Smart Contact Lens (Glucose) Sensor ASIC Market Insights

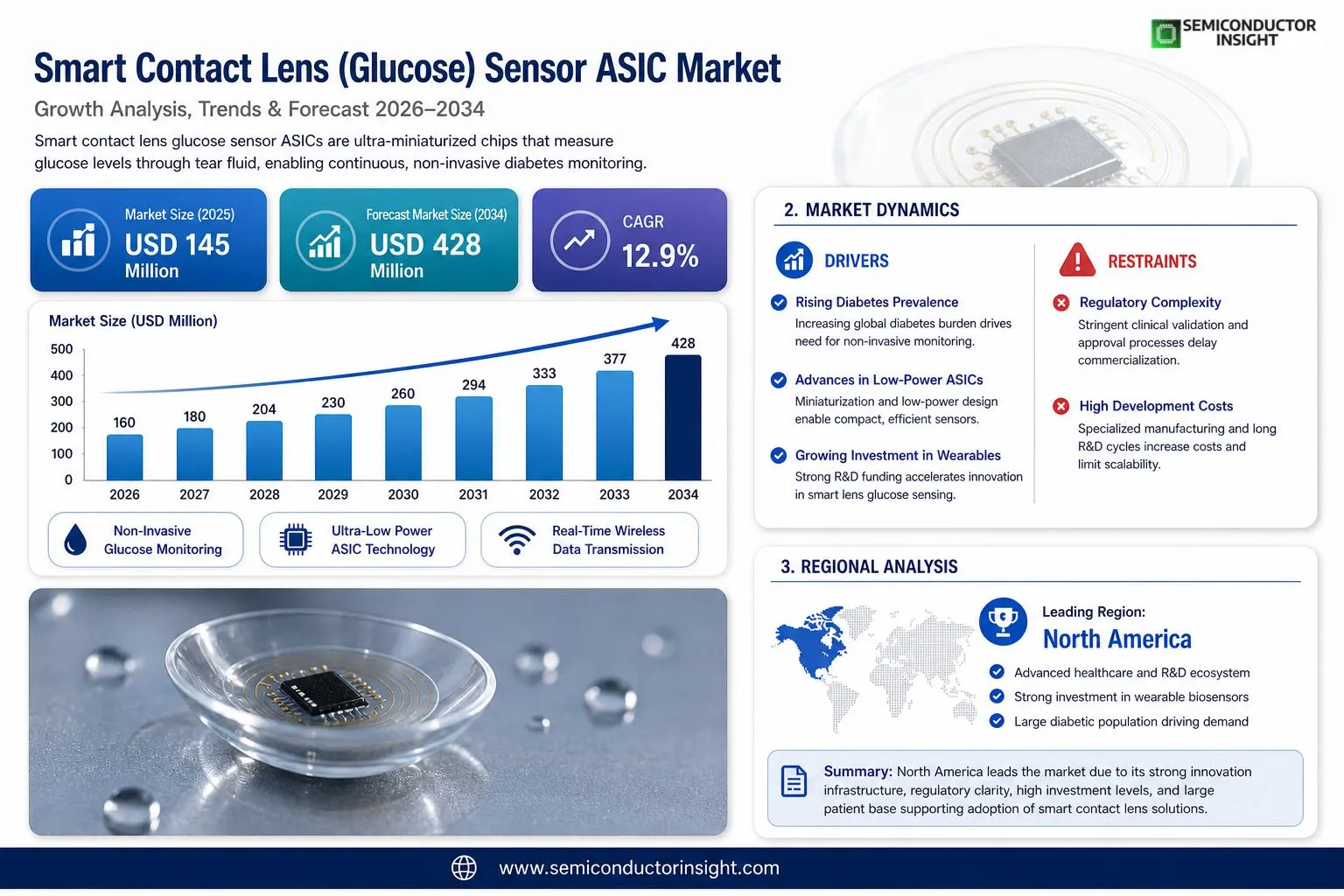

Global Smart Contact Lens (Glucose) Sensor ASIC Market size is estimated to be valued at USD 145 million in 2025. The market is projected to grow to USD 428 million by 2034, exhibiting a CAGR of 12.9% during the forecast period.

Smart contact lens glucose sensor ASICs are ultra‑miniaturized application-specific integrated circuits designed to measure glucose levels through tear fluid. These ASICs enable continuous, non-invasive glucose monitoring by integrating biochemical sensing modules, low-power wireless communication, and micro-scale signal processing. The technology combines advanced semiconductor engineering, biosensing materials, and medical-grade microelectronics to deliver real-time data for diabetes management. Because they must fit within the thin profile of a soft contact lens, these chips are engineered for extremely low energy consumption, high sensitivity, and reliable calibration stability.

