Key players operating in this space include Sonova Holding AG, Starkey Hearing Technologies, and GN Audio A/S, each maintaining diversified product portfolios that integrate tinnitus masking IC capabilities within broader audiological device ecosystems.

MARKET DRIVERS

Rising Global Prevalence of Tinnitus Fueling Demand for Sound Generator ICs

The growing incidence of tinnitus worldwide stands as one of the most significant factors propelling Tinnitus Masking (Sound Generator) IC Market forward. According to epidemiological data, tinnitus affects a substantial portion of the adult population globally, with chronic cases creating persistent demand for therapeutic and management devices. As awareness of tinnitus as a clinical condition continues to improve among both patients and healthcare providers, the adoption of sound masking solutions embedded with specialized integrated circuits has accelerated considerably. The shift from simple analog noise generators toward sophisticated digital sound generator ICs capable of producing personalized masking sounds has further expanded addressable market opportunities.

Technological Advancements in Hearing Aid and Wearable Audio Devices

Continuous innovation in hearing aid platforms and miniaturized wearable audio electronics has created a strong technology pull for advanced tinnitus masking sound generator ICs. Modern hearing aids increasingly integrate tinnitus sound therapy features, requiring highly efficient, low-power ICs capable of generating a broad spectrum of therapeutic sounds including white noise, pink noise, and nature-inspired audio profiles. Semiconductor manufacturers have responded by developing purpose-built IC solutions with enhanced digital signal processing capabilities, ultra-low power consumption, and reduced form factors compatible with in-ear and behind-the-ear device architectures. These hardware improvements directly support wider clinical deployment of tinnitus masking solutions.

➤ The integration of AI-driven adaptive sound generation algorithms into tinnitus masking ICs represents a pivotal shift in the market, enabling devices to dynamically adjust masking frequencies to individual audiological profiles , significantly improving therapeutic efficacy and patient compliance.

Healthcare system investments in audiology infrastructure across developed and emerging economies are further reinforcing market growth. Increased reimbursement coverage for tinnitus management devices in several countries, combined with expanding networks of audiological clinics and ENT specialists, ensures a steady pipeline of end-user demand. Tinnitus Masking (Sound Generator) IC Market benefits from this institutional support as device manufacturers scale production and pursue regulatory clearances for next-generation masking platforms built on advanced IC architectures.

MARKET CHALLENGES

Complex Regulatory Pathways and Clinical Validation Requirements Constraining Market Entry

One of the principal challenges confronting participants in Tinnitus Masking (Sound Generator) IC Market is navigating complex and regionally inconsistent regulatory frameworks governing medical-grade audio devices. In many jurisdictions, tinnitus masking devices incorporating sound generator ICs must meet stringent medical device standards, requiring extensive clinical validation, electromagnetic compatibility testing, and biocompatibility assessments. These requirements impose significant cost and time burdens on both IC developers and device manufacturers, particularly smaller companies and startups seeking to commercialize innovative masking solutions. The absence of globally harmonized standards for tinnitus therapy devices creates additional compliance complexity for companies targeting multi-regional market entry.

Other Challenges

Limited Clinical Consensus on Masking Efficacy

Despite widespread clinical use, the broader audiology and otolaryngology communities have not reached full consensus on the long-term therapeutic efficacy of sound masking as a standalone tinnitus management strategy. This ambiguity can affect prescribing behavior among clinicians and limit the pace at which tinnitus masking devices , and the sound generator ICs within them , achieve mainstream clinical adoption. Device makers must invest in robust clinical evidence generation to sustain product credibility and encourage wider professional endorsement.

Supply Chain Vulnerabilities and Semiconductor Procurement Risks

The tinnitus sound generator IC segment, like the broader semiconductor industry, remains exposed to periodic supply chain disruptions. Fluctuations in the availability of specialized components, fabrication capacity constraints at advanced process nodes, and geopolitical factors affecting semiconductor trade flows can all introduce procurement uncertainties. These supply-side risks may impair manufacturers’ ability to fulfill device production schedules, potentially undermining revenue predictability and customer confidence in the tinnitus masking device ecosystem.

