Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market Insights

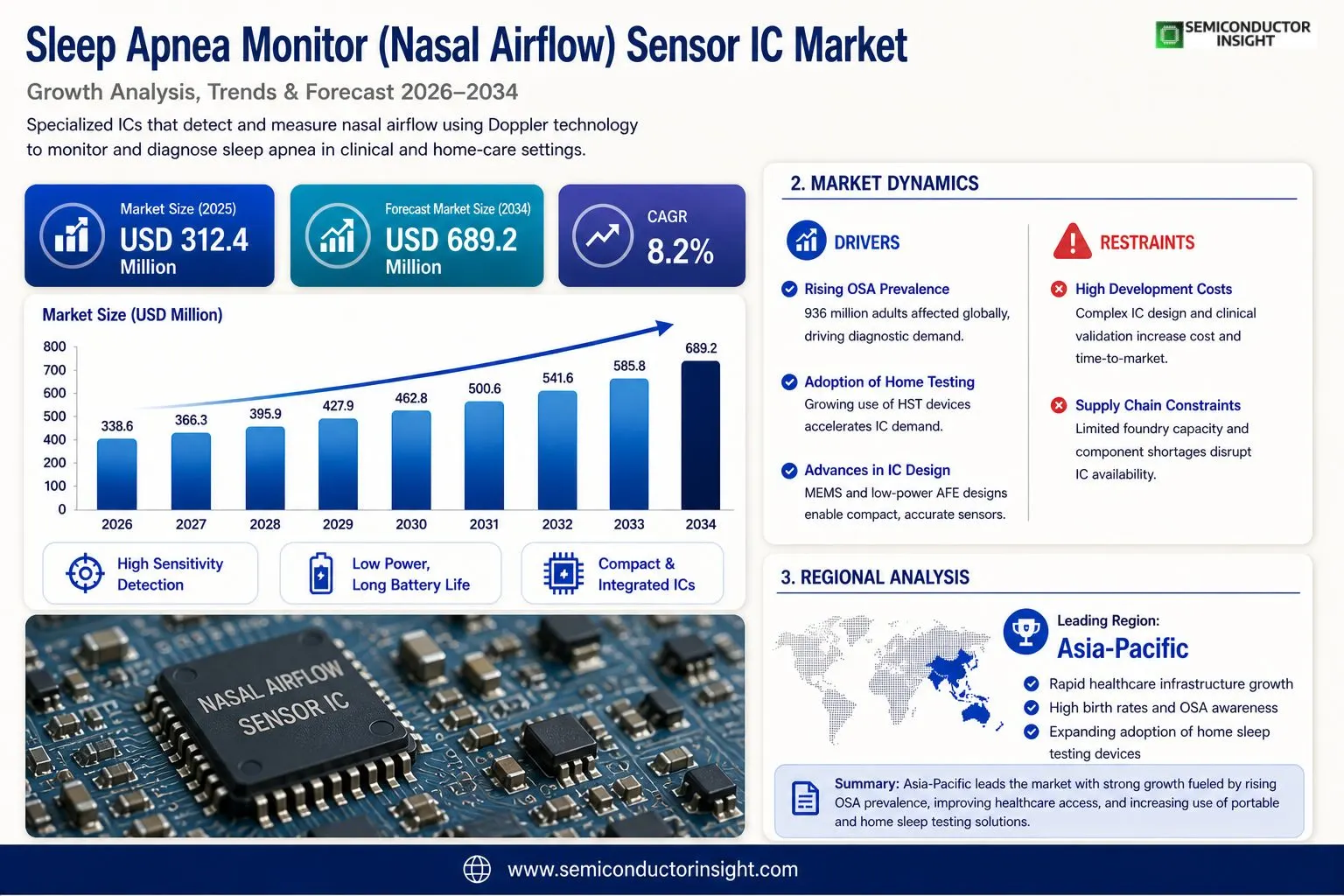

Global Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market size was valued at USD 312.4 million in 2025. The market is projected to grow from USD 338.6 million in 2026 to USD 689.2 million by 2034, exhibiting a CAGR of 8.2% during the forecast period.

