Automotive V2X (C-V2X, DSRC) Chip Market Insights

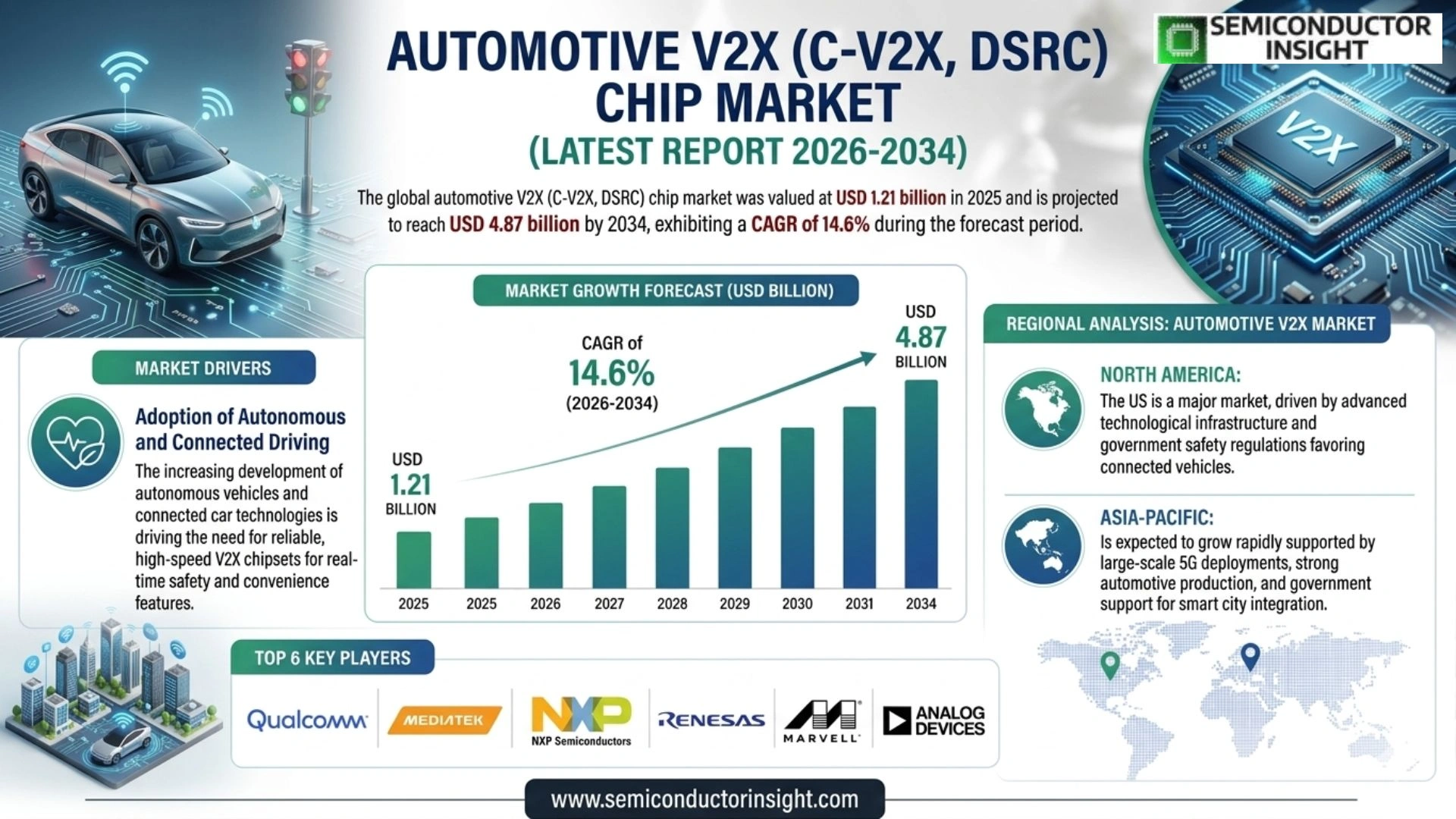

Global Automotive V2X (C-V2X, DSRC) Chip Market size was valued at USD 1.21 billion in 2025. The market is projected to grow from USD 1.42 billion in 2026 to USD 4.87 billion by 2034, exhibiting a CAGR of 14.6% during the forecast period.