MARKET RESTRAINTS

High Development Costs and Price Sensitivity Limiting Broad Market Penetration

The development of application-specific integrated circuits for tinnitus masking applications entails substantial engineering investment, including the costs associated with custom DSP algorithm design, ASIC tape-out, and iterative validation cycles. These elevated development expenditures translate into higher per-unit IC costs, which ultimately affect the retail pricing of end-user tinnitus masking devices. In price-sensitive markets, particularly across developing economies in Asia-Pacific, Latin America, and Africa, the resulting device cost structures can impede consumer access and slow market penetration. Many potential patients in these regions remain dependent on lower-cost general-purpose audio solutions that lack the clinical precision of dedicated tinnitus masking sound generator ICs.

Fragmented Reimbursement Landscape Undermining Device Affordability

Insurance and public healthcare reimbursement policies for tinnitus management devices vary considerably across markets, creating an uneven commercial environment for Tinnitus Masking (Sound Generator) IC Market. In several major markets, tinnitus masking devices are classified as wellness or consumer audio products rather than reimbursable medical devices, placing the full cost burden on end users. This classification challenge restrains the willingness of healthcare providers to recommend dedicated masking solutions and limits patient uptake. Until reimbursement frameworks evolve to more consistently recognize the clinical value of evidence-based sound therapy delivered through purpose-built IC platforms, the market’s growth potential will remain partially constrained by affordability barriers.

MARKET OPPORTUNITIES

Expansion of Consumer-Grade Tinnitus Masking Wearables Opening New IC Application Segments

The rapid growth of the consumer hearables and wellness wearables market presents a compelling opportunity for tinnitus masking sound generator IC developers to address an expanded addressable market beyond traditional clinical hearing aid platforms. Mainstream audio brands and digital health startups are increasingly incorporating tinnitus relief modes into wireless earbuds, sleep headbands, and smart hearing devices targeting the broader wellness consumer segment. This trend creates demand for highly integrated, cost-optimized sound generator ICs capable of delivering clinically meaningful masking performance within consumer-grade power and cost envelopes, representing a significant new revenue stream for semiconductor designers active in this space.

Telehealth and Remote Audiological Care Models Accelerating Digital Tinnitus Therapy Adoption

The accelerating global adoption of telehealth platforms and remote patient monitoring solutions creates a favorable environment for digitally connected tinnitus masking devices incorporating advanced sound generator ICs. Remote audiology programs enable patients to receive personalized tinnitus sound therapy prescriptions and real-time device adjustments through connected platforms, enhancing clinical outcomes while expanding geographic reach beyond traditional clinic-centric care models. IC developers that engineer Bluetooth-enabled, app-configurable sound generator solutions compatible with telehealth workflows are well-positioned to capture disproportionate share of this emerging opportunity within the broader Tinnitus Masking (Sound Generator) IC Market.

Emerging Markets Presenting Untapped Growth Potential Driven by Rising Audiological Awareness

Rapidly developing healthcare infrastructure across emerging economies in Southeast Asia, the Middle East, and Latin America, combined with increasing public and professional awareness of tinnitus as a treatable audiological condition, presents a long-term structural growth opportunity for Tinnitus Masking (Sound Generator) IC Market. As local audiological device manufacturing capabilities mature in countries such as India, China, and Brazil, regional demand for cost-competitive sound generator ICs suited to locally produced tinnitus masking devices is expected to grow meaningfully. Strategic partnerships between global IC manufacturers and regional device makers could prove instrumental in unlocking these high-potential geographies and diversifying market growth beyond established North American and European demand centers.

