MEMS Flow Sensor (Gas, Liquid) Market Insights

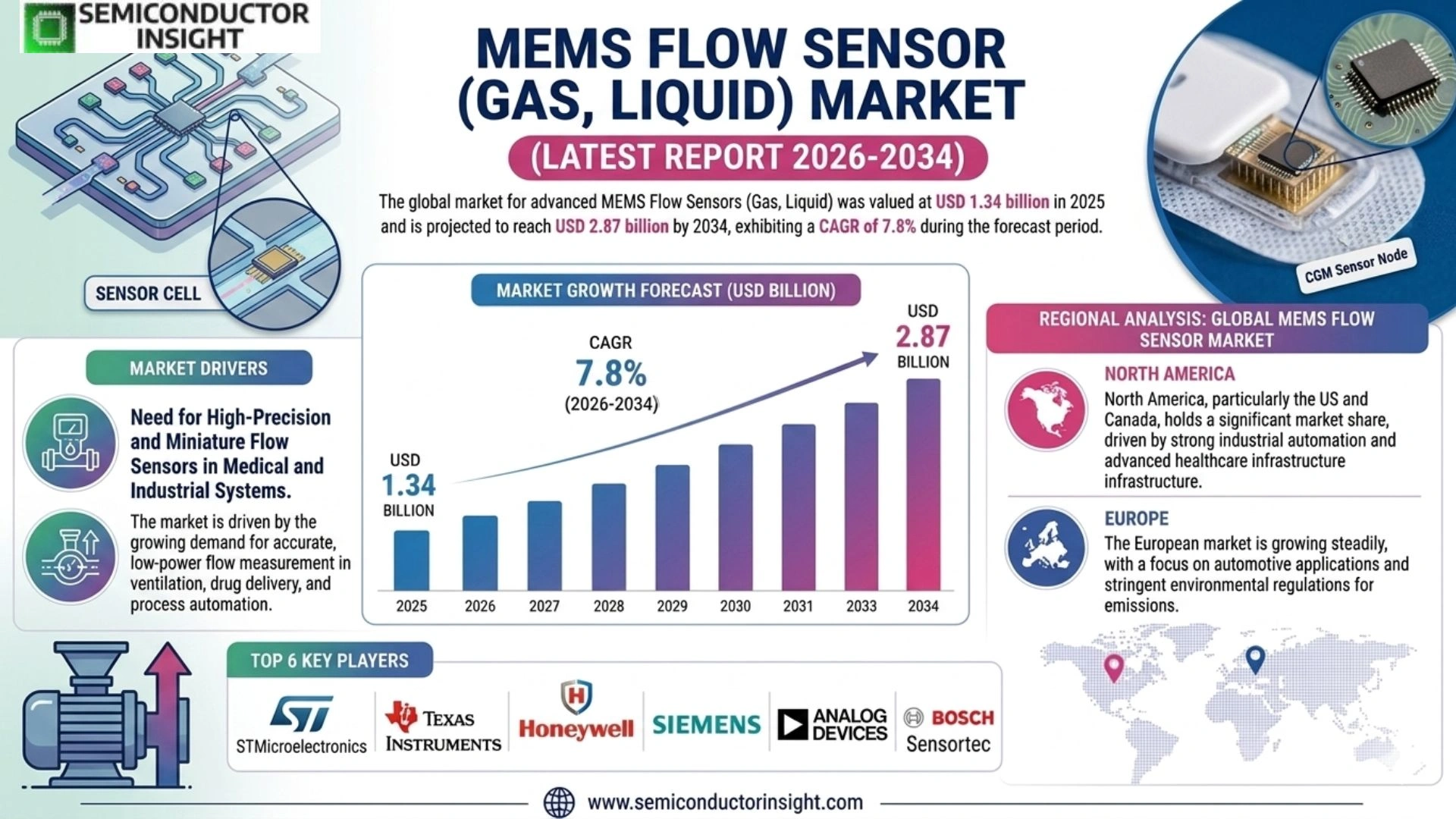

MEMS Flow Sensor (Gas, Liquid) Market size was valued at USD 1.34 billion in 2025. The market is projected to grow from USD 1.46 billion in 2026 to USD 2.87 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period.