The market is gaining traction due to increasing global diabetes prevalence, rising demand for non-invasive monitoring solutions, and ongoing investment in wearable medical electronics. Furthermore, advancements in semiconductor miniaturization and flexible electronics are accelerating product development. Recent progress by leading players in smart wearable biosensors is reshaping competitive dynamics. For instance, in 2023 and 2024, multiple R&D programs across the U.S., South Korea, and Japan reported significant improvements in tear‑based glucose sensing accuracy and ASIC power efficiency, signaling strong innovation momentum. While commercialization timelines remain cautious due to regulatory complexity, sustained investment by medical device manufacturers and semiconductor companies is expected to strengthen market expansion.

MARKET DRIVERS

Rising Global Diabetes Prevalence Fueling Demand for Continuous Glucose Monitoring Solutions

The escalating global burden of diabetes mellitus remains one of the most significant forces propelling Smart Contact Lens (Glucose) Sensor ASIC Market forward. With hundreds of millions of individuals worldwide living with Type 1 and Type 2 diabetes, the clinical need for non-invasive, real-time glucose monitoring has never been more pressing. Traditional fingerstick methods and subcutaneous continuous glucose monitors (CGMs) present compliance and comfort challenges, creating a clear market opening for smart contact lens-based glucose sensing technologies. Application-Specific Integrated Circuits (ASICs) embedded within these lenses are engineered to process electrochemical signals from tear fluid glucose with high precision and ultra-low power consumption, making them a cornerstone component of next-generation wearable diagnostics.

Advances in Low-Power ASIC Design and Microelectronics Enabling Miniaturized Ocular Biosensors

Breakthroughs in semiconductor miniaturization and low-power circuit architecture are strongly accelerating the development pipeline within Smart Contact Lens (Glucose) Sensor ASIC Market. Modern ASIC designs tailored for ocular biosensor applications must operate within extremely tight power envelopes , often harvesting energy wirelessly via near-field communication (NFC) , while maintaining signal fidelity across varying glucose concentration ranges. The convergence of sub-micron CMOS fabrication processes, flexible substrate integration, and biocompatible encapsulation techniques is enabling chipmakers and research institutions to bring increasingly viable prototypes closer to commercialization. These technical advances reduce form-factor constraints, making the embedded ASIC both mechanically compatible with soft contact lens materials and physiologically safe for continuous ocular wear.

➤ The integration of glucose-sensing ASICs within smart contact lenses represents a paradigm shift in non-invasive metabolic monitoring, converging semiconductor innovation with wearable bioelectronics to address one of healthcare’s most persistent unmet needs.

Increasing strategic investment from both established semiconductor companies and well-funded medtech startups is providing further momentum to the Smart Contact Lens Glucose Sensor ASIC landscape. Research collaborations between academic institutions, ophthalmology-focused device developers, and chip design houses are shortening development cycles. Regulatory interest in novel non-invasive glucose monitoring pathways is also creating a more defined approval trajectory, lending commercial confidence to ASIC suppliers and system integrators operating in this space.

MARKET CHALLENGES

Establishing Reliable Correlation Between Tear Fluid Glucose and Blood Glucose Levels

One of the foremost technical challenges confronting Smart Contact Lens (Glucose) Sensor ASIC Market is the physiological complexity of using lacrimal (tear) glucose as a reliable proxy for blood glucose concentrations. Scientific literature indicates that while a correlation between the two exists, it is subject to time lags, inter-individual variability, and sensitivity to ocular surface conditions such as evaporation rate, blinking frequency, and inflammation. The ASIC must therefore be designed not only to detect glucose electrochemically with high sensitivity at the low micromolar concentrations present in tear fluid but also to compensate for these confounding biological variables through onboard signal processing algorithms , a formidable combined hardware and software engineering challenge.

Other Challenges

Biocompatibility and Long-Term Ocular Safety

Ensuring that the ASIC, its interconnects, antenna structures, and encapsulants remain fully biocompatible during extended ocular contact is a non-trivial regulatory and materials science challenge. Any leaching of chemical compounds or thermal dissipation from the chip onto the corneal surface could compromise patient safety, necessitating extensive pre-clinical and clinical validation before regulatory clearance. This substantially increases the time and capital required to bring Smart Contact Lens Glucose Sensor ASIC-integrated products to market.

