Focal Plane Array (FPA) for IR Imaging Market Insights

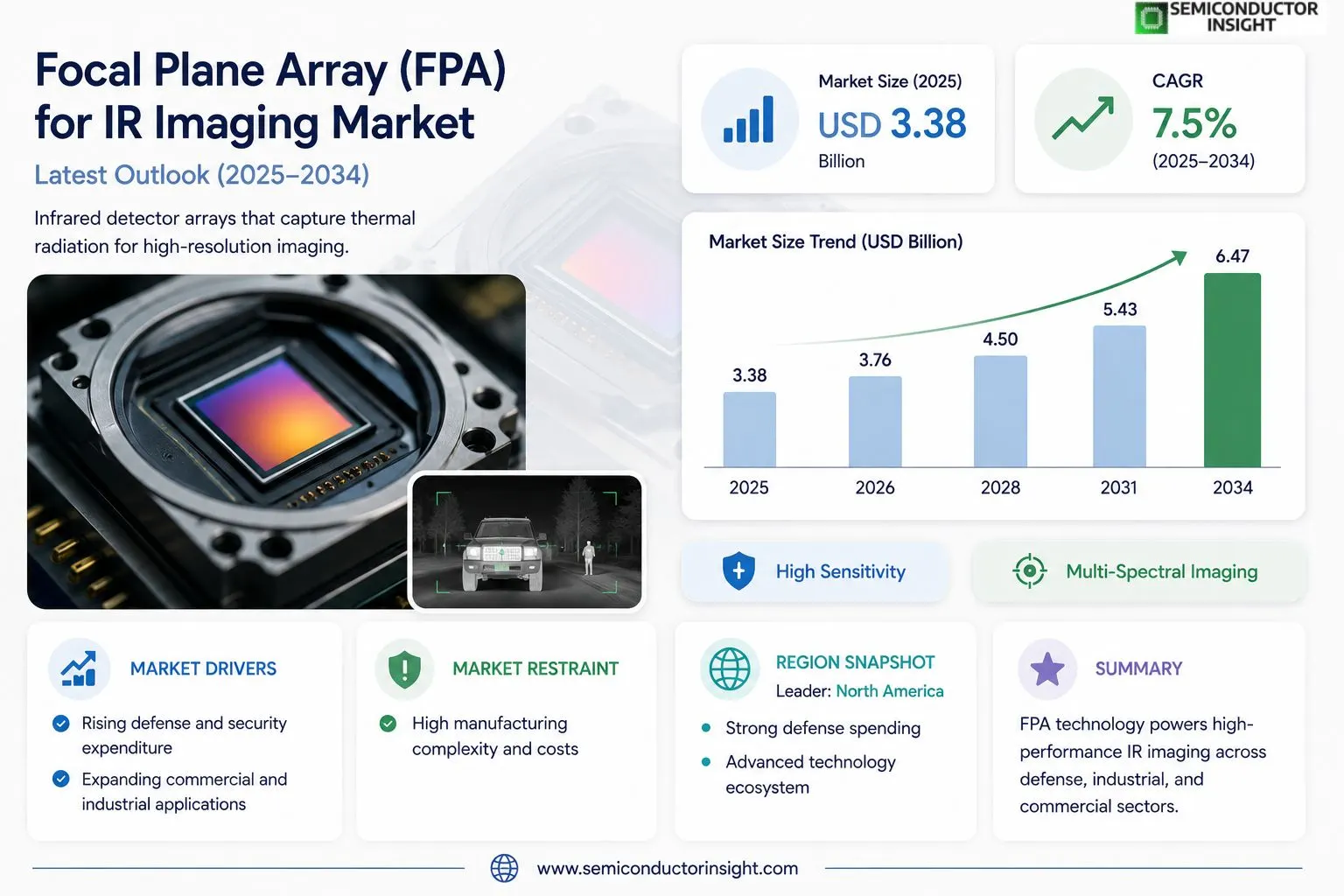

Global Focal Plane Array (FPA) for IR Imaging market size was valued at USD 3.12 billion in 2024. The market is projected to grow from USD 3.38 billion in 2025 to USD 6.47 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period.

Focal Plane Arrays (FPAs) are two-dimensional arrays of photodetector elements positioned at the focal plane of an imaging system, specifically engineered to detect infrared radiation emitted by objects. These detector arrays are central to a wide range of infrared imaging applications and are manufactured using materials such as indium antimonide (InSb), mercury cadmium telluride (MCT or HgCdTe), indium gallium arsenide (InGaAs), and vanadium oxide-based microbolometers, each suited to distinct spectral bands including short-wave infrared (SWIR), mid-wave infrared (MWIR), and long-wave infrared (LWIR).