MEMS (Micro-Electro-Mechanical Systems) flow sensors are miniaturized devices engineered to measure the flow rate of gases and liquids with high precision and minimal energy consumption. These sensors leverage semiconductor fabrication techniques to integrate mechanical and electronic components at the microscale, enabling accurate measurement across a wide range of fluid media. The product category encompasses thermal mass flow sensors, differential pressure-based sensors, ultrasonic MEMS flow sensors, and Coriolis-type MEMS sensors, serving applications across gas metering, medical devices, industrial process control, and automotive systems.

The market is gaining strong momentum driven by escalating demand for precise fluid management in healthcare, the rapid adoption of smart gas metering infrastructure, and the expanding use of MEMS-based sensors in automotive fuel and emission control systems. Furthermore, the proliferation of IoT-enabled industrial automation and the push toward miniaturized, low-power sensing solutions are reinforcing market expansion. Key industry participants such as Sensirion AG, Honeywell International Inc., ams-OSRAM AG, Siargo Ltd., and Omron Corporation continue to broaden their MEMS flow sensor portfolios, strengthening their global presence across both gas and liquid sensing segments.

MARKET DRIVERS

Rising Demand for Precision Flow Measurement in Industrial Automation

The MEMS flow sensor market for both gas and liquid applications is experiencing robust growth driven by the accelerating adoption of industrial automation and smart manufacturing practices globally. As industries increasingly transition toward Industry 4.0 frameworks, the need for highly accurate, miniaturized, and low-power flow sensing solutions has intensified. MEMS-based flow sensors offer distinct advantages over conventional flow measurement technologies, including reduced size, lower power consumption, faster response times, and enhanced integration capabilities with digital control systems. These attributes make them indispensable in process industries such as chemicals, pharmaceuticals, food and beverage, and oil and gas, where precise flow measurement of both gases and liquids is critical to operational efficiency and product quality.

Expanding Applications in Medical Devices and Healthcare Diagnostics

The healthcare sector represents one of the most significant growth drivers for MEMS Flow Sensor (Gas, Liquid) Market. Increasing global demand for portable medical devices, respiratory care equipment, and point-of-care diagnostic instruments has created sustained demand for miniaturized flow sensing components. MEMS gas flow sensors are widely deployed in ventilators, spirometers, anesthesia delivery systems, and oxygen concentrators, particularly following heightened awareness of respiratory health infrastructure post the COVID-19 pandemic. Similarly, MEMS liquid flow sensors are integral to infusion pumps, dialysis machines, and microfluidic lab-on-chip platforms. The global push for home-based healthcare and remote patient monitoring continues to amplify the need for compact, reliable, and energy-efficient MEMS flow sensing solutions.

➤ The integration of MEMS flow sensors with IoT-enabled platforms and wireless communication protocols is fundamentally reshaping how industries monitor and manage fluid and gas flow, enabling real-time data analytics, predictive maintenance, and significant reductions in operational downtime.

Government initiatives promoting energy efficiency and environmental sustainability are further propelling demand across the MEMS flow sensor market. In the energy sector, MEMS gas flow sensors are increasingly deployed in smart gas meters, HVAC systems, and combustion control applications to optimize fuel consumption and reduce emissions. Regulatory mandates across North America, Europe, and the Asia-Pacific region requiring accurate utility metering and emissions monitoring are compelling utility providers and industrial operators to upgrade legacy flow measurement infrastructure with advanced MEMS-based alternatives. This regulatory tailwind, combined with growing environmental consciousness among end-users, is expected to sustain demand growth through the forecast period.

