NAND Flash (TLC, QLC, PLC) Market Insights

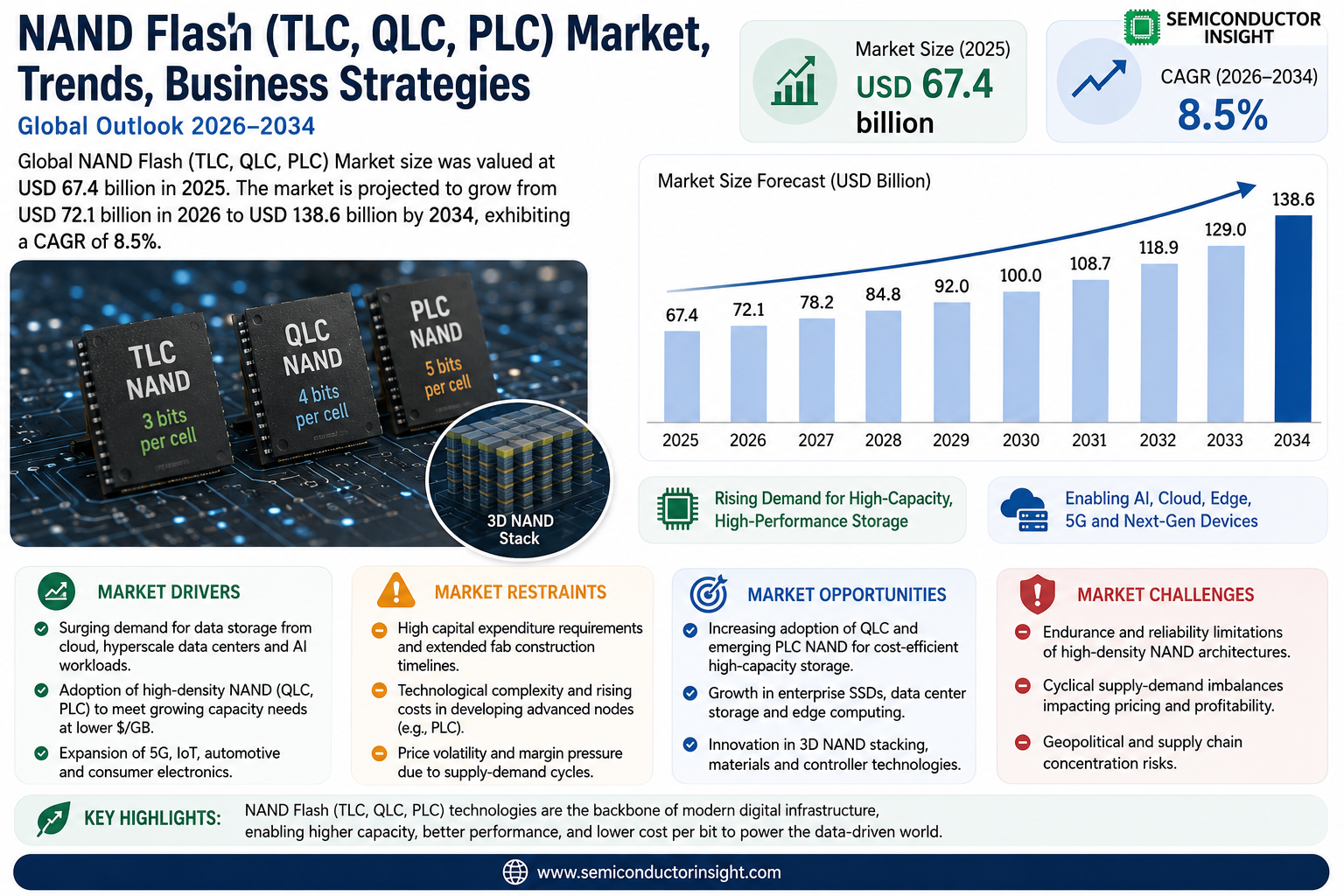

Global NAND Flash (TLC, QLC, PLC) Market size was valued at USD 67.4 billion in 2025. The market is projected to grow from USD 72.1 billion in 2026 to USD 138.6 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period.