Automotive V2X (Vehicle-to-Everything) chips are specialized semiconductor components that enable real-time wireless communication between vehicles and their surrounding environment. These chips support two primary technology standards , Cellular Vehicle-to-Everything (C-V2X), which leverages LTE and 5G cellular networks, and Dedicated Short-Range Communications (DSRC), which operates over the 5.9 GHz spectrum using IEEE 802.11p protocol. Together, they facilitate critical communication modes including Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), and Vehicle-to-Network (V2N) interactions.

The market is witnessing robust expansion driven by accelerating adoption of advanced driver assistance systems (ADAS), growing regulatory mandates for vehicle safety communications, and rapid deployment of smart transportation infrastructure globally. Furthermore, the global push toward autonomous and connected vehicles has significantly elevated demand for high-performance V2X chips capable of ultra-low latency communication. Key industry participants such as Qualcomm Technologies, Inc., NXP Semiconductors N.V., and Autotalks Ltd. continue to drive innovation through strategic partnerships and next-generation chipset development, reinforcing the market’s strong growth trajectory.

MARKET DRIVERS

Rising Government Mandates and Regulatory Push for Connected Vehicle Safety Standards

Regulatory frameworks across major automotive markets are increasingly mandating vehicle-to-everything communication capabilities, acting as a significant catalyst for Automotive V2X (C-V2X, DSRC) Chip Market. In the United States, the Federal Communications Commission has allocated the 5.9 GHz spectrum band specifically for intelligent transportation system applications, providing a dedicated channel for both Cellular Vehicle-to-Everything (C-V2X) and Dedicated Short-Range Communications (DSRC) technologies. The European Union has similarly advanced its cooperative intelligent transport systems directives, compelling automakers to integrate V2X communication modules into new vehicle platforms. These mandates are directly translating into growing chip procurement pipelines for semiconductor manufacturers operating in this space.

Accelerating Autonomous and Semi-Autonomous Vehicle Development Programs

The global push toward higher levels of vehicle autonomy is fundamentally driving demand for advanced V2X chip solutions. Autonomous vehicles require real-time situational awareness that extends beyond onboard sensor capabilities such as LiDAR and radar, making V2X communication an indispensable technology layer. C-V2X chips, in particular, enable vehicles to receive and transmit safety-critical data including road hazard alerts, traffic signal phase and timing information, and pedestrian proximity warnings with ultra-low latency. Leading automotive OEMs and Tier-1 suppliers are actively integrating V2X chipsets into their advanced driver assistance system architectures as a prerequisite for achieving SAE Level 3 and Level 4 autonomy targets.

➤ C-V2X technology, built on the 3GPP standard, offers a clear evolutionary path toward 5G-NR V2X, enabling chipmakers to develop scalable, forward-compatible platforms that serve both current and next-generation connected vehicle ecosystems.

The convergence of 5G network rollout with automotive connectivity requirements is creating a powerful synergy that is directly benefiting Automotive V2X (C-V2X, DSRC) Chip Market. As telecom operators expand 5G coverage along major transportation corridors and urban centers, the viability of C-V2X solutions operating over cellular infrastructure becomes increasingly compelling for automakers. Semiconductor companies are responding with highly integrated system-on-chip designs that combine V2X processing, GNSS positioning, and security engine capabilities within a single package, reducing both cost and footprint while enhancing overall vehicle communication performance.

MARKET CHALLENGES

Ongoing Technology Fragmentation Between C-V2X and DSRC Standards

One of the most persistent challenges confronting Automotive V2X (C-V2X, DSRC) Chip Market is the continued lack of a unified global technology standard. The competition between DSRC, which is based on the IEEE 802.11p protocol, and C-V2X, which is championed by the 3GPP standards body, has created significant uncertainty for automakers, infrastructure operators, and chip developers alike. Different regulatory jurisdictions have adopted divergent positions, with Japan and parts of Europe historically favoring DSRC deployments while the United States and China have increasingly pivoted toward C-V2X. This fragmentation complicates chip design roadmaps, increases development costs, and delays large-scale deployment commitments from major automotive OEMs.

Other Challenges

Cybersecurity and Data Integrity Concerns

The expansion of V2X communication networks introduces substantial cybersecurity vulnerabilities that must be addressed at the chip level. V2X chipsets must incorporate robust hardware security modules, certificate management systems, and cryptographic processing capabilities to authenticate messages and prevent spoofing or replay attacks. Developing and validating these security features adds considerable engineering complexity and time-to-market pressure for semiconductor firms. Standardizing security credential management systems across international borders remains an unresolved technical and governance challenge that continues to slow ecosystem maturation.