MARKET CHALLENGES

Technical Complexity in Calibration and Long-Term Sensor Drift

Despite their technological advantages, MEMS flow sensors for gas and liquid applications face notable technical challenges that can hinder broader adoption. One of the primary concerns is sensor drift over extended operational periods, particularly in harsh or chemically aggressive environments. MEMS flow sensors based on thermal sensing principles can be susceptible to contamination, humidity variations, and particulate matter, which may affect measurement accuracy and long-term reliability. Ensuring consistent calibration across a sensor’s operational lifetime requires sophisticated compensation algorithms and periodic recalibration procedures, adding to the total cost of ownership for end-users, particularly in demanding industrial and medical applications where measurement precision is non-negotiable.

Other Challenges

High Development and Fabrication Costs

The fabrication of MEMS flow sensors involves highly specialized semiconductor manufacturing processes, including photolithography, etching, and wafer bonding, which demand significant capital investment and advanced cleanroom facilities. These elevated production costs can restrict market entry for smaller manufacturers and limit the ability of vendors to offer competitive pricing, particularly for high-volume commodity applications. While economies of scale are gradually improving cost dynamics, the initial engineering and tooling expenses associated with customized MEMS flow sensor designs for specific gas or liquid media remain a meaningful barrier for prospective adopters in cost-sensitive end markets.

Integration and Compatibility Constraints

Integrating MEMS flow sensors into existing industrial or medical systems can present engineering challenges related to interface compatibility, signal conditioning, and packaging requirements. Liquid flow sensing applications in particular demand robust fluidic sealing, chemical resistance, and biocompatibility for medical-grade deployments, which adds complexity to the sensor package design and validation process. Ensuring seamless compatibility with a wide range of fluid media , including corrosive chemicals, viscous liquids, and high-purity gases , requires extensive application-specific design customization, which can extend product development timelines and increase time-to-market for new entrants and established players alike.

MARKET RESTRAINTS

Competition from Alternative Flow Measurement Technologies

MEMS Flow Sensor (Gas, Liquid) Market faces persistent competitive pressure from established alternative flow measurement technologies, including ultrasonic flow meters, Coriolis mass flow meters, and electromagnetic flow sensors. In certain high-flow industrial applications, these conventional technologies offer advantages in terms of measurement range, robustness, and compatibility with a broader spectrum of process media. Large-scale oil and gas operations, for example, often favor Coriolis or ultrasonic flow meters for their proven track record and ability to handle extreme pressure and temperature conditions. This entrenched competition limits the rate of displacement of legacy technologies and can restrain the pace of adoption of MEMS-based alternatives in segments where switching costs and qualification requirements are high.

Supply Chain Vulnerabilities and Semiconductor Material Constraints

The MEMS flow sensor market is not immune to the broader supply chain disruptions that have affected the global semiconductor and microelectronics industry. Dependence on specialized substrate materials, including silicon wafers and precision thin-film deposition materials, exposes MEMS flow sensor manufacturers to supply chain vulnerabilities linked to geopolitical tensions, raw material shortages, and concentration of fabrication capacity in limited geographic regions. Lead time extensions and input cost inflation can adversely impact production schedules and margin profiles for sensor manufacturers, while also creating uncertainty for end-users planning large-scale deployments. These supply chain constraints represent a structural restraint that the industry must address through diversification of supplier bases and investments in regional manufacturing resilience.

Regulatory compliance and certification requirements also act as a restraint on market velocity, particularly for MEMS flow sensors deployed in safety-critical applications. Medical-grade liquid flow sensors, for instance, must comply with rigorous regulatory standards set by bodies such as the U.S. FDA and the European MDR framework, requiring extensive clinical validation, biocompatibility testing, and quality management system certification. Similarly, gas flow sensors used in hazardous area classifications must meet ATEX, IECEx, or equivalent explosion-proof standards. These compliance pathways are time-intensive and resource-demanding, effectively slowing the speed at which new MEMS flow sensing technologies can be commercialized and scaled across regulated end markets.

