Mobile DRAM (LPDDR5X, LPDDR6) Market Insights

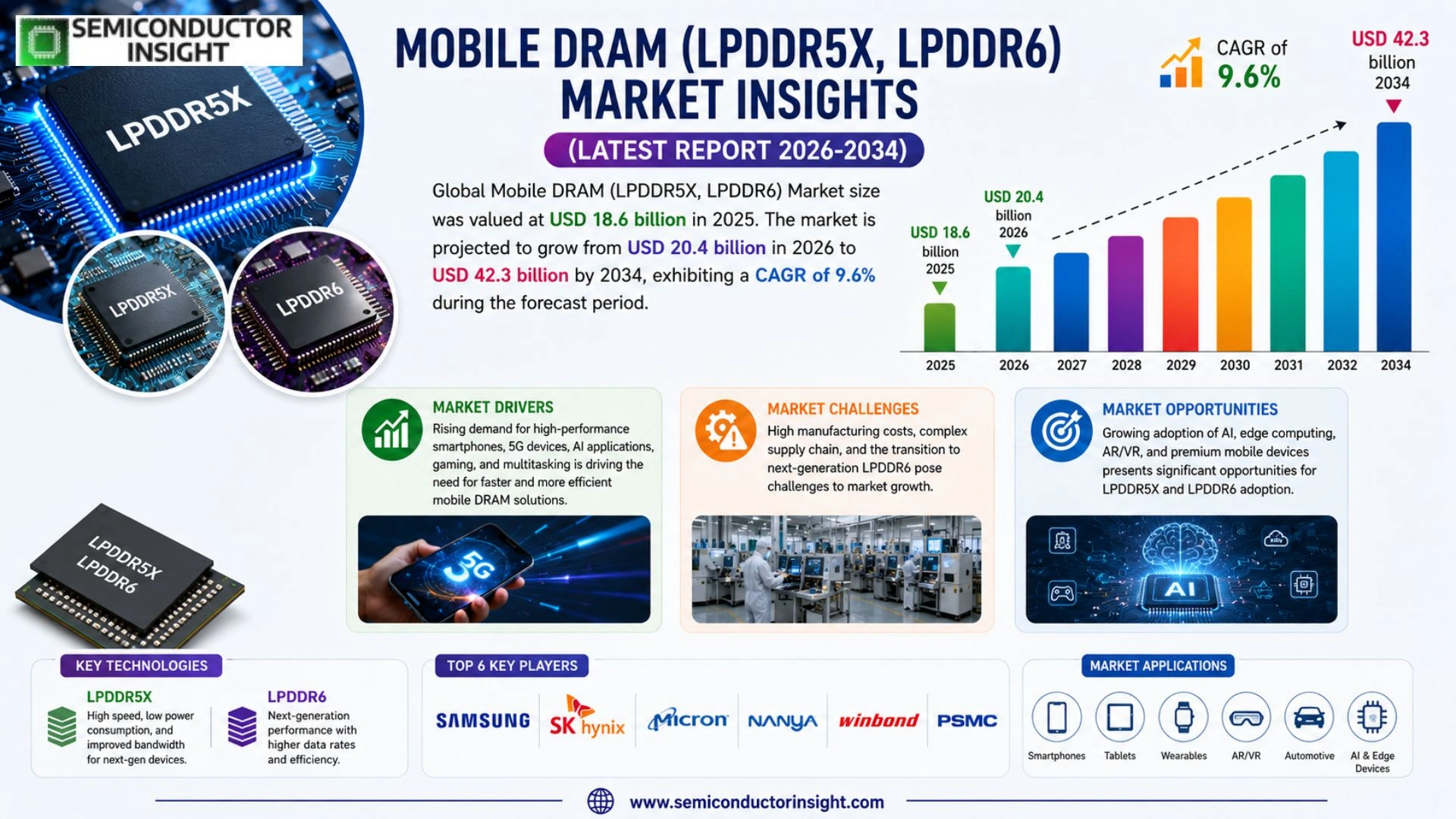

Global Mobile DRAM (LPDDR5X, LPDDR6) Market size was valued at USD 18.6 billion in 2025. The market is projected to grow from USD 20.4 billion in 2026 to USD 42.3 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period.

Mobile DRAM, particularly LPDDR5X and the emerging LPDDR6 variants, consists of low-power, high-speed memory solutions optimized for battery-powered devices. These specialized DRAM chips deliver exceptional performance while maintaining energy efficiency, making them essential for modern smartphones, tablets, wearables, and automotive infotainment systems. LPDDR5X offers enhanced speeds and efficiency over previous generations, while LPDDR6 introduces further advancements in bandwidth and power management to support demanding applications like on-device AI processing.