The market is witnessing robust expansion driven by escalating defense procurement budgets, growing adoption of thermal imaging in commercial and industrial sectors, and rapid advancements in detector sensitivity and resolution. Furthermore, the proliferation of FPA-based systems in medical thermography, automotive night vision, border surveillance, and space-based Earth observation is broadening the addressable market considerably. Strategic initiatives by leading industry participants are also reinforcing growth momentum. FLIR Systems (now part of Teledyne Technologies), Raytheon Technologies, Leonardo DRS, and Lynred are among the prominent players operating in the Focal Plane Array for IR Imaging market with extensive and diversified product portfolios spanning both cooled and uncooled detector platforms.

MARKET DRIVERS

Rising Defense and Security Expenditure Fueling Demand for IR Imaging Systems

Global defense modernization programs have become one of the most powerful catalysts for Focal Plane Array (FPA) for IR Imaging Market. Governments across North America, Europe, and the Asia-Pacific region are significantly increasing their defense budgets, channeling substantial investments toward advanced surveillance, targeting, and reconnaissance systems. Focal Plane Array detectors serve as the core sensing element in thermal imaging equipment used in night-vision goggles, missile guidance systems, airborne surveillance platforms, and border security installations. As geopolitical tensions persist and military forces seek technological superiority, the procurement of high-resolution infrared imaging solutions continues to accelerate, directly driving volume demand for FPA components across both cooled and uncooled detector categories.

Expanding Commercial and Industrial Applications Broadening the FPA Addressable Market

Beyond defense, the Focal Plane Array (FPA) for IR Imaging landscape is being reshaped by robust growth in commercial verticals including industrial thermography, predictive maintenance, automotive advanced driver-assistance systems (ADAS), and medical diagnostics. In industrial settings, infrared cameras equipped with FPA detectors enable non-contact temperature measurement and early detection of equipment failures, reducing unplanned downtime and operational costs. The automotive sector’s transition toward autonomous and semi-autonomous vehicles has introduced new requirements for long-wave infrared (LWIR) sensors that can detect pedestrians and obstacles in low-visibility conditions. Simultaneously, the medical sector’s adoption of thermal imaging for fever screening and vascular diagnostics continues to expand the commercial footprint of IR FPA technology.

➤ The integration of Focal Plane Array technology into next-generation ADAS platforms and autonomous vehicle systems represents one of the most significant volume growth opportunities for uncooled IR FPA manufacturers over the coming decade, as automotive OEMs increasingly adopt thermal sensing as a standard safety feature.

Technological advancements in detector materials,particularly the transition from traditional indium antimonide (InSb) and mercury cadmium telluride (MCT/HgCdTe) toward emerging alternatives such as type-II superlattice (T2SL) and quantum dot infrared photodetectors (QDIP),are enhancing sensitivity, reducing production costs, and improving operational temperature ranges. These material innovations are enabling manufacturers to develop smaller, lighter, and more power-efficient FPA modules, making infrared imaging accessible to a broader range of end-use applications and driving overall market expansion.

MARKET CHALLENGES

High Manufacturing Complexity and Cost Barriers Constraining Wider Market Penetration

Despite strong demand signals, Focal Plane Array (FPA) for IR Imaging Market faces persistent challenges rooted in the inherent complexity of FPA fabrication. Cooled FPA detectors, which offer superior sensitivity and are preferred in high-performance defense and scientific applications, require cryogenic cooling systems and are manufactured using sophisticated epitaxial growth processes under stringent cleanroom conditions. The capital-intensive nature of these processes translates into elevated per-unit costs that limit adoption among cost-sensitive commercial buyers. Furthermore, achieving consistent pixel uniformity and minimizing detector non-uniformity correction (NUC) requirements across large-format arrays remains technically demanding, leading to relatively low manufacturing yields and contributing to supply-side constraints within the industry.

Other Challenges

Export Control and Regulatory Restrictions

Infrared FPA technology is subject to stringent international export controls, including the U.S. International Traffic in Arms Regulations (ITAR) and Export Administration Regulations (EAR), as well as equivalent frameworks in the European Union and other jurisdictions. These regulations significantly complicate Global distribution of high-performance FPA detectors and limit the ability of manufacturers to serve certain international markets. Compliance obligations increase administrative and legal costs for both established players and new entrants, while also creating barriers to international partnerships and technology transfer arrangements that could otherwise accelerate innovation and scale economies within the Focal Plane Array for IR Imaging supply chain.