MARKET OPPORTUNITIES

Proliferation of Smart Gas Metering and Advanced Utility Infrastructure

The global rollout of smart city infrastructure and advanced metering initiatives presents a compelling growth opportunity for MEMS Flow Sensor (Gas, Liquid) Market. Governments and utility operators across Europe, North America, and Asia-Pacific are investing heavily in smart gas meter deployments as part of broader energy efficiency mandates and grid modernization programs. MEMS gas flow sensors are ideally suited for next-generation smart meters due to their compact form factor, ultra-low power consumption, and capability for direct digital output integration with AMI (Advanced Metering Infrastructure) networks. As billions of legacy mechanical meters are slated for replacement over the coming decade, MEMS-based sensor manufacturers are positioned to capture significant volume opportunities within this expanding infrastructure modernization wave.

Growth in Microfluidics and Lab-on-Chip Technologies for Life Sciences

Advances in microfluidics and the rapid commercialization of lab-on-chip platforms are creating high-value opportunities for MEMS liquid flow sensors in the life sciences and biotechnology sectors. Microfluidic systems used for genomic sequencing, drug discovery, cell analysis, and point-of-care diagnostics require precise nanoliter-to-microliter scale liquid flow control, which MEMS sensors are uniquely capable of delivering. The increasing adoption of microfluidic-based systems by pharmaceutical companies, academic research institutions, and clinical laboratories is generating sustained demand for highly integrated, low dead-volume MEMS flow sensing components. Partnerships between MEMS sensor manufacturers and microfluidic platform developers are expected to accelerate product innovation and open new revenue streams across the diagnostics and life sciences value chain.

The emergence of hydrogen as a clean energy carrier presents a forward-looking opportunity for the MEMS gas flow sensor market. As hydrogen production, distribution, and end-use applications scale globally in support of decarbonization goals, accurate and reliable measurement of hydrogen gas flow becomes critical across the entire value chain , from electrolyzers and hydrogen refueling stations to fuel cell vehicles and stationary power systems. MEMS flow sensors capable of accurately measuring low-density, highly diffusive hydrogen gas while maintaining intrinsic safety and compact packaging are increasingly viewed as enabling components for the hydrogen economy. Early-mover investments in hydrogen-compatible MEMS flow sensing technologies are expected to yield significant competitive advantages as the hydrogen infrastructure market matures through the latter half of this decade.

Trends

Rising Demand for Precision Fluid Management in Healthcare Driving MEMS Flow Sensor Adoption

MEMS Flow Sensor (Gas, Liquid) Market is experiencing significant momentum driven by escalating demand for precise fluid management in the healthcare sector. MEMS-based flow sensors are increasingly integrated into medical devices such as respiratory equipment, infusion pumps, and anesthesia delivery systems, where accurate measurement of gas and liquid flow rates is critical for patient safety. The miniaturized form factor and low power consumption of MEMS flow sensors make them particularly well-suited for portable and wearable medical applications, a segment that continues to expand as healthcare providers prioritize patient-centric monitoring solutions. This trend is reinforcing the strategic importance of MEMS flow sensor technology across both developed and emerging healthcare markets globally.

Other Trends

Smart Gas Metering Infrastructure Expansion

The rapid adoption of smart gas metering infrastructure across residential, commercial, and industrial sectors is emerging as a pivotal trend withMEMS Flow Sensor (Gas, Liquid) Market. Governments and utility providers worldwide are accelerating the rollout of advanced metering infrastructure programs, creating substantial demand for high-precision, low-power MEMS gas flow sensors. These sensors enable real-time consumption monitoring, leak detection, and remote data transmission, aligning with broader smart city and energy efficiency initiatives. Key industry participants such as Sensirion AG, Honeywell International Inc., and Omron Corporation are actively expanding their MEMS flow sensor portfolios to address the growing requirements of smart gas metering deployments.

