Automotive LIDAR (Flash, MEMS, FMCW) Chip Market Insights

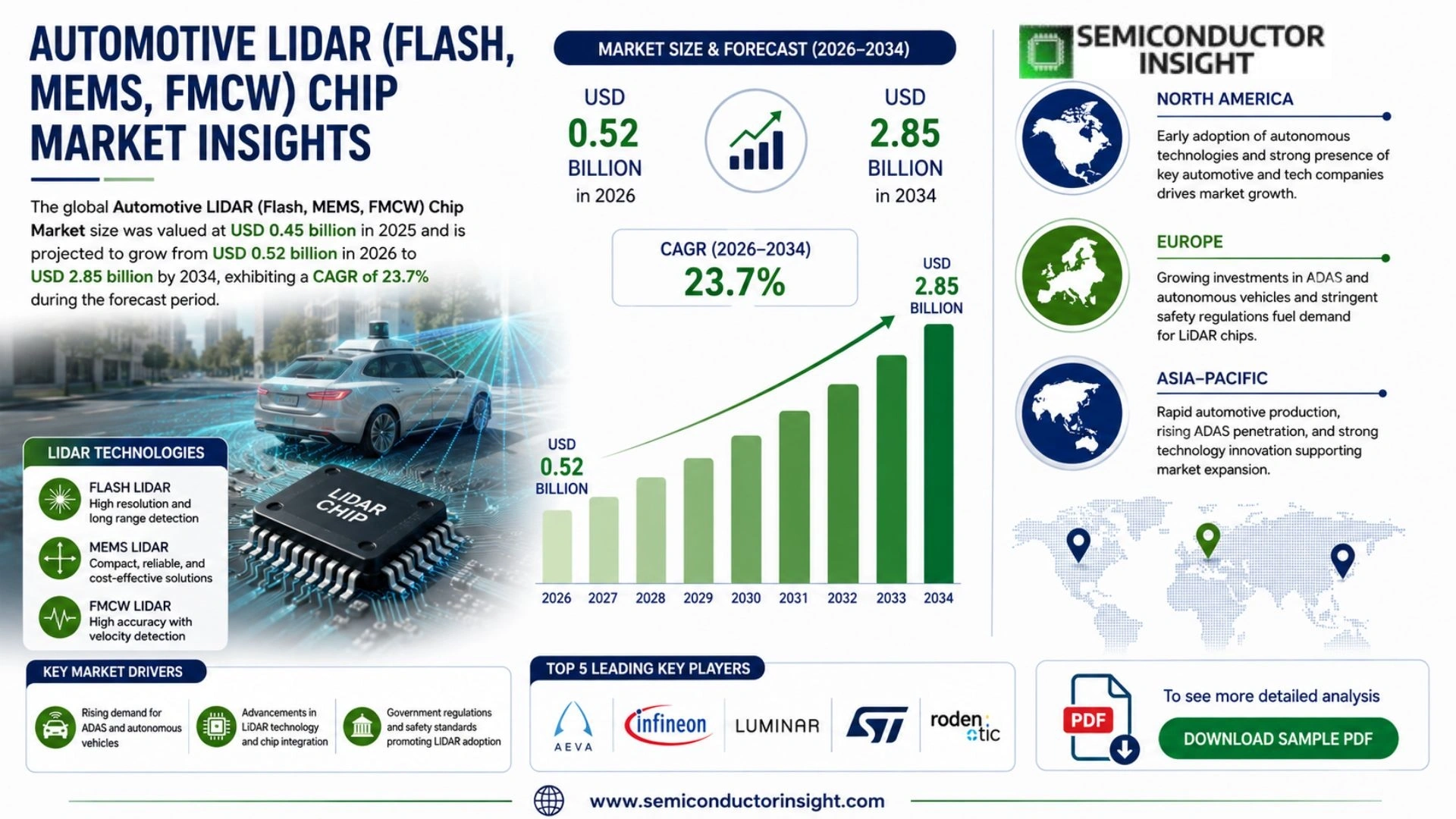

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.52 billion in 2026 to USD 2.85 billion by 2034, exhibiting a CAGR of 23.7% during the forecast period.

Automotive LIDAR chips for Flash, MEMS, and FMCW technologies are specialized semiconductors designed to enable high-resolution 3D sensing critical for advanced driver assistance systems and autonomous vehicles. These chips integrate signal processing, laser control, and data conversion functionalities to support different LiDAR architectures. Flash LIDAR chips facilitate instantaneous scene illumination and capture, MEMS variants provide efficient beam steering through micro-mirrors, while FMCW chips excel in coherent detection for simultaneous range and velocity measurement with superior interference rejection.

