DNA Data Storage Enablement Chip Market Insights

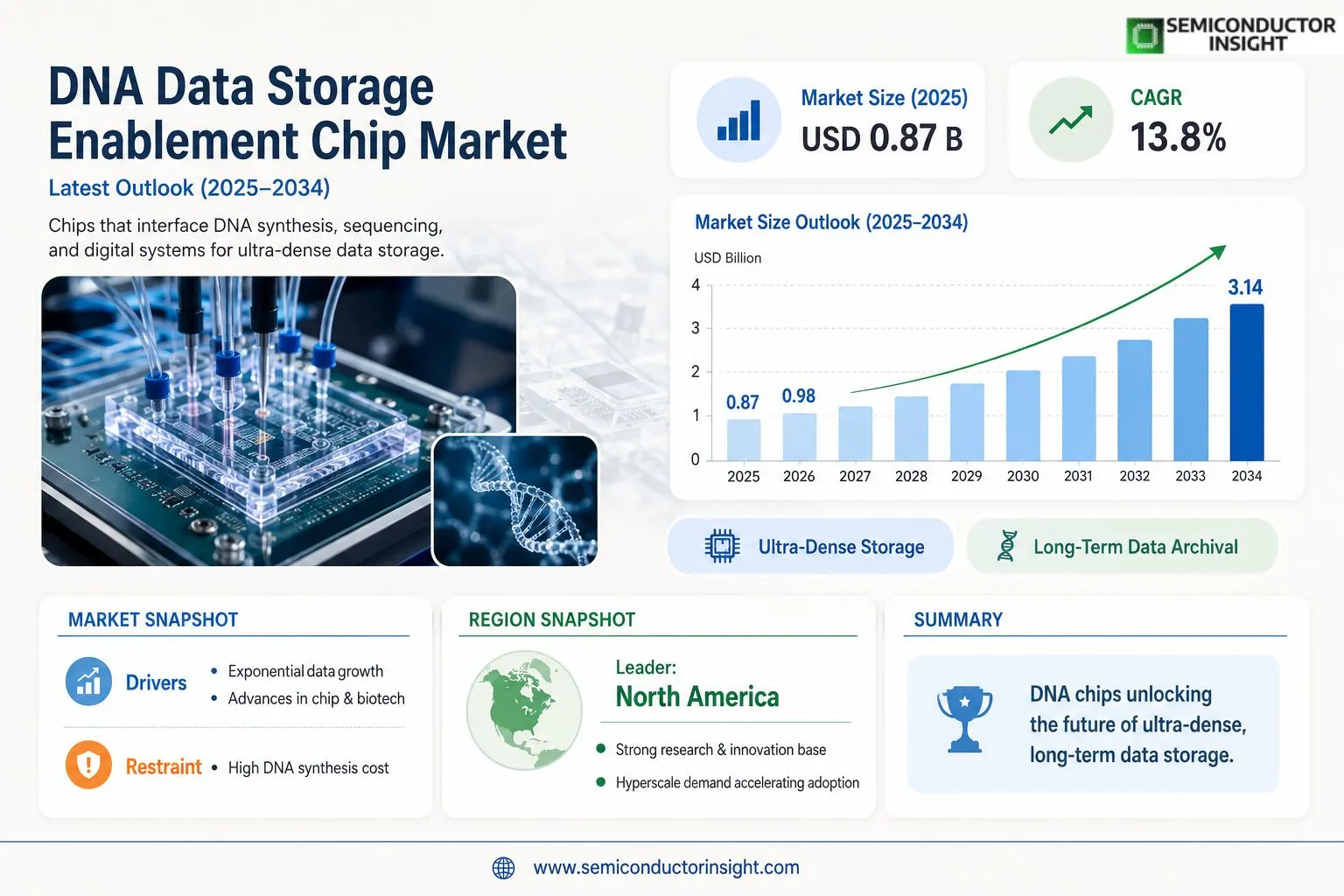

DNA Data Storage Enablement Chip Market size was valued at USD 0.87 billion in 2025. The market is projected to grow from USD 0.98 billion in 2026 to USD 3.14 billion by 2034, exhibiting a CAGR of 13.8% during the forecast period.