NAND Flash memory is a non-volatile storage technology widely used across consumer electronics, data centers, automotive systems, and enterprise storage solutions. The market is broadly segmented by cell architecture, encompassing Triple-Level Cell (TLC), which stores three bits per cell and offers a balance between performance and cost; Quad-Level Cell (QLC), which stores four bits per cell and delivers higher storage density at lower cost; and the emerging Penta-Level Cell (PLC) technology, storing five bits per cell to further maximize capacity and reduce per-gigabyte pricing.

The market is witnessing robust growth driven by surging demand for high-capacity storage in hyperscale data centers, the rapid proliferation of AI workloads, and expanding adoption of solid-state drives (SSDs) in both consumer and enterprise segments. Furthermore, the continued transition from HDD to NAND-based storage solutions is accelerating market expansion. Key industry participants shaping this landscape include Samsung Electronics, SK Hynix, Kioxia Corporation, Western Digital, Micron Technology, and Intel Corporation, all of which maintain significant manufacturing and technology development capabilities across TLC, QLC, and next-generation PLC architectures.

MARKET DRIVERS

Surging Demand for High-Density Storage in Consumer and Enterprise Applications

NAND Flash (TLC, QLC, PLC) Market is experiencing robust growth, primarily driven by the exponential increase in data generation across consumer electronics, enterprise data centers, and cloud computing infrastructure. Triple-Level Cell (TLC) NAND remains the dominant technology in solid-state drives (SSDs) due to its optimal balance between cost, performance, and endurance. As smartphone manufacturers, laptop OEMs, and hyperscale cloud providers continue to scale their storage requirements, demand for high-density NAND Flash solutions has intensified considerably, underpinning sustained investment across the supply chain.

Proliferation of AI Workloads and Data-Intensive Computing Architectures

Artificial intelligence, machine learning, and large language model (LLM) deployments have dramatically increased the volume of data that must be stored, retrieved, and processed at high speeds. This trend is a significant structural driver for NAND Flash (TLC, QLC, PLC) Market, as enterprise SSDs based on TLC and QLC (Quad-Level Cell) NAND are increasingly deployed in AI training clusters and inference servers. QLC NAND, which stores four bits per cell, offers superior storage density at a lower cost per gigabyte, making it an attractive solution for read-intensive AI and analytics workloads where write endurance requirements are relatively moderate.

➤ The global transition toward AI-optimized data center infrastructure is expected to remain one of the most consequential long-term demand drivers for high-density NAND Flash technologies, including emerging PLC (Penta-Level Cell) architectures currently under active development by leading semiconductor manufacturers.

Beyond enterprise applications, the consumer electronics sector continues to provide a high-volume demand base for TLC and QLC NAND Flash. The ongoing replacement cycle for NAND-based SSDs in personal computing, gaming consoles, and mobile devices — combined with the gradual phase-out of traditional hard disk drives in mainstream laptops — reinforces consistent demand momentum. Falling average selling prices (ASPs) per gigabyte are further accelerating adoption across price-sensitive market segments, broadening the overall addressable market for NAND Flash (TLC, QLC, PLC) solutions globally.

MARKET CHALLENGES

Endurance and Reliability Limitations of High-Density NAND Architectures

One of the most persistent technical challenges facing NAND Flash (TLC, QLC, PLC) Market is the inverse relationship between storage density and endurance. As cell architectures progress from TLC to QLC and toward PLC configurations, the number of program/erase (P/E) cycles a cell can reliably sustain decreases significantly. QLC NAND typically supports fewer P/E cycles than TLC NAND, requiring sophisticated error correction code (ECC) engines, wear-leveling algorithms, and over-provisioning strategies to maintain data integrity over the product lifecycle. For write-intensive enterprise use cases such as online transaction processing (OLTP) and real-time analytics, these endurance constraints can limit the suitability of QLC and emerging PLC technologies without additional engineering overhead.

Other Challenges

Cyclical Supply-Demand Imbalances

The NAND Flash industry has historically been susceptible to pronounced boom-and-bust pricing cycles driven by capacity additions from major manufacturers including Samsung, SK Hynix, Micron, Kioxia, and Western Digital. Periods of oversupply can compress margins significantly across the value chain, creating financial pressure on both manufacturers and module suppliers. Managing inventory levels and capital expenditure timing in alignment with demand signals remains a critical operational challenge for all participants NAND Flash (TLC, QLC, PLC) Market.