The market is experiencing robust growth due to several factors, including the rapid proliferation of 5G-enabled smartphones, increasing integration of artificial intelligence features in mobile devices, and the rising demand for higher memory capacities to handle complex multitasking and multimedia applications. Furthermore, advancements in automotive electronics and the expansion of edge computing contribute significantly to market expansion. Key industry players are actively investing in next-generation technologies, with major manufacturers introducing LPDDR6 solutions that provide up to 33% faster performance and improved power efficiency compared to LPDDR5X. Samsung, SK Hynix, and Micron are leading the development and commercialization of these advanced memory solutions, driving innovation across the ecosystem with a strong focus on high-density, low-power architectures.

MARKET DRIVERS

Surging Demand for On-Device AI in Premium Smartphones

Mobile DRAM (LPDDR5X, LPDDR6) Market is propelled by the rapid integration of generative AI and advanced neural processing capabilities in flagship and mid-tier smartphones. LPDDR5X and emerging LPDDR6 solutions deliver the high bandwidth and power efficiency required for real-time AI inference, computational photography, and multitasking, with data rates exceeding 9.6 Gbps and significant improvements over prior generations.

Transition to 5G-Advanced and Higher Memory Capacities

Global rollout of 5G networks and the push toward higher-resolution displays, gaming, and multimedia applications continue to drive per-device memory content upward. Manufacturers are shifting from LPDDR4X to LPDDR5X, with average capacities in premium devices rising notably as OEMs standardize on these technologies for enhanced performance and future-proofing.

➤ LPDDR6 offers up to 33% higher performance and over 20% better power efficiency compared to LPDDR5X, enabling new use cases in mobile AI platforms.

Strong growth in emerging markets, combined with premiumization trends among major brands, supports sustained expansion of the Mobile DRAM (LPDDR5X, LPDDR6) segment through the late 2020s.

MARKET CHALLENGES

Sharp Price Increases and Supply Tightness

Mobile DRAM prices have experienced significant quarter-over-quarter surges, with LPDDR5X contracts reflecting strong upward pressure due to capacity reallocation toward higher-margin AI applications. This volatility challenges handset manufacturers in managing bill-of-materials costs while maintaining competitive pricing.

Other Challenges

Production Transition Complexities

Many mid-range chipsets remain optimized for earlier standards, slowing full ecosystem adoption of LPDDR5X and LPDDR6 while suppliers reduce output of legacy LPDDR4X solutions.

Geopolitical and Supply Chain Risks

Ongoing trade tensions and regional disruptions impact raw material availability and global logistics, adding uncertainty to capacity planning for Mobile DRAM (LPDDR5X, LPDDR6) production.

MARKET RESTRAINTS

High Development Costs and Qualification Barriers

Advancing to LPDDR6 involves substantial R&D investment and lengthy qualification processes, particularly for automotive-grade and high-reliability applications. These technical and financial hurdles slow broader market penetration beyond premium consumer devices.

Capacity Allocation Toward AI Infrastructure

Major suppliers prioritize production of high-bandwidth memory for data centers, constraining wafer availability for mobile LPDDR solutions and contributing to extended lead times and elevated pricing Mobile DRAM (LPDDR5X, LPDDR6) Market.

MARKET OPPORTUNITIES

Expansion into AI PCs, Automotive, and Edge Devices

LPDDR5X and LPDDR6 technologies are increasingly adopted beyond traditional smartphones into AI-enabled laptops, automotive ADAS systems, and industrial edge computing platforms. This diversification presents substantial growth avenues as power-efficient, high-bandwidth memory becomes critical across multiple sectors.

Next-Generation Standardization and Higher Density Solutions

The JEDEC LPDDR6 standard unlocks new performance levels, supporting greater memory densities and efficiency modes. Continued innovation in process nodes by leading suppliers positions Mobile DRAM (LPDDR5X, LPDDR6) Market for robust long-term expansion aligned with evolving AI and connectivity demands.

Trends

Transition to LPDDR6 for AI-Enabled Mobile Devices

Mobile DRAM (LPDDR5X, LPDDR6) Market continues to evolve rapidly as manufacturers prioritize higher bandwidth and superior power efficiency to support advanced applications. LPDDR6 introduces significant improvements over LPDDR5X, delivering enhanced performance while maintaining the low-power characteristics essential for battery-operated devices. These memory solutions play a critical role in enabling seamless operation of modern smartphones, tablets, and wearables where energy efficiency directly impacts user experience.

Other Trends

Rising Demand Driven by 5G and AI Integration

The proliferation of 5G-enabled smartphones has accelerated the need for faster memory architectures capable of handling increased data throughput and complex multitasking. Integration of artificial intelligence features in mobile devices further drives adoption of LPDDR5X and LPDDR6 solutions, which provide the necessary speed and efficiency for on-device AI processing. Higher memory capacities are becoming standard to support multimedia applications and sophisticated software environments.

