Autonomous Driving (Level 3–4) Processor Market Insights

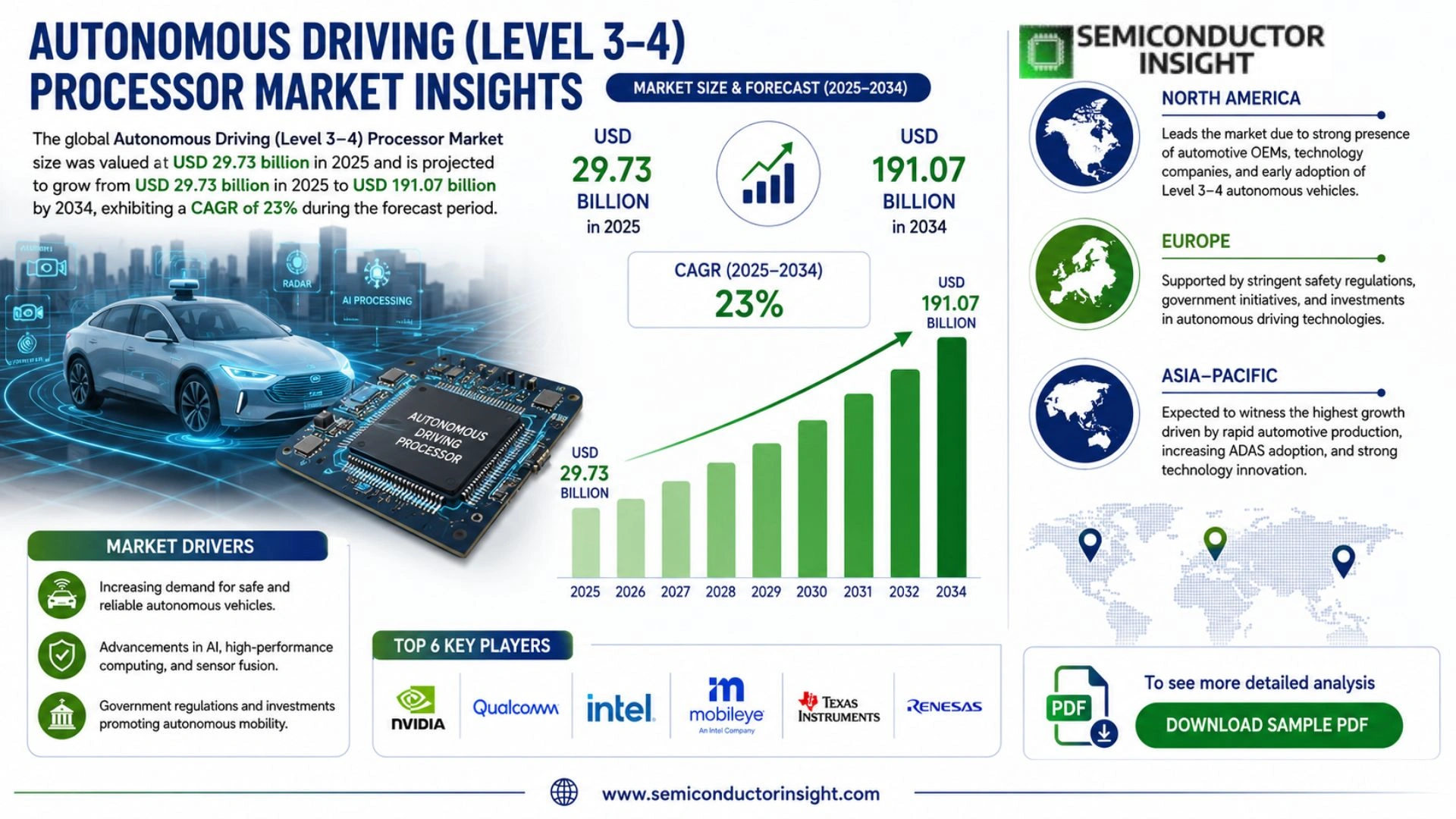

Autonomous Driving (Level 3–4) Processor Market size was valued at USD 29.73 billion in 2025. The market is projected to grow from USD 29.73 billion in 2025 to USD 191.07 billion by 2034, exhibiting a CAGR of 23% during the forecast period.

Autonomous Driving (Level 3–4) processors are specialized high-performance computing chips designed to handle the intensive real-time data processing required for conditional and high automation in vehicles. These processors manage complex tasks including sensor fusion, computer vision, artificial intelligence inference, decision-making algorithms, and path planning, enabling vehicles to operate with minimal or no human intervention in defined scenarios for Level 3 and broader operational domains for Level 4.