Sleep apnea monitor nasal airflow sensor integrated circuits (ICs) are specialized semiconductor components designed to detect and measure airflow through the nasal passage during sleep. These ICs form the core sensing element in diagnostic and home-use sleep apnea monitoring devices, capturing subtle changes in airflow velocity, temperature, and pressure to identify apneic events and hypopneas. The sensor IC category encompasses thermistor-based ICs, pressure transducer ICs, and MEMS-integrated flow sensing chips, all engineered for high sensitivity, low power consumption, and seamless integration into wearable and polysomnography-grade monitoring systems.

The market is witnessing robust expansion driven by the rising global prevalence of obstructive sleep apnea (OSA), which affects an estimated 936 million adults worldwide, according to data published in The Lancet Respiratory Medicine. Growing awareness of sleep-disordered breathing, combined with increasing adoption of home sleep testing (HST) devices, is accelerating demand for high-performance nasal airflow sensor ICs. Furthermore, advancements in MEMS fabrication and low-power analog front-end (AFE) design are enabling more compact, accurate, and energy-efficient sensor solutions. Key players operating across this space include Analog Devices, Inc., Texas Instruments Incorporated, Sensirion AG, and ams-OSRAM AG, each contributing differentiated sensor IC platforms tailored to clinical and consumer-grade sleep monitoring applications.

MARKET DRIVERS

Rising Global Prevalence of Sleep Apnea Fueling Demand for Advanced Sensor IC Solutions

Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market is experiencing significant growth momentum, driven primarily by the escalating global burden of obstructive sleep apnea (OSA) and related sleep-disordered breathing conditions. Healthcare organizations worldwide estimate that hundreds of millions of adults suffer from moderate to severe sleep apnea, with a substantial proportion remaining undiagnosed. This diagnostic gap has intensified the demand for compact, accurate, and energy-efficient nasal airflow sensor integrated circuits capable of enabling continuous, non-invasive respiratory monitoring. As awareness campaigns by pulmonologists, sleep specialists, and public health agencies gain traction, more patients are being directed toward formal sleep studies and home-based monitoring devices that rely on high-precision nasal airflow sensor IC technology.

Technological Advancements in MEMS and Mixed-Signal IC Design Accelerating Market Adoption

Breakthroughs in Micro-Electro-Mechanical Systems (MEMS) fabrication and mixed-signal integrated circuit architecture have substantially elevated the performance benchmarks for nasal airflow detection components used in sleep apnea monitors. Modern sensor ICs now offer ultra-low power consumption, miniaturized form factors, and improved signal-to-noise ratios, making them ideally suited for wearable and home sleep testing (HST) devices. The convergence of analog front-end (AFE) circuitry with digital signal processing capabilities within a single IC die has reduced both bill-of-materials costs and device complexity. These engineering advances are enabling medical device manufacturers to develop Sleep Apnea Monitor (Nasal Airflow) Sensor IC-based products that meet stringent clinical accuracy standards while remaining accessible for ambulatory use outside traditional polysomnography lab settings.

➤ The shift toward home sleep testing, driven by patient preference for non-invasive, comfortable monitoring, is a pivotal structural driver reshaping procurement patterns across Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market globally.

Regulatory momentum is also reinforcing market drivers, as health authorities in North America, Europe, and the Asia-Pacific region continue to broaden reimbursement coverage for home-based sleep apnea diagnostics. This policy evolution is prompting original equipment manufacturers (OEMs) and contract device manufacturers to scale up procurement of reliable nasal airflow sensor ICs, creating sustained volume demand. Strategic partnerships between semiconductor companies and medical device firms are further accelerating design-win cycles, ensuring that next-generation sleep monitoring platforms are built around application-specific IC solutions optimized for respiratory airflow measurement.

MARKET CHALLENGES

Stringent Regulatory Compliance and Clinical Validation Requirements Posing Barriers to Market Entry

One of the foremost challenges confronting participants in Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market is the rigorous regulatory approval process governing medical-grade sensor components. Integrated circuits embedded in sleep apnea monitors are subject to classification requirements under frameworks such as the FDA’s Quality System Regulation (QSR) and the EU Medical Device Regulation (MDR 2017/745). Achieving and maintaining compliance demands extensive clinical validation, biocompatibility testing, and traceability documentation, which significantly extends time-to-market and escalates development expenditures for IC vendors. Smaller semiconductor firms with limited regulatory infrastructure often find it difficult to compete with established players that have pre-existing quality management systems aligned with ISO 13485 standards.