High Integration and Validation Costs for Automotive-Grade Chips

Meeting AEC-Q100 automotive-grade qualification requirements for V2X chipsets involves extensive reliability testing across temperature extremes, vibration profiles, and electromagnetic compatibility standards. These qualification processes are resource-intensive and can extend development cycles significantly. For fabless semiconductor companies and new entrants, the capital requirements associated with achieving automotive-grade certification represent a meaningful barrier, potentially limiting competitive diversity in the Automotive V2X chip supply chain over the medium term.

MARKET RESTRAINTS

Insufficient Roadside Infrastructure Deployment Constraining V2X Ecosystem Value

The effectiveness of Automotive V2X (C-V2X, DSRC) chip-enabled communication is inherently dependent on a corresponding deployment of roadside units and smart infrastructure nodes. Without adequate vehicle-to-infrastructure communication endpoints installed at intersections, highway on-ramps, and hazard zones, the practical safety and efficiency benefits of V2X technology remain limited. Public infrastructure investment programs have proceeded at an uneven pace globally, constrained by municipal budget limitations, competing transportation priorities, and the absence of clear interoperability standards. This infrastructure gap is a critical restraint moderating the rate of V2X chip adoption in the near term, as automakers weigh the cost of standard integration against a partially realized communication network.

Cost Sensitivity in Mass-Market Vehicle Segments Limiting Chipset Penetration

While premium and luxury vehicle segments have demonstrated greater willingness to absorb V2X chip integration costs, the high-volume mass-market passenger car segment remains highly price-sensitive. Bill-of-materials pressures on mainstream vehicle platforms make optional or non-mandated connectivity technologies difficult to justify from a cost-benefit perspective for automakers operating on thin margins. The added cost of a dedicated V2X chipset, associated antenna systems, and software stack validation can represent a non-trivial incremental expense per vehicle at scale. Until chip prices decline through volume manufacturing economies and standardization, widespread adoption across entry-level and mid-range vehicle segments will remain constrained, moderating overall market growth trajectories.

MARKET OPPORTUNITIES

Expansion of Smart City Initiatives Creating New V2X Infrastructure Demand Vectors

The accelerating global investment in smart city infrastructure is opening substantial new market opportunities for Automotive V2X (C-V2X, DSRC) chip manufacturers and ecosystem participants. Urban mobility programs in China, South Korea, the European Union, and the United States are incorporating connected intersection management, dynamic traffic signal control, and emergency vehicle preemption systems that rely directly on V2X communication protocols. These programs are creating institutional procurement channels for V2X chipsets beyond the traditional automotive OEM supply chain, expanding the total addressable market for semiconductor companies with proven V2X solutions. Partnerships between chip vendors, infrastructure technology firms, and municipal transportation authorities are emerging as a critical go-to-market pathway.

Transition to 5G-NR V2X Enabling Next-Generation Use Cases and Chip Platform Renewal

The evolution from LTE-based C-V2X to 5G New Radio V2X (NR-V2X) represents a significant product renewal cycle opportunity for the Automotive V2X chip market. 5G NR-V2X supports advanced use cases including sensor data sharing between vehicles, high-definition map updates, and cooperative maneuver planning that are beyond the capability of current-generation chipsets. This technological transition is expected to drive a new wave of design wins and platform upgrades across both automotive OEM and aftermarket channels. Semiconductor companies that establish early 5G NR-V2X chip platforms with demonstrated interoperability and functional safety compliance are well-positioned to capture dominant market share as the ecosystem matures through the latter half of this decade.

Commercial vehicle fleets, including freight trucks, public transit buses, and logistics vehicles, represent an increasingly compelling application segment for V2X chip deployment. Fleet operators stand to derive measurable operational benefits from V2X-enabled platooning, intersection priority signaling, and hazard notification capabilities, creating a business-case-driven adoption pathway that complements regulatory mandates in the passenger vehicle segment. Automotive V2X (C-V2X, DSRC) Chip Market participants that develop ruggedized, cost-optimized chipset solutions tailored to commercial vehicle duty cycles and connectivity requirements are positioned to access a high-volume, recurring procurement market with strong return-on-investment drivers for fleet customers.