The market is experiencing rapid growth due to several factors, including surging investments in autonomous vehicle technology, advancements in AI and semiconductor design, and increasing deployment of advanced driver assistance systems transitioning toward higher automation levels. Additionally, the rising demand for safer and more efficient mobility solutions, coupled with supportive regulatory frameworks in key regions, are contributing to market expansion. Initiatives by the key players in the market are also expected to fuel the market growth. For instance, leading companies continue to innovate with next-generation system-on-chip solutions optimized for power efficiency and computational performance in automotive environments. NVIDIA, Mobileye (Intel), Qualcomm, and others are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Rising Demand for Level 3 and Level 4 Autonomy Features

Autonomous Driving (Level 3/4) Processor Market is experiencing robust growth driven by increasing adoption of conditional and high automation systems in premium and commercial vehicles. Automotive manufacturers are integrating advanced processors to support real-time sensor fusion, computer vision, and decision-making algorithms essential for Level 3 hands-off capabilities and Level 4 geo-fenced operations.

Advancements in AI Computing Power and SoC Designs

Processors delivering 100+ TOPS are becoming standard for Level 4 applications, compared to lower requirements in earlier automation levels. Leading solutions from companies like NVIDIA, Qualcomm, and Mobileye enable efficient handling of complex AI workloads while meeting stringent automotive safety standards such as ISO 26262 ASIL-D.

➤ The global processors for self-driving market is projected to grow significantly, supported by OEM focus on scalable computing platforms for progressive autonomy deployment.

Regulatory support for Level 3 systems in key markets, combined with consumer demand for enhanced safety and convenience features like highway pilot and traffic jam assist, continues to accelerate processor demand in Autonomous Driving (Level 3/4) Processor Market.

MARKET CHALLENGES

Regulatory and Liability Uncertainties

Complex approval processes and varying global regulations for Level 3 and Level 4 systems create deployment delays. Questions around liability during conditional automation handovers remain a significant hurdle for widespread commercialization.

Other Challenges

High Development Costs and Technical Complexity

Designing processors that balance high performance, low power consumption, and functional safety requires substantial R&D investment, limiting market entry for smaller players.

Integration with Multi-Sensor Ecosystems

Ensuring seamless operation with LiDAR, radar, cameras, and HD mapping systems demands sophisticated fusion capabilities, increasing system validation timelines.

MARKET RESTRAINTS

Slower Commercial Rollout of Level 4 Autonomy

Despite technological progress, Autonomous Driving (Level 3/4) Processor Market faces restraints from delayed full commercialization timelines of Level 4 vehicles due to persistent technical, infrastructure, and public acceptance challenges. Many deployments remain in pilot or limited operational design domains.

Supply chain constraints for advanced semiconductor manufacturing and competition for fabrication capacity further moderate near-term growth momentum in high-performance autonomous processors.

MARKET OPPORTUNITIES

Expansion in Commercial and Robotaxi Applications

Level 4 autonomous processors present substantial opportunities in robotaxi fleets, last-mile delivery, and commercial trucking, where operational domains allow for higher utilization rates and faster ROI compared to private vehicles. Emerging markets in Asia-Pacific offer particularly strong potential due to supportive policies and urban mobility needs.

The shift toward software-defined vehicles and centralized computing architectures creates demand for next-generation, scalable processors capable of supporting over-the-air updates and evolving AI models in Autonomous Driving (Level 3/4) Processor Market.

Trends

Advancements in AI-Optimized Semiconductor Architectures

The Autonomous Driving (Level 3-4) Processor Market continues to evolve rapidly as semiconductor manufacturers develop specialized chips capable of handling intensive real-time data processing demands. These high-performance processors integrate advanced capabilities for sensor fusion, computer vision, and AI inference, which are essential for enabling conditional automation in Level 3 systems and broader operational domains in Level 4 vehicles.

Other Trends

Rising Demand for Power-Efficient System-on-Chip Solutions

Automotive manufacturers are prioritizing processors that deliver high computational performance while maintaining energy efficiency suitable for vehicle environments. Leading technology providers are focusing on next-generation designs that optimize power consumption without compromising the ability to execute complex decision-making algorithms and path planning in real time.

Transition from ADAS to Higher Automation Levels

The increasing deployment of advanced driver assistance systems is accelerating the shift toward Level 3 and Level 4 autonomy. This progression requires more sophisticated processors that can manage the growing complexity of environmental perception and vehicle control, driving innovation across the Autonomous Driving (Level 3-4) Processor Market.