Expansion into Automotive and Edge Computing Applications

Beyond consumer electronics, Mobile DRAM (LPDDR5X, LPDDR6) technologies are gaining traction in automotive infotainment systems and edge computing deployments. These sectors require reliable, high-performance memory that operates efficiently under varying power constraints, creating new growth avenues for specialized DRAM solutions optimized for such environments.

Industry Leadership and Technological Innovation

Major manufacturers are actively advancing next-generation memory solutions with a focus on high-density, low-power architectures. Samsung, SK Hynix, and Micron lead development efforts, introducing LPDDR6 variants that offer improved bandwidth and power management compared to previous generations. Their innovations emphasize performance gains while addressing the critical need for energy conservation in portable devices. The competitive landscape encourages continuous refinement of these technologies to meet evolving requirements across smartphones, tablets, and emerging device categories. As applications become more demanding, Mobile DRAM (LPDDR5X, LPDDR6) Market trends reflect a clear industry shift toward memory solutions that balance speed, efficiency, and reliability for sustained market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Oligopolistic Market Led by Technological Innovators in Advanced LPDDR Solutions

The Mobile DRAM market for LPDDR5X and LPDDR6 is highly concentrated, with Samsung Electronics, SK Hynix, and Micron Technology collectively commanding the vast majority of global production capacity. These leaders drive innovation in high-speed, low-power memory architectures essential for premium smartphones, AI-enabled devices, and automotive applications. Samsung maintains strong leadership through rapid commercialization of LPDDR6 solutions offering superior bandwidth and power efficiency, while SK Hynix and Micron compete aggressively on process technology advancements and strategic design wins with major device OEMs.

While the top three dominate the high-performance segments, niche players contribute to supply chain diversity in specialty and lower-density variants. Companies such as Nanya Technology and Winbond Electronics focus on targeted applications in IoT, industrial, and automotive sectors, providing complementary solutions. Emerging challengers, including ChangXin Memory Technologies (CXMT), are gradually expanding capabilities in mobile DRAM, though they currently hold limited market share compared to the established leaders.

List of Key Mobile DRAM Companies Profiled

- Samsung Electronics

- SK Hynix

- Micron Technology

- Nanya Technology Corporation

- Winbond Electronics Corporation

- ChangXin Memory Technologies (CXMT)

- Powerchip Technology Corporation

- Etron Technology

- BIWIN

- Kingston Technology

- Kioxia Corporation

- Western Digital Corporation

- Infineon Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

LPDDR6 represents the cutting-edge evolution in mobile DRAM technology, delivering superior bandwidth and enhanced power management capabilities essential for next-generation mobile experiences. It excels in supporting intensive on-device AI processing and complex multitasking scenarios while optimizing battery life. Manufacturers prioritize this variant for flagship devices where performance demands continue to escalate. Key advantages include improved data transfer rates and architectural refinements that enable seamless integration with advanced processors. |

| By Application |

|

Smartphones dominate as the primary application segment due to the relentless push for higher resolution displays, sophisticated camera systems, and real-time AI features. These devices require memory solutions that balance high-speed performance with exceptional energy efficiency to support extended usage. LPDDR5X and LPDDR6 enable fluid gaming experiences, seamless 5G connectivity, and advanced photography capabilities. The segment benefits from continuous innovation cycles that align memory advancements with processor roadmaps for premium user experiences. |

| By End User |

|

Consumer Electronics stands out as the leading end-user segment, fueled by widespread adoption of smart devices that demand efficient, high-performance memory. This category encompasses a broad range of battery-powered products where low power consumption directly translates to better user satisfaction and device competitiveness. Innovations in LPDDR technologies allow for richer multimedia consumption and more responsive interfaces. The segment continues to evolve with emerging form factors and use cases that push the boundaries of memory capabilities. |

| By Density |

|

Ultra-High Density configurations are gaining prominence to accommodate the growing needs of data-intensive applications and multitasking environments. These solutions support expansive memory requirements in compact form factors without compromising on power efficiency. They play a crucial role in enabling advanced features such as on-device machine learning models and high-fidelity content creation. The focus remains on architectural optimizations that maximize capacity while minimizing thermal output and energy draw. |

| By Speed |

|

Ultra-High Speed variants lead the segment by providing the bandwidth necessary for future-proof mobile experiences. They facilitate rapid data handling required by emerging technologies including augmented reality and sophisticated AI workloads. These solutions ensure smooth performance during peak usage periods while maintaining thermal stability. Industry efforts concentrate on refining signal integrity and power delivery to sustain these elevated speeds in real-world operating conditions across diverse device ecosystems. |

Regional Analysis: Mobile DRAM (LPDDR5X, LPDDR6) Market

Asia-Pacific

Asia-Pacific hosts world-class research and development centers dedicated to Mobile DRAM advancements. Clusters in South Korea, Taiwan, and China foster breakthroughs in interface protocols and packaging technologies tailored for LPDDR5X and upcoming LPDDR6 generations, enabling seamless integration with cutting-edge application processors.