Trends

Rising Adoption of C-V2X Technology Over DSRC

Automotive V2X (C-V2X, DSRC) Chip Market is experiencing a significant shift in technology preference, with Cellular Vehicle-to-Everything (C-V2X) increasingly gaining ground over the traditional Dedicated Short-Range Communications (DSRC) standard. C-V2X, which operates over LTE and 5G cellular networks, offers superior range, network scalability, and compatibility with next-generation connected vehicle ecosystems. Automakers and chipset developers are progressively aligning their roadmaps with C-V2X architecture, particularly as 5G infrastructure deployment accelerates across North America, Europe, and Asia-Pacific. This transition is reshaping procurement strategies within the automotive semiconductor supply chain and influencing chipset design priorities across the industry.

Other Trends

Regulatory Mandates Driving V2X Chip Integration

Government regulations and safety mandates are playing a pivotal role in accelerating the integration of V2X communication chips into passenger and commercial vehicles. Regulatory bodies in the United States, European Union, and China have introduced or are advancing frameworks that require vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication capabilities in new vehicle models. These policy-driven requirements are compelling original equipment manufacturers (OEMs) to embed V2X chips at the production stage, directly supporting sustained demand across the Automotive V2X Chip Market.

5G Network Expansion Amplifying C-V2X Chipset Demand

The global rollout of 5G networks is serving as a major catalyst for advanced C-V2X chipset development. Fifth-generation connectivity enables ultra-low latency communication essential for real-time Vehicle-to-Pedestrian (V2P) and Vehicle-to-Network (V2N) interactions. Leading semiconductor companies, including Qualcomm Technologies, Inc. and NXP Semiconductors N.V., are actively developing next-generation chipsets optimized for 5G-based C-V2X deployments. This innovation trend is reinforcing the competitive landscape and elevating performance benchmarks within the broader Automotive V2X (C-V2X, DSRC) Chip Market.

Strategic Collaborations Among Key Industry Players

Strategic partnerships between automotive manufacturers, technology firms, and chipset developers are becoming increasingly common as stakeholders work to accelerate V2X ecosystem maturity. Companies such as Autotalks Ltd. are engaging in collaborative arrangements with Tier-1 automotive suppliers to integrate V2X communication modules into production-ready platforms. These alliances are facilitating faster time-to-market for advanced chipset solutions while enabling the standardization of V2X communication protocols across vehicle classes.

Smart Transportation Infrastructure Supporting Long-Term Market Growth

The expansion of smart city and intelligent transportation system (ITS) initiatives globally is creating a robust demand environment for Automotive V2X (C-V2X, DSRC) chips. Governments and municipal authorities are investing in roadside units (RSUs) and connected infrastructure capable of interfacing with V2X-enabled vehicles. As vehicle-to-infrastructure communication becomes integral to traffic management, emergency response coordination, and road safety optimization, the demand for high-performance V2X chips supporting both C-V2X and DSRC standards is expected to remain strong throughout the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive V2X (C-V2X, DSRC) Chip Market: Competitive Dynamics and Leading Innovators Shaping the Future of Connected Mobility

The Global Automotive V2X (C-V2X, DSRC) Chip Market is characterized by a moderately consolidated competitive structure, with a handful of dominant semiconductor and telecommunications companies commanding significant market share. Qualcomm Technologies, Inc. stands as the foremost leader in the C-V2X chipset segment, leveraging its deep expertise in cellular communications and 5G technology to deliver advanced platforms such as the Snapdragon Auto 5G Modem-RF and its dedicated V2X chipsets. NXP Semiconductors N.V. is another pivotal force, offering comprehensive DSRC and C-V2X solutions that are widely integrated across OEM vehicle platforms globally. Autotalks Ltd., an Israel-based fabless semiconductor company, has emerged as a specialized innovator, producing dedicated V2X chipsets that support both DSRC and C-V2X standards, earning design wins across multiple Tier-1 automotive suppliers. These leading players invest heavily in R&D, strategic collaborations with automakers, and standards-body participation to maintain their technological edge amid intensifying competition and evolving regulatory frameworks across North America, Europe, and Asia-Pacific.

Beyond the market leaders, several niche and regionally significant players are actively contributing to the Automotive V2X chip ecosystem. Ficosa International, Cohda Wireless, and Harman International (a Samsung subsidiary) have developed complementary V2X hardware and software stacks, often partnering with chipset vendors to deliver integrated telematics control units. Continental AG and Robert Bosch GmbH, while primarily Tier-1 automotive suppliers, maintain proprietary V2X module development capabilities built around leading semiconductor platforms. In Asia, companies such as Huawei Technologies and Datang Semiconductor are advancing C-V2X chipset development with strong backing from China’s national connected vehicle initiatives, while LG Electronics and Samsung Electronics contribute to the broader ecosystem through integrated communication modules. Renesas Electronics and STMicroelectronics are also expanding their automotive-grade wireless communication portfolios to include V2X-compatible components, further intensifying competition across the value chain.