Tinnitus Masking (Sound Generator) IC Market Trends

Rising Global Prevalence of Tinnitus Driving Demand for Masking IC Solutions

Tinnitus Masking (Sound Generator) IC Market is experiencing notable momentum as Global burden of tinnitus continues to expand. Tinnitus affects approximately 15% of the world’s population , an estimated 750 million individuals , according to World Health Organization data. This widespread prevalence is compelling device manufacturers and semiconductor developers to accelerate investment in specialized integrated circuits engineered for therapeutic sound generation. As awareness of sound therapy grows among both clinicians and patients, demand for tinnitus masking ICs embedded within hearing aids, wearable sound generators, and dedicated relief devices is strengthening considerably across developed and emerging markets alike.

Other Trends

Aging Population Accelerating Audiological Device Adoption

A prominent trend shaping Tinnitus Masking (Sound Generator) IC Market is the correlation between tinnitus incidence and age-related hearing loss. As Global population ages, healthcare systems are observing a parallel rise in patients reporting persistent ringing, buzzing, or hissing ear conditions. This demographic shift is prompting audiological device manufacturers to integrate tinnitus masking IC functionality directly into hearing aids and assistive listening devices, effectively expanding the addressable market for these semiconductor components beyond standalone sound therapy instruments.

Miniaturization and Low-Power IC Design Innovation

Advancements in low-power integrated circuit design and semiconductor miniaturization are reshaping how tinnitus masking solutions are engineered and delivered. Manufacturers are increasingly developing compact, energy-efficient ICs capable of producing white noise, pink noise, notched sound therapy, and customizable broadband audio outputs within form factors compatible with next-generation hearing aids and consumer-grade wearables. This convergence of audiological functionality with miniaturized semiconductor architecture is enabling a new class of discreet, patient-friendly masking devices that support prolonged daily use without compromising battery life or acoustic performance.

Diversified Product Portfolios Among Leading Market Participants

Key players in Tinnitus Masking (Sound Generator) IC Market, including Sonova Holding AG, Starkey Hearing Technologies, and GN Audio A/S, are maintaining diversified product portfolios that embed tinnitus masking IC capabilities within broader audiological device ecosystems. This strategic integration approach reflects a broader industry trend toward multifunctional hearing solutions that address both hearing amplification and tinnitus relief within a single platform. Both analog and digital signal generation architectures continue to advance, offering clinicians and end users greater flexibility in customizing therapeutic sound profiles to individual patient needs , a trend that is expected to remain central to product development strategies across Tinnitus Masking (Sound Generator) IC Market going forward.

COMPETITIVE LANDSCAPE

Key Industry Players

Tinnitus Masking (Sound Generator) IC Market , Competitive Dynamics and Leading Manufacturers

Global Tinnitus Masking (Sound Generator) IC market is characterized by a moderately consolidated competitive landscape, with a handful of dominant players commanding significant market share through diversified audiological device portfolios and vertically integrated semiconductor capabilities. Sonova Holding AG, Starkey Hearing Technologies, and GN Audio A/S represent the leading tier of market participants, each embedding proprietary tinnitus masking IC technologies within their broader hearing aid and sound therapy device ecosystems. These companies leverage substantial R&D investments to advance low-power digital signal processing (DSP) architectures, enabling compact, energy-efficient masking solutions that generate white noise, pink noise, notched sound therapy, and customizable broadband audio outputs suited for next-generation wearable devices. Their established global distribution networks and clinical validation pipelines further reinforce competitive barriers against emerging entrants.

Beyond the market leaders, a number of niche and specialized players contribute meaningfully to the competitive dynamics of the Tinnitus Masking IC space. Companies such as Widex A/S (now part of WS Audiology following its merger with Sivantos), Demant A/S, and Cochlear Limited maintain strong positions through targeted innovation in sound therapy algorithms and IC miniaturization. Semiconductor-focused firms including Texas Instruments, Analog Devices, and NXP Semiconductors supply foundational analog and mixed-signal IC components that underpin many tinnitus masking device platforms, while pure-play hearing technology innovators such as Audina Hearing Instruments and Intrasonics continue to develop differentiated masking signal generation solutions. Collectively, these players are responding to accelerating market demand driven by rising global tinnitus prevalence , affecting approximately 750 million individuals worldwide , and the expanding aging population base, which correlates strongly with age-related hearing loss and tinnitus incidence.