The market is experiencing rapid growth due to several factors, including accelerating adoption of Level 3 and higher autonomous driving features, substantial investments in vehicle electrification and safety technologies, and the push toward cost-effective solid-state solutions. Furthermore, advancements in semiconductor fabrication are reducing power consumption and improving integration levels, making these chips more viable for mass-market vehicles. The transition from mechanical to solid-state systems has lowered overall costs significantly, with Flash, MEMS, and FMCW approaches gaining traction for their reliability and compact form factors. Initiatives by key players in the market are also expected to fuel the market growth. For instance, ongoing collaborations focus on silicon photonics integration and next-generation photonic integrated circuits tailored for automotive-grade FMCW and MEMS implementations. Leading companies such as those advancing Aeva-style FMCW platforms, Hesai, and innovators in MEMS scanning maintain wide portfolios that drive competition and technological progress in this dynamic sector.

MARKET DRIVERS

Rising Demand for Advanced Driver Assistance Systems and Autonomous Vehicles

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market is experiencing robust growth driven by the accelerating adoption of Level 3 and higher autonomous driving technologies. OEMs are integrating solid-state LIDAR solutions including Flash, MEMS-based, and FMCW architectures to enable precise 3D environmental mapping and real-time object detection essential for safety-critical applications.

Technological Advancements in Solid-State and Coherent Detection

Continuous innovation in chip-scale integration, particularly silicon photonics for FMCW LIDAR and MEMS beam steering, is reducing size, power consumption, and costs while improving range and velocity measurement capabilities. These advancements support better performance in diverse driving conditions compared to traditional mechanical systems.

➤ Automotive LIDAR shipments reached significant volumes in 2024 with major Chinese OEMs like BYD and Li Auto leading mass-market integration of solid-state solutions.

Supportive government regulations mandating enhanced vehicle safety features and investments in smart mobility infrastructure further propel demand for high-performance Automotive LIDAR (Flash, MEMS, FMCW) Chip solutions across passenger vehicles and commercial fleets.

MARKET CHALLENGES

Complex Integration and Performance Consistency

Integrating Automotive LIDAR (Flash, MEMS, FMCW) Chip technologies into vehicle platforms presents engineering hurdles related to sensor fusion with cameras and radar, thermal management, and maintaining reliable operation across extreme temperatures and environmental conditions.

Other Challenges

High Development Costs

Significant R&D investment is required for automotive-grade qualification, with lengthy validation processes for safety compliance adding to overall program expenses for Flash, MEMS, and FMCW chip solutions.

Supply Chain and Scalability Issues

Achieving high-volume, cost-effective production while ensuring consistent quality and yield for specialized photonic and MEMS components remains a key industry challenge.

MARKET RESTRAINTS

Elevated System Costs and Qualification Barriers

Despite cost reductions in solid-state designs, the initial high pricing of advanced Automotive LIDAR (Flash, MEMS, FMCW) Chip solutions, combined with stringent automotive safety validation requirements, continues to limit broader adoption beyond premium and early-adopter vehicle segments.

Technical complexities in achieving required reliability, eye-safety standards, and interference-free operation in real-world scenarios further restrain faster market penetration for these sophisticated chip technologies.

MARKET OPPORTUNITIES

Photonic Integration and Cost Reduction Pathways

Advances in silicon photonics and hybrid integration for FMCW and MEMS-based LIDAR chips offer substantial opportunities to achieve sub-$500 sensor pricing at volume, enabling deployment across mid-range vehicles and expanding the addressable Automotive LIDAR (Flash, MEMS, FMCW) Chip Market significantly.

The convergence of AI-driven perception software with high-resolution LIDAR data, alongside rising investments in robotaxis and commercial autonomous applications, creates strong growth avenues for specialized chip solutions optimized for performance and efficiency.

Trends

Accelerating Adoption of Solid-State LiDAR Architectures

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market is witnessing significant momentum driven by the transition from mechanical to solid-state systems. Flash LIDAR chips enable instantaneous scene illumination and capture for rapid 3D mapping, while MEMS variants deliver efficient beam steering through micro-mirrors. FMCW chips stand out with coherent detection capabilities that provide simultaneous range and velocity measurement along with superior interference rejection. These specialized semiconductors integrate signal processing, laser control, and data conversion to support advanced driver assistance systems and autonomous vehicles.