List of Key Automotive V2X (C-V2X, DSRC) Chip Companies Profiled

- Qualcomm Technologies, Inc.

- NXP Semiconductors N.V.

- Autotalks Ltd.

- Continental AG

- Robert Bosch GmbH

- Harman International Industries, Inc. (Samsung Electronics Co., Ltd.)

- Cohda Wireless Pty Ltd.

- Ficosa International S.A.

- Huawei Technologies Co., Ltd.

- Datang Semiconductor Technology Co., Ltd.

- LG Electronics Inc.

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Savari Inc.

- Commsignia Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

C-V2X Chips represent the dominant and fastest-evolving technology type in the Automotive V2X chip market, driven by their inherent compatibility with existing LTE and next-generation 5G cellular network infrastructure.

|

| By Application |

|

Vehicle-to-Infrastructure (V2I) emerges as a critical leading application segment, underpinned by rapid global investment in smart transportation infrastructure and intelligent traffic management systems.

|

| By End User |

|

Passenger Vehicles constitute the leading end-user segment within the Automotive V2X chip market, reflecting the large-scale adoption of connected vehicle technologies driven by consumer demand for enhanced safety features and advanced driver assistance systems (ADAS).

|

| By Communication Range |

|

Short-Range Communication leads this segment as the foundational communication mode underpinning both DSRC and direct C-V2X (PC5 mode) interactions, which are essential for time-critical safety applications requiring ultra-low latency.

|

| By Vehicle Autonomy Level |

|

Level 3 (Conditional Automation) vehicles represent the most strategically significant autonomy segment for V2X chip adoption, as this level of automation demands dependable environmental communication to safely manage the complex handoff between automated and human control.

|

Regional Analysis: Automotive V2X (C-V2X, DSRC) Chip Market

Asia-Pacific

China’s regulatory framework mandates C-V2X integration across a rapidly expanding fleet of connected and electric vehicles. State-sponsored road infrastructure upgrades are embedding roadside units capable of communicating with V2X-enabled chips at highway and urban scales. Domestic semiconductor companies are gaining competitive ground by developing chips tailored to China’s specific frequency allocations and network standards, consolidating the country’s strategic leadership in the Automotive V2X Chip Market.

Japan and South Korea contribute sophisticated semiconductor design capabilities and deep OEM integration to the Asia-Pacific V2X landscape. Both nations have established collaborative frameworks between automakers, chipmakers, and telecom operators to ensure seamless V2X communication interoperability. Ongoing investments in 5G-to-vehicle communication trials and cross-border standardization efforts reflect a strategic commitment to ensuring regional V2X chip solutions meet evolving global safety and performance benchmarks.

The proliferation of smart city initiatives across Asia-Pacific creates a highly favorable environment for Automotive V2X (C-V2X, DSRC) Chip Market expansion. Integrated traffic management systems, intelligent intersections, and connected toll infrastructure in countries like Singapore, South Korea, and China serve as catalysts for wider V2X chip adoption. These deployments validate real-world use cases and provide manufacturers with actionable data to refine chip performance and communication reliability.

Asia-Pacific’s vertically integrated automotive supply chains offer a distinct structural advantage in the V2X chip ecosystem. Regional players are investing in indigenous chip design, fabrication partnerships, and software stack development to reduce external dependencies. This localization trend not only accelerates time-to-market for new V2X solutions but also insulates the region’s automotive sector from global semiconductor supply disruptions, strengthening its position within the broader Automotive V2X Chip Market.

North America

North America represents a strategically mature and innovation-intensive region within Automotive V2X (C-V2X, DSRC) Chip Market. The United States has been a foundational market for DSRC technology, with decades of federally funded research underpinning early vehicle-to-infrastructure deployments. However, the regulatory landscape has shifted significantly in favor of C-V2X, prompting automakers, chipmakers, and connectivity solution providers to recalibrate their development roadmaps accordingly. The U.S. Department of Transportation’s continued emphasis on connected vehicle safety programs sustains long-term demand for V2X chip integration. Major automotive hubs in Michigan, California, and Texas are home to both legacy OEMs and emerging mobility technology firms actively deploying V2X-enabled platforms. Canada is also advancing intelligent transportation initiatives that incorporate V2X communication standards. The region’s robust technology investment culture, combined with active collaboration between government agencies, automakers, and semiconductor manufacturers, ensures North America remains a critical contributor to shaping the global trajectory of the Automotive V2X Chip Market through 2034.