Other Challenges

Signal Interference and Measurement Accuracy in Real-World Conditions

Nasal airflow sensor ICs must maintain measurement fidelity across diverse patient anatomies, ambient temperature variations, and physical movement during sleep. Motion artifacts, humidity fluctuations near the nasal passage, and electromagnetic interference from co-located wireless communication modules can compromise sensor output integrity. Engineering robust analog front-end designs that deliver consistent accuracy under these variable real-world conditions remains a persistent technical challenge for IC developers targeting Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market.

Supply Chain Vulnerabilities and Semiconductor Component Shortages

Global semiconductor supply chain has demonstrated structural fragility, particularly for specialty analog and mixed-signal ICs produced in low-to-mid volume tiers. Medical device manufacturers dependent on specific nasal airflow sensor IC configurations face procurement risks when foundry capacity is constrained or when sole-sourced components reach end-of-life status. Building supply chain resilience through dual-sourcing strategies and safety stock management is increasingly prioritized, though it adds operational complexity and working capital requirements across the value chain.

MARKET RESTRAINTS

High Development Costs and Long Design Cycles Limiting Commercialization Speed

The development of application-specific nasal airflow sensor ICs for sleep apnea monitoring entails significant non-recurring engineering (NRE) costs, particularly when custom ASIC or specialized mixed-signal designs are required. Tape-out expenses at advanced process nodes, combined with iterative prototype validation and clinical testing cycles, can stretch development timelines considerably. These financial and temporal barriers restrain the pace at which new entrants can bring differentiated sensor IC solutions to market, effectively consolidating design activity among a limited number of well-capitalized semiconductor vendors. Smaller medical device OEMs, especially in emerging markets, may defer adoption of advanced sensor ICs in favor of lower-cost thermistor-based airflow detection alternatives, constraining addressable market expansion for premium IC solutions.

Competition from Alternative Airflow Detection Technologies Moderating Market Penetration

Despite the clinical advantages associated with semiconductor-based nasal airflow sensor ICs, Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market faces competitive pressure from legacy detection modalities including thermistors, thermocouple arrays, and pressure transducer cannula systems. These technologies benefit from established clinical familiarity, lower per-unit cost structures, and broad compatibility with existing polysomnography hardware ecosystems. In cost-sensitive healthcare procurement environments, particularly across public health systems in developing economies, the economic calculus frequently favors conventional airflow detection components over advanced sensor IC alternatives. This substitution risk acts as a meaningful restraint on volume growth within the dedicated sensor IC segment, particularly in the near-to-medium term horizon.

MARKET OPPORTUNITIES

Expansion of Wearable and Connected Health Ecosystems Creating New Application Frontiers

The rapid proliferation of connected health platforms and wearable medical devices presents a compelling growth opportunity for Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market. As consumer health technology companies and clinical-grade device manufacturers converge on the sleep health segment, demand is growing for ultra-miniaturized, Bluetooth-enabled sensor IC modules capable of transmitting nasal airflow data to cloud-based analytics platforms in real time. Integration of nasal airflow sensor ICs into form factors such as smart sleep masks, nasal interface wearables, and integrated CPAP therapy monitoring systems is opening addressable markets that extend well beyond traditional polysomnography equipment. IC vendors that invest in developing low-power, wireless-compatible sensor solutions with open digital interfaces are well-positioned to capture design wins across this expanding product landscape.

Emerging Market Healthcare Infrastructure Development Unlocking Significant Untapped Demand

Rapid healthcare infrastructure expansion across the Asia-Pacific, Latin America, and Middle East & Africa regions is creating substantial untapped demand within Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market. Rising middle-class populations, increasing health insurance penetration, and growing government investment in non-communicable disease management programs are collectively elevating diagnostic capacity for sleep disorders in markets that have historically been underserved. Local medical device manufacturing initiatives, supported by favorable industrial policy frameworks in countries such as India, China, and Brazil, are generating new procurement channels for nasal airflow sensor IC components. Semiconductor suppliers that develop region-specific product configurations , optimized for cost, regulatory compatibility, and local environmental operating conditions , stand to benefit materially from this geographic market diversification opportunity.