Talent Scarcity in Specialized Engineering Disciplines

The design, development, and production of Focal Plane Array detectors demand highly specialized expertise spanning semiconductor physics, cryogenics, optical engineering, and readout integrated circuit (ROIC) design. Global talent pool for professionals with this combination of competencies remains limited, creating recruitment and retention challenges for manufacturers seeking to scale operations or accelerate product development cycles. This scarcity of qualified engineering talent is particularly acute in emerging market economies where the infrared imaging industry is at an earlier stage of development, potentially limiting the geographic diversification of Global FPA supply base over the near to medium term.

MARKET RESTRAINTS

Technological Substitution Risk from Alternative Sensing Modalities

Focal Plane Array (FPA) for IR Imaging Market faces a meaningful restraint from competing sensing technologies that offer overlapping functional capabilities at potentially lower costs. LiDAR systems, radar-based sensors, and advanced visible-spectrum low-light cameras have made significant performance improvements in recent years, positioning them as viable alternatives or complements to infrared FPA solutions in certain application segments,particularly automotive perception and short-range surveillance. While IR FPA technology retains distinct advantages in passive thermal detection and through-obscurant imaging, the continuous improvement of competing modalities exerts pricing pressure and may limit FPA adoption growth in applications where thermal imaging does not provide an insurmountable performance advantage.

Supply Chain Vulnerabilities and Critical Material Dependencies

The production of high-performance Focal Plane Array detectors for infrared imaging is dependent on a limited number of specialty substrate materials and rare compounds, including tellurium, indium, and antimony, whose global supply chains are geographically concentrated and susceptible to geopolitical disruption. The fabrication of MCT-based FPAs, in particular, relies on cadmium telluride substrates sourced from a small number of qualified suppliers, creating single-source dependency risks that can disrupt manufacturing continuity. Additionally, the specialized molecular beam epitaxy (MBE) and metal-organic chemical vapor deposition (MOCVD) equipment required for FPA detector growth is produced by a narrow base of equipment manufacturers, further concentrating supply-side risk and limiting the flexibility of FPA producers to rapidly scale capacity in response to demand surges.

MARKET OPPORTUNITIES

Emergence of Space-Based Infrared Sensing as a High-Growth Application Vertical

The growing commercialization of space and the expansion of government satellite programs present a compelling long-term opportunity for Focal Plane Array (FPA) for IR Imaging Market. Earth observation satellites, missile warning systems, and space situational awareness platforms rely on specialized infrared FPA detectors capable of operating reliably under the extreme thermal cycling and radiation environments encountered in orbit. The rapid proliferation of small satellite constellations by commercial operators and national space agencies is generating incremental demand for compact, radiation-hardened IR FPA modules. As launch costs continue to decline and the satellite industry scales, manufacturers capable of delivering space-qualified FPA detectors with proven heritage are well-positioned to capture significant revenue growth from this emerging application segment.

Integration of AI and Machine Learning Enhancing Value Proposition of FPA-Based Systems

The convergence of Focal Plane Array infrared imaging technology with artificial intelligence and machine learning-based image processing represents a transformative opportunity to enhance the analytical value and operational utility of IR imaging systems. AI-enabled FPA systems can autonomously detect, classify, and track objects of interest within thermal imagery in real time, reducing operator workload and enabling deployment in unmanned platforms. In industrial and infrastructure monitoring applications, AI-augmented infrared imaging powered by FPA detectors can deliver predictive maintenance insights and anomaly detection at scale, unlocking subscription-based software revenue models that complement traditional hardware sales. This fusion of FPA hardware with intelligent software layers is expected to expand addressable markets, improve system margins, and attract new categories of end users to infrared imaging solutions over the forecast horizon.

Growing Adoption of Uncooled FPA Technology in Emerging Economy Markets

Ongoing cost reduction in uncooled microbolometer-based Focal Plane Array detectors is progressively lowering the entry barrier for infrared imaging adoption across emerging economy markets in Asia-Pacific, Latin America, the Middle East, and Africa. As governments and enterprises in these regions invest in smart city infrastructure, border surveillance, firefighting equipment, and industrial automation, the demand for affordable, maintenance-free thermal imaging solutions based on uncooled FPA technology is expected to grow at an above-average rate. Domestic manufacturing initiatives in countries such as China and India,supported by government incentives and technology localization policies,are also creating new production hubs that may further reduce system costs and accelerate market penetration, presenting both competitive challenges and partnership opportunities for established global FPA manufacturers.