Geopolitical and Supply Chain Concentration Risks

A significant proportion of global NAND Flash manufacturing capacity is concentrated in a small number of geographies, particularly South Korea, Japan, and the United States. Trade policy uncertainty, export control regulations, and potential disruptions to advanced semiconductor equipment supply represent material risks to production continuity. These concentration risks have prompted governments in multiple regions to incentivize domestic semiconductor manufacturing investment, though the capital intensity of NAND Flash fabrication means meaningful capacity diversification will take years to materialize.

MARKET RESTRAINTS

High Capital Expenditure Requirements and Extended Fab Construction Timelines

NAND Flash (TLC, QLC, PLC) Market faces a structural restraint in the form of exceptionally high capital requirements associated with building and equipping advanced NAND Flash fabrication facilities. State-of-the-art 3D NAND fabs capable of producing 200-plus layer stacked architectures require multi-billion-dollar investments and construction timelines spanning several years. This capital intensity creates significant barriers to entry, concentrating production among a handful of established players and limiting the speed at which new capacity can respond to demand shifts. For smaller or newer entrants, accessing the leading-edge process nodes necessary for competitive TLC, QLC, and PLC NAND production is practically prohibitive without substantial government support or strategic partnerships.

Increasing Physical and Engineering Complexity of Advanced 3D NAND Stacking

As NAND Flash manufacturers push toward higher layer counts to improve density and reduce cost per bit, the engineering challenges associated with 3D NAND fabrication have intensified. Achieving reliable cell-to-cell interference management, maintaining consistent etch depth uniformity across hundreds of layers, and ensuring adequate read/write performance in ultra-high-density QLC and PLC structures demand increasingly sophisticated process control and materials innovation. These technical complexities translate into longer development cycles, higher yield risk during technology transitions, and elevated research and development expenditure — all of which can restrain the pace of commercialization for next-generation NAND Flash architectures and weigh on near-term profitability within the broader NAND Flash (TLC, QLC, PLC) Market.

MARKET OPPORTUNITIES

Expansion of QLC and PLC NAND in Hyperscale and Cold Storage Applications

A compelling growth opportunity withNAND Flash (TLC, QLC, PLC) Market lies in the accelerating adoption of QLC NAND for hyperscale data center cold and warm storage tiers, where high capacity density and low cost per terabyte take precedence over write endurance. Major cloud providers actively evaluating QLC-based SSDs as replacements for nearline hard disk drives in archival and backup applications represent a substantial incremental demand pool. PLC NAND, currently in advanced research and early development stages, is expected to further extend this opportunity by delivering even higher bit density per cell, potentially enabling cost structures that make all-flash storage economically viable across a broader range of enterprise workload categories.

Automotive, Industrial IoT, and Edge Computing as Emerging Demand Verticals

Beyond traditional consumer and enterprise end markets, NAND Flash (TLC, QLC, PLC) Market stands to benefit from structural demand growth in automotive electronics, industrial IoT deployments, and edge computing infrastructure. Modern vehicles equipped with advanced driver-assistance systems (ADAS) and in-vehicle infotainment platforms require high-reliability, high-capacity NAND Flash storage capable of operating across wide temperature ranges and harsh environmental conditions. Similarly, the proliferation of intelligent edge nodes for manufacturing automation, smart city infrastructure, and telecommunications (including 5G base station deployments) is creating incremental demand for ruggedized TLC NAND solutions. These verticals offer higher average selling prices and more stable demand profiles compared to commodity consumer markets, providing NAND Flash manufacturers with an opportunity to diversify revenue streams and improve overall portfolio margin mix withNAND Flash (TLC, QLC, PLC) Market.