Artificial Intelligence Integration Enhancing Diagnostic Value of Nasal Airflow Sensor IC Platforms

The integration of artificial intelligence and machine learning algorithms with nasal airflow sensor IC output represents one of the most strategically significant opportunities shaping the future trajectory of Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market. Embedded AI inference engines, increasingly implemented at the edge within the sensor IC or companion microcontroller, enable real-time classification of apneic events, hypopneas, and respiratory effort-related arousals with clinically meaningful accuracy. This on-device intelligence reduces dependence on cloud connectivity for diagnostic decision support, enhances patient data privacy, and lowers latency in therapy-triggering applications. IC vendors collaborating with software analytics firms and clinical AI developers to create validated, algorithm-paired sensor solutions are establishing durable competitive differentiation and unlocking premium pricing opportunities within this evolving market segment.

Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market Trends

Rising Prevalence of Obstructive Sleep Apnea Accelerating Demand for Nasal Airflow Sensor ICs

Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market is experiencing significant momentum driven by the escalating global burden of obstructive sleep apnea (OSA). With an estimated 936 million adults affected worldwide, as reported in The Lancet Respiratory Medicine, healthcare providers and device manufacturers are increasingly prioritizing high-performance nasal airflow sensor integrated circuits to meet diagnostic demands. This surge in OSA prevalence is compelling medical device companies to invest in next-generation sensor IC platforms capable of delivering precise airflow detection with minimal power consumption, particularly for both clinical polysomnography systems and home sleep testing environments.

Other Trends

Rapid Adoption of Home Sleep Testing Devices

One of the most prominent trends shaping Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market is the accelerating shift toward home sleep testing (HST). Patients and clinicians alike are favoring HST solutions over traditional in-lab polysomnography due to their convenience, lower cost, and improved patient compliance. This transition is directly fueling demand for compact, low-power nasal airflow sensor ICs that can be seamlessly embedded into portable monitoring wearables. Thermistor-based ICs and MEMS-integrated flow sensing chips are increasingly being engineered to meet the stringent accuracy and energy efficiency requirements of these home-use diagnostic platforms.

Advancements in MEMS Fabrication and Low-Power AFE Design

Technological innovation in microelectromechanical systems (MEMS) fabrication and analog front-end (AFE) circuit design is redefining performance benchmarks within Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market. Manufacturers are developing sensor ICs with enhanced sensitivity to subtle changes in airflow velocity, temperature, and nasal pressure, enabling more reliable detection of apneic events and hypopneas. The integration of low-power AFE architectures is allowing device designers to extend battery life in wearable sleep monitors without compromising signal fidelity, a critical requirement for overnight diagnostic use cases.

Competitive Innovation Among Key Market Players Driving Differentiated Sensor IC Platforms

Leading companies operating in Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market, including Analog Devices, Inc., Texas Instruments Incorporated, Sensirion AG, and ams-OSRAM AG, are actively advancing differentiated sensor IC solutions tailored to both clinical-grade and consumer sleep monitoring applications. These players are focusing on enhancing chip-level integration, improving signal processing capabilities, and reducing form factors to address the evolving needs of device manufacturers. Growing awareness of sleep-disordered breathing among the general population, combined with supportive regulatory pathways for home diagnostic devices, continues to reinforce sustained innovation and competitive positioning across the nasal airflow sensor IC landscape.

COMPETITIVE LANDSCAPE

Key Industry Players

Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market: Competitive Dynamics and Leading Innovators

Global Sleep Apnea Monitor (Nasal Airflow) Sensor IC market is moderately consolidated, with a mix of established semiconductor giants and specialized MEMS sensor developers competing for market share. Analog Devices, Inc. and Texas Instruments Incorporated lead the market by leveraging their extensive analog front-end (AFE) IC portfolios and precision signal conditioning capabilities tailored for medical-grade nasal airflow sensing applications. These companies benefit from deep R&D investment, robust manufacturing infrastructure, and long-standing relationships with original equipment manufacturers (OEMs) of polysomnography and home sleep testing (HST) devices. Sensirion AG has emerged as a strong contender, distinguished by its proprietary MEMS-based flow sensing technology optimized for low-power, high-sensitivity detection of subtle nasal airflow variations associated with apneic events and hypopneas. ams-OSRAM AG further reinforces the competitive intensity with its integrated sensor IC solutions combining optical and analog sensing capabilities suited for wearable sleep monitoring systems.