Focal Plane Array (FPA) for IR Imaging Market Trends

Rising Defense Procurement Driving Demand for Advanced IR Imaging Systems

Focal Plane Array (FPA) for IR Imaging Market is experiencing sustained momentum, largely propelled by escalating defense budgets across North America, Europe, and the Asia-Pacific region. Military modernization programs have intensified procurement of high-performance cooled and uncooled FPA-based systems for applications including missile guidance, airborne surveillance, and soldier-worn thermal optics. Cooled detectors utilizing materials such as mercury cadmium telluride (HgCdTe) and indium antimonide (InSb) remain preferred in defense-grade platforms owing to their superior sensitivity across mid-wave infrared (MWIR) and long-wave infrared (LWIR) spectral bands. Leading players such as Raytheon Technologies, Leonardo DRS, and FLIR Systems , now operating under Teledyne Technologies , continue to expand their cooled detector portfolios to address increasingly complex threat environments.

Other Trends

Commercial and Industrial Adoption of Uncooled FPA Technology

Beyond defense, the Focal Plane Array for IR Imaging market is witnessing accelerating adoption of uncooled microbolometer-based FPAs across commercial and industrial verticals. Vanadium oxide-based microbolometers, valued for their lower cost, compact form factor, and reduced power consumption, are enabling deployment in predictive maintenance, building diagnostics, and industrial process monitoring. The automotive sector represents a particularly dynamic growth avenue, with FPA-based night vision systems being integrated into advanced driver assistance systems (ADAS) to improve pedestrian detection and road safety in low-visibility conditions.

Medical Thermography and Border Surveillance Expanding Addressable Applications

Medical thermography utilizing FPA-based infrared cameras has gained renewed attention as healthcare providers increasingly adopt non-contact thermal screening solutions. Concurrently, border security agencies globally are deploying long-range FPA-enabled surveillance systems to enhance perimeter monitoring capabilities. These dual-use applications are broadening the addressable market for infrared imaging detectors considerably, drawing participation from both established defense contractors and specialized commercial imaging firms such as Lynred.

Technological Advancements in Detector Sensitivity and Resolution Reshaping Market Landscape

Continuous innovation in detector materials and fabrication processes is a defining trend within the Focal Plane Array for IR Imaging market. Advances in indium gallium arsenide (InGaAs) detectors are enabling improved short-wave infrared (SWIR) imaging performance for machine vision and telecommunications applications. Simultaneously, ongoing progress in pixel pitch reduction , enabling higher-resolution arrays within compact packaging , is expanding FPA utility in space-based Earth observation programs. These technological developments, supported by strategic R&D investments from key industry participants, are reinforcing competitive differentiation and sustaining long-term growth momentum across Global infrared imaging ecosystem.

COMPETITIVE LANDSCAPE

Key Industry Players

Focal Plane Array (FPA) for IR Imaging Market: Competitive Dynamics and Leading Industry Participants

Global Focal Plane Array (FPA) for IR Imaging market is characterized by a moderately consolidated competitive structure, with a handful of technologically advanced defense and photonics-focused corporations commanding significant market share. Teledyne Technologies, through its acquisition of FLIR Systems, has emerged as a dominant force in the FPA landscape, offering an extensive portfolio spanning cooled and uncooled detector platforms across SWIR, MWIR, and LWIR spectral bands. Raytheon Technologies and Leonardo DRS further anchor the competitive hierarchy, leveraging deep-rooted defense contracts, proprietary detector fabrication capabilities, and vertically integrated manufacturing to maintain durable competitive moats. These leading players benefit from sustained demand driven by escalating global defense procurement budgets, border surveillance modernization programs, and the growing integration of thermal imaging into advanced airborne and space-based Earth observation systems. Continued investment in detector sensitivity enhancement and resolution scaling remains a defining competitive differentiator among top-tier participants.