The region maintains sophisticated fabrication facilities optimized for high-volume production of power-efficient memory solutions. This vertical integration allows rapid scaling to support global smartphone brands while maintaining stringent quality standards required for premium mobile applications.

Close partnerships between memory suppliers, display manufacturers, and device assemblers create a vibrant ecosystem. This synergy drives holistic optimization of Mobile DRAM performance within complete mobile platforms, addressing thermal, power, and performance challenges holistically.

Strategic investments in next-generation facilities and talent development ensure Asia-Pacific remains at the forefront. Focus areas include enhanced data rates and AI-optimized memory architectures that will define competitive differentiation in the mobile sector through the forecast period.

North America

North America plays a vital role Mobile DRAM (LPDDR5X, LPDDR6) Market through its emphasis on design innovation and early adoption of advanced technologies. The region excels in developing software ecosystems and AI frameworks that leverage high-bandwidth memory for superior mobile experiences. Leading technology companies drive demand for premium specifications, influencing global product roadmaps. Strong intellectual property frameworks and research institutions contribute to breakthroughs in memory controller integration and system-level optimization. Consumer preference for high-end devices supports steady uptake of latest LPDDR solutions, while strategic partnerships with Asian manufacturers ensure supply chain alignment. The market dynamics here center on performance leadership rather than volume, with focus on specialized applications including professional productivity tools and immersive gaming platforms.

Europe

Europe demonstrates measured yet strategic growth Mobile DRAM (LPDDR5X, LPDDR6) Market, prioritizing energy efficiency and sustainability alongside performance. Regulatory emphasis on lower power consumption aligns perfectly with evolving LPDDR architectures that reduce thermal output in mobile devices. The region benefits from strong automotive and industrial crossovers, where mobile-derived memory technologies find applications in connected systems. Collaborative R&D initiatives across member states enhance capabilities in secure memory solutions critical for privacy-focused applications. While manufacturing presence remains selective, design and engineering expertise significantly influence product specifications. Market participants focus on differentiation through reliability and compliance, supporting premium segments where users value long-term device performance and environmental considerations.

South America

South America represents an emerging frontier for Mobile DRAM (LPDDR5X, LPDDR6) Market, characterized by expanding digital inclusion and rising smartphone penetration. Local demand increasingly shifts toward mid-to-premium devices incorporating advanced memory for better multitasking and media consumption. Infrastructure improvements and digital economy initiatives create favorable conditions for technology adoption. Regional players explore partnerships to localize assembly and customization, gradually building technical capabilities. Challenges related to economic variability exist, yet growing middle-class aspirations drive interest in devices featuring LPDDR5X and future LPDDR6 capabilities. The market evolves with focus on value-for-money propositions that deliver meaningful performance improvements accessible to broader consumer bases.

Middle East & Africa

The Middle East and Africa region shows promising potential Mobile DRAM (LPDDR5X, LPDDR6) Market fueled by youthful demographics and accelerating mobile-first digital transformation. Smart city projects and expanding connectivity infrastructure boost demand for capable devices suited for data-intensive applications. Several markets prioritize technology leapfrogging, favoring devices with modern memory solutions that support future-proof experiences. Investment in education and innovation hubs nurtures local talent while attracting global players seeking growth opportunities. The focus remains on balancing performance with affordability, making LPDDR advancements accessible across diverse economic contexts. Strategic distribution networks and localized content development further support adoption of advanced mobile memory technologies across the region.

Report Scope

This market research report provides a comprehensive analysis of the Mobile DRAM (LPDDR5X, LPDDR6) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Mobile DRAM (LPDDR5X, LPDDR6) Market?

-> Mobile DRAM (LPDDR5X, LPDDR6) Market was valued at USD 18.6 billion in 2025 and is expected to reach USD 42.3 billion by 2034.

Which key companies operate Mobile DRAM (LPDDR5X, LPDDR6) Market?

-> Key players include Samsung, SK Hynix, and Micron, among others.

What are the key growth drivers?

-> Key growth drivers include proliferation of 5G-enabled smartphones, AI integration in mobile devices, and rising demand for higher memory capacities.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Asia-Pacific remains a dominant market.

What are the emerging trends?

-> Emerging trends include LPDDR6 adoption, on-device AI processing, and low-power high-bandwidth architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...