Beyond the dominant players, a cohort of specialized and emerging companies is actively advancing the Sleep Apnea Monitor (Nasal Airflow) Sensor IC landscape. STMicroelectronics and NXP Semiconductors bring significant MEMS fabrication expertise and ultra-low-power IC design capabilities to clinical and consumer-grade applications. Infineon Technologies AG contributes pressure transducer and MEMS sensor IC platforms relevant to nasal airflow monitoring, while Honeywell International Inc. offers precision airflow sensing solutions with proven medical device certifications. Bosch Sensortec GmbH, a recognized leader in MEMS sensors for consumer health applications, is expanding its footprint in sleep diagnostics through miniaturized, energy-efficient sensor ICs. Additional participants including Microchip Technology Inc., Silicon Laboratories Inc., Maxim Integrated (now part of Analog Devices), and ROHM Semiconductor are also active in supplying low-power analog and mixed-signal ICs applicable to nasal airflow sensor platforms. Collectively, these companies are intensifying competition through product differentiation, strategic partnerships with sleep diagnostic device manufacturers, and continuous investment in MEMS process innovation to address the growing global burden of obstructive sleep apnea (OSA).

List of Key Sleep Apnea Monitor (Nasal Airflow) Sensor IC Companies Profiled

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Sensirion AG

- ams-OSRAM AG

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies AG

- Honeywell International Inc.

- Bosch Sensortec GmbH

- Microchip Technology Inc.

- Silicon Laboratories Inc.

- Maxim Integrated (part of Analog Devices)

- ROHM Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MEMS-Integrated Flow Sensing ICs represent the most dynamically advancing sensor type within this market, driven by rapid miniaturization trends and growing demand for wearable-compatible monitoring solutions.

|

| By Application |

|

Home Sleep Testing (HST) Devices have emerged as the dominant application segment, reflecting a broader global shift toward patient-centric, out-of-clinic diagnostic pathways for obstructive sleep apnea.

|

| By End User |

|

Home Care Settings constitute the fastest-growing end user category, fueled by patient preference for comfortable, non-disruptive sleep monitoring in familiar environments combined with widespread insurance coverage expansion for home-based diagnostics.

|

| By Technology Platform |

|

Wireless and Bluetooth-Enabled Sensor ICs are gaining considerable traction as device manufacturers prioritize patient comfort and seamless connectivity with mobile health ecosystems.

|

| By Device Grade |

|

Clinical-Grade Sensor ICs continue to command a position of strategic importance within the market, as they underpin the reliability and regulatory compliance of diagnostic-grade sleep apnea monitoring equipment used in professional healthcare settings.

|

Regional Analysis: Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market

North America

North America’s extensive network of sleep disorder centers and pulmonology clinics provides a strong foundation for nasal airflow sensor IC deployment. Hospitals and outpatient facilities increasingly integrate advanced sensor IC-based monitors into their diagnostic protocols, ensuring early detection and continuous monitoring of sleep apnea patients across diverse demographic groups throughout the region.

The FDA’s streamlined approval pathways for sensor IC-integrated sleep apnea monitoring devices have greatly reduced time-to-market for manufacturers. Favorable reimbursement policies from both private insurers and government-backed healthcare programs encourage widespread clinical utilization of nasal airflow monitoring technologies, directly supporting sustained market expansion across the United States and Canada.

North America hosts a concentration of semiconductor firms and medical technology innovators actively developing miniaturized, low-power nasal airflow sensor ICs. Collaborative research between academic institutions and industry players accelerates the commercialization of next-generation solutions, with a strong emphasis on wireless connectivity, AI-assisted signal processing, and enhanced patient comfort for long-term sleep monitoring applications.

A clear shift toward home sleep testing in North America is expanding the addressable market for nasal airflow sensor IC-enabled portable devices. Patients and clinicians alike favor ambulatory diagnostic solutions that reduce hospital visits while maintaining diagnostic accuracy. This transition is prompting manufacturers to prioritize compact, user-friendly sensor IC architectures compatible with connected home healthcare ecosystems.