Beyond the dominant players, the Focal Plane Array for IR Imaging market hosts a dynamic set of specialized manufacturers and technology innovators contributing to a broadening competitive ecosystem. Lynred, a European leader in infrared detector technology, commands a strong position particularly in cooled HgCdTe-based FPA solutions for aerospace and scientific applications. Sofradir’s legacy capabilities, now consolidated under Lynred, and Xenics’ expertise in InGaAs and SWIR imaging further diversify the European competitive landscape. In the United States, companies such as DRS Technologies (a Leonardo DRS subsidiary), SCD (Semi Conductor Devices), and Sierra Nevada Corporation contribute to niche high-performance cooled FPA segments. Emerging players including Vigo System, IRnova, and Infrared Focal Plane are advancing next-generation detector materials and chip architectures targeting commercial thermography, automotive night vision, and industrial predictive maintenance applications. Collectively, these participants are accelerating market expansion, which is projected to grow from USD 3.38 billion in 2025 to USD 6.47 billion by 2034 at a CAGR of 7.5%.

List of Key Focal Plane Array (FPA) for IR Imaging Companies Profiled

- Teledyne Technologies (FLIR Systems)

- Raytheon Technologies

- Leonardo DRS

- Lynred

- SCD (Semi Conductor Devices)

- Xenics

- IRnova

- Vigo System

- Sierra Nevada Corporation

- Infrared Focal Plane

- L3Harris Technologies

- Northrop Grumman Corporation

- BAE Systems

- Photon etc.

- New Infrared Technologies (NIT)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cooled FPA continues to dominate the premium performance tier of the market, driven by its unrivaled sensitivity and resolution in demanding operational environments.

|

| By Application |

|

Defense & Surveillance remains the foremost application segment, underpinned by sustained and escalating global defense procurement investments and the strategic imperative for advanced situational awareness capabilities.

|

| By End User |

|

Defense & Military end users constitute the largest and most strategically significant buyer segment for FPA-based IR imaging systems, consistently driving demand for the highest-performance cooled detector solutions.

|

| By Spectral Band |

|

Long-Wave Infrared (LWIR) holds the broadest deployment footprint across the FPA for IR Imaging market, owing to its alignment with the peak thermal emission characteristics of objects at ambient temperatures, making it the spectral band of choice for the widest range of commercial and military applications.

|

| By Detector Material |

|

Mercury Cadmium Telluride (MCT/HgCdTe) retains its position as the leading detector material for high-performance FPA applications, prized for its tunable bandgap, exceptional quantum efficiency, and versatility across multiple infrared spectral bands.

|

Regional Analysis: Focal Plane Array (FPA) for IR Imaging Market

North America

North America’s defense sector remains the single most influential driver of Focal Plane Array (FPA) for IR Imaging market growth in the region. Continuous modernization programs across military branches sustain demand for high-sensitivity infrared detector arrays used in targeting, surveillance, and situational awareness platforms. Long-term procurement contracts and classified research initiatives further entrench the region’s leadership in this technology vertical.

Beyond defense, commercial industries across North America are integrating FPA-based infrared imaging systems into predictive maintenance, energy auditing, and smart manufacturing workflows. The industrial thermography segment has seen growing uptake as facilities seek non-contact diagnostic tools capable of detecting anomalies in real time. This diversification of end-use applications is helping Focal Plane Array (FPA) for IR Imaging Market expand its commercial footprint across the region.

The concentration of semiconductor fabrication expertise, university research programs, and federal funding mechanisms has positioned North America as a global innovation hub for infrared detector technology. Collaborative efforts between government agencies and private sensor developers continue to advance detector sensitivity, miniaturization, and integration capabilities. These sustained innovation pipelines ensure the region remains at the forefront of Focal Plane Array (FPA) for IR Imaging Market landscape.

The United States government maintains stringent export control frameworks governing the transfer of advanced infrared imaging technologies, particularly those with dual-use applicability. While these regulations protect strategic interests, they also shape competitive dynamics by limiting certain forms of international technology sharing. For domestic players in Focal Plane Array (FPA) for IR Imaging Market, navigating these compliance requirements is integral to their international expansion and partnership strategies.

Europe

Europe represents a significant and steadily evolving market for Focal Plane Array (FPA) for IR Imaging technologies, underpinned by strong defense collaboration frameworks, substantial research funding, and growing commercial applications. Countries such as France, Germany, and the United Kingdom have historically maintained advanced domestic capabilities in infrared sensor development, supported by both national defense programs and pan-European initiatives. The European Defence Agency and various Horizon-funded research programs have catalyzed innovation in infrared imaging, creating fertile ground for both established manufacturers and emerging technology firms. The region’s industrial base has embraced IR imaging solutions across automotive night vision systems, building inspection, and medical thermography. Additionally, Europe’s emphasis on energy efficiency and sustainable infrastructure has generated new demand for thermal imaging tools used in building diagnostics and renewable energy monitoring. As geopolitical pressures continue to shape defense spending priorities across NATO member states, Focal Plane Array (FPA) for IR Imaging Market in Europe is expected to benefit from renewed investment in border security, airborne surveillance, and next-generation soldier systems throughout the forecast period.

