High Bandwidth Memory (HBM3, HBM3E, HBM4) Market Insights

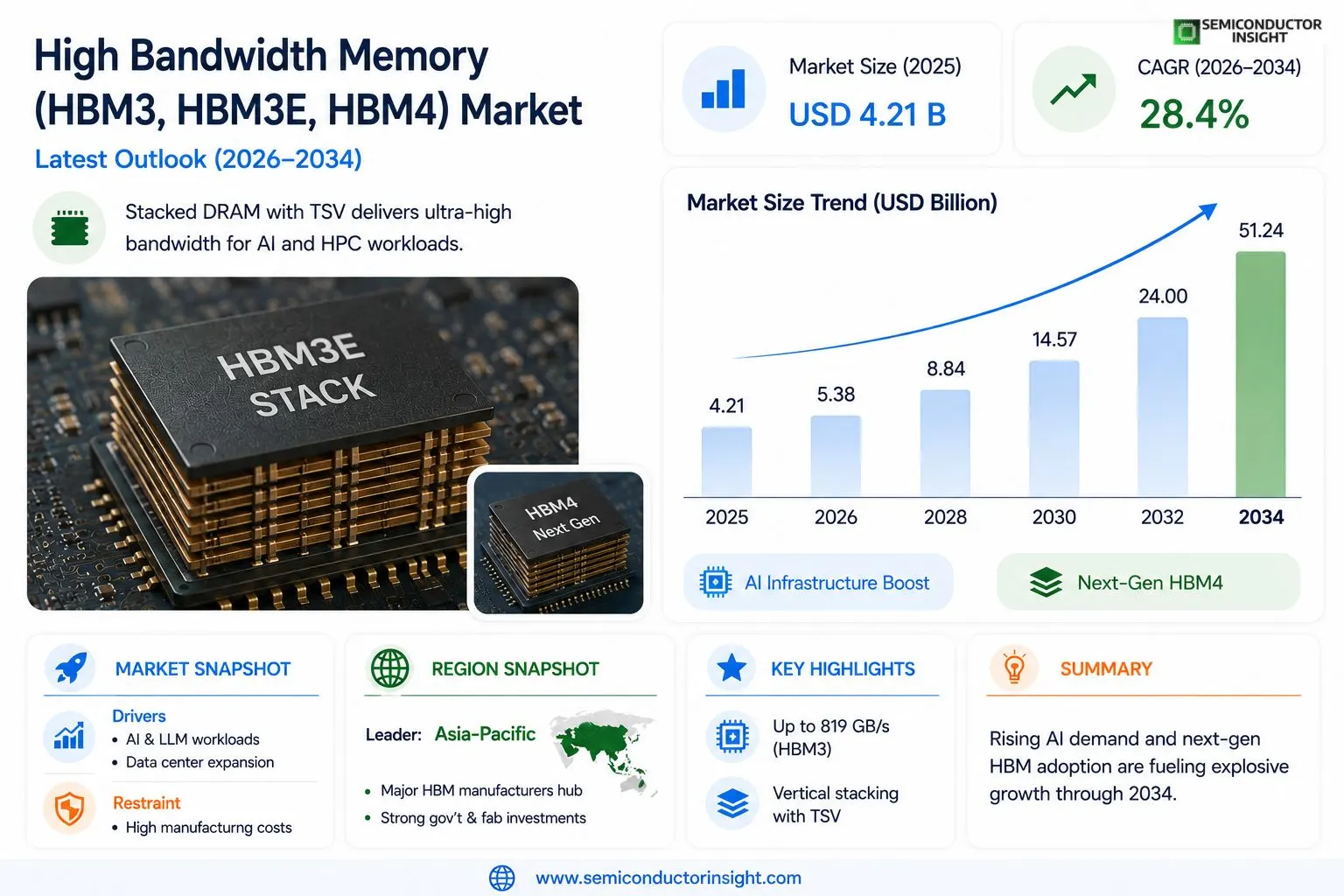

Global High Bandwidth Memory (HBM3, HBM3E, HBM4) market size was valued at USD 4.21 billion in 2025. The market is projected to grow from USD 5.38 billion in 2026 to USD 51.24 billion by 2034, exhibiting a CAGR of 28.4% during the forecast period.

High Bandwidth Memory (HBM) refers to a high-performance RAM interface designed for use in conjunction with high-end processors, graphics cards, and AI accelerators. HBM3, HBM3E, and HBM4 are successive generations offering exponentially greater memory bandwidth, higher capacity, and improved energy efficiency compared to conventional DRAM solutions. These technologies stack multiple DRAM dies vertically using through-silicon via (TSV) interconnects, enabling significantly wider bus widths and faster data transfer rates. HBM3 delivers up to 819 GB/s bandwidth per stack, while HBM3E pushes this further, and HBM4 is anticipated to offer even greater performance improvements in capacity and speed.

The market is experiencing exceptional growth driven by the accelerating demand for AI and machine learning workloads, high-performance computing (HPC), and next-generation data center infrastructure. The explosive adoption of large language models (LLMs) and generative AI platforms has created unprecedented demand for memory solutions capable of feeding massive compute clusters with data at extreme speeds. Furthermore, leading semiconductor companies have significantly ramped up investments in HBM production capacity. For instance, SK Hynix began mass production of HBM3E in early 2024 and secured a major supply agreement with NVIDIA for use in its H200 and Blackwell GPU architectures. Samsung Electronics and Micron Technology are also key players actively scaling HBM3E output while advancing HBM4 development, positioning themselves to meet surging demand from hyperscale cloud providers and AI hardware manufacturers worldwide.

MARKET DRIVERS

Surging Demand from AI and High-Performance Computing Accelerates HBM Adoption

The rapid proliferation of artificial intelligence workloads, large language models, and generative AI infrastructure has emerged as the most significant driver propelling the High Bandwidth Memory market forward. Modern AI accelerators and GPUs require memory solutions capable of delivering exceptional throughput with minimal latency, conditions that HBM3, HBM3E, and HBM4 architectures are uniquely engineered to fulfill. Leading AI chip designers have integrated HBM stacks as a foundational component in their flagship products, creating a consistent and growing demand pipeline for advanced HBM generations. The convergence of model complexity and data center scale-out requirements has made high bandwidth memory not merely a performance advantage but an operational necessity.

Data Center Expansion and Hyperscaler Investment Fueling HBM3E and HBM4 Uptake

Global hyperscale cloud operators continue to invest heavily in next-generation computing infrastructure to support AI-as-a-service offerings, distributed training clusters, and inference at scale. These investments directly translate into procurement of AI accelerators that rely on HBM3E and, increasingly, HBM4 memory stacks. HBM3E delivers bandwidth in excess of 1.2 TB/s per stack, enabling data centers to process larger model batches with greater energy efficiency compared to previous memory generations. As the number of AI inference requests grows in line with enterprise adoption of AI applications, the demand for high-density, high-speed memory solutions embedded in data center hardware continues to intensify.

➤ The transition from HBM2E to HBM3 and HBM3E in leading AI accelerators has demonstrated bandwidth improvements of up to 50% generation over generation, reinforcing HBM’s irreplaceable role in AI silicon architecture.

Beyond AI, the High Performance Computing segment continues to serve as a reliable demand anchor for the HBM market. Scientific simulations, climate modeling, genomic analysis, and defense-grade computing platforms all leverage the superior memory bandwidth that HBM3 and HBM3E provide. Government-backed supercomputing programs across North America, Europe, and Asia-Pacific have specified HBM-equipped accelerators as core components of national exascale initiatives, providing long-term, contract-backed demand that supports HBM supply chain investment and manufacturing capacity expansion among leading memory producers.

MARKET CHALLENGES

Highly Concentrated Supply Chain Creates Structural Vulnerability in the HBM Ecosystem

The global supply of HBM3, HBM3E, and HBM4 remains concentrated among a small number of manufacturers, with SK Hynix, Samsung, and Micron collectively accounting for the entirety of commercially available HBM production. This oligopolistic supply structure creates significant challenges for system integrators and AI chip developers seeking supply assurance and competitive pricing. Lead times for HBM3E allocations extended to over 12 months at peak demand periods, highlighting the fragility of a supply chain that cannot rapidly scale in response to sudden demand surges. Any disruption at a single major fab , whether due to technical yield issues, geopolitical tensions, or natural events , carries the potential to create cascading shortages across the AI hardware ecosystem.

Other Challenges

Complex Integration and Advanced Packaging Requirements

HBM stacks are not plug-and-play components. Their integration with logic dies through 2.5D packaging technologies such as silicon interposers and through-silicon vias demands advanced semiconductor packaging expertise that remains in limited supply globally. The cost and complexity of CoWoS and similar advanced packaging platforms add friction to the adoption curve, particularly for second-tier chip developers and emerging AI hardware startups that lack established relationships with advanced packaging foundries.

Thermal Management at High Bandwidth Densities

As HBM3E and HBM4 push bandwidth and capacity boundaries, the thermal output of densely stacked memory dies presents an increasingly difficult engineering challenge. Sustained high-throughput operations in server environments can cause localized hotspots within HBM stacks, requiring sophisticated cooling architectures that add system cost and design complexity. Liquid cooling and immersion cooling adoption, while growing, introduces additional operational requirements that not all data center operators are currently equipped to manage at scale.

MARKET RESTRAINTS

Prohibitive Manufacturing Costs Limit Accessibility and Broaden the Price Premium Gap

The fabrication of HBM3, HBM3E, and HBM4 involves multi-die stacking processes, precision TSV drilling, and tight yield requirements that make production inherently capital-intensive. The per-gigabyte cost of HBM remains substantially higher than GDDR6X and LPDDR5X alternatives, creating a meaningful cost barrier that restricts deployment to premium-tier accelerators and limits adoption across cost-sensitive market segments such as edge AI and mid-range workstation hardware. While economies of scale are gradually moderating pricing over time, the structural cost floor for HBM manufacturing is unlikely to approach commodity DRAM economics in the foreseeable future, constraining its addressable market to high-value applications.

Geopolitical Tensions and Export Controls Introduce Supply Chain Uncertainty

Escalating technology trade restrictions between major economies have introduced a layer of regulatory risk that constrains the free flow of advanced memory technology and HBM-equipped AI hardware across borders. Export control frameworks have targeted high-performance AI accelerators, which by extension affects the demand visibility and market planning for HBM producers. Customers in restricted markets that previously represented growing demand opportunities are now subject to compliance-driven procurement limitations, reducing the effective global market size for top-tier HBM products and creating uncertainty in long-term capacity investment decisions for manufacturers.

Yield Constraints in Next-Generation HBM4 Ramp Delay Broad Market Availability

The transition to HBM4, which involves further increases in stack height, die count, and interface complexity, presents significant yield management challenges during initial production ramp phases. Early-stage manufacturing of advanced HBM generations historically delivers lower yields that elevate effective unit costs and restrict volume availability. These yield constraints delay broad market availability, limiting HBM4 adoption to flagship products from the most resource-intensive customers during the initial commercialization window and slowing the overall market’s progression toward the next performance tier.

MARKET OPPORTUNITIES

HBM4 Architecture Opens New Frontiers in AI Accelerator Performance and Memory Capacity

The commercial development and anticipated broad deployment of HBM4 represents a substantial market opportunity for memory manufacturers, packaging foundries, and system integrators. HBM4 is designed to support greater per-stack capacity and higher interface widths compared to HBM3E, enabling the next generation of AI training clusters to handle significantly larger model parameters without bottlenecking on memory bandwidth or capacity. As frontier AI model sizes continue to scale, HBM4 adoption is positioned to accelerate beginning in the 2025–2026 timeframe, driven by demand from hyperscalers and sovereign AI infrastructure programs that require state-of-the-art memory performance.

Expansion into Automotive, Networking, and Edge AI Segments Broadens the HBM Addressable Market

While AI data center applications have historically driven HBM demand, emerging use cases in automotive AI processing, high-speed networking silicon, and advanced edge computing are beginning to create incremental demand vectors for High Bandwidth Memory. Next-generation autonomous driving compute platforms and software-defined vehicle architectures require processing and memory bandwidth profiles that conventional DRAM solutions struggle to satisfy. Similarly, high-radix network switch ASICs and programmable packet processing chips represent a growing class of applications where HBM’s density and bandwidth characteristics provide meaningful architectural advantages, expanding the HBM total addressable market beyond its current AI-centric concentration.

Capacity Investments and New Entrants in Advanced Packaging Drive Supply Chain Resilience Opportunities

Substantial capital investments being directed toward advanced packaging capacity globally present an opportunity to resolve the supply constraints that have historically restrained HBM market growth. Government-backed semiconductor initiatives in the United States, South Korea, Japan, and the European Union are funding the expansion of domestic advanced packaging infrastructure, which is essential to scaling HBM supply. New entrants into CoWoS-equivalent packaging capacity are expected to reduce bottlenecks that currently limit the number of HBM-enabled AI accelerators that can reach the market annually. As packaging capacity grows in line with HBM die supply, the ecosystem is poised to support a broader array of system designs that incorporate HBM3E and HBM4, creating opportunities across the full value chain from substrate suppliers to end-system OEMs.

High Bandwidth Memory (HBM3, HBM3E, HBM4) Market Trends

AI and Generative Workloads Accelerating Demand for High Bandwidth Memory

The High Bandwidth Memory (HBM3, HBM3E, HBM4) market is undergoing a significant transformation, primarily driven by the rapid proliferation of artificial intelligence and machine learning applications. The explosive adoption of large language models (LLMs) and generative AI platforms has created unprecedented demand for memory architectures capable of sustaining extreme data throughput. HBM technologies, which stack multiple DRAM dies vertically through through-silicon via (TSV) interconnects, deliver substantially wider bus widths and faster transfer rates than conventional DRAM solutions. HBM3, for instance, delivers up to 819 GB/s of bandwidth per stack, a capability that has made it foundational to modern AI accelerator design and high-performance computing infrastructure.

Other Trends

Mass Production Ramp-Up by Leading Semiconductor Manufacturers

A defining trend shaping the High Bandwidth Memory (HBM3, HBM3E, HBM4) market is the aggressive capacity expansion undertaken by major semiconductor players. SK Hynix commenced mass production of HBM3E in early 2024 and secured a pivotal supply agreement with NVIDIA for integration into its H200 and Blackwell GPU architectures. Concurrently, Samsung Electronics and Micron Technology are actively scaling HBM3E output while advancing their respective HBM4 development roadmaps. This competitive production ramp is enabling the ecosystem to keep pace with surging demand from hyperscale cloud providers and AI hardware manufacturers globally.

Next-Generation HBM4 Development Gaining Strategic Momentum

Industry leaders are increasingly directing R&D investments toward HBM4, the next evolutionary step in high bandwidth memory technology. HBM4 is anticipated to deliver substantial improvements in both memory capacity and data transfer speeds compared to HBM3E, positioning it as a critical enabler for future AI compute clusters and exascale computing systems. Semiconductor manufacturers are accelerating their HBM4 qualification timelines to align with the product cycles of next-generation GPU and AI accelerator platforms, reflecting strong forward-looking demand signals from data center operators.

Deepening Integration with Data Center and HPC Infrastructure

The High Bandwidth Memory (HBM3, HBM3E, HBM4) market is also being shaped by the deepening reliance on HBM within next-generation data center and high-performance computing environments. As cloud service providers and enterprises expand their AI infrastructure investments, the requirement for memory solutions that can sustain massive compute throughput at reduced energy consumption continues to intensify. HBM’s energy efficiency advantage over conventional DRAM alternatives further reinforces its adoption trajectory, making it a strategic component in the broader evolution of memory-intensive computing architectures worldwide.

COMPETITIVE LANDSCAPE

Key Industry Players

High Bandwidth Memory (HBM3, HBM3E, HBM4) Market: Competitive Dynamics and Strategic Positioning of Leading Semiconductor Players

The global High Bandwidth Memory (HBM3, HBM3E, HBM4) market is dominated by a concentrated group of advanced semiconductor manufacturers, with SK Hynix holding a leading position as the foremost supplier of HBM solutions worldwide. SK Hynix was the first to achieve mass production of HBM3E in early 2024 and secured a landmark supply agreement with NVIDIA for integration into its H200 and Blackwell GPU architectures, cementing its technological edge in the AI accelerator space. The company’s deep investment in through-silicon via (TSV) stacking technology and its strategic roadmap toward HBM4 development further reinforce its competitive moat. Samsung Electronics and Micron Technology represent the other two pillars of the HBM triopoly, both aggressively scaling HBM3E output while concurrently advancing next-generation HBM4 architectures to address surging demand from hyperscale cloud providers, AI hardware manufacturers, and high-performance computing (HPC) cluster operators globally.

Beyond the primary memory manufacturers, the HBM ecosystem encompasses a broader network of critical enablers including advanced packaging specialists, substrate suppliers, and chipmakers whose products integrate HBM solutions directly into end platforms. Companies such as NVIDIA and AMD are pivotal demand drivers, designing flagship GPU and AI accelerator products , including the H100, H200, Instinct MI300X, and Blackwell series , that rely exclusively on HBM3 and HBM3E for their extreme memory bandwidth requirements. TSMC and ASE Technology play essential roles in advanced packaging and chip-on-wafer-on-substrate (CoWoS) integration processes that physically bond HBM stacks to logic dies. Additionally, Cadence Design Systems and Synopsys provide critical EDA tooling and IP that underpin HBM interface design and verification, while companies like Rambus contribute standardization and memory interface controller IP critical to HBM adoption across next-generation platforms.

List of Key High Bandwidth Memory (HBM3, HBM3E, HBM4) Companies Profiled

- SK Hynix Inc.

- Samsung Electronics Co., Ltd.

- Micron Technology, Inc.

- NVIDIA Corporation

- Advanced Micro Devices, Inc. (AMD)

- Taiwan Semiconductor Manufacturing Company (TSMC)

- ASE Technology Holding Co., Ltd.

- Rambus Inc.

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- Intel Corporation

- Amkor Technology, Inc.

- JEDEC Solid State Technology Association

- Graphcore Limited

- Cerebras Systems

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

HBM3E currently represents the leading segment in the High Bandwidth Memory market, driven by its rapid adoption in cutting-edge AI accelerators and high-performance GPU architectures.

|

| By Application |

|

Artificial Intelligence & Machine Learning Accelerators dominate the application landscape of the HBM market, emerging as the single most transformative force reshaping memory architecture requirements globally.

|

| By End User |

|

Hyperscale Cloud Service Providers represent the dominant end-user segment, anchoring the commercial trajectory of the HBM3, HBM3E, and HBM4 market through their voracious and continuously expanding infrastructure investments.

|

| By Technology Architecture |

|

2.5D Integration via Silicon Interposer currently leads as the most widely adopted packaging architecture for HBM deployment, enabling the co-placement of logic dies and HBM stacks on a shared substrate with minimal signal latency.

|

| By Supply Chain Tier |

|

Tier 1 HBM DRAM Manufacturers occupy the most influential position in the supply chain, exercising decisive control over production volume, technology generation timelines, and the pace at which next-generation HBM capabilities reach the broader market.

|

Regional Analysis: High Bandwidth Memory (HBM3, HBM3E, HBM4) Market

Asia-Pacific

South Korea serves as the technological epicenter of the High Bandwidth Memory (HBM3, HBM3E, HBM4) market. Leading memory manufacturers headquartered here drive continuous architectural improvements, pioneering through-silicon via stacking densities and thermal management solutions that define industry benchmarks. Strategic partnerships with global AI chip designers further reinforce South Korea’s irreplaceable role in the HBM supply chain, securing its dominance well into the next decade.

Taiwan’s advanced semiconductor packaging infrastructure is critically intertwined with HBM3 and HBM4 deployment at scale. The island’s chip-on-wafer-on-substrate and integrated fan-out technologies enable seamless integration of high bandwidth memory stacks with leading-edge AI processors. Taiwan’s foundry and OSAT ecosystem provides the assembly precision that memory chipmakers require to deliver HBM modules meeting stringent performance and reliability specifications demanded by hyperscale data center operators.

Japan’s contribution to the High Bandwidth Memory (HBM3, HBM3E, HBM4) market is foundational rather than visible at the product level. Japanese suppliers dominate the provision of photoresists, polishing slurries, bonding adhesives, and precision lithography equipment essential to HBM wafer processing. Government-supported semiconductor revitalization programs are also spurring domestic capacity expansions, ensuring Japan remains an indispensable upstream partner across the entire HBM value chain.

China is channeling substantial national resources into developing indigenous High Bandwidth Memory capabilities as international supply restrictions intensify. While HBM3E and HBM4 remain technically challenging for Chinese producers to replicate near-term, state-directed investment is compressing the innovation gap. China’s vast domestic AI infrastructure rollout , spanning cloud computing, autonomous systems, and smart manufacturing , creates a captive demand base that is accelerating the urgency and scale of its HBM self-sufficiency programs.

North America

North America represents the most influential demand-side region in the global High Bandwidth Memory (HBM3, HBM3E, HBM4) market, even as its domestic manufacturing footprint remains comparatively limited. The United States is home to the world’s preeminent AI chip designers, whose accelerators, GPUs, and custom silicon architectures are the primary consumption drivers for HBM3 and HBM3E technologies today, with HBM4 integration already on near-term product roadmaps. Hyperscale cloud providers headquartered across North America are deploying AI infrastructure at an unprecedented pace, creating sustained and growing demand for high bandwidth memory solutions capable of supporting large language model training and inference at scale. Federal semiconductor policy initiatives, including incentives to attract advanced memory production onshore, are beginning to shape long-term supply chain diversification strategies. Research universities and national laboratories are also active contributors to HBM architecture innovation, particularly in areas of thermal co-design and heterogeneous integration. While North America may not lead in HBM production volume, its architectural influence, design ecosystem, and capital deployment make it a pivotal force in determining how the High Bandwidth Memory market evolves through 2034.

Europe

Europe occupies a strategically significant but distinct position in the High Bandwidth Memory (HBM3, HBM3E, HBM4) market, characterized more by end-user adoption and research contribution than by volume manufacturing. The European Union’s emphasis on technological sovereignty has spurred coordinated investment in semiconductor capabilities through landmark industrial policy frameworks, with ambitions to foster advanced packaging and chiplet assembly competencies that are directly relevant to HBM integration. Leading European research institutions are actively engaged in HBM co-design projects targeting high-performance computing, automotive AI, and industrial automation applications. Germany, France, and the Netherlands host critical equipment makers whose photolithography and metrology systems underpin HBM wafer fabrication globally. European hyperscalers and sovereign cloud initiatives are scaling AI infrastructure deployments, translating into growing regional consumption of HBM3 and HBM3E modules. As HBM4 standards mature, Europe’s deep expertise in system-level integration and its regulatory influence over semiconductor supply chain transparency will further shape regional market dynamics through the forecast period.

South America

South America remains an emerging participant in the High Bandwidth Memory (HBM3, HBM3E, HBM4) market, with demand currently concentrated in adoption rather than production. Brazil leads regional engagement, driven by expanding cloud infrastructure deployments, growing AI research communities, and a maturing digital economy that is creating upstream demand for advanced computing hardware incorporating HBM technologies. Regional data center investments by global hyperscale operators are gradually introducing HBM-equipped AI accelerators into South American markets. Government-backed programs in Brazil and Chile aimed at advancing domestic technology industries may over the long term create conditions for localized semiconductor assembly activity. However, the absence of indigenous HBM manufacturing capacity and limited access to advanced node fabrication keep South America in a net-import position for the foreseeable future. The region’s trajectory through 2034 will be shaped largely by the pace of digital infrastructure buildout and the ability of local enterprises to integrate AI-driven capabilities that depend on high bandwidth memory performance.

Middle East & Africa

The Middle East & Africa region is at an early but accelerating stage of engagement with the High Bandwidth Memory (HBM3, HBM3E, HBM4) market, driven primarily by large-scale data center and AI infrastructure investments concentrated in Gulf Cooperation Council nations. Saudi Arabia and the United Arab Emirates are deploying sovereign AI strategies that envision substantial compute infrastructure buildouts, directly fueling demand for HBM-equipped accelerators and AI servers. Strategic partnerships between GCC sovereign wealth funds and leading global semiconductor and cloud companies are expected to sustain this investment momentum through the forecast period. Africa’s engagement remains nascent, centered on digital connectivity expansion rather than advanced semiconductor adoption, though long-term urbanization and fintech growth trends may gradually elevate regional demand for AI-capable hardware. The Middle East & Africa region’s role in the High Bandwidth Memory market will primarily be that of a strategic end-market rather than a production hub, with growth trajectories closely tied to the pace of regional AI infrastructure development and technology transfer agreements established through international partnerships.

Report Scope

This market research report provides a comprehensive analysis of the High Bandwidth Memory (HBM3, HBM3E, HBM4) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High Bandwidth Memory (HBM3, HBM3E, HBM4) Market?

-> Global High Bandwidth Memory (HBM3, HBM3E, HBM4) Market was valued at USD 4.21 billion in 2025 and is projected to grow from USD 5.38 billion in 2026 to USD 51.24 billion by 2034, exhibiting a CAGR of 28.4% during the forecast period.

Which key companies operate in High Bandwidth Memory (HBM3, HBM3E, HBM4) Market?

-> Key players include SK Hynix, Samsung Electronics, and Micron Technology, among others. These companies are actively scaling HBM3E output while advancing HBM4 development to meet surging demand from hyperscale cloud providers and AI hardware manufacturers worldwide.

What are the key growth drivers?

-> Key growth drivers include accelerating demand for AI and machine learning workloads, high-performance computing (HPC), and next-generation data center infrastructure. The explosive adoption of large language models (LLMs) and generative AI platforms has created unprecedented demand for memory solutions capable of feeding massive compute clusters with data at extreme speeds.

Which region dominates the market?

-> Asia-Pacific is a leading region in the High Bandwidth Memory market, driven by major semiconductor manufacturers such as SK Hynix and Samsung Electronics, which are headquartered in South Korea and are key suppliers of HBM3E and HBM4 technologies to global AI hardware manufacturers.

What are the emerging trends?

-> Emerging trends include mass production of HBM3E, advancement toward HBM4 development, and integration of high bandwidth memory into next-generation GPU architectures such as NVIDIA’s H200 and Blackwell platforms. Additionally, the use of through-silicon via (TSV) interconnects enabling up to 819 GB/s bandwidth per stack in HBM3 represents a significant technological advancement shaping the market.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...