Europe

Europe represents a significant and steadily growing region within Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market, supported by universal healthcare systems that prioritize respiratory health management. Countries such as Germany, France, the United Kingdom, and the Netherlands have established comprehensive national sleep health programs that promote early diagnosis of obstructive sleep apnea using advanced nasal airflow monitoring technologies. The European Medicines Agency and country-level regulatory bodies maintain rigorous standards that ensure only clinically validated sensor IC devices reach the market, reinforcing patient safety and product quality. Europe’s aging population and the consequent rise in sleep-disordered breathing conditions continue to generate consistent demand. Additionally, a growing emphasis on digital health integration and cross-border data sharing among EU member states is creating favorable conditions for the deployment of smart, connected nasal airflow sensor IC platforms within the regional Sleep Apnea Monitor market ecosystem.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region in Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market, propelled by rapidly expanding healthcare access, increasing urbanization, and a growing awareness of sleep health across populous nations including China, Japan, India, South Korea, and Australia. The region’s large undiagnosed sleep apnea patient pool represents a substantial untapped opportunity for nasal airflow sensor IC solution providers. Government-led healthcare modernization initiatives in China and India are channeling significant investment into hospital infrastructure and diagnostic equipment procurement. Japan and South Korea, known for their advanced electronics manufacturing capabilities, are contributing to local sensor IC innovation tailored for sleep monitoring applications. Rising disposable incomes and greater health consciousness among middle-class populations are further accelerating the adoption of both clinical-grade and consumer-oriented nasal airflow monitoring solutions throughout Asia-Pacific.

South America

South America presents a developing yet progressively important market within Global Sleep Apnea Monitor (Nasal Airflow) Sensor IC landscape. Brazil and Argentina lead regional adoption, supported by gradually improving healthcare access and growing clinical awareness of sleep-disordered breathing conditions. Private healthcare providers in major urban centers are beginning to incorporate nasal airflow sensor IC-based diagnostic tools into their pulmonology and ENT practices, responding to rising patient demand for accurate sleep disorder assessments. However, economic volatility, limited reimbursement coverage, and inconsistent regulatory frameworks across different countries remain challenges that temper the pace of market expansion. Despite these constraints, international medical device manufacturers are increasingly viewing South America as a long-term strategic opportunity, establishing local distribution partnerships to navigate regulatory complexities and reach an underserved patient population in need of effective sleep apnea monitoring solutions.

Middle East & Africa

The Middle East & Africa region occupies a nascent but gradually evolving position in Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are leading regional adoption by investing in world-class hospital facilities and attracting internationally trained sleep medicine specialists. Elevated rates of obesity and metabolic syndrome across GCC populations are contributing to a rising burden of obstructive sleep apnea, generating demand for advanced nasal airflow sensor IC-integrated diagnostic devices. In contrast, Sub-Saharan Africa faces significant infrastructure and affordability barriers that currently limit widespread market penetration. Nonetheless, international health organizations and development programs are gradually improving diagnostic capabilities in the region. Over the forecast horizon to 2034, targeted investment in healthcare infrastructure and increasing awareness campaigns are expected to progressively open new growth avenues for Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market across both subregions.

Report Scope

This market research report provides a comprehensive analysis of the Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market?

-> Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market was valued at USD 312.4 million in 2025 and is expected to reach USD 689.2 million by 2034, growing at a CAGR of 8.2% during the forecast period from 2026 to 2034.

Which key companies operate in Sleep Apnea Monitor (Nasal Airflow) Sensor IC Market?

-> Key players include Analog Devices, Inc., Texas Instruments Incorporated, Sensirion AG, and ams-OSRAM AG, among others, each contributing differentiated sensor IC platforms tailored to clinical and consumer-grade sleep monitoring applications.

What are the key growth drivers?

-> Key growth drivers include the rising global prevalence of obstructive sleep apnea (OSA), which affects an estimated 936 million adults worldwide, growing awareness of sleep-disordered breathing, increasing adoption of home sleep testing (HST) devices, and advancements in MEMS fabrication and low-power analog front-end (AFE) design.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to expanding healthcare infrastructure and rising OSA awareness, while North America remains a dominant market driven by high adoption of home sleep testing devices and advanced diagnostic technologies.

What are the emerging trends?

-> Emerging trends include MEMS-integrated flow sensing chips, wearable polysomnography-grade monitoring systems, low-power analog front-end (AFE) sensor designs, and the integration of thermistor-based ICs and pressure transducer ICs into compact, energy-efficient sleep apnea diagnostic platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...