Power Module (SiC & GaN) for Electric Vehicles Market Insights

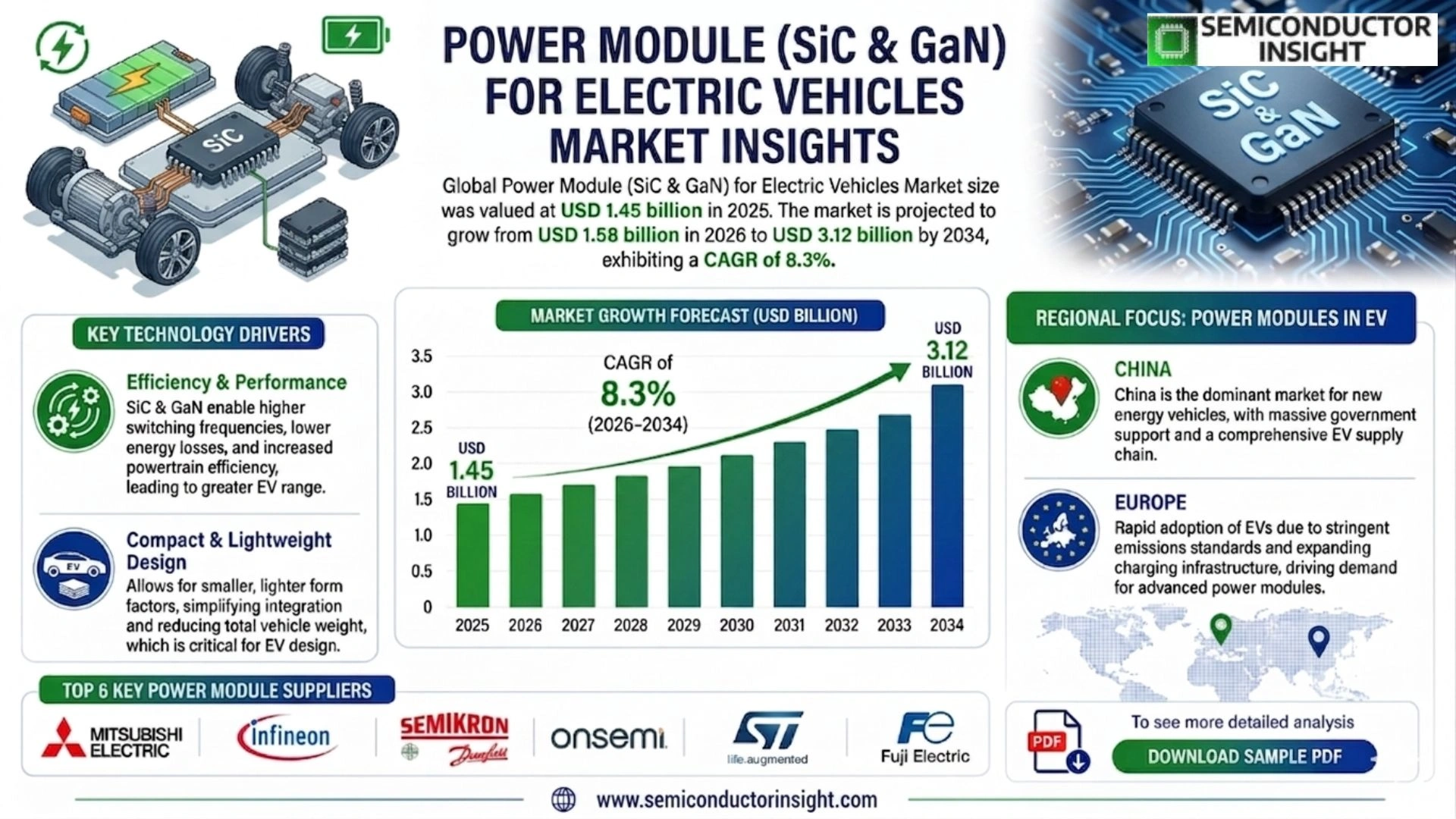

Power Module (SiC & GaN) for Electric Vehicles Market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.58 billion in 2025 to USD 3.12 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period.