Trends

Accelerating Transition from HDD to NAND-Based Storage Solutions

NAND Flash (TLC, QLC, PLC) Market is experiencing a sustained and structural shift as enterprises and consumers progressively abandon traditional hard disk drives in favor of NAND-based solid-state storage. This transition is being propelled by the superior read/write speeds, lower power consumption, and compact form factors inherent to NAND Flash architectures. Triple-Level Cell (TLC) technology, which stores three bits per cell, continues to serve as the dominant choice for enterprise SSDs owing to its balanced performance and endurance characteristics. Meanwhile, the growing adoption of SSDs in laptops, gaming consoles, and embedded computing devices is reinforcing demand across TLC-based product lines, as manufacturers scale production to meet evolving consumer expectations for faster and more reliable storage.

Other Trends

Rising Adoption of QLC Architecture in Hyperscale Data Centers

Quad-Level Cell (QLC) NAND Flash is gaining significant traction within hyperscale data center environments, where storage density and cost efficiency are critical priorities. By storing four bits per cell, QLC architecture enables operators to achieve substantially higher capacity per physical footprint compared to TLC-based solutions. Leading hyperscale cloud providers are increasingly integrating QLC-based SSDs into read-intensive and warm storage workloads, where access frequency is moderate and the endurance limitations of QLC are manageable. This trend is further supported by the rapid expansion of AI and machine learning workloads, which generate enormous volumes of data requiring cost-effective, high-capacity storage infrastructure. Major manufacturers including Samsung Electronics, SK Hynix, Micron Technology, and Kioxia Corporation have expanded their QLC product portfolios to address this growing demand.

Emergence of PLC Technology as the Next Frontier in NAND Density

Penta-Level Cell (PLC) NAND Flash, capable of storing five bits per cell, represents the next significant architectural advancement NAND Flash (TLC, QLC, PLC) Market. PLC technology is positioned to deliver even lower per-gigabyte costs and higher storage densities compared to QLC, making it particularly attractive for cold storage and archival applications where write endurance is less critical. While PLC remains in early-stage development and commercialization, leading industry participants including Western Digital and Kioxia Corporation have publicly acknowledged ongoing research and development efforts in this domain, signaling its growing strategic importance.

AI Workload Expansion Driving Demand Across All NAND Cell Architectures

The rapid proliferation of artificial intelligence applications is emerging as a transformative demand driver across NAND Flash (TLC, QLC, PLC) Market. AI model training and inference processes require high-throughput, low-latency storage systems capable of managing large datasets efficiently. This is reinforcing demand for both TLC-based SSDs in performance-sensitive applications and QLC-based solutions in capacity-optimized deployments. As AI infrastructure continues to scale globally, all three cell architectures — TLC, QLC, and the emerging PLC — are expected to play complementary roles in meeting diverse storage performance and cost requirements across enterprise and cloud environments.

COMPETITIVE LANDSCAPE

Key Industry Players

NAND Flash (TLC, QLC, PLC) Market: Competitive Dynamics and Leading Manufacturers

Global NAND Flash (TLC, QLC, PLC) Market is highly consolidated, with a small number of vertically integrated manufacturers commanding the majority of worldwide production capacity and technological development. Samsung Electronics leads the competitive landscape, leveraging its advanced V-NAND (Vertical NAND) architecture and extensive R&D investment to maintain its dominant market position across TLC, QLC, and emerging PLC cell architectures. SK Hynix and Kioxia Corporation are equally prominent, with both companies aggressively expanding their 3D NAND layer counts to deliver higher storage densities and improved cost-per-gigabyte metrics. Micron Technology and Western Digital continue to invest heavily in next-generation QLC and PLC NAND solutions, targeting hyperscale data centers and enterprise SSD applications where storage density and total cost of ownership are critical procurement drivers. The competitive intensity in this market is further amplified by the rapid adoption of AI workloads and the accelerating transition from HDD to NAND-based solid-state storage, compelling all major players to accelerate technology roadmaps and scale manufacturing output to meet surging global demand.

Beyond the tier-one integrated device manufacturers, several significant niche and downstream players contribute meaningfully to the NAND Flash competitive ecosystem. Intel Corporation, though having divested its NAND business unit to SK Hynix, retains relevance through its Optane and enterprise SSD product lines, while companies such as Solidigm (the entity formed from Intel’s NAND acquisition) have emerged as notable standalone competitors in the enterprise and data center SSD segments. SanDisk, operating as a Western Digital brand, commands a substantial share of the consumer and prosumer SSD markets utilizing TLC and QLC NAND. Additionally, companies including Yangtze Memory Technologies Co. (YMTC) have rapidly expanded their global footprint, offering competitive TLC NAND products and investing in advanced 3D NAND stacking technologies. Downstream SSD and storage solution providers such as Kingston Technology, Seagate Technology, and Pure Storage further shape competitive dynamics by sourcing NAND from primary manufacturers and delivering differentiated storage platforms to enterprise, cloud, and consumer end markets.