Other Trends

Advancements in Semiconductor Fabrication and Integration

Ongoing progress in semiconductor technologies is enhancing the performance of Automotive LIDAR (Flash, MEMS, FMCW) Chip solutions by reducing power consumption and improving overall integration levels. This makes the chips increasingly suitable for mass-market vehicle applications, supporting the broader industry shift toward reliable and compact solid-state designs that prioritize both performance and cost-effectiveness.

Strategic Collaborations Driving Technological Progress

Key players Automotive LIDAR (Flash, MEMS, FMCW) Chip Market are advancing through targeted collaborations focused on silicon photonics integration and next-generation photonic integrated circuits. These efforts particularly benefit automotive-grade FMCW and MEMS implementations, fostering innovation across platforms similar to Aeva-style FMCW approaches and contributions from specialists like Hesai in MEMS scanning technologies. Such partnerships are strengthening competitive dynamics and accelerating the development of high-resolution 3D sensing critical for Level 3 and higher autonomous driving features, while supporting investments in vehicle safety and electrification initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market Competitive Analysis

The Automotive LIDAR chip market for Flash, MEMS, and FMCW technologies is characterized by a dynamic competitive structure dominated by specialized semiconductor innovators and integrated LiDAR system leaders with in-house chip design capabilities. Luminar Technologies stands out as a leading player through its vertical integration strategy, developing proprietary semiconductor components including custom ASICs and photonic integrated circuits optimized for high-performance solid-state LiDAR solutions. The market features a mix of pure-play LiDAR developers advancing application-specific chips and established automotive Tier-1 suppliers leveraging their semiconductor expertise for scalable production. Rapid technological convergence around silicon photonics and advanced signal processing is intensifying competition, with companies focusing on reducing power consumption, enhancing integration, and achieving automotive-grade reliability for mass-market ADAS and autonomous driving applications.

Other significant players include innovators specializing in FMCW coherent detection chips like Aeva, which excels in 4D LiDAR with simultaneous velocity measurement capabilities, alongside MEMS-focused developers such as Hesai Technology and Innoviz Technologies that provide efficient beam-steering semiconductor solutions. Niche contributors are advancing Flash LiDAR architectures and hybrid approaches, supported by collaborations in silicon photonics and photonic integrated circuits. The competitive landscape is further shaped by strategic partnerships between chip designers, LiDAR OEMs, and vehicle manufacturers, driving innovation while addressing cost and performance barriers for broader adoption in Level 3+ autonomous vehicles.

List of Key Automotive LIDAR Chip Companies Profiled

- Luminar Technologies

- Aeva Inc.

- Hesai Technology

- Innoviz Technologies

- Valeo S.A.

- RoboSense

- Ouster Inc.

- Continental AG

- MicroVision

- Cepton Technologies

- LeddarTech

- Quanergy Systems

- Baraja Pty Ltd.

- Opsys Tech Ltd.

- Seyond

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

FMCW LIDAR Chips are gaining prominence for their ability to deliver simultaneous range and velocity measurements through coherent detection. This technology provides superior interference rejection in complex driving environments. It supports robust performance in adverse weather conditions where traditional methods may falter. The integration of advanced signal processing enhances data accuracy for real-time decision making in autonomous systems. |

| By Application |

|

Autonomous Vehicle Navigation represents a critical application area driving innovation in LIDAR chip design. These chips enable precise 3D environmental mapping essential for safe path planning. They facilitate seamless sensor fusion with other vehicle systems for enhanced situational awareness. The demand for high-resolution, real-time data processing pushes continuous improvements in chip efficiency and reliability. |

| By End User |

|

Automotive OEMs are increasingly incorporating these specialized chips to differentiate their vehicle platforms. They prioritize solutions that offer scalability across vehicle models while maintaining automotive-grade reliability standards. Collaboration with chip developers helps tailor solutions to specific platform requirements. This segment emphasizes long-term durability and seamless integration into next-generation vehicle architectures. |

| By Vehicle Type |

|

Passenger Vehicles drive significant demand for compact and cost-effective LIDAR chip solutions. These applications require high-performance sensing in everyday urban and highway scenarios. Manufacturers focus on low-power designs suitable for electric vehicle integration. The emphasis remains on delivering reliable perception capabilities that enhance safety features across diverse driving conditions. |

| By Architecture |

|

Solid-State Solutions are preferred for their durability and lack of moving parts compared to traditional mechanical systems. They enable smaller form factors ideal for seamless vehicle integration. Enhanced semiconductor fabrication techniques improve overall system efficiency and thermal management. This architecture supports the industry shift toward more reliable and scalable autonomous driving technologies. |