DNA data storage enablement chips are specialized semiconductor and microfluidic devices designed to interface biological DNA synthesis, sequencing, and retrieval processes with digital data systems. These chips facilitate the encoding of binary data into nucleotide sequences and the subsequent decoding of stored information, supporting key operations such as oligonucleotide synthesis, error correction, random access retrieval, and parallel read/write processing. The technology spans application-specific integrated circuits (ASICs), field-programmable gate arrays (FPGAs), and hybrid bio-electronic chip architectures engineered specifically for high-density, long-term data archival.

The market is gaining significant momentum driven by the exponential growth of global data volumes, with the global datasphere projected to reach 175 zettabytes, creating urgent demand for ultra-dense, energy-efficient storage alternatives. Furthermore, increasing investment from hyperscale cloud providers and government-backed research programs into next-generation storage infrastructure is accelerating commercialization. Notable industry activity reinforces this trajectory , in 2023, Microsoft and University of Washington advanced their DNA storage platform demonstrating automated end-to-end data storage and retrieval, while Catalog Technologies reported writing 200 MB of data onto DNA using its proprietary enzymatic synthesis platform. Companies such as Twist Bioscience, Illumina, and Intel are among the key players actively contributing to this evolving market landscape.

MARKET DRIVERS

Exponential Growth in Global Data Volumes Fueling Demand for DNA-Based Storage Solutions

The rapid acceleration of data generation across industries , from genomics and cloud computing to artificial intelligence and the Internet of Things , is placing extraordinary pressure on conventional storage technologies. Hard disk drives and flash memory face well-documented limitations in terms of physical density, energy consumption, and longevity. DNA Data Storage Enablement Chip Market is emerging as a critical response to these constraints, as DNA-based chips facilitate the encoding, writing, and retrieval of digital data using synthetic DNA strands. With global data volumes projected to reach hundreds of zettabytes in the coming decade, the structural demand for high-density, durable storage architectures is intensifying rapidly.

Advances in Semiconductor Integration and Synthetic Biology Accelerating Chip Development

A convergence of progress in semiconductor fabrication and synthetic biology is enabling the development of more capable and miniaturized enablement chips for DNA data storage. Modern chip architectures are being designed to interface directly with DNA synthesis and sequencing workflows, dramatically reducing the time and cost associated with read and write operations. Companies and research institutions developing DNA data storage enablement chips are leveraging advances in microfluidics, electrochemical synthesis, and CMOS-compatible manufacturing to bring viable prototypes closer to commercial deployment. This interdisciplinary innovation pipeline is a central driver shaping competitive dynamics in the market.

➤ Institutional investment from both government agencies and private venture capital into DNA-based data technologies has grown substantially, with national data infrastructure programs in the United States, European Union, and Asia-Pacific regions increasingly recognizing synthetic biology storage as a strategic priority.

Long-term data archiving requirements across sectors such as healthcare, defense, legal compliance, and digital media are creating sustained demand for storage solutions capable of preserving information reliably for decades or centuries. DNA, as a storage medium, offers theoretical density and stability advantages that silicon-based media cannot match. DNA Data Storage Enablement Chip Market benefits directly from this archival demand, as enablement chips serve as the essential hardware interface enabling practical implementation of DNA storage pipelines at scale.

MARKET CHALLENGES

High Cost of DNA Synthesis and Sequencing Constraining Near-Term Commercial Scalability

Despite significant technological promise, the DNA data storage enablement chip sector faces substantial cost barriers that constrain its near-term commercial scalability. The per-base cost of oligonucleotide synthesis, while declining, remains orders of magnitude higher than the per-bit cost of conventional storage media. Enablement chips must integrate tightly with synthesis and sequencing hardware, meaning that total system costs compound across the storage pipeline. Until synthesis costs reach economically viable thresholds for enterprise or consumer deployment, the addressable market for DNA data storage chips will remain concentrated in high-value, specialized use cases such as long-term archival storage and classified data preservation.

Other Challenges

Slow Read and Write Speeds Relative to Conventional Storage Media

Current DNA synthesis and sequencing processes operate at speeds that are significantly slower than electronic storage alternatives. While DNA Data Storage Enablement Chip Market is advancing toward faster enzymatic synthesis methods and nanopore-based sequencing interfaces, achieving competitive data throughput remains a central engineering challenge. Chip designs must account for parallelization strategies and error-correction protocols that add complexity and cost to the overall system architecture.