Wireless Power Delivery and Data Transmission Constraints

Passive NFC-based power delivery, the most commonly proposed energy mechanism for smart contact lens ASICs, imposes strict constraints on data throughput, reading distance, and operational continuity. Designing an ASIC that can reliably perform analog signal acquisition, analog-to-digital conversion, and wireless data transmission within the microwatt power budgets achievable through inductive coupling requires highly optimized circuit topologies. Interference from ambient electromagnetic sources and alignment sensitivity between the lens antenna and the external reader represent additional engineering hurdles that ASIC designers must address systematically.

MARKET RESTRAINTS

Complex Regulatory Pathways and Extended Clinical Validation Requirements

Smart Contact Lens (Glucose) Sensor ASIC Market faces substantial restraint from the lengthy and complex regulatory frameworks governing combination medical devices that integrate semiconductor components with contact lens materials intended for continuous ocular use. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) classify such devices under stringent categories that require extensive biocompatibility testing per ISO 10993 standards, analytical performance validation, and multi-phase clinical trials demonstrating both safety and accuracy equivalence to established glucose monitoring benchmarks. These processes typically span multiple years and require significant capital allocation, creating high barriers to entry that restrain the pace of commercialization within the market.

High Development Costs and Limited Established Manufacturing Infrastructure for Flexible Ocular ASICs

The specialized nature of ASICs designed for integration into hydrogel or silicone hydrogel contact lens matrices imposes exceptionally high non-recurring engineering (NRE) costs and demands fabrication capabilities that are not widely available within standard semiconductor foundry ecosystems. Unlike conventional rigid PCB-mounted ASICs, ocular biosensor chips must be thinned to micrometer-scale profiles, mounted on flexible substrates, and encapsulated using processes that preserve both electrical performance and mechanical pliability. The limited number of foundries equipped to handle this combination of requirements restricts supply chain scalability and sustains elevated unit costs, which in turn constrains the commercial viability and broad market adoption of Smart Contact Lens Glucose Sensor ASIC-based products in the near-to-medium term.

MARKET OPPORTUNITIES

Convergence of Digital Health Ecosystems and IoMT Creating High-Value Integration Opportunities

The rapid expansion of the Internet of Medical Things (IoMT) and digitally connected health management platforms presents a compelling growth opportunity for Smart Contact Lens (Glucose) Sensor ASIC Market. As healthcare systems globally transition toward remote patient monitoring, predictive analytics, and personalized chronic disease management, a continuously transmitting ocular glucose sensor ASIC becomes a high-value node within a broader digital health architecture. ASIC developers that architect their chips with standardized wireless communication interfaces and secure data output protocols are well-positioned to partner with diabetes management software platforms, electronic health record (EHR) integrators, and telehealth providers , significantly expanding their addressable market beyond the hardware component itself.

Emerging Market Expansion and Untapped Demand in High-Diabetes-Burden Regions

Regions including South and Southeast Asia, the Middle East, and Latin America carry among the highest and fastest-growing diabetes prevalence rates globally, yet remain significantly underserved by advanced continuous glucose monitoring technologies due to cost and accessibility barriers. As ASIC fabrication economies of scale improve and smart contact lens manufacturing processes mature, price points are expected to decline, making non-invasive ocular glucose monitoring more accessible to these large patient populations. Companies investing now in localized clinical validation, distribution partnerships, and regulatory engagement within these high-burden regions can establish durable first-mover advantages as the Smart Contact Lens Glucose Sensor ASIC Market transitions from early adoption to broader commercial deployment over the coming decade.

Multi-Analyte Sensing Expansion Beyond Glucose Broadening ASIC Platform Value

While glucose monitoring represents the primary commercial driver, the underlying ASIC platform architecture being developed for smart contact lens applications holds strong potential for extension to the simultaneous detection of additional clinically relevant analytes including lactate, cortisol, uric acid, and intraocular pressure. ASIC designers who develop modular, multi-channel analog front-end architectures capable of accommodating diverse biosensor modalities will be positioned to serve a considerably broader diagnostic device market. This platform versatility enhances the return on substantial R&D investment, provides a differentiated value proposition to ophthalmic and systemic disease management stakeholders, and strengthens the long-term commercial outlook for participants active across the Smart Contact Lens Glucose Sensor ASIC ecosystem.