List of Key Tinnitus Masking (Sound Generator) IC Companies Profiled

- Sonova Holding AG

- Starkey Hearing Technologies

- GN Audio A/S

- WS Audiology (Widex / Sivantos)

- Demant A/S

- Cochlear Limited

- Texas Instruments Incorporated

- Analog Devices, Inc.

- NXP Semiconductors N.V.

- Intrasonics LLC

- Audina Hearing Instruments

- Microchip Technology Inc.

- ON Semiconductor (onsemi)

- Cirrus Logic, Inc.

- Unitron Hearing Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Digital Signal Generator ICs represent the leading segment within the Tinnitus Masking IC market, driven by their superior programmability and versatility in delivering a wide range of therapeutic audio outputs.

|

| By Application |

|

Hearing Aids with Tinnitus Masking constitute the dominant application segment, as the convergence of hearing amplification and tinnitus relief within a single device offers a compelling value proposition for both clinicians and patients.

|

| By End User |

|

Hearing Aid Manufacturers (OEM) represent the leading end-user segment, as they are the primary integrators of tinnitus masking ICs into commercially deployed audiological products.

|

| By Sound Output |

|

Notched Sound Therapy is emerging as the most clinically differentiated and rapidly evolving sound output segment within the tinnitus masking IC market, reflecting a broader shift toward evidence-based, personalized therapeutic approaches.

|

| By Power Architecture |

|

Ultra-Low Power ICs dominate the power architecture segment, as the pervasive adoption of wearable and miniaturized tinnitus therapy devices places stringent energy efficiency requirements at the forefront of IC design priorities.

|

Regional Analysis: Tinnitus Masking (Sound Generator) IC Market

North America

North America’s tinnitus masking IC landscape is underpinned by a thriving research and development ecosystem. Prominent semiconductor companies and medical device startups consistently channel resources into the design of low-power, high-fidelity sound generator integrated circuits. Strategic partnerships between audiology clinics and chip designers are accelerating product refinement, ensuring that clinical efficacy remains central to technological advancement in this specialized market segment.

Favorable regulatory pathways established by the U.S. Food and Drug Administration provide a structured route for tinnitus masking sound generator IC-based devices to reach the market efficiently. Growing recognition of tinnitus as a significant public health concern has prompted increased reimbursement consideration by both private insurers and Medicare programs, creating a commercially supportive environment for integrated circuit developers and hearing device manufacturers alike.

Heightened consumer awareness campaigns led by audiological associations and hearing health advocacy groups have meaningfully expanded the patient population actively seeking tinnitus masking solutions across North America. Clinicians are increasingly recommending sound generator IC-embedded devices as a frontline therapeutic option, and the integration of these technologies into telehealth platforms is broadening accessibility well beyond traditional audiology clinic settings.

North America’s well-established semiconductor manufacturing base and diversified supply chain infrastructure provide a resilient foundation for tinnitus masking sound generator IC production. Domestic fabrication capabilities, supplemented by strategic sourcing partnerships, enable manufacturers to maintain consistent quality standards and respond aggressively to fluctuating clinical demand, thereby sustaining the region’s competitive edge in global hearing health IC markets.