Error Rates and Data Integrity Concerns in Encoding Workflows

DNA synthesis is inherently prone to insertion, deletion, and substitution errors, and the enablement chips responsible for managing encoding and decoding workflows must incorporate robust error-correction algorithms. Ensuring data fidelity across repeated read cycles and long-term storage conditions presents ongoing technical challenges. Standardization of error-correction frameworks across chip platforms has yet to mature, creating interoperability concerns for enterprises evaluating the DNA data storage enablement chip ecosystem.

MARKET RESTRAINTS

Absence of Industry-Wide Standards and Regulatory Frameworks Limiting Market Expansion

DNA Data Storage Enablement Chip Market currently operates without established industry-wide technical standards governing chip interfaces, data encoding formats, or compatibility between competing platforms. This fragmentation creates significant uncertainty for enterprise buyers and system integrators who require interoperability assurances before committing to infrastructure investments. The lack of standardized protocols also complicates regulatory classification, particularly in jurisdictions where DNA-based technologies intersect with biosafety, biosecurity, and data sovereignty regulations. Until coherent regulatory and technical frameworks emerge, many potential adopters are expected to maintain a cautious stance.

Limited Ecosystem of Supporting Infrastructure and Skilled Workforce Availability

Commercialization of the DNA data storage enablement chip technology requires a supporting ecosystem that includes compatible synthesis hardware, sequencing platforms, biochemical reagents, and specialized software for encoding and retrieval. This ecosystem is nascent and unevenly distributed geographically, creating supply chain dependencies and deployment barriers for organizations outside major research and technology hubs. Furthermore, the interdisciplinary expertise required to develop, deploy, and maintain DNA storage chip systems , spanning molecular biology, semiconductor engineering, and data science , is scarce, limiting the pace at which organizations can build internal capabilities. These structural ecosystem gaps represent meaningful restraints on the market’s growth trajectory over the medium term.

MARKET OPPORTUNITIES

Strategic Partnerships Between Semiconductor Firms and Synthetic Biology Companies Opening New Development Pathways

The intersection of semiconductor manufacturing expertise and synthetic biology innovation is creating significant partnership opportunities that could accelerate the commercialization of DNA Data Storage Enablement Chip Market. Established chip manufacturers possess the fabrication infrastructure, quality control processes, and supply chain relationships needed to scale production, while synthetic biology firms bring proprietary DNA synthesis chemistries and encoding algorithms. Collaborative development agreements and licensing arrangements between these two communities are expected to compress the timeline to commercially viable products, broadening the competitive landscape and creating new revenue streams for early movers in the enablement chip space.

Growing Adoption of Cold Data Archival Applications in Healthcare, Government, and Media Sectors

Sectors with large-scale, long-retention data archival requirements represent a high-priority opportunity for the DNA data storage enablement chip industry. Healthcare organizations managing genomic databases, imaging archives, and longitudinal patient records are generating cold data at rates that strain conventional tape and disk-based archival systems. Similarly, national archives, defense agencies, and entertainment content libraries require cost-effective, durable storage for data that is infrequently accessed but must be preserved with complete integrity for extended periods. Enablement chips that can support reliable, cost-efficient DNA-based archival workflows in these verticals stand to capture substantial market share as the technology matures and per-unit economics improve.

Emerging Role of Enzymatic DNA Synthesis in Reducing Costs and Improving Chip Performance

Enzymatic DNA synthesis represents a promising technological shift that could meaningfully improve both the economics and performance profile of DNA data storage enablement chips. Unlike conventional phosphoramidite chemistry, enzymatic approaches operate under aqueous conditions at ambient temperatures, offering compatibility with chip-integrated microfluidic architectures and the potential for faster synthesis cycles with reduced reagent consumption. As enzymatic synthesis methodologies continue to mature, they are expected to enable a new generation of enablement chips with higher throughput, lower error rates, and reduced operational costs. Market participants investing in enzymatic synthesis integration are well-positioned to differentiate their chip offerings and address the cost barriers currently restraining broader adoption of DNA-based data storage solutions.