Smart Contact Lens (Glucose) Sensor ASIC Market Trends

Rising Diabetes Prevalence Driving Demand for Non-Invasive Glucose Monitoring Solutions

Smart Contact Lens (Glucose) Sensor ASIC Market is experiencing notable momentum, driven primarily by the escalating global burden of diabetes. As millions of individuals worldwide require continuous glucose monitoring, the limitations of conventional invasive methods have created a compelling need for alternative approaches. Smart contact lens glucose sensor ASICs, which measure glucose levels through tear fluid analysis, have emerged as a highly promising non-invasive solution. These ultra-miniaturized application-specific integrated circuits integrate biochemical sensing modules, low-power wireless communication, and micro-scale signal processing within the thin profile of a soft contact lens, enabling real-time, continuous glucose tracking without the discomfort of traditional finger-prick or subcutaneous methods. This fundamental value proposition is a core trend shaping Smart Contact Lens (Glucose) Sensor ASIC Market today.

Other Trends

Semiconductor Miniaturization and Flexible Electronics Accelerating Innovation

Advancements in semiconductor miniaturization and flexible electronics are playing a transformative role in Smart Contact Lens (Glucose) Sensor ASIC Market. Engineers are developing ASICs with increasingly lower energy consumption profiles and higher sensitivity thresholds, both of which are essential requirements for a chip embedded within a soft contact lens. Progress in medical-grade microelectronics and biosensing materials continues to improve calibration stability and signal accuracy. Notably, R&D programs across the United States, South Korea, and Japan reported meaningful improvements in tear-based glucose sensing accuracy and ASIC power efficiency during 2023 and 2024, signaling robust innovation activity across key technology hubs.

Growing Investment by Medical Device and Semiconductor Companies

Sustained capital investment from both medical device manufacturers and semiconductor companies is a defining trend in Smart Contact Lens (Glucose) Sensor ASIC Market. Leading players in smart wearable biosensors are actively reshaping competitive dynamics by committing resources to long-term research programs. This cross-industry convergence between semiconductor engineering and medical device development is accelerating the transition from laboratory prototypes to clinically viable products. Investment inflows are also supporting improvements in manufacturing scalability, which will be critical as commercialization progresses.

Regulatory Complexity Tempering Near-Term Commercialization Timelines

Despite strong innovation momentum, regulatory complexity remains a significant trend influencing the pace of commercialization in Smart Contact Lens (Glucose) Sensor ASIC Market. Medical-grade contact lens devices with integrated sensing and wireless communication capabilities must satisfy rigorous safety, efficacy, and biocompatibility standards across major regulatory jurisdictions. This has led market participants to adopt measured timelines for product launches. However, as regulatory frameworks for smart wearable medical electronics continue to mature, industry observers anticipate a gradual easing of approval pathways, which is expected to support broader market expansion in the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart Contact Lens (Glucose) Sensor ASIC Market: Competitive Dynamics and Leading Innovators

The global Smart Contact Lens (Glucose) Sensor ASIC market is characterized by a highly specialized and innovation-driven competitive landscape, where a select group of semiconductor companies, medical device giants, and advanced research-backed startups are vying for technological leadership. Among the most prominent entities shaping this space, companies such as Novartis (in collaboration with Alcon) and Google’s Verily Life Sciences have historically been at the forefront of smart contact lens research, having invested significantly in tear-based glucose sensing platforms. The market, valued at approximately USD 145 million in 2025 and projected to reach USD 428 million by 2034 at a CAGR of 12.9%, is attracting both established semiconductor manufacturers and emerging bioelectronics firms. Key competitive differentiators include ASIC power efficiency, chip miniaturization capability, biosensing accuracy in tear fluid environments, and regulatory compliance expertise. Major players with foundational semiconductor capabilities,such as Texas Instruments and STMicroelectronics,are well-positioned to supply low-power ASIC architectures suited for wearable biosensor applications, giving them a competitive edge in component supply chains.

Beyond the dominant players, several niche and regionally significant companies are making notable strides in the smart contact lens glucose sensor ASIC segment. South Korean conglomerate Samsung Electronics and Japanese firm Sony Semiconductor Solutions are leveraging their advanced CMOS and micro-fabrication capabilities to develop ultra-miniaturized sensing modules compatible with flexible lens substrates. Startup ecosystems in the United States and Europe,including companies like Mojo Vision and Imec (the Belgian nanoelectronics research center),are accelerating ASIC innovation through interdisciplinary R&D combining biosensor chemistry, wireless power transfer, and ultra-low-power IC design. Meanwhile, Medtronic and Abbott Laboratories, both leaders in continuous glucose monitoring (CGM), are increasingly exploring non-invasive tear-based sensing as a complementary technology. The competitive intensity is further amplified by university spin-offs and government-funded research programs in the U.S., South Korea, and Japan, all of which reported measurable advances in tear glucose sensing accuracy and ASIC efficiency in 2023 and 2024, contributing to a rapidly evolving and increasingly crowded innovation pipeline.