Europe

Europe represents a highly significant and rapidly maturing region within Global Tinnitus Masking (Sound Generator) IC Market, characterized by strong audiological healthcare systems and well-established medical device manufacturing sectors particularly in Germany, Switzerland, and the Netherlands. European Union regulatory harmonization through the Medical Device Regulation framework has created a cohesive commercial environment that supports the introduction of innovative sound generator IC technologies across member states. The region’s aging demographic profile, combined with increasing awareness of occupational noise exposure as a primary tinnitus trigger, continues to expand the addressable patient population. Leading European hearing aid manufacturers are actively embedding advanced tinnitus masking sound generator integrated circuits into next-generation devices, reflecting a strategic commitment to addressing audiological comorbidities. Growing collaboration between European academic research institutions and semiconductor firms is further strengthening the regional innovation pipeline in this specialized IC market segment through the forecast horizon.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region in Tinnitus Masking (Sound Generator) IC Market, propelled by rapidly expanding healthcare infrastructure, rising disposable incomes, and growing clinical recognition of tinnitus as a treatable condition across countries such as China, Japan, South Korea, and India. Japan’s sophisticated electronics manufacturing ecosystem positions it as a key hub for tinnitus masking IC development, while South Korea’s semiconductor prowess enables cost-competitive production of advanced sound generator chipsets. China’s enormous patient population and increasing penetration of private audiological healthcare services are creating substantial demand opportunities. Governments across the region are progressively investing in hearing health awareness programs, which is expected to accelerate early diagnosis and treatment adoption, thereby directly stimulating demand for tinnitus masking sound generator integrated circuits embedded within consumer and clinical-grade hearing devices over the coming years.

South America

South America occupies a developing but progressively important position in Global Tinnitus Masking (Sound Generator) IC Market. Brazil leads regional market activity, supported by its sizeable healthcare expenditure and growing network of audiology clinics that are beginning to adopt sound generator IC-based therapeutic devices. Argentina and Colombia also demonstrate emerging interest in advanced hearing health technologies as middle-class populations gain greater access to specialized audiological care. While economic volatility and import dependency for semiconductor components present notable headwinds, regional governments are increasingly prioritizing healthcare modernization, which is anticipated to improve the commercial viability of tinnitus masking solutions. The gradual expansion of health insurance coverage and heightened public awareness regarding hearing disorders are expected to progressively strengthen demand fundamentals across the South American tinnitus masking IC landscape through 2034.

Middle East & Africa

The Middle East and Africa region currently represents the nascent stage of development within Tinnitus Masking (Sound Generator) IC Market, yet notable growth foundations are being established. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are actively investing in world-class healthcare infrastructure and are importing technologically advanced audiological devices that incorporate sound generator integrated circuits. Africa’s large and youthful population, paradoxically affected by tinnitus due to high noise exposure in urban and industrial environments, represents an underserved yet long-term growth opportunity for market participants. The gradual strengthening of regional regulatory frameworks for medical devices, coupled with increasing foreign direct investment in healthcare sectors across key African economies, is expected to progressively open commercial pathways for tinnitus masking sound generator IC products as the forecast period advances toward 2034.

Report Scope

This market research report provides a comprehensive analysis of the Tinnitus Masking (Sound Generator) IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Tinnitus Masking (Sound Generator) IC Market?

-> Tinnitus Masking (Sound Generator) IC Market was valued at USD 280.4 million in 2025 and is expected to reach USD 512.3 million by 2034, growing at a CAGR of 6.2% during the forecast period from 2026 to 2034.

Which key companies operate in Tinnitus Masking (Sound Generator) IC Market?

-> Key players include Sonova Holding AG, Starkey Hearing Technologies, and GN Audio A/S, among others, each maintaining diversified product portfolios that integrate tinnitus masking IC capabilities within broader audiological device ecosystems.

What are the key growth drivers?

-> Key growth drivers include the rising global prevalence of tinnitus, which affects approximately 15% of the world’s population (roughly 750 million individuals), the aging global population with age-related hearing loss, and advancements in low-power IC design and miniaturization technologies enabling compact and energy-efficient masking solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by increasing awareness of tinnitus treatment and expanding healthcare infrastructure, while North America remains a dominant market due to high adoption of advanced audiological devices.

What are the emerging trends?

-> Emerging trends include wearable sound generators, hearing aids with integrated masking functionality, notched sound therapy, and customizable broadband audio outputs, along with the development of next-generation analog and digital signal generation architectures producing white noise and pink noise therapies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...