Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market Insights

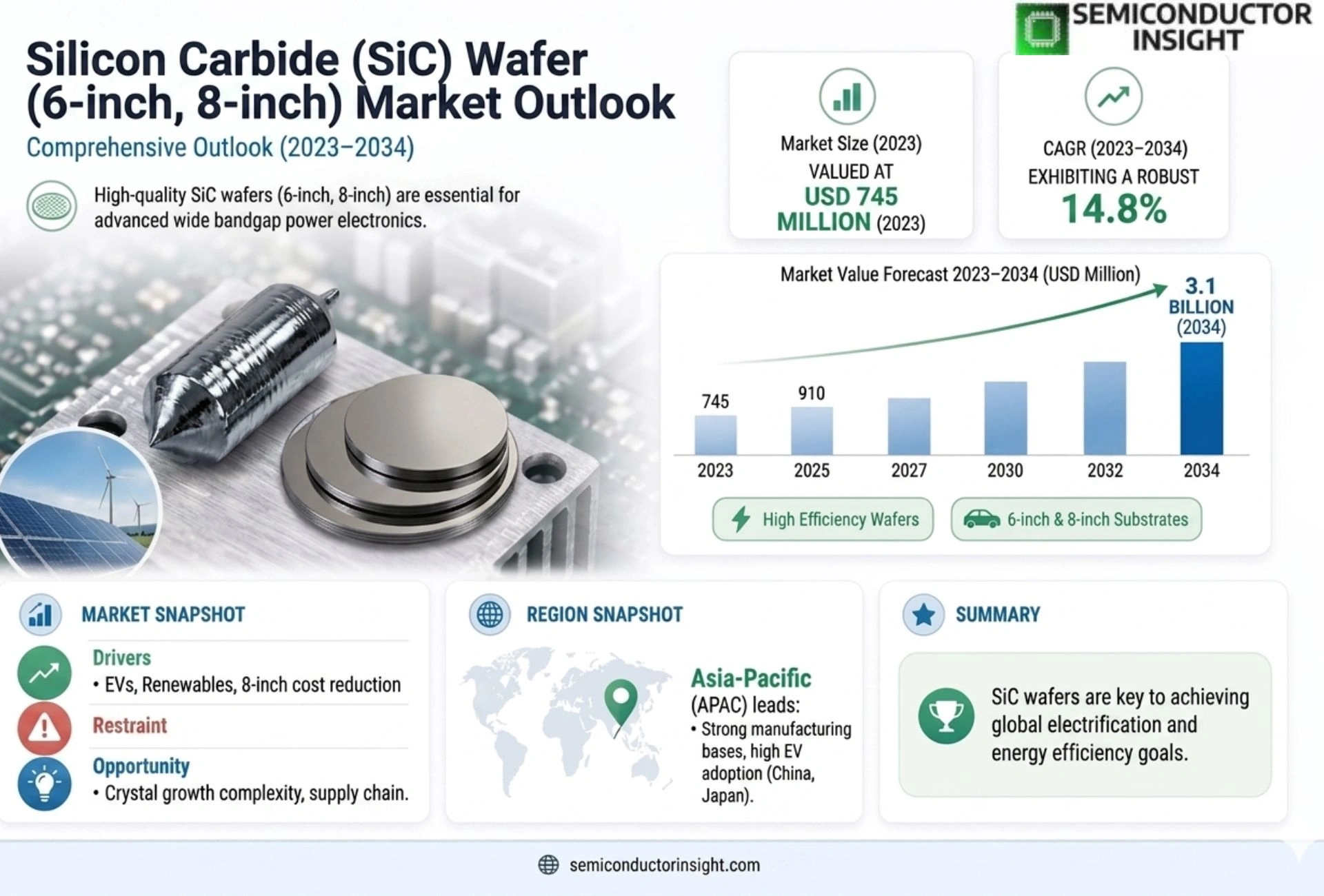

Global Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market size was valued at USD 745 million in 2023 and is projected to expand from USD 910 million in 2025 to USD 3.1 billion by 2034, exhibiting a robust CAGR of 14.8% during the forecast period.

This rapid growth trajectory reflects the escalating adoption of SiC wafers across high-power electronics, electric vehicles (EVs), and renewable energy systems due to their superior thermal conductivity, wide bandgap properties, and efficiency advantages over traditional silicon-based substrates.