Power modules based on Silicon Carbide (SiC) and Gallium Nitride (GaN) are advanced semiconductor devices designed to manage and convert electrical power efficiently in electric vehicles (EVs). These modules offer superior performance in terms of higher switching frequencies, lower power losses, and enhanced thermal management compared to traditional silicon-based modules. SiC and GaN power modules are critical components in EV powertrains, enabling improved energy efficiency, extended driving range, and reduced charging times.

The market is witnessing rapid expansion driven by increasing adoption of electric vehicles worldwide, stringent emission regulations, and the demand for higher efficiency power electronics. Furthermore, advancements in SiC and GaN technologies have led to cost reductions and enhanced reliability, encouraging OEMs and Tier 1 suppliers to integrate these modules into next-generation EV platforms. Leading players are investing heavily in R&D and strategic partnerships to capitalize on this growth. For instance, in early 2024, several collaborations between semiconductor manufacturers and automotive companies were announced to accelerate the commercialization of SiC and GaN power modules for electric vehicles.

MARKET DRIVERS

Increasing Demand for Energy-Efficient Electric Vehicles

The rising global emphasis on reducing carbon emissions has driven the adoption of electric vehicles (EVs), which require more efficient power management systems. Power modules based on Silicon Carbide (SiC) and Gallium Nitride (GaN) technologies provide superior energy efficiency compared to traditional silicon-based devices, enabling extended driving range and enhanced performance for EVs.

Technological Advancements Enhancing Module Performance

Advances in wide bandgap semiconductor materials such as SiC and GaN have resulted in power modules capable of operating at higher voltages, frequencies, and temperatures. These features contribute to improved thermal management and reduced energy losses, critical for meeting the stringent requirements of electric vehicle powertrains.

➤ Integration of SiC and GaN power modules significantly boosts EV efficiency, driving adoption in passenger and commercial electric vehicles globally.

Moreover, the adoption of these power modules aligns with OEMs’ targets for weight reduction and miniaturization of electronic components within electric vehicles, leading to more cost-effective and reliable power systems.

MARKET CHALLENGES

High Production Costs and Scalability Issues

Despite their performance advantages, SiC and GaN power modules entail higher manufacturing costs than traditional silicon modules due to complex fabrication and material expenses. This cost barrier limits their widespread adoption, especially in mid- to low-end electric vehicle segments where cost sensitivity is high.

Other Challenges

Thermal Management Complexity

The increased power density of SiC and GaN modules generates significant heat, requiring advanced cooling mechanisms to ensure reliability and longevity, which can increase system complexity and expense.

Supply Chain Constraints

Limited availability of high-purity substrates and specialized manufacturing capacity restrict scaling potential, impacting timely supply to EV manufacturers.

MARKET RESTRAINTS

Stringent Industry Standards and Regulatory Hurdles

Power Module (SiC & GaN) for Electric Vehicles Market faces restraints from rigorous safety and performance standards mandated by automotive regulatory authorities globally. Compliance with these evolving standards necessitates extensive testing and certification efforts, contributing to prolonged product development cycles and increased deployment costs.

MARKET OPPORTUNITIES

Expansion in Commercial EV and Charging Infrastructure

The expansion of the commercial electric vehicle sector, including buses and delivery trucks, presents a significant growth opportunity for SiC and GaN power modules due to their ability to improve system efficiency and reduce vehicle weight. Further, advancements in fast-charging infrastructure offer avenues to leverage these power modules to optimize energy conversion and thermal management during rapid charging cycles.

Trends

Increasing Adoption and Technological Advancements

Power Module (SiC & GaN) for Electric Vehicles Market is experiencing significant growth driven by the rising global adoption of electric vehicles (EVs). Silicon Carbide (SiC) and Gallium Nitride (GaN) power modules present considerable advantages over traditional silicon-based modules, including higher switching frequencies and lower power losses. These benefits enhance the overall efficiency of EV powertrains, which is critical for extending driving ranges and reducing charging times. Consequently, manufacturers are prioritizing the integration of these advanced semiconductor devices into new EV models.

Advancements in SiC and GaN semiconductor technology have contributed to improved thermal management and reliability of power modules, supporting higher power densities and longer component lifespans. These factors, combined with cost reductions resulting from technological progress and scaled production, are making SiC and GaN power modules increasingly attractive to automotive OEMs and Tier 1 suppliers. This trend is fostering a competitive market landscape characterized by robust research and development activities and strategic partnerships.