List of Key Smart Contact Lens (Glucose) Sensor ASIC Companies Profiled

- Verily Life Sciences (Google/Alphabet)

- Novartis AG (in collaboration with Alcon)

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Samsung Electronics Co., Ltd.

- Sony Semiconductor Solutions Corporation

- Mojo Vision, Inc.

- Imec (Interuniversity Microelectronics Centre)

- Medtronic plc

- Abbott Laboratories

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Tohoku University (Research Consortium, Japan)

- Korea Advanced Institute of Science and Technology (KAIST)

- Sensirion AG

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Wireless-Enabled Glucose Sensor ASIC is the leading segment in this category, driven by the growing need for continuous, real-time glucose data transmission without physical connectors.

|

| By Application |

|

Continuous Glucose Monitoring (CGM) stands as the dominant application segment, reflecting the fundamental clinical purpose for which smart contact lens glucose sensor ASICs are engineered.

|

| By End User |

|

Diabetic Patients (Type 1 and Type 2) represent the primary and most strategically significant end-user segment for smart contact lens glucose sensor ASICs, as the technology is fundamentally designed to serve the daily glucose management needs of this population.

|

| By Power Source |

|

RF/NFC Energy Harvesting is the leading power source segment for smart contact lens glucose sensor ASICs, emerging as the most technically mature and practically viable solution to the extreme space and energy constraints inherent to the contact lens form factor.

|

| By Distribution Channel |

|

Direct Sales to Medical Device Manufacturers (OEM) constitutes the dominant distribution channel for smart contact lens glucose sensor ASICs, reflecting the highly specialized and deeply integrated nature of this component within finished medical device products.

|

Regional Analysis: Smart Contact Lens (Glucose) Sensor ASIC Market

North America

North America’s dominance in Smart Contact Lens (Glucose) Sensor ASIC Market is deeply anchored in its unmatched research and development infrastructure. Leading universities, national laboratories, and private sector giants continuously push the boundaries of ASIC miniaturization and biocompatibility. Cross-disciplinary collaboration between electrical engineers, biomedical scientists, and clinicians creates fertile ground for next-generation glucose biosensing architectures in ocular wearables.

The United States offers one of the most mature regulatory environments for advanced medical-grade wearables. FDA’s established frameworks for combination products , merging ophthalmic devices with biosensors , give developers a navigable path to market approval. This regulatory clarity significantly de-risks ASIC investment, encouraging both established semiconductor firms and emerging startups to commit resources to glucose-sensing contact lens technology development.

North America’s venture capital and strategic corporate investment culture plays a pivotal role in advancing Smart Contact Lens (Glucose) Sensor ASIC Market. Partnerships between semiconductor design firms and medical device companies are actively structured to fast-track ASIC prototyping and clinical validation. Strong investor appetite for diabetes management technologies ensures consistent funding flows toward ocular biosensor platforms from concept through commercialization.

The North American diabetic population represents a substantial and growing addressable market for non-invasive continuous glucose monitoring solutions. High awareness of diabetes management, combined with widespread health insurance coverage and patient willingness to adopt wearable technology, creates powerful demand-side momentum. This patient-driven urgency compels healthcare providers and device manufacturers to prioritize commercialization of glucose-sensing smart contact lens ASIC platforms.

Europe

Europe represents a highly significant region in Smart Contact Lens (Glucose) Sensor ASIC Market, characterized by a strong tradition of precision engineering, microelectronics excellence, and patient-centric healthcare systems. Countries such as Germany, Switzerland, the Netherlands, and the United Kingdom host world-class semiconductor research institutes and ophthalmic device manufacturers that are actively engaging with glucose biosensing wearable technologies. The European Medicines Agency’s evolving frameworks for digital health and combination medical devices are creating greater regulatory predictability, supporting long-term ASIC investment decisions. European healthcare systems, with their emphasis on preventive care and chronic disease management, represent receptive environments for non-invasive continuous glucose monitoring innovations. Moreover, strong public funding through programs such as Horizon Europe is channeling resources into biosensor miniaturization and biocompatible ASIC research, ensuring that European players remain competitive in shaping global Smart Contact Lens (Glucose) Sensor ASIC Market standards and technology roadmaps through 2034.