Silicon Carbide (SiC) wafers are advanced semiconductor substrates engineered for high-voltage and high-temperature applications. Available primarily in 6-inch (150mm) and 8-inch (200mm) diameters, these wafers enable the fabrication of power devices such as MOSFETs, Schottky diodes, and IGBTs that operate at elevated frequencies with minimal energy loss. The transition from smaller diameters to larger formats,particularly the industry-wide shift toward 8-inch SiC wafers,is driven by economies of scale, improved yield rates, and compatibility with existing silicon-based fabrication infrastructure. While 6-inch wafers currently dominate production due to established manufacturing maturity, the adoption of 8-inch wafers is accelerating as leading manufacturers like Wolfspeed, II-VI Incorporated, and SK Siltron invest heavily in capacity expansion to meet surging demand from automotive OEMs and industrial sectors.

MARKET DRIVERS

Rapid Electrification of Automotive Sector

The automotive industry is undergoing a transformative shift toward electric vehicles (EVs), which is a primary catalyst for the growth of Global Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market. Manufacturers are increasingly adopting SiC power MOSFETs and Schottky diodes in electric inverters and on-board chargers to increase efficiency and reduce energy loss. This transition demands advanced semiconductor materials, driving the need for larger and high-quality wafers.

Enhanced Thermal and Electrical Properties

SiC offers superior thermal conductivity and higher breakdown electric field strength compared to traditional silicon. This makes it ideal for high-power and high-frequency applications. As the industry moves toward 8-inch wafer production, manufacturers can achieve lower production costs while utilizing these superior material properties to create more compact and efficient electronic systems.

➤ The shift from 150mm to 200mm (8-inch) wafers allows for significantly higher throughput and reduced manufacturing costs per device.

Furthermore, the demand for 6-inch wafers remains stable, primarily serving industrial motor drives and renewable energy converters where efficiency is critical. Analysts project that the continued integration of these higher-performing wafers will solidify the market’s upward trajectory.

MARKET CHALLENGES

Supply Chain Volatility

One of the significant hurdles facing the industry is the complex and often fragmented supply chain for semiconductor raw materials. Sourcing high-purity quartz sand and other precursor chemicals requires rigorous quality control to ensure the final wafer meets industry standards. Disruptions in logistics or fluctuating prices of raw materials can directly impact the manufacturing timelines for Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market.

Material Quality Consistency

Producing SiC wafers with consistent crystal structure and defect-free surfaces is technically demanding. Variations in material quality can lead to yield issues, especially during the diffusion processes of 8-inch wafers. Achieving uniformity across large surface areas at industrial scales presents a persistent engineering challenge for manufacturers.

Other Challenges

Initial Capital Expenditure

Establishing production facilities capable of handling SiC wafers requires substantial financial investment, particularly for equipment designed to manage the hardness of the substrate.

Competition from SiC vs. GaN

Gallium Nitride (GaN) power electronics are gaining traction in certain niche applications, forcing SiC players to constantly innovate to maintain their competitive edge.

MARKET RESTRAINTS

High Manufacturing Costs

The production process for silicon carbide wafers, particularly the formation of semi-insulating substrates required for high-power devices, is energy-intensive and expensive. These high production costs are often passed down to the end consumer, potentially slowing the adoption rate in cost-sensitive markets. The economic viability of 8-inch wafers depends heavily on achieving high yield rates to offset these initial expenses.

The adoption rate in grid power and industrial sectors is sometimes restrained by the price sensitivity of utility companies. While the lifecycle cost savings of SiC devices are compelling, the upfront capital required to upgrade legacy equipment utilizing silicon or other competing technologies remains a barrier to entry for many organizations.

MARKET OPPORTUNITIES

Expansion of 8-Inch Wafer Production Capacities

The transition to 8-inch wafer formats presents a massive opportunity for market consolidation and quality improvement. Moving to larger substrates allows for a reduction in the cost per die, making high-performance silicon carbide technology accessible to a broader range of applications. Companies that successfully scale their 8-inch fabrication capabilities are well-positioned to capture significant market share.

Renewable Energy Infrastructure

The global push for sustainable energy sources, including solar and wind power, creates a robust demand for power electronics that can efficiently manage energy conversion. SiC wafers play a crucial role in high-voltage applications such as solar inverters and wind turbine power conversion systems. The growth of renewable energy infrastructure is a key driver for increasing the supply and consumption of SiC wafers.

Trends

Transition to Larger Diameter Wafers

The industrial landscape is witnessing a substantial modernization of fabrication capabilities to support the growing demand for next-generation power electronic solutions. This evolution is characterized by a strategic shift from smaller 150mm wafers to larger 200mm formats. The primary driver behind this transition is the economic advantage gained through economies of scale and improved silicon yields. By utilizing larger substrates, manufacturers can fabricate more power devices on a single wafer, thereby reducing the per-unit cost. This efficiency is becoming critical as the supply chain strives to meet the escalating requirements of the automotive and industrial machinery sectors. Industry leaders are investing significantly in capacity expansion to facilitate this technological upgrade, ensuring that production lines remain competitive in a rapidly evolving marketplace.