IoT-Enabled Industrial Automation and Process Control

The proliferation of IoT-enabled industrial automation is creating robust demand for MEMS flow sensors in process control applications. Industries including chemicals, food and beverage, and semiconductor manufacturing are integrating MEMS-based thermal mass flow sensors and differential pressure sensors to achieve tighter process tolerances and reduce operational waste. The ability of MEMS flow sensors to deliver accurate, real-time flow data with minimal footprint and energy consumption positions them as preferred sensing solutions within connected industrial environments. Companies such as ams-OSRAM AG and Siargo Ltd. are broadening their offerings to serve this expanding industrial automation segment.

Automotive Fuel and Emission Control Systems Fueling Market Growth

The expanding integration of MEMS flow sensors in automotive fuel management and emission control systems represents another critical trend shaping MEMS Flow Sensor (Gas, Liquid) Market. Increasingly stringent vehicular emission regulations across major automotive markets are compelling manufacturers to deploy highly precise gas flow sensing technologies for exhaust gas recirculation and fuel injection monitoring. MEMS-based sensors, leveraging semiconductor fabrication techniques to integrate mechanical and electronic components at the microscale, offer the accuracy and reliability required to meet evolving regulatory standards, further solidifying their role across next-generation automotive platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

MEMS Flow Sensor (Gas, Liquid) Market , Competitive Dynamics and Leading Innovators

Global MEMS Flow Sensor (Gas, Liquid) Market is characterized by a moderately consolidated competitive landscape, with a handful of technologically advanced players commanding significant market share. Sensirion AG stands out as a dominant force, recognized for its highly integrated thermal mass flow sensors widely deployed across medical devices, HVAC systems, and industrial automation. Honeywell International Inc. reinforces its competitive positioning through a broad portfolio of MEMS-based gas and liquid flow sensing solutions tailored to aerospace, process industries, and smart metering applications. ams-OSRAM AG and Omron Corporation further strengthen the competitive fabric by delivering precision microflow sensing platforms that address the growing demand for low-power, miniaturized sensors in IoT-connected environments. The market, valued at USD 1.34 billion in 2025 and projected to reach USD 2.87 billion by 2034 at a CAGR of 7.8%, continues to attract sustained R&D investment from incumbent players aiming to extend their technological differentiation across both gas and liquid sensing segments.

Beyond the leading players, a cohort of specialized and regionally significant companies contributes meaningfully to the competitive ecosystem of the MEMS Flow Sensor market. Siargo Ltd. has carved out a notable niche with its silicon-based MEMS mass flow sensors targeting gas metering and respiratory medical applications. Renesas Electronics and Bosch Sensortec leverage their broader semiconductor manufacturing capabilities to develop MEMS flow sensing solutions optimized for automotive fuel management and emission control systems. Companies such as Gems Sensors & Controls, First Sensor AG (a TE Connectivity company), and Posifa Technologies continue to expand their product lines to serve industrial process control and precision liquid dispensing markets. The competitive intensity is further elevated by emerging players from Asia-Pacific, including Hanwei Electronics and Cubic Sensor and Instrument Co., who are rapidly scaling their MEMS flow sensor capabilities to address both domestic and export markets, intensifying price competition while driving broader technology adoption across diversified end-use industries.

List of Key MEMS Flow Sensor (Gas, Liquid) Companies Profiled

- Sensirion AG

- Honeywell International Inc.

- ams-OSRAM AG

- Omron Corporation

- Siargo Ltd.

- Bosch Sensortec GmbH

- Renesas Electronics Corporation

- Gems Sensors & Controls

- First Sensor AG (TE Connectivity)

- Posifa Technologies

- Hanwei Electronics Group Corporation

- Cubic Sensor and Instrument Co., Ltd.