Supportive Regulatory Frameworks and Industry Collaborations

Supportive regulatory developments in key regions are facilitating greater adoption of automated driving technologies. These frameworks encourage the integration of robust processing solutions that meet stringent safety and reliability standards. Collaborative initiatives among automotive OEMs and semiconductor companies are further strengthening ecosystem development for higher automation levels.

Focus on Enhanced Safety and Mobility Solutions

Market participants are emphasizing processor technologies that contribute to safer and more efficient mobility. By enabling vehicles to operate with minimal human intervention in defined scenarios, these specialized chips support the broader goals of reducing accidents and improving traffic flow through precise real-time processing.

Strategic Innovations by Key Market Players

Companies such as NVIDIA, Mobileye (Intel), and Qualcomm are advancing their portfolios with optimized solutions for automotive applications. Their ongoing innovations in high-performance computing architectures are setting new benchmarks for processing power and integration in autonomous systems, positioning the Autonomous Driving (Level 3-4) Processor Market for sustained technological progress.

The convergence of artificial intelligence advancements and semiconductor expertise remains central to addressing the computational challenges of higher autonomy levels. As vehicle architectures become more software-defined, demand for versatile and scalable processors is expected to shape competitive dynamics in the sector.

COMPETITIVE LANDSCAPE

Key Industry Players

Autonomous Driving (Level 3–4) Processor Market Competitive Landscape

Autonomous Driving (Level 3–4) Processor Market is led by NVIDIA, which maintains a dominant position through its powerful DRIVE Orin and upcoming Thor platforms. These high-performance SoCs excel in AI inference, sensor fusion, and real-time decision-making, powering solutions for major OEMs and robotaxi developers. The market structure features a concentrated competitive field where a few semiconductor giants control significant share, supported by their ability to deliver scalable, automotive-grade computing solutions amid rising demand for higher autonomy levels.

Other significant players include Mobileye (Intel), Qualcomm, and emerging challengers such as Horizon Robotics and Huawei, which are particularly strong in specific regional markets. These companies focus on differentiated approaches, including vision-centric processing, power-efficient designs, and integrated platforms tailored for Level 3 conditional automation and Level 4 operational domains. Established automotive chip suppliers like NXP Semiconductors, Renesas Electronics, and Texas Instruments also play key niche roles by providing specialized components and cross-domain controllers that complement high-performance processors.

List of Key Autonomous Driving Processor Companies Profiled

- NVIDIA Corporation

- Mobileye (Intel)

- Qualcomm Technologies

- Horizon Robotics

- Huawei Technologies

- NXP Semiconductors

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Infineon Technologies

- STMicroelectronics

- Ambarella Inc.

- Samsung Electronics

- Black Sesame Technologies

- SemiDrive

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC-based Processors dominate due to their superior power efficiency and optimized performance tailored for specific autonomous driving workloads. These chips excel in handling repetitive AI inference tasks with minimal energy consumption, making them ideal for automotive environments where thermal management is critical. Their dedicated architecture supports rapid sensor data processing and real-time decision making while maintaining the reliability required for safety-critical applications. This leads to smoother integration in production vehicles and better overall system stability during extended operations. |

| By Application |

|

Sensor Fusion emerges as the leading application segment given its foundational role in creating a comprehensive environmental model from multiple data sources. Processors in this area must deliver ultra-low latency processing to merge inputs from cameras, LiDAR, radar, and ultrasonic sensors seamlessly. This capability enables more accurate perception in complex driving scenarios, enhancing predictive analytics for safer navigation. Advanced fusion algorithms running on these processors facilitate robust performance under varying weather and lighting conditions, supporting the transition to higher autonomy levels with greater confidence. |

| By End User |

|

Original Equipment Manufacturers (OEMs) represent the primary end user segment as they integrate processors directly into vehicle platforms for mass production. These processors empower OEMs to deliver differentiated autonomous features that enhance brand value and customer safety perceptions. Close collaboration between processor providers and OEMs drives customized solutions that meet stringent automotive-grade reliability standards. This integration supports scalable deployment across vehicle lines, accelerating the adoption of Level 3 and Level 4 capabilities in consumer and commercial markets. |

| By Architecture |

|

Centralized Computing stands out for its ability to consolidate high-performance processing into a single powerful domain controller. This approach simplifies software development and enables more sophisticated AI models to run holistically across all vehicle systems. Centralized architectures provide superior coordination between perception, planning, and control functions, resulting in more coherent autonomous behavior. They also facilitate easier over-the-air updates and future-proofing as computational demands increase with advancing autonomy features. |

| By Integration Level |

|

Integrated SoC Solutions lead by combining multiple processing units, memory, and interfaces on a single chip, reducing system complexity and power draw. This integration enhances reliability through fewer interconnects while delivering the high bandwidth needed for real-time autonomous operations. Such solutions streamline vehicle design and lower overall costs for manufacturers. They support seamless scalability from Level 3 conditional automation to more expansive Level 4 use cases, fostering innovation in efficient, compact hardware designs optimized for the demanding automotive environment. |