DNA Data Storage Enablement Chip Market Trends

Rising Data Volumes Accelerating Demand for DNA Data Storage Enablement Chips

DNA Data Storage Enablement Chip Market is witnessing accelerating momentum as global data generation reaches unprecedented scales. With the global datasphere projected to reach 175 zettabytes, enterprises and cloud providers are actively seeking ultra-dense, energy-efficient alternatives to conventional storage media. DNA data storage enablement chips , encompassing ASICs, FPGAs, and hybrid bio-electronic architectures , are emerging as a transformative solution, capable of encoding binary data into nucleotide sequences with remarkable density and longevity. This fundamental shift in storage infrastructure is reshaping how the technology and data industries approach long-term archival challenges.

Other Trends

Hyperscale Cloud Investment Driving Commercialization

Increasing capital allocation from hyperscale cloud providers and government-backed research initiatives is significantly accelerating the commercialization of DNA data storage enablement chips. These investments are enabling the transition from laboratory-scale demonstrations to scalable, deployment-ready platforms. The convergence of semiconductor engineering and synthetic biology is attracting cross-sector collaboration, with technology firms and life sciences companies jointly developing chip architectures optimized for high-throughput oligonucleotide synthesis, error correction, and parallel read/write processing , key functional requirements for viable commercial deployment.

Industry Milestones Validating Technology Readiness

Notable industry activity continues to validate the commercial readiness of DNA Data Storage Enablement Chip Market. In 2023, Microsoft and the University of Washington advanced their DNA storage platform by demonstrating automated end-to-end data storage and retrieval. Separately, Catalog Technologies reported successfully writing 200 MB of data onto DNA using its proprietary enzymatic synthesis platform. These milestones reflect a broader industry trend toward automation and scalability, signaling that the DNA data storage enablement chip ecosystem is progressing beyond proof-of-concept toward practical implementation.

Expanding Role of Key Market Players in Shaping the DNA Data Storage Enablement Chip Landscape

Prominent companies including Twist Bioscience, Illumina, and Intel are actively contributing to the evolution of DNA Data Storage Enablement Chip Market, each bringing distinct competencies in synthesis, sequencing, and semiconductor design. Their participation is fostering a competitive and collaborative ecosystem where chip-level innovation is advancing in tandem with biological process optimization. As random access retrieval capabilities improve and synthesis costs decline, DNA Data Storage Enablement Chip Market is expected to attract broader adoption across data-intensive sectors including cloud computing, healthcare informatics, and government archival infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

DNA Data Storage Enablement Chip Market: Competitive Dynamics and Leading Innovators Shaping Next-Generation Biological Data Storage Infrastructure

DNA Data Storage Enablement Chip Market is characterized by a dynamic mix of established semiconductor giants, specialized biotechnology firms, and well-funded deep-tech startups competing across chip architecture design, oligonucleotide synthesis platforms, and bio-electronic integration. Microsoft remains one of the most prominent institutional players in this space, having advanced its DNA storage platform in collaboration with the University of Washington to demonstrate fully automated end-to-end data encoding and retrieval. Intel contributes foundational semiconductor expertise, particularly in the development of application-specific integrated circuits (ASICs) and field-programmable gate arrays (FPGAs) tailored for biological data interfacing. Twist Bioscience and Illumina are equally significant, with Twist providing high-throughput DNA synthesis capabilities and Illumina offering sequencing infrastructure that underpins read operations critical to data retrieval workflows. Catalog Technologies has distinguished itself by reporting the encoding of 200 MB of data onto DNA using its proprietary enzymatic synthesis platform, positioning it as a key commercialization-stage innovator.

Beyond the market frontrunners, a number of niche yet strategically significant players are expanding the competitive perimeter of the DNA data storage enablement chip landscape. Iridia Inc. is pioneering electrochemical DNA synthesis chip technology, while Molecular Assemblies focuses on enzymatic DNA synthesis approaches that reduce synthesis error rates and improve throughput efficiency. DNA Script, a Paris-based biotech, has developed a proprietary enzymatic DNA synthesis platform leveraging terminal deoxynucleotidyl transferase (TdT) to enable template-free synthesis. Ansa Biotechnologies and Nuclera are also emerging contributors developing bio-electronic chip systems for on-demand DNA writing and reading. On the sequencing and retrieval side, Oxford Nanopore Technologies offers portable nanopore-based sequencing chips that are increasingly evaluated for integration into DNA storage retrieval pipelines. Pacific Biosciences (PacBio) brings long-read single-molecule sequencing capabilities relevant to high-fidelity data decoding applications. Additionally, startups such as Biomemory and CATALOG are gaining investor attention for scalable DNA archival chip solutions targeting hyperscale data center deployments.