List of Key NAND Flash Companies Profiled

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Kioxia Corporation

- Micron Technology, Inc.

- Western Digital Corporation

- Solidigm (formerly Intel NAND Solutions Group)

- Intel Corporation

- SanDisk (a Western Digital brand)

- Yangtze Memory Technologies Co., Ltd. (YMTC)

- Kingston Technology Company, Inc.

- Seagate Technology Holdings plc

- Pure Storage, Inc.

- Phison Electronics Corporation

- Silicon Motion Technology Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Triple-Level Cell (TLC) holds the leading position in the NAND Flash market, owing to its well-established maturity and the favorable equilibrium it strikes between performance, endurance, and cost-effectiveness.

|

| By Application |

|

Solid-State Drives (SSDs) dominate the application landscape for NAND Flash memory, driven by the accelerating global transition away from traditional hard disk drives toward faster, more energy-efficient, and compact storage solutions.

|

| By End User |

|

Data Centers & Cloud Providers represent the most influential end-user segment in the NAND Flash market, as the global proliferation of AI workloads and cloud-native applications continues to place extraordinary pressure on storage infrastructure.

|

| By Interface Technology |

|

NVMe (Non-Volatile Memory Express) has emerged as the dominant interface standard for NAND Flash-based storage, fundamentally transforming how data is accessed and transferred across both enterprise and consumer environments.

|

| By Layer Architecture |

|

3D NAND (128 Layers and Above) leads the layer architecture segment and is widely regarded as the cornerstone of modern NAND Flash development, enabling manufacturers to achieve unprecedented storage densities on a compact physical footprint.

|

Regional Analysis: NAND Flash (TLC, QLC, PLC) Market

Asia-Pacific

Asia-Pacific hosts the majority of the world’s NAND Flash fabrication facilities, with South Korea and Taiwan operating at the cutting edge of TLC and QLC node shrinks. The region’s deeply integrated supplier networks — encompassing photolithography equipment, specialty chemicals, and advanced packaging — provide a structural cost and speed-to-market advantage that competing regions are unable to replicate in the near term.

The region’s massive consumer base for smartphones, laptops, and tablets continues to drive robust TLC NAND Flash absorption. Simultaneously, hyperscale data center expansions across China, India, and Southeast Asia are accelerating the adoption of QLC NAND for high-capacity, cost-sensitive storage workloads, positioning Asia-Pacific as both the primary producer and largest consumer of NAND Flash globally.

Strategic national policies in China, India, Japan, and South Korea are actively channeling capital into domestic semiconductor ecosystems. Subsidies, tax incentives, and state-funded research programs are accelerating indigenous NAND Flash development, particularly for advanced QLC and emerging PLC technologies. These policy tailwinds are expected to deepen regional self-reliance and expand production capacity significantly through the forecast period.

The rapid rollout of 5G infrastructure, AI edge computing, and smart city projects across Asia-Pacific is generating fresh demand vectors for high-density NAND Flash storage. Industrial IoT deployments in manufacturing hubs and automotive electronics growth in Japan and South Korea are further broadening the addressable market for TLC and QLC NAND Flash variants beyond traditional consumer segments.

North America

North America represents a critically important market within the global NAND Flash (TLC, QLC, PLC) landscape, underpinned by its world-leading hyperscale cloud infrastructure, robust enterprise storage sector, and advanced defense and aerospace applications. The United States is home to dominant cloud service providers whose massive data center expansion programs are among the most significant drivers of QLC NAND Flash adoption globally. The region’s advanced technology ecosystem, encompassing semiconductor design firms, system integrators, and storage solution providers, ensures sustained demand for high-performance TLC NAND in enterprise SSDs and next-generation computing platforms. Additionally, domestic policy efforts aimed at reshoring semiconductor manufacturing are beginning to attract fabrication investments, though North America’s primary strength remains in NAND Flash design, ecosystem development, and end-market consumption rather than volume production. Increasing interest in PLC NAND Flash for archival and cold storage use cases further differentiates North America’s demand profile through 2034.