Other Trends

Strategic Collaborations

Collaborations between semiconductor manufacturers and automotive companies have become a key trend in accelerating the commercialization of SiC and GaN power modules. In early 2024, numerous partnerships were announced to develop optimized power modules tailored for EV applications. Such collaborations aim to improve module performance, reduce costs, and shorten time-to-market for next-generation EV platforms, reflecting the industry’s commitment to meeting stringent emission standards and consumer demand for enhanced vehicle efficiency.

Regulatory Influence

Stringent emission regulations worldwide are exerting pressure on automotive manufacturers to improve the energy efficiency of electric vehicles. This regulatory environment is indirectly fueling the demand for advanced power modules like SiC and GaN by incentivizing the adoption of technologies that reduce power losses and improve thermal management. These regulatory drivers ensure sustained market momentum and encourage continuous innovation within the semiconductor industry.

Market Outlook and Industry Focus

Looking ahead, Power Module (SiC & GaN) for Electric Vehicles Market is poised for continued expansion, supported by ongoing advancements and increasing EV production volumes. Leading industry players are expected to maintain heavy investment in research and new product development to capture significant market shares. Additionally, as SiC and GaN technologies mature, further cost reductions and integration improvements will promote wider adoption across various electric vehicle segments, including passenger cars, commercial vehicles, and two-wheelers. These developments collectively underpin a positive growth trajectory for power modules in the evolving electric mobility landscape.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics Power Module (SiC & GaN) for Electric Vehicles Market

The Power Module (SiC & GaN) market for electric vehicles is characterized by a competitive landscape dominated by several multinational semiconductor companies and specialized power electronics firms. Leading the market are industry giants such as Infineon Technologies and Wolfspeed, whose extensive R&D investments and strategic alliances with automotive OEMs position them at the forefront of innovation. These companies leverage advanced manufacturing capabilities and proprietary SiC and GaN technologies to deliver high-performance power modules crucial for enhancing EV efficiency and driving range. The market structure is increasingly shaped by collaborations between semiconductor leaders and EV manufacturers to accelerate the integration of these power modules into next-generation electric vehicles.

Other notable players include STMicroelectronics and Mitsubishi Electric, which focus on niche applications and cost-effective SiC modules, appealing to diverse segments within the EV supply chain. Emerging companies such as ROHM Semiconductor and ON Semiconductor are carving out significant market shares by advancing GaN power module technology aimed at reducing charging times and improving thermal management. Additionally, firms like Toshiba and United Silicon Carbide are gaining traction through specialized solutions tailored to high-power density requirements. The competitive environment is further enriched by companies such as Texas Instruments, Hitachi Automotive Systems, and Nissin Electric, which capitalize on their automotive expertise to deliver integrated power electronics solutions. The increasingly fragmented yet innovation-driven market underscores the importance of continuous product development and strategic partnerships to maintain competitive advantage.

List of Key Power Module (SiC & GaN) for Electric Vehicles Companies Profiled

- Infineon Technologies

- Wolfspeed

- STMicroelectronics

- Mitsubishi Electric

- ROHM Semiconductor

- ON Semiconductor

- Toshiba

- United Silicon Carbide

- Texas Instruments

- Hitachi Automotive Systems

- Nissin Electric

- Fuji Electric

- Alpha and Omega Semiconductor

- Vishay Intertechnology

- Microchip Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon Carbide (SiC) Power Modules lead the market with their superior thermal performance and efficiency which directly enhance EV powertrain robustness.

Gallium Nitride (GaN) Power Modules complement SiC by delivering high-frequency switching capabilities fully optimizing inverter and onboard charger performance.

|

| By Application |

|

Inverters represent a critical application segment as they convert DC battery power to AC for the electric motor, necessitating efficient and robust power modules.

Onboard Chargers benefit from SiC and GaN modules by enabling faster, more efficient battery charging systems.

DC-DC Converters utilize these power modules to manage voltage conversions for different vehicle subsystems.

|

| By End User |

|

Original Equipment Manufacturers (OEMs) dominate as they integrate SiC & GaN power modules directly into EV production platforms.

Aftermarket Suppliers expand opportunities by providing retrofit and replacement power modules.