- Integrated Device Technology (IDT)

- AEMSENSORS

- Microbridge Technologies Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thermal Mass Flow Sensors represent the leading sensor type in the MEMS flow sensor market, owing to their exceptional suitability for both gas and liquid measurement applications across a broad spectrum of industries.

|

| By Application |

|

Medical Devices & Healthcare emerge as the dominant application segment within the MEMS flow sensor market, fueled by the escalating global demand for precise fluid management solutions in clinical and patient-care environments.

|

| By End User |

|

Healthcare & Pharmaceutical Institutions constitute the foremost end-user category for MEMS flow sensors, driven by the critical role that precise flow measurement plays in both therapeutic and diagnostic applications.

|

| By Fluid Medium |

|

Gas Flow Sensors represent the leading fluid medium segment, propelled by the rapid global expansion of smart gas metering infrastructure and the growing need for emission monitoring in automotive and industrial environments.

|

| By Technology Integration |

|

IoT-Enabled Smart MEMS Flow Sensors are rapidly emerging as the most dynamic and strategically significant technology integration segment, reflecting the broader industrial transition toward connected, data-driven operational frameworks.

|

Regional Analysis: MEMS Flow Sensor (Gas, Liquid) Market

Asia-Pacific

Asia-Pacific’s rapid adoption of Industry 4.0 principles has significantly elevated the demand for MEMS flow sensors across gas and liquid applications. Smart factories in China and South Korea are increasingly integrating precision flow measurement systems into automated production lines, enabling real-time process control, reduced wastage, and improved operational efficiency across chemical, food processing, and electronics manufacturing sectors.

The region’s ambitious energy transition goals are accelerating deployment of MEMS flow sensors in natural gas distribution networks, hydrogen fuel infrastructure, and renewable energy systems. Utilities across Japan and India are investing in advanced metering infrastructure where accurate gas and liquid flow monitoring is essential for grid balancing, leak detection, and consumption optimization across both residential and industrial utility networks.

Asia-Pacific’s expanding healthcare infrastructure is a significant driver for MEMS flow sensor adoption in medical gas delivery systems, diagnostic devices, and laboratory instrumentation. Countries like Japan and South Korea lead in medical device innovation, embedding miniaturized MEMS flow sensors into respiratory equipment and drug infusion systems, where precise liquid flow measurement is non-negotiable for patient safety and clinical accuracy.

The region hosts a world-class semiconductor manufacturing ecosystem that directly supports advanced MEMS flow sensor development. Taiwan’s foundry capabilities, Japan’s precision fabrication expertise, and China’s growing domestic chip design industry collectively enable cost-effective, high-volume production of next-generation MEMS sensing components, fostering innovation cycles that keep Asia-Pacific technologically competitive on the global stage.

North America

North America represents one of the most technologically mature and innovation-intensive regions in the global MEMS flow sensor market. The United States, in particular, is home to a dense concentration of MEMS technology developers, systems integrators, and end-use industries that collectively sustain robust demand for both gas and liquid flow sensing solutions. The aerospace, defense, and advanced manufacturing sectors are key consumers, relying on high-precision MEMS flow sensors for fuel monitoring, environmental control, and process automation. The region’s well-established oil and gas industry also presents a sustained demand base, where MEMS-enabled flow meters support pipeline integrity monitoring and upstream production optimization. Additionally, the rapid growth of the semiconductor and cleanroom industries in the United States reinforces the need for ultra-precise liquid flow measurement tools. Strong venture capital activity and federal funding for MEMS research further stimulate the commercialization of next-generation flow sensor technologies. Canada contributes through its mining and energy sectors, where reliable gas flow measurement is critical to safety compliance and operational efficiency.