Asia-Pacific

Asia-Pacific is rapidly emerging as a transformative force in Smart Contact Lens (Glucose) Sensor ASIC Market, propelled by the region’s enormous and expanding diabetic population, aggressive semiconductor manufacturing investments, and government-led digital health initiatives. Nations including Japan, South Korea, China, and Taiwan possess deep ASIC fabrication expertise and are actively directing these capabilities toward medical biosensor applications. Japan’s precision optics and microelectronics heritage positions it as a natural innovator in ocular wearable biosensing. South Korea’s leading semiconductor conglomerates are exploring ultra-low-power chip architectures suited for continuous glucose monitoring contact lenses. China’s rapidly maturing domestic medical device industry, backed by substantial state investment, is accelerating indigenous ASIC development for glucose-sensing platforms. The region’s cost-competitive manufacturing environment also makes Asia-Pacific a critical hub for scaling production of smart contact lens sensor components as the global market matures toward broader commercial deployment.

South America

South America occupies an emerging but increasingly relevant position within Smart Contact Lens (Glucose) Sensor ASIC Market. Brazil and Argentina, as the region’s largest economies, are witnessing growing awareness of advanced diabetes management technologies among both healthcare professionals and patients. Rising rates of diabetes across the continent are creating latent demand for innovative non-invasive glucose monitoring solutions, including smart contact lens platforms. While the region currently depends heavily on imported semiconductor components and medical devices, nascent efforts to develop local biosensor research capabilities are evident in academic and government-supported programs. Regulatory modernization efforts, particularly in Brazil through ANVISA’s evolving medical device frameworks, are gradually improving the environment for introducing advanced wearable biosensing technologies. As global manufacturers seek to expand their market reach, South America is expected to gain strategic attention as a distribution and early adoption market for Smart Contact Lens (Glucose) Sensor ASIC solutions during the forecast period.

Middle East & Africa

The Middle East and Africa region presents a distinctive long-term growth narrative for Smart Contact Lens (Glucose) Sensor ASIC Market, shaped by the region’s alarmingly high and rapidly rising prevalence of diabetes , particularly in Gulf Cooperation Council countries. Nations such as Saudi Arabia, the UAE, and Kuwait are investing substantially in healthcare modernization, digital health infrastructure, and medical technology adoption, creating a receptive environment for advanced wearable biosensing innovations. Government-driven Vision programs across Gulf states are prioritizing healthcare technology as a pillar of economic diversification, which may accelerate the introduction of glucose-sensing smart contact lens platforms into clinical and consumer settings. In Africa, while infrastructure and regulatory capacity remain developmental, South Africa and select North African markets are showing early interest in advanced diabetes management technologies. Over the forecast period through 2034, the Middle East is expected to serve as the primary adoption gateway for Smart Contact Lens (Glucose) Sensor ASIC Market expansion across this broader regional landscape.

Report Scope

This market research report provides a comprehensive analysis of the Smart Contact Lens (Glucose) Sensor ASIC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Contact Lens (Glucose) Sensor ASIC Market?

-> Global Smart Contact Lens (Glucose) Sensor ASIC Market size is estimated to be valued at USD 145 million in 2025 and is expected to reach USD 428 million by 2034, exhibiting a CAGR of 12.9% during the forecast period.

Which key companies operate in Smart Contact Lens (Glucose) Sensor ASIC Market?

-> Key players in Smart Contact Lens (Glucose) Sensor ASIC Market include leading medical device manufacturers, semiconductor companies, and smart wearable biosensor developers across the U.S., South Korea, and Japan, among others, who are actively investing in R&D programs to advance tear-based glucose sensing accuracy and ASIC power efficiency.

What are the key growth drivers?

-> Key growth drivers include increasing global diabetes prevalence, rising demand for non-invasive glucose monitoring solutions, ongoing investment in wearable medical electronics, advancements in semiconductor miniaturization, and progress in flexible electronics accelerating product development.

Which region dominates the market?

-> Asia-Pacific is among the fastest-growing regions, with significant R&D activity reported in South Korea and Japan, while North America, particularly the U.S., also plays a dominant role driven by sustained investment from medical device manufacturers and semiconductor companies.

What are the emerging trends?

-> Emerging trends include ultra-miniaturized ASIC design for contact lens form factors, biochemical sensing module integration, low-power wireless communication advancements, tear-fluid glucose sensing innovations, and flexible medical-grade microelectronics enabling continuous, non-invasive diabetes management solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...