List of Key DNA Data Storage Enablement Chip Companies Profiled

- Microsoft Corporation

- Twist Bioscience Corporation

- Illumina, Inc.

- Intel Corporation

- Catalog Technologies, Inc.

- DNA Script

- Iridia, Inc.

- Molecular Assemblies, Inc.

- Ansa Biotechnologies

- Nuclera

- Oxford Nanopore Technologies

- Pacific Biosciences of California, Inc. (PacBio)

- Biomemory

- University of Washington (DNA Storage Research Program)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Application-Specific Integrated Circuits (ASICs) represent the leading chip type in the DNA data storage enablement market, owing to their purpose-built architecture optimized for high-throughput oligonucleotide synthesis and sequencing operations.

|

| By Application |

|

Data Archival and Long-Term Storage stands as the dominant application segment, driven by the critical need for ultra-dense, energy-efficient solutions capable of preserving vast quantities of cold data over extended periods.

|

| By End User |

|

Cloud Service Providers and Hyperscalers represent the most influential end-user segment, as these organizations face the greatest urgency in identifying scalable, cost-effective alternatives to conventional data center storage infrastructure.

|

| By Synthesis Technology |

|

Enzymatic Synthesis Chips are emerging as the leading segment within this category, reflecting a broader industry shift toward biologically compatible, scalable synthesis approaches that overcome the throughput and chemical waste limitations of traditional phosphoramidite methods.

|

| By Integration Level |

|

System-on-Chip (SoC) Integrated Solutions are gaining strong traction as the preferred integration model for next-generation DNA data storage systems, consolidating synthesis control, sequencing interface, error correction logic, and data encoding functions within a unified chip architecture.

|

Regional Analysis: DNA Data Storage Enablement Chip Market

North America

The United States anchors North America’s dominance in DNA Data Storage Enablement Chip Market through its dense network of research universities, national laboratories, and pioneering biotech firms. Public and private investments continue to accelerate the translation of laboratory-scale DNA synthesis and sequencing techniques into commercially viable chip architectures, positioning the country at the frontier of this transformative technology.

Canada plays a complementary yet strategically significant role within the North American DNA data storage enablement chip landscape. Canadian research institutions specializing in photonics, nanomaterials, and quantum biology contribute enabling technologies that feed into broader chip development efforts. Government-backed innovation programs and cross-border academic collaborations further strengthen Canada’s position as a valuable regional partner.

North America’s hyperscale cloud infrastructure operators represent a powerful demand catalyst for DNA Data Storage Enablement Chip Market. As exabyte-scale cold data management challenges intensify, leading cloud providers are actively evaluating biological storage architectures. This growing institutional interest is creating measurable pull-through demand for specialized enablement chips designed to interface biological and electronic storage layers seamlessly.

A mature intellectual property protection framework and progressively clarifying regulatory environment for synthetic biology applications provide North American companies in DNA Data Storage Enablement Chip Market with significant competitive advantages. Clear patent pathways encourage sustained R&D investment, while emerging biosafety guidelines specifically addressing engineered nucleic acid systems are being developed with commercial applicability in mind.

Europe

Europe represents the second most advanced region in the global DNA data storage enablement chip market, underpinned by strong academic research traditions and coordinated supranational funding mechanisms. The European Union’s Horizon research programs have channeled significant resources into synthetic biology and nanotechnology convergence projects, several of which directly address the development of biological data encoding and retrieval architectures. Countries such as Germany, the United Kingdom, the Netherlands, and Switzerland are home to leading molecular biology research centers and semiconductor design firms that are progressively aligning their roadmaps with DNA-based computing and storage applications. Europe’s emphasis on data sovereignty and long-term digital preservation of cultural and scientific heritage further amplifies institutional interest in DNA data storage enablement chip technologies. The region’s stringent yet increasingly adaptive regulatory frameworks for biotechnology are evolving to accommodate novel bio-electronic hybrid systems, creating a more permissive environment for applied research and early commercialization. Collaborative public-private partnerships between universities, national research institutes, and technology corporations are accelerating prototype development and helping bridge the gap between academic discovery and market-ready DNA data storage enablement chip solutions across the continent.