Europe

Europe occupies a prominent position in the Global Automotive V2X (C-V2X, DSRC) Chip Market, underpinned by stringent vehicle safety regulations, ambitious connected mobility mandates, and a world-class automotive manufacturing base. The European Union’s C-ITS (Cooperative Intelligent Transport Systems) framework has catalyzed coordinated V2X deployments across member states, with countries such as Germany, France, Sweden, and the Netherlands leading harmonized adoption efforts. European automotive giants are actively integrating V2X chip capabilities into premium and mass-market vehicle lines alike, driven both by regulatory compliance requirements and competitive differentiation imperatives. The region’s emphasis on interoperability between C-V2X and DSRC standards reflects a pragmatic policy posture designed to accelerate market readiness without sacrificing safety performance. European semiconductor suppliers and Tier-1 automotive technology providers are investing in next-generation V2X chip architectures optimized for the continent’s evolving connected road ecosystem, reinforcing Europe’s role as a global standard-setter in the Automotive V2X Chip Market.

South America

South America represents an emerging frontier in Automotive V2X (C-V2X, DSRC) Chip Market, characterized by nascent but growing interest in connected vehicle technologies and intelligent transportation infrastructure. Brazil leads the region in automotive production scale and has begun exploring C-V2X pilot programs in select urban corridors as part of broader smart mobility initiatives. While widespread V2X chip adoption remains constrained by infrastructure investment gaps and regulatory fragmentation across national markets, the region’s expanding middle class, rising vehicle sales, and increasing penetration of connected mobility services are gradually creating conditions favorable to market development. Multinational automakers operating manufacturing facilities in Brazil, Argentina, and Colombia are beginning to introduce V2X-capable vehicle platforms into local lineups, introducing regional consumers and fleet operators to the benefits of vehicle-to-everything communication. As regional governments strengthen digital infrastructure policies and align more closely with global automotive safety standards, South America is expected to progressively increase its participation in the global Automotive V2X Chip Market landscape.

Middle East & Africa

The Middle East & Africa region is at an early but increasingly deliberate stage of engagement with Automotive V2X (C-V2X, DSRC) Chip Market. The Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are channeling significant investment into smart city infrastructure, autonomous mobility pilots, and intelligent transportation systems as part of their national economic diversification agendas. These initiatives create a compelling foundation for V2X chip integration, particularly within controlled urban environments and newly constructed smart districts. South Africa serves as the primary automotive manufacturing hub on the African continent, and while V2X adoption remains limited, growing OEM partnerships and technology transfer agreements are laying groundwork for future deployment. Across the broader region, the expansion of 5G network coverage is an enabling condition that will support C-V2X communication technology rollout in the medium term. As regulatory frameworks mature and infrastructure investment accelerates, the Middle East & Africa region is positioned to emerge as a meaningful growth contributor within the global Automotive V2X Chip Market through the 2026–2034 forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Automotive V2X (C-V2X, DSRC) Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive V2X (C-V2X, DSRC) Chip Market?

-> Global Automotive V2X (C-V2X, DSRC) Chip Market size was valued at USD 1.21 billion in 2025 and is projected to grow from USD 1.42 billion in 2026 to USD 4.87 billion by 2034, exhibiting a CAGR of 14.6% during the forecast period.

Which key companies operate in Automotive V2X (C-V2X, DSRC) Chip Market?

-> Key players include Qualcomm Technologies, Inc., NXP Semiconductors N.V., and Autotalks Ltd., among others, who continue to drive innovation through strategic partnerships and next-generation chipset development.

What are the key growth drivers?

-> Key growth drivers include accelerating adoption of advanced driver assistance systems (ADAS), growing regulatory mandates for vehicle safety communications, rapid deployment of smart transportation infrastructure globally, and the global push toward autonomous and connected vehicles demanding high-performance V2X chips capable of ultra-low latency communication.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America and Europe remain dominant markets, driven by strong regulatory frameworks and early adoption of connected vehicle technologies.

What are the emerging trends?

-> Emerging trends include 5G-enabled C-V2X communication, integration of V2X chips with ADAS platforms, shift from DSRC to Cellular V2X (C-V2X) standards, and the expansion of Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), and Vehicle-to-Network (V2N) communication capabilities across smart transportation ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...