Regional Analysis: Autonomous Driving (Level 3-4) Processor Market

Asia-Pacific

Asia-Pacific benefits from concentrated R&D clusters that drive breakthroughs in processor architectures specifically engineered for autonomous driving workloads. These hubs emphasize custom silicon solutions that excel in handling multi-modal sensor data processing while maintaining energy efficiency for extended vehicle operation.

Strong partnerships between processor manufacturers, vehicle OEMs, and research institutions accelerate the customization of chips for regional driving patterns. This collaborative approach ensures that Autonomous Driving (Level 3-4) Processor solutions address specific challenges like mixed traffic flows and diverse weather conditions prevalent in the region.

Established semiconductor fabrication expertise provides a competitive edge in producing high-volume, specialized processors for autonomous applications. This vertical integration supports faster iteration cycles and cost-effective scaling of Level 3-4 technologies across diverse vehicle segments.

North America

North America maintains a significant position in the Autonomous Driving (Level 3-4) Processor Market through its leadership in AI software integration and advanced chip design. The region excels in developing processors that prioritize safety validation and redundant computing architectures critical for higher autonomy levels. Tech giants and automotive innovators collaborate closely to refine edge AI capabilities, enabling processors to manage complex urban driving scenarios with enhanced perception and planning modules. Emphasis on cybersecurity features within processor designs addresses data protection needs in connected autonomous environments, building consumer confidence. Regulatory evolution and pilot programs in select states further stimulate demand for sophisticated processor solutions tailored to Level 3-4 requirements.

Europe

Europe demonstrates strong momentum in the Autonomous Driving (Level 3-4) Processor Market with a focus on ethical AI frameworks and stringent safety standards. The region’s processor development stresses compliance with rigorous functional safety requirements while optimizing for energy-efficient performance in premium vehicles. Collaborative projects across automotive manufacturers and semiconductor firms drive innovations in multi-core architectures capable of real-time environmental interpretation. Emphasis on sustainable mobility aligns processor advancements with broader environmental goals, favoring designs that minimize power consumption without compromising computational power. Strategic initiatives in smart infrastructure support the seamless operation of autonomous systems, enhancing the overall regional ecosystem for Level 3-4 processor adoption.

South America

South America is gradually emerging in the Autonomous Driving (Level 3-4) Processor Market as urbanization drives interest in intelligent transportation solutions. The region focuses on adapting global processor technologies to local infrastructure challenges and diverse geographical conditions. Growing partnerships with international technology providers introduce advanced computing platforms suited for Level 3-4 applications in public transit and logistics. While adoption remains in early stages, increasing awareness of autonomous benefits encourages investment in processor-enabled pilot projects. Local market dynamics emphasize cost-effective implementations that balance performance with regional economic considerations, paving the way for future expansion of autonomous driving capabilities.

Middle East & Africa

The Middle East & Africa region shows promising potential in the Autonomous Driving (Level 3-4) Processor Market, particularly in smart city developments and desert-adapted mobility solutions. Strategic investments in technology infrastructure support the integration of high-performance processors designed for extreme environmental conditions. Focus areas include logistics and premium mobility sectors where Level 3-4 systems can deliver substantial efficiency gains. Regional players are exploring partnerships to localize processor applications, addressing unique challenges such as sandstorms and high temperatures. As digital transformation initiatives progress, the demand for reliable autonomous processors is expected to rise, contributing to diversified growth patterns in the global market.

Report Scope

This market research report provides a comprehensive analysis of the Autonomous Driving (Level 3-4) Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Autonomous Driving (Level 3-4) Processor Market?

-> The Autonomous Driving (Level 3-4) Processor Market was valued at USD 29.73 billion in 2025 and is expected to reach USD 191.07 billion by 2034.

Which key companies operate in Autonomous Driving (Level 3-4) Processor Market?

-> Key players include NVIDIA, Mobileye (Intel), Qualcomm, and others.

What are the key growth drivers?

-> Key growth drivers include surging investments in autonomous vehicle technology, advancements in AI and semiconductor design, and increasing deployment of advanced driver assistance systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include next-generation system-on-chip solutions, AI inference optimization, and power-efficient automotive processors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...