HUD (Head-Up Display) Controller IC Market Insights

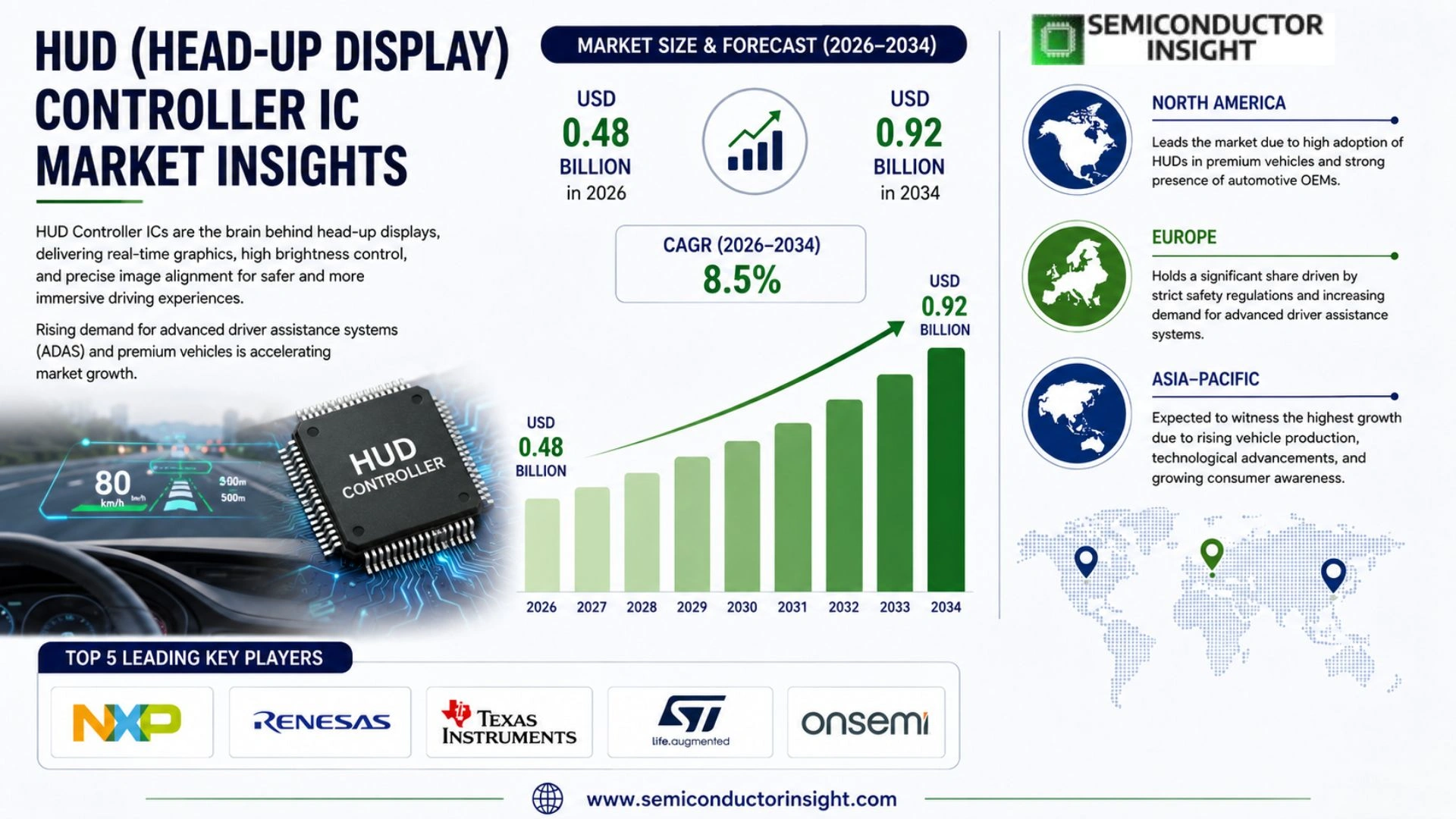

HUD (Head-Up Display) Controller IC Market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.92 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period.

HUD Controller ICs are specialized semiconductor components designed to manage the processing, warping correction, image rendering, and interface functions essential for modern Head-Up Display systems in vehicles. These integrated circuits handle critical tasks including video signal processing from multiple sources, distortion compensation for curved windshields, safety monitoring features, and seamless integration with vehicle networks such as CAN, LIN, and Ethernet. They enable real-time projection of navigation data, vehicle speed, ADAS alerts, and other vital information directly into the driver’s line of sight.