Tier 1 Suppliers play a pivotal role as intermediaries developing and supplying advanced modules.

|

| By Technology Integration |

|

Hybrid Power Modules are increasingly preferred for their ability to combine SiC and GaN advantages for optimized performance.

Discrete Power Modules remain relevant due to ease of assembly and cost-effectiveness.

Monolithic Power Modules offer benefits in miniaturization and reliability.

|

| By Vehicle Type |

|

Passenger Vehicles lead the demand for power modules due to the rapid adoption of electric cars across consumer markets.

Commercial Vehicles present a growing opportunity with their specific efficiency and durability needs.

Two-wheelers and Others represent an emerging market segment that benefits from compact, lightweight power modules.

|

Regional Analysis: Power Module (SiC & GaN) for Electric Vehicles Market

Asia-Pacific

Asia-Pacific’s leadership is fueled by its established semiconductor fabrication industry, which supports large-scale production of SiC and GaN power modules. This manufacturing strength ensures competitive pricing and quick turnaround times, crucial for EV supply chains.

Governments in the region actively promote electrification through subsidies, tax benefits, and infrastructure development. These measures accelerate the integration of advanced power modules in EVs, facilitating sustainable market growth.

Partnerships between technology providers and automotive companies drive innovation in compact and high-efficiency power module designs, enhancing the performance and range of electric vehicles operating within the regional market.

Increasing consumer adoption of electric vehicles and expanding charging infrastructure create robust demand for reliable and efficient SiC & GaN power modules, supporting sustained market expansion across Asia-Pacific.

North America

North America is witnessing steady growth Power Module (SiC & GaN) for Electric Vehicles Market, driven by technological advancements and rising environmental awareness. The U.S. leads with innovative companies developing next-generation power modules aimed at boosting EV performance and energy efficiency. Government regulations focused on reducing carbon emissions, combined with substantial investments in EV infrastructure, contribute to increasing demand for SiC and GaN components. Additionally, collaborations between semiconductor manufacturers and automotive OEMs are laying the foundation for more scalable and efficient power electronics solutions, stimulating regional market prospects through 2034.

Europe

Europe’s electric vehicles market is evolving rapidly with a strong emphasis on sustainability and emissions regulations. The demand for power modules using silicon carbide and gallium nitride is rising sharply as automakers seek to enhance electric powertrain efficiency and extend vehicle range. Countries such as Germany, France, and the UK prioritize local production capabilities and innovative technologies, supported by government policies encouraging clean transportation. The regional focus on research, development, and deployment of advanced power electronics plays a pivotal role in Europe’s strategy to lead the EV power module sector globally.

South America

South America’s Power Module (SiC & GaN) market for electric vehicles is in infancy but showing promising potential, particularly in Brazil and Chile, where eco-friendly policies are gaining traction. Market development is influenced by gradual EV adoption and emerging investments in EV infrastructure. Though production capabilities remain limited, the region benefits from increasing technology transfers and growing interest from international suppliers. Expansion of localized supply chains and favorable regulatory environments are expected to enhance the deployment of power modules for EVs within the next decade.

Middle East & Africa

The Middle East and Africa region is gradually embracing the electric vehicle revolution, creating nascent demand for SiC and GaN power modules. Investments in sustainable transportation and renewable energy frameworks form the backbone for market growth. However, infrastructural and technological constraints limit large-scale adoption. Initiatives to develop charging networks and partnerships with global technology providers are underway to facilitate market entry. Continued governmental and private sector support will be critical to unlocking growth potential in power module applications for electric vehicles across these emerging markets.

Report Scope

This market research report provides a comprehensive analysis of the Power Module (SiC & GaN) for Electric Vehicles Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power Module (SiC & GaN) for Electric Vehicles Market?

-> Power Module (SiC & GaN) for Electric Vehicles Market was valued at USD 1.45 billion in 2025 and is expected to reach USD 3.12 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period.

Which key companies operate Power Module (SiC & GaN) for Electric Vehicles Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of electric vehicles worldwide, stringent emission regulations, and the demand for higher efficiency power electronics.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by rapid EV adoption, while Europe remains a dominant market due to strong regulatory frameworks.

What are the emerging trends?

-> Emerging trends include advancements in SiC and GaN technologies leading to cost reductions, enhanced reliability, and strategic collaborations accelerating commercialization of power modules for electric vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...