Europe

Europe maintains a strategically significant position in the MEMS flow sensor market, underpinned by stringent regulatory frameworks, a strong industrial base, and a sustained commitment to environmental sustainability. Germany, the Netherlands, France, and Switzerland are particularly prominent, housing leading manufacturers and research institutions focused on advancing MEMS-based flow measurement technologies for both gas and liquid applications. The European Union’s emphasis on energy efficiency and carbon emission reduction has accelerated adoption of smart metering and flow monitoring systems across utilities, industrial facilities, and commercial buildings. The automotive sector, especially within Germany, continues to demand high-reliability MEMS flow sensors for fuel injection systems, exhaust monitoring, and hydrogen powertrain development. The region’s strong pharmaceutical and biotech industries further drive demand for precision liquid flow sensors in manufacturing and quality assurance processes. Europe’s regulatory environment, particularly around emissions and process safety, acts as a consistent market catalyst, encouraging investment in accurate and durable MEMS flow sensing technologies.

South America

South America presents an emerging but increasingly promising landscape for the MEMS flow sensor market, with Brazil and Argentina serving as the primary growth anchors. The region’s expanding oil and gas industry, particularly in Brazil’s offshore deep-water operations, is generating demand for robust flow measurement solutions capable of operating in demanding environments. Agricultural industrialization is another key driver, as precision irrigation and water management systems increasingly incorporate liquid flow sensors to optimize resource usage and crop yields. The mining sector across Chile and Peru further contributes to demand, where accurate gas and liquid flow monitoring supports safety and process control in mineral extraction. While the market remains in a relatively nascent stage compared to North America or Asia-Pacific, growing infrastructure investment, increasing industrial digitalization, and a rising awareness of smart flow measurement benefits are gradually shaping a more favorable environment for MEMS flow sensor adoption across the region through the forecast period.

Middle East & Africa

The Middle East and Africa region occupies a developing but strategically relevant position in the global MEMS flow sensor market. The Gulf Cooperation Council countries, particularly Saudi Arabia, the UAE, and Qatar, represent the most active markets within this region, driven primarily by the extensive oil and gas industry that demands reliable gas flow measurement across exploration, production, and distribution infrastructure. National diversification strategies, such as Saudi Arabia’s Vision 2030, are encouraging investment in non-oil industrial sectors including water desalination, smart city infrastructure, and advanced manufacturing, each creating new avenues for MEMS flow sensor deployment. In Africa, the gradual expansion of industrial and agricultural infrastructure, particularly in South Africa, Nigeria, and Kenya, is fostering nascent demand for both gas and liquid flow sensors. Challenges related to technology adoption costs and infrastructure development persist; however, international partnerships and increasing foreign direct investment are steadily building a more receptive market environment for MEMS-based flow measurement solutions across the region.

Report Scope

This market research report provides a comprehensive analysis of the MEMS Flow Sensor (Gas, Liquid) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MEMS Flow Sensor (Gas, Liquid) Market?

-> MEMS Flow Sensor (Gas, Liquid) Market was valued at USD 1.34 billion in 2025 and is expected to reach USD 2.87 billion by 2034, growing at a CAGR of 7.8% during the forecast period from 2026 to 2034.

Which key companies operate MEMS Flow Sensor (Gas, Liquid) Market?

-> Key players include Sensirion AG, Honeywell International Inc., ams-OSRAM AG, Siargo Ltd., and Omron Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for precise fluid management in healthcare, rapid adoption of smart gas metering infrastructure, expanding use of MEMS-based sensors in automotive fuel and emission control systems, proliferation of IoT-enabled industrial automation, and the push toward miniaturized, low-power sensing solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by industrial automation and smart metering adoption, while North America and Europe remain dominant markets supported by advanced healthcare infrastructure and stringent emission regulations.

What are the emerging trends?

-> Emerging trends include thermal mass flow sensors, differential pressure-based sensors, ultrasonic MEMS flow sensors, Coriolis-type MEMS sensors, IoT-integrated sensing platforms, and miniaturized low-power MEMS devices for medical, automotive, and industrial process control applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...