The market is experiencing steady growth due to several factors, including the rising adoption of advanced driver-assistance systems (ADAS), increasing demand for enhanced vehicle safety features, and the expansion of augmented reality (AR) HUD technologies in both premium and mid-range vehicles. Furthermore, the proliferation of electric vehicles and software-defined architectures has accelerated the need for sophisticated display controllers capable of handling complex graphics and low-latency operations. Initiatives by key semiconductor players are also expected to fuel market growth through continuous innovation in power efficiency and functional safety compliance. Major companies offering portfolios in this space include Epson, Rohm Semiconductor, and other automotive-grade IC suppliers focused on cockpit electronics.

MARKET DRIVERS

Rising Adoption of AR-HUD in Premium and Mid-Range Vehicles

HUD (Head-Up Display) Controller IC Market is experiencing robust growth driven by the expanding integration of augmented reality head-up displays in automotive applications. As automakers advance digital cockpits, controller ICs enable precise image warping correction, local dimming, and real-time data overlay for navigation and ADAS alerts directly in the driver’s line of sight. This reduces distraction and improves safety, with AR-HUD systems gaining traction across vehicle segments.

Advancements in Automotive Semiconductor Solutions

Innovations from semiconductor leaders, including specialized HUD controller ICs with flexible video interfaces and automotive-grade reliability, are accelerating market expansion. These ICs address key technical requirements such as distortion correction for curved windshields and support for higher-resolution displays, facilitating smoother integration into electric and software-defined vehicles. Growing demand for connected car features further propels the need for sophisticated controller ICs that process inputs from multiple sensors and ECUs.

➤ Regulatory mandates for enhanced driver safety and ADAS compliance continue to boost demand for advanced HUD systems and their enabling controller ICs.

Overall, the proliferation of HUD technology in response to consumer demand for immersive driving experiences and OEM focus on differentiation positions the HUD Controller IC Market for sustained expansion through the forecast period.

MARKET CHALLENGES

Technical Complexity in High-Resolution AR Integration

Developing HUD Controller ICs capable of handling high-resolution augmented reality overlays while maintaining low latency and power efficiency presents significant engineering hurdles. Ensuring distortion-free projection on varying windshield curvatures and consistent performance across lighting conditions requires advanced processing capabilities, challenging suppliers to balance performance with thermal and size constraints.

Other Challenges

Supply Chain and Qualification Barriers

Automotive-grade qualification processes for controller ICs are lengthy and stringent, delaying time-to-market for new innovations amid global semiconductor supply dynamics.

Cost Pressures in Mass-Market Adoption

While premium vehicles readily adopt sophisticated HUD systems, bringing advanced controller IC solutions to mid-range and economy vehicles remains challenging due to cost sensitivities and the need for scalable designs.

MARKET RESTRAINTS

High Development Costs and Packaging Constraints

HUD (Head-Up Display) Controller IC Market faces restraints from elevated R&D expenses associated with creating robust, safety-certified components suitable for harsh automotive environments. Spatial limitations within vehicle dashboards further complicate integration of powerful controller ICs alongside projectors and optics, particularly for compact designs required in modern vehicle architectures.

The need for seamless compatibility with diverse display technologies and ECU architectures adds layers of complexity, potentially slowing broader market penetration despite overall HUD growth trends.

MARKET OPPORTUNITIES

Expansion into Electric and Autonomous Vehicle Platforms

Significant opportunities exist in the rising adoption of electric vehicles and autonomous driving technologies, where HUD Controller ICs play a critical role in delivering real-time information for enhanced situational awareness. Partnerships between semiconductor firms and Tier-1 suppliers are enabling faster development cycles and customization for next-generation software-defined vehicles.

Emerging applications in commercial vehicles and two-wheelers, combined with advancements in local dimming and higher-resolution capabilities, offer new avenues for market participants to capture value in a diversifying ecosystem. Continued innovation in power-efficient designs will further unlock potential in cost-sensitive segments.

Trends

Rising Integration of ADAS and Vehicle Safety Features

HUD (Head-Up Display) Controller IC Market continues to evolve as automotive manufacturers prioritize enhanced driver visibility and safety. These specialized integrated circuits serve as the core processing units for modern Head-Up Display systems, managing video signal processing from multiple sources, distortion compensation for curved windshields, and real-time rendering of critical information such as navigation data, vehicle speed, and ADAS alerts directly in the driver’s line of sight.

Other Trends

Expansion of Augmented Reality Capabilities

AR-enabled HUD systems are gaining traction across both premium and mid-range vehicle segments. HUD (Head-Up Display) Controller IC solutions now incorporate advanced image warping correction and seamless interface functions that support complex graphics overlays. This development allows for more intuitive presentation of layered information, improving situational awareness while maintaining focus on the road ahead.

Support for Software-Defined Vehicle Architectures

The shift toward software-defined vehicles has increased demand for versatile HUD (Head-Up Display) Controller IC components capable of handling low-latency operations and integration with multiple vehicle networks including CAN, LIN, and Ethernet. These ICs enable efficient data exchange between display systems and broader cockpit electronics, facilitating faster updates and customization of display content.

Focus on Power Efficiency and Functional Safety

Leading semiconductor suppliers are advancing HUD (Head-Up Display) Controller IC designs with emphasis on power optimization and compliance with stringent automotive safety standards. This trend is particularly relevant as electric vehicles proliferate, requiring efficient thermal management and reliable performance in diverse operating conditions. Innovations in these areas help manufacturers balance sophisticated graphics processing with energy constraints while ensuring fail-safe operation of safety-critical display functions.

The ongoing development of HUD (Head-Up Display) Controller IC technologies reflects the broader automotive industry’s commitment to intelligent cockpit solutions. As vehicle systems become more interconnected, these controller ICs play an essential role in delivering clear, undistorted visual information that supports both driver convenience and advanced safety protocols. Continued collaboration among automotive-grade IC providers is expected to drive further refinements in processing speed, integration flexibility, and overall system reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

The HUD Controller IC Market Features Specialized Semiconductor Leaders Driving Innovation in Automotive Display Processing

HUD (Head-Up Display) Controller IC Market is characterized by a concentrated competitive structure dominated by established semiconductor manufacturers with deep expertise in automotive-grade electronics. Seiko Epson Corporation and ROHM Semiconductor emerge as leading players, offering dedicated warping correction and video processing ICs tailored for high-resolution HUD systems. These companies focus on critical functions such as image distortion compensation for curved windshields, low-latency rendering, and functional safety compliance, positioning them strongly amid rising demand for AR-HUD integration in next-generation vehicles.

Other significant players include major automotive semiconductor suppliers expanding into display controller solutions to address the needs of software-defined vehicles and advanced ADAS applications. Companies such as Texas Instruments, Renesas Electronics, and STMicroelectronics contribute through broader cockpit domain controller platforms and specialized processing capabilities, while niche innovators support power efficiency and high-performance graphics requirements. The market remains innovation-driven, with ongoing advancements in power optimization, multi-interface support, and integration with vehicle networks like Ethernet and CAN.

List of Key HUD Controller IC Companies Profiled

- Seiko Epson Corporation

- ROHM Semiconductor

- Texas Instruments (TI)

- Renesas Electronics

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Panasonic Corporation

- Continental AG

- DENSO Corporation

- Visteon Corporation

- Robert Bosch GmbH

- Harman International

- Nippon Seiki Co., Ltd.

- Yazaki Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AR HUD Controller ICs represent the leading segment due to their advanced capabilities in rendering dynamic overlays and real-time data fusion. These ICs excel in handling complex image warping and distortion correction for curved windshields, ensuring crisp visuals in varying lighting conditions. Their integration with multiple video sources enables seamless presentation of navigation, speed, and safety alerts directly in the driver’s view. This type supports low-latency operations critical for modern vehicle architectures and facilitates enhanced user experiences through augmented reality features. |

| By Application |

|

Windshield HUD emerges as the dominant application segment owing to its ability to project information directly onto the vehicle’s windshield for an unobstructed driver focus. Controller ICs in this category manage sophisticated signal processing to compensate for optical distortions and maintain image stability during vehicle motion. They support integration with vehicle networks for real-time data delivery, enhancing situational awareness. This application drives innovation in functional safety features and power-efficient designs suitable for continuous operation in automotive environments. |

| By End User |

|

Passenger Vehicles constitute the leading end-user segment fueled by rising consumer expectations for intuitive and safety-oriented cockpit experiences. Controller ICs tailored for this segment prioritize compact designs that integrate smoothly with existing electronic control units while delivering high-quality graphics. They enable personalized information display that reduces driver distraction and supports advanced driver-assistance features. The emphasis on user-centric interfaces in passenger cars accelerates demand for versatile ICs capable of handling diverse input sources and output formats. |

| By Technology |

|

LCoS-based Controllers lead this segment through superior brightness, contrast, and compact form factors ideal for space-constrained vehicle dashboards. These technologies allow precise light modulation essential for clear daytime visibility and detailed imagery. Integration with automotive-grade processors ensures compliance with stringent reliability standards while optimizing thermal management. Their flexibility in supporting high-resolution content positions them favorably for next-generation HUD implementations requiring rich visual data. |

| By Functionality |

|

ADAS Integrated functionality leads due to its critical role in fusing sensor data with visual outputs for proactive safety notifications. These controller ICs incorporate robust monitoring and diagnostic capabilities to ensure uninterrupted performance under demanding conditions. They facilitate low-latency communication across vehicle networks, supporting features like collision warnings and lane guidance overlays. This functional category promotes innovation in software-defined architectures and enhances overall system reliability in intelligent vehicles. |

Regional Analysis: HUD (Head-Up Display) Controller IC Market

Asia-Pacific

Strong automotive production bases and increasing integration of ADAS technologies fuel demand for advanced HUD controller ICs. Focus on vehicle connectivity and digital cockpits encourages manufacturers to prioritize high-speed processing chips that deliver clear, low-latency projections.

Regional players excel in developing compact, power-efficient ICs compatible with AR-HUD systems. Continuous improvements in thermal management and signal processing enable brighter displays and wider field-of-view capabilities tailored to diverse driving conditions.

Close partnerships between IC suppliers, display manufacturers, and automakers streamline product development cycles. This synergy supports customization for electric and autonomous vehicles, reinforcing the region’s competitive edge in HUD (Head-Up Display) Controller IC solutions.

Sustained investments in smart transportation infrastructure and favorable policies for automotive innovation will drive steady growth. The region is poised to lead in scaling next-generation HUD controller technologies for global markets.

North America

North America maintains a significant presence HUD (Head-Up Display) Controller IC Market through its focus on premium vehicle segments and technological innovation. The United States leads with strong emphasis on safety regulations and consumer preference for advanced in-vehicle displays. Automotive giants and tech firms collaborate to enhance HUD systems that provide critical driving information with superior clarity. The region’s mature semiconductor industry contributes specialized controller ICs designed for high reliability in diverse climates. Emphasis on autonomous vehicle research further integrates sophisticated HUD solutions, creating sustained opportunities for IC manufacturers. Strategic investments in research and development ensure North America remains a key innovator, particularly in software-defined vehicle architectures that leverage HUD controller capabilities for enhanced user interfaces.

Europe

Europe exhibits steady progress HUD (Head-Up Display) Controller IC Market, supported by stringent safety standards and a robust luxury automotive sector. Germany, France, and the UK drive adoption through premium brands that incorporate advanced HUD technologies for superior driver assistance. The region’s commitment to sustainable mobility encourages development of energy-efficient controller ICs suitable for electric vehicles. Collaborative ecosystems involving automakers, suppliers, and research institutions accelerate refinement of projection accuracy and integration with vehicle sensor networks. Regulatory push toward reduced emissions and improved road safety reinforces demand for intuitive display systems. Europe’s focus on quality and precision positions it as an important market for high-end HUD (Head-Up Display) Controller IC applications.

South America

South America shows emerging potential HUD (Head-Up Display) Controller IC Market as automotive markets expand and consumer awareness of safety technologies grows. Brazil and other key countries witness gradual integration of HUD systems in mid-to-high segment vehicles. Local manufacturing initiatives and foreign investments help establish basic supply chains for electronic components. While infrastructure development varies, increasing urbanization drives interest in advanced driver interfaces that improve navigation and safety. The region benefits from technology transfer from global partners, fostering gradual capability building in controller IC applications. Future growth will depend on economic stability and expanding middle-class demand for modern vehicle features incorporating HUD technologies.

Middle East & Africa

The Middle East and Africa region presents developing opportunities withHUD (Head-Up Display) Controller IC Market, primarily linked to luxury vehicle imports and smart city initiatives. Gulf countries invest in premium automotive technologies, creating demand for sophisticated HUD systems in high-end models. Infrastructure modernization projects support integration of advanced display solutions for better traffic management and driver information. Although the market remains nascent compared to other regions, rising interest in vehicle connectivity and safety features stimulates gradual adoption of controller ICs. Partnerships with international technology providers facilitate knowledge transfer and localized adaptation. Long-term prospects align with economic diversification efforts and growing emphasis on intelligent transportation systems across key markets.

Report Scope

This market research report provides a comprehensive analysis of the HUD (Head-Up Display) Controller IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of HUD (Head-Up Display) Controller IC Market?

-> HUD (Head-Up Display) Controller IC Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.92 billion by 2034.

Which key companies operate HUD (Head-Up Display) Controller IC Market?

-> Key players include Epson, Rohm Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of advanced driver-assistance systems (ADAS), increasing demand for enhanced vehicle safety features, and the expansion of augmented reality (AR) HUD technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include AR HUD integration, power efficiency improvements, and functional safety compliance for automotive-grade ICs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...