Asia-Pacific

Asia-Pacific is emerging as a rapidly ascending force in DNA Data Storage Enablement Chip Market, with China, Japan, South Korea, and Singapore leading regional advancement efforts. China has made DNA data storage a component of its broader national strategy for achieving technological self-sufficiency in advanced data infrastructure, resulting in substantial state-directed investment in synthetic biology and integrated circuit design capabilities. Japan’s precision engineering heritage and South Korea’s world-class semiconductor manufacturing ecosystem provide strong industrial foundations for scaling DNA data storage enablement chip production once technology readiness levels mature sufficiently. Singapore has positioned itself as a regional biotech hub with targeted initiatives attracting global talent and multinational research collaborations in biological data systems. While Asia-Pacific currently trails North America and Europe in fundamental research output within this niche, the region’s manufacturing scale advantages and aggressive government-industry coordination strategies suggest it will play an increasingly prominent role in DNA Data Storage Enablement Chip Market throughout the forecast period and beyond.

South America

South America occupies an early-stage position in the global DNA data storage enablement chip market, with activity currently concentrated in academic research clusters rather than applied commercial development. Brazil leads the region through its network of federal universities and research foundations that engage in molecular biology and bioinformatics, providing a modest but growing knowledge base relevant to DNA-based data systems. Argentina and Chile also harbor emerging biotechnology communities supported by regional science and technology agencies. The primary constraints limiting South America’s advancement in DNA Data Storage Enablement Chip Market include limited access to specialized semiconductor fabrication infrastructure, constrained venture capital availability for deep-tech ventures, and comparatively smaller data economy scales that reduce near-term commercial demand urgency. However, regional interest in biodiversity informatics, agricultural genomics, and scientific data archiving may create niche application pathways that could stimulate localized demand for DNA data storage enablement chip technologies over the longer term.

Middle East & Africa

The Middle East and Africa region currently represents the nascent frontier of the global DNA data storage enablement chip market, with adoption and research activity at the earliest formative stages. The Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing heavily in diversifying their technology economies and have demonstrated growing interest in advanced data infrastructure as part of broader digital transformation agendas. National vision programs in these countries increasingly incorporate synthetic biology and next-generation computing within their long-term technology investment frameworks. South Africa and select North African nations maintain university-based molecular biology programs that provide foundational human capital relevant to the DNA data storage enablement chip field. Despite current market immaturity, the region’s substantial long-term data archiving needs driven by energy sector digitalization, government records management, and expanding cloud infrastructure development could position the Middle East and Africa as a meaningful future growth market for DNA data storage enablement chip solutions as the technology approaches commercial scalability.

Report Scope

This market research report provides a comprehensive analysis of the DNA Data Storage Enablement Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of DNA Data Storage Enablement Chip Market?

-> DNA Data Storage Enablement Chip Market was valued at USD 0.87 billion in 2025 and is projected to grow from USD 0.98 billion in 2026 to USD 3.14 billion by 2034, exhibiting a CAGR of 13.8% during the forecast period.

Which key companies operate in DNA Data Storage Enablement Chip Market?

-> Key players include Twist Bioscience, Illumina, Intel, Microsoft, Catalog Technologies, and University of Washington, among others.

What are the key growth drivers?

-> Key growth drivers include the exponential growth of global data volumes, with the global datasphere projected to reach 175 zettabytes, creating urgent demand for ultra-dense, energy-efficient storage alternatives. Additionally, increasing investment from hyperscale cloud providers and government-backed research programs into next-generation storage infrastructure is accelerating commercialization.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market, driven by leading technology companies and government-backed research investments in next-generation data storage infrastructure.

What are the emerging trends?

-> Emerging trends include automated end-to-end DNA data storage and retrieval platforms, enzymatic oligonucleotide synthesis, hybrid bio-electronic chip architectures, and the development of ASICs and FPGAs engineered specifically for high-density, long-term data archival applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...