Regional Analysis: Automotive LIDAR (Flash, MEMS, FMCW) Chip Market

Asia-Pacific

Asia-Pacific demonstrates superior capabilities in integrating Flash and FMCW LIDAR chip technologies through advanced semiconductor processes. Regional players focus on enhancing detection range and resolution while reducing power consumption, essential for continuous operation in diverse climates. Collaborative R&D efforts drive breakthroughs in hybrid MEMS designs that offer mechanical reliability with solid-state efficiency.

The region benefits from vertically integrated supply chains that streamline production of Automotive LIDAR (Flash, MEMS, FMCW) Chip components. Strong partnerships between wafer fabrication facilities and automotive Tier-1 suppliers ensure consistent quality and rapid iteration. This ecosystem supports cost-effective scaling necessary for widespread adoption across mid-to-premium vehicle segments.

Rapid urbanization and supportive policies propel demand for advanced driver assistance systems incorporating sophisticated LIDAR chips. Local manufacturers prioritize solutions that address challenging traffic scenarios and environmental factors unique to Asian markets, fostering tailored innovations in beam steering and signal processing technologies.

Strategic investments in next-generation fabrication and talent development ensure sustained leadership. The focus remains on achieving higher levels of vehicle autonomy through refined Flash, MEMS, and FMCW LIDAR chip performance, solidifying Asia-Pacific’s pivotal role in global automotive transformation.

North America

North America exhibits strong innovation momentum Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, particularly through pioneering research in Silicon Valley and automotive hubs across the United States and Canada. The region emphasizes software-hardware co-design for enhanced perception capabilities, with companies focusing on robust FMCW architectures suitable for complex urban environments. Strategic collaborations between technology startups and established automakers accelerate the commercialization of high-resolution LIDAR chips. Regulatory frameworks promoting vehicle safety further encourage integration of advanced sensing solutions, while the presence of leading semiconductor design expertise supports rapid prototyping and customization for premium autonomous platforms.

Europe

Europe maintains a significant position Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, driven by stringent safety regulations and a legacy of automotive engineering excellence in Germany, France, and other key nations. The region prioritizes reliability and compliance in MEMS and Flash LIDAR chip development, aligning with comprehensive ADAS and autonomous driving standards. European manufacturers focus on sustainable production methods and seamless integration with existing vehicle architectures. Cross-border initiatives foster knowledge sharing, enhancing capabilities in environmental perception technologies crucial for all-weather performance in varied European climates.

South America

South America is gradually emerging Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, with Brazil and other countries exploring opportunities through technology transfer and localized assembly. The focus centers on adapting global LIDAR solutions to regional infrastructure challenges and cost-sensitive markets. Growing interest in smart mobility solutions encourages partnerships that introduce MEMS-based systems for entry-level autonomous features. While infrastructure development remains key, increasing investments in electric vehicles create a foundation for future demand of affordable LIDAR chip technologies tailored to local transportation needs.

Middle East & Africa

The Middle East and Africa region shows promising potential Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, particularly in Gulf countries investing in futuristic smart cities and autonomous transport initiatives. Efforts concentrate on deploying robust FMCW LIDAR chips capable of handling extreme environmental conditions like high temperatures and dust. Strategic vision programs in nations such as the UAE drive adoption of advanced sensing technologies. Africa presents opportunities through urban mobility projects, with emphasis on cost-effective solutions that can support gradual implementation of LIDAR-enabled safety systems across developing transportation networks.

Report Scope

This market research report provides a comprehensive analysis of the Automotive LIDAR (Flash, MEMS, FMCW) Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive LIDAR (Flash, MEMS, FMCW) Chip Market?

-> Automotive LIDAR (Flash, MEMS, FMCW) Chip Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 2.85 billion by 2034.

Which key companies operate Automotive LIDAR (Flash, MEMS, FMCW) Chip Market?

-> Key players include Aeva, Hesai, and MEMS scanning innovators, among others.

What are the key growth drivers?

-> Key growth drivers include accelerating adoption of Level 3 and higher autonomous driving features, substantial investments in vehicle electrification and safety technologies, and the push toward cost-effective solid-state solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include silicon photonics integration, next-generation photonic integrated circuits, and advancements in semiconductor fabrication for lower power consumption.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...