Europe

Europe occupies a strategically significant position NAND Flash (TLC, QLC, PLC) Market, characterized by strong industrial, automotive, and enterprise storage demand rather than mass consumer electronics consumption. Germany, the Netherlands, and France lead regional demand, driven by advanced manufacturing, smart factory deployments, and automotive-grade storage requirements where TLC NAND Flash reliability standards are particularly stringent. Europe’s commitment to digital sovereignty is catalyzing investment in regional data center infrastructure, creating expanding demand for QLC NAND in scalable, energy-efficient storage architectures. The European Chips Act is further stimulating semiconductor investment within the region, with long-term implications for NAND Flash supply chain resilience. Regulatory frameworks emphasizing data security, sustainability, and circular economy principles are also influencing product specifications and procurement strategies across European enterprise and public sector buyers of NAND Flash solutions.

South America

South America remains an emerging but progressively relevant participant in Global NAND Flash (TLC, QLC, PLC) Market. Brazil anchors regional demand, supported by a growing consumer electronics market, expanding internet penetration, and nascent cloud infrastructure development. While the region currently relies heavily on imports of TLC and QLC NAND Flash-based products, increasing smartphone adoption and digital transformation initiatives across sectors such as financial services, retail, and government are steadily expanding the addressable market. Logistical challenges, import tariffs, and currency volatility present ongoing barriers to more rapid market penetration; however, regional e-commerce growth and the gradual buildout of local data center capacity by global hyperscalers signal improving long-term prospects for NAND Flash consumption across South America through the forecast horizon.

Middle East & Africa

The Middle East & Africa region is emerging as a noteworthy growth frontier for NAND Flash (TLC, QLC, PLC) Market, driven by ambitious digital infrastructure programs, sovereign cloud initiatives, and rising consumer technology adoption. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing heavily in hyperscale data centers and smart city infrastructure, creating meaningful demand for QLC NAND Flash in high-density storage deployments. Africa’s rapidly expanding mobile-first internet user base is generating incremental demand for TLC NAND Flash within affordable smartphone and entry-level computing segments. While the region currently accounts for a smaller share of global NAND Flash consumption, accelerating digitalization programs, improving telecommunications infrastructure, and growing interest in AI and cloud computing position the Middle East & Africa as a steadily expanding market through 2034.

Report Scope

This market research report provides a comprehensive analysis of the NAND Flash (TLC, QLC, PLC) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of NAND Flash (TLC, QLC, PLC) Market?

-> NAND Flash (TLC, QLC, PLC) Market was valued at USD 67.4 billion in 2025 and is expected to reach USD 138.6 billion by 2034, growing at a CAGR of 8.5% during the forecast period from 2026 to 2034.

Which key companies operate NAND Flash (TLC, QLC, PLC) Market?

-> Key players include Samsung Electronics, SK Hynix, Kioxia Corporation, Western Digital, Micron Technology, and Intel Corporation, among others, all of which maintain significant manufacturing and technology development capabilities across TLC, QLC, and next-generation PLC architectures.

What are the key growth drivers?

-> Key growth drivers include surging demand for high-capacity storage in hyperscale data centers, the rapid proliferation of AI workloads, expanding adoption of solid-state drives (SSDs) in both consumer and enterprise segments, and the continued transition from HDD to NAND-based storage solutions.

Which region dominates the market?

-> Asia-Pacific is a leading region in the NAND Flash market, driven by major manufacturing hubs and key industry participants, while North America remains a significant market supported by hyperscale data center investments and enterprise storage demand.

What are the emerging trends?

-> Emerging trends include the advancement of Penta-Level Cell (PLC) technology storing five bits per cell to maximize capacity and reduce per-gigabyte pricing, growing adoption of QLC NAND for higher storage density at lower cost, and the rapid integration of NAND Flash solutions into AI infrastructure, automotive systems, and enterprise SSD deployments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...