Other Trends

Automotive EV Adoption

The primary application area for these advanced substrates is the electric vehicle sector. Vehicle architectures now heavily integrate power electronic systems comprising MOSFETs and Schottky diodes. The material properties of silicon carbide allow for superior thermal conductivity, which is essential for high-voltage operation in confined spaces. As vehicle electrification accelerates, the reliability of SiC-based devices ensures superior energy conversion efficiency and extended driving range.

Renewable Energy Infrastructure

Beyond automotive, the energy sector is leveraging these substrates to enhance grid stability. Silicon carbide technology supports high-efficiency power inverters and converters used in solar and wind energy harvesting. The ability to operate at elevated frequencies with minimal energy loss contributes to a more robust and sustainable energy grid, reducing transmission losses across the network.

Enhanced Electronic Performance

The adoption of these substrates is fundamentally altering power electronics. The wide bandgap properties of the material allow for higher breakdown fields and lower switching losses compared to traditional silicon. This enables the development of compact, lightweight power modules that can handle greater power densities, expanding the operational envelope for industrial and mobile applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Global SiC Wafer Market Dynamics

Global Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market is witnessing robust growth due to the shifting preference for wide bandgap semiconductors in high-power applications. The market size reached USD 745 million in 2023 and is projected to reach USD 3.1 billion by 2034, driven by the increasing demand from electric vehicles and renewable energy sectors. The transition from 6-inch to 8-inch wafer production is a key competitive differentiator, enabling manufacturers to leverage economies of scale and improve yield rates for advanced power devices.

The competitive landscape is characterized by a mix of vertically integrated companies and specialized foundries that focus on crystal growth and substrate quality. While tier-one automotive OEMs drive adoption, niche players are establishing footholds by optimizing manufacturing processes for specific diameters and power grades.

List of Key SiC Wafer Manufacturers Profiled

- Wolfspeed

- II-VI Incorporated

- Soitec

- SK Siltron

- Norstel

- Microchip Technology

- Qorvo

- STMicroelectronics

- Rohm

- Sumitomo Heavy Industries

- Winbond

- Infineon

- On Semiconductor

- Nexperia

- Epistar

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

8-inch Wafers description with qualitative insights only [Pointers preferred in bullets atleast 2-3].

The industry is witnessing a rapid transition from the established 6-inch wafer format towards the larger 8-inch diameter. This strategic shift is primarily driven by the fundamental economic need for improved scalability and reduced manufacturing costs. Moving to larger wafer sizes allows manufacturers to significantly increase the yield per silicon carbide ingot, directly lowering the unit cost of power devices. This economic pressure is forcing leading semiconductor companies to invest heavily in advanced fabrication capabilities to handle the complexity of larger substrates. The adoption of 8-inch wafers simplifies integration with existing silicon fabrication infrastructure, thereby accelerating the mass production of SiC power electronics and facilitating their broader market penetration. |

| By Application |

|

High-Power Applications description with qualitative insights only [Pointers preferred in bullets atleast 2-3].

The market is fundamentally driven by the superior performance of silicon carbide wafers in high-voltage and high-frequency electronic environments. Unlike standard silicon, SiC substrates offer significantly higher thermal conductivity, allowing power devices to operate efficiently at elevated temperatures without excessive cooling. This thermal management advantage is crucial for the electrification of transportation, where compact and efficient power conversion systems are paramount. Furthermore, the wide bandgap properties of SiC enable fast switching speeds, which translates into reduced energy losses during power transmission and conversion. Consequently, automotive and industrial sectors are leveraging these material properties to enhance the efficiency, speed, and reliability of their next-generation electronic systems, creating a robust demand curve for robust SiC substrates. |

| By End User |

|

Automotive OEMs description with qualitative insights only [Pointers preferred in bullets atleast 2-3].

Automotive Original Equipment Manufacturers represent a critical growth catalyst for the silicon carbide wafer market as the industry pivots towards comprehensive electrification. The demand stems from the necessity to develop lightweight, compact power electronics that can withstand the rigorous demands of high-power vehicle platforms. By utilizing SiC wafers in the electric powertrain, manufacturers can achieve extended driving ranges and faster acceleration by minimizing energy dissipation during power conversion. This shift is supported by major automakers aiming to meet stringent environmental regulations and consumer expectations for high-performance electric vehicles. The sustained investment by automotive giants in powertrain technology continues to fuel a steady and predictable uptake of advanced semiconductor substrates capable of meeting these performance benchmarks. |

| By Wafer Diameter |

|

Economies of Scale description with qualitative insights only [Pointers preferred in bullets atleast 2-3].

The strategic decision to adopt larger wafer diameters is underpinned by the pursuit of economies of scale, which are essential for the widespread commercial viability of SiC technology in the consumer and industrial sectors. As demand grows, the industry is compelled to maximize the number of functional chips produced from a single ingot. A larger wafer diameter not only increases the throughput of manufacturing lines but also enhances the overall yield potential when combined with mature fabrication processes. This scaling strategy reduces the marginal cost per device, making SiC-based solutions competitive against traditional silicon technologies. Investors and manufacturers alike are focusing their capital expansion efforts on facilities that can support the processing of larger wafers, viewing this transition as a necessary step for long-term market leadership. |

| By Crystal Orientation |

|

Superior Material Properties description with qualitative insights only [Pointers preferred in bullets atleast 2-3].

The choice of crystal polytype is a decisive factor in determining the semiconductor characteristics of the final power device, with 4H-SiC emerging as the undisputed industry standard due to its superior electronic and thermal properties. While 6H-SiC has historically been available, 4H-SiC offers a larger bandgap energy and higher breakdown field strength, which are critical for high-voltage applications. This specific orientation allows for the creation of power devices that can efficiently handle higher power densities and operate reliably across a wide temperature range. Consequently, leading material suppliers are prioritizing the production and development of 4H-SiC crystals to ensure that the components manufactured meet the rigorous performance standards required for demanding sectors like power grids and electric mobility. |

Regional Analysis: Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market

Asia-Pacific

Robust investments in smart grid infrastructure and renewable energy projects are creating substantial opportunities for SiC wafer manufacturers across the region.

A distinct shift towards 8-inch wafer fabrication is underway to meet the growing demands of high-volume automotive and industrial applications.

The proliferation of electric mobility ecosystems in emerging markets is driving the integration of SiC devices to enhance vehicle range and charging efficiency.

Key industries are modernizing power conversion systems, utilizing SiC technology for superior efficiency and reliability under high-voltage conditions.

North America

North America secures a significant position in the Silicon Carbide (6-inch, 8-inch) Wafer Market due to advanced R&D infrastructure and a mature adoption of EV technologies. The United States demonstrates a keen interest in utilizing SiC wafers within aerospace and defense applications, capitalizing on the material’s resilience in extreme thermal conditions compared to traditional silicon solutions. Additionally, the region’s support for grid modernization initiatives supports the demand for efficient power conversion systems essential for renewable energy integration.

Europe

Europe remains a critical growth engine for the Silicon Carbide (6-inch, 8-inch) Wafer Market, largely fueled by strict environmental regulations aimed at reducing industrial emissions. The automotive sector in Europe is actively transitioning to SiC-based powertrains to maximize efficiency and minimize energy loss in electric vehicles. Furthermore, the region’s commitment to green energy projects, including wind and solar farms, necessitates the use of high-performance semiconductors to optimize grid stability and energy transmission.

South America

South America presents a developing landscape for the Silicon Carbide wafer sector, characterized by increasing interest in renewable energy projects and industrial modernization. Although the market is currently emerging, the potential for SiC integration into regional power grids is high due to the pressing need for efficient voltage control and distribution. Local industries are beginning to recognize the long-term cost benefits and technical superiority of SiC devices over conventional silicon options.

Middle East & Africa

The Middle East and Africa region are positioning themselves strategically within the Silicon Carbide (6-inch, 8-inch) Wafer Market, driven by mega-projects focused on energy independence and desalination. The adoption of SiC technology here is primarily targeted at enhancing the reliability and lifespan of power conversion units operating in harsh environmental and climatic conditions.

Report Scope

This market research report provides a comprehensive analysis of the Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market?

-> Global Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market size was valued at USD 910 million in 2025 and is expected to reach USD 3.1 billion by 2034 with a CAGR of 14.8%.

Which key companies operate Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market?

-> Key players include Wolfspeed, II-VI Incorporated, and SK Siltron.

What are the key growth drivers?

-> Key growth drivers include high-power electronics, electric vehicles (EVs), and renewable energy systems, driven by SiC’s superior thermal conductivity, wide bandgap properties, and efficiency advantages over traditional silicon-based substrates.

Which region dominates the market?

-> The market is driven by surging demand from automotive OEMs and industrial sectors.

What are the emerging trends?

-> Emerging trends include the expansion of 8-inch SiC wafers for improved economies of scale and yield rates, alongside the continued production of established 6-inch wafers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...