Asia-Pacific

Asia-Pacific is emerging as one of the most dynamic and fastest-growing regions in Global Focal Plane Array (FPA) for IR Imaging market, driven by escalating defense modernization efforts, expanding industrial automation, and significant government investment in domestic sensor manufacturing capabilities. China, Japan, South Korea, and India are at the forefront of this regional expansion, each pursuing distinct but complementary strategies to develop or acquire advanced infrared imaging technologies. China’s ambitious military modernization agenda and growing domestic semiconductor industry have accelerated indigenous development of FPA-based IR imaging systems. Japan and South Korea bring deep electronics manufacturing expertise that supports both defense and commercial infrared applications. India’s increasing defense procurement budgets and push for self-reliance in strategic technologies are creating new avenues for market growth. The proliferation of smart city infrastructure, automotive advanced driver assistance systems (ADAS), and industrial automation across the region further broadens the commercial demand base for Focal Plane Array (FPA) for IR Imaging Market.

South America

South America occupies a developing position in Global Focal Plane Array (FPA) for IR Imaging market, with market growth primarily concentrated in Brazil and, to a lesser extent, Colombia and Argentina. Brazil’s defense sector has demonstrated a consistent interest in upgrading surveillance and border monitoring capabilities, particularly given the country’s vast and challenging geographic terrain. IR imaging technologies are increasingly being deployed for environmental monitoring, deforestation detection, and wildfire surveillance across the Amazon basin, creating a unique regional use case that distinguishes South America from other markets. Industrial applications in mining, oil and gas, and power generation also contribute to demand for thermal imaging solutions. However, economic volatility, limited local manufacturing infrastructure, and import dependency remain structural constraints that temper the pace of market expansion. As regional governments prioritize public safety and environmental stewardship, Focal Plane Array (FPA) for IR Imaging Market in South America is expected to achieve measured but meaningful growth over the coming years.

Middle East & Africa

The Middle East and Africa region presents a strategically important, if uneven, landscape for Focal Plane Array (FPA) for IR Imaging Market. In the Middle East, Gulf Cooperation Council nations , particularly Saudi Arabia, the UAE, and Israel , represent the primary growth engines, fueled by substantial defense budgets, advanced military procurement programs, and growing investments in border security infrastructure. Israel’s highly sophisticated defense technology industry has long been a significant contributor to global infrared imaging innovation, with its capabilities frequently integrated into regional and international security platforms. In Africa, market development remains nascent but is gaining traction in areas such as wildlife conservation, anti-poaching surveillance, and public safety monitoring. The continent’s expanding power and utility sector also offers incremental opportunities for thermal inspection applications. While infrastructure limitations and procurement constraints continue to present challenges, increasing international defense partnerships and development funding are expected to gradually unlock Focal Plane Array (FPA) for IR Imaging Market’s potential across the broader Middle East and Africa region during the forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Focal Plane Array (FPA) for IR Imaging Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Focal Plane Array (FPA) for IR Imaging Market?

-> Global Focal Plane Array (FPA) for IR Imaging Market was valued at USD 3.38 billion in 2025 and is expected to reach USD 6.47 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period.

Which key companies operate in Focal Plane Array (FPA) for IR Imaging Market?

-> Key players include FLIR Systems (now part of Teledyne Technologies), Raytheon Technologies, Leonardo DRS, and Lynred, among others, with extensive and diversified product portfolios spanning both cooled and uncooled detector platforms.

What are the key growth drivers?

-> Key growth drivers include escalating defense procurement budgets, growing adoption of thermal imaging in commercial and industrial sectors, rapid advancements in detector sensitivity and resolution, and the proliferation of FPA-based systems in medical thermography, automotive night vision, border surveillance, and space-based Earth observation.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market driven by strong defense procurement and advanced technology adoption.

What are the emerging trends?

-> Emerging trends include advancements in detector materials such as indium antimonide (InSb), mercury cadmium telluride (HgCdTe), and indium gallium arsenide (InGaAs), integration of AI-enabled thermal imaging systems, miniaturization of FPA modules, and expanded use across SWIR, MWIR, and LWIR spectral bands for next-